Table of contents

- Introduction

- Data sources

- Quality issues

- Results

- Conclusion

- Authors and acknowledgement

- References

- Links to related statistics

- Annex 1: Sections and divisions in the 2007 Standard Industrial Classification (SIC 2007)

- Annex 2: Share of approximate gross value added (aGVA) for firms sampled in two consecutive years of the Annual Business Survey (ABS) as a proportion of total UK aGVA from the ABS population

- Annex 3: Share of firms in the Annual Business Survey population by employment size

- Annex 4: Share of workers in the Annual Business Survey population by firm size

1. Introduction

The UK’s poor productivity performance since the onset of the economic downturn in 2008 is unprecedented in post-war economic history. Understanding this “productivity puzzle” has been an important priority for the research and policy communities, as productivity growth is a driver of economic growth and welfare gains in the long run. This article contributes to this debate and presents new labour productivity analysis using data from the Annual Business Survey (ABS) for the period 2006 to 2015. This is an extension of a series of releases on firm-level productivity, the last of which covered the period 2008 to 2012 (Franklin and Murphy, 2014) and draws on previous ONS analysis (ONS 2016). This analysis uses firm-level data from the ABS to deliver more detailed information on recent productivity trends for a variety of business characteristics and groups, than available from the Productivity statistical bulletin. These detailed analyses can shape our understanding of how the aggregate economy is driven by the performance of particular industries or groups of businesses, and also how certain industries perform relative to others.

In this release for the first time, we combine the Annual Business Surveys of Great Britain and Northern Ireland to present productivity analysis that covers the UK as a whole. We also extend our most recent work to present results prior to 2008, resolving problems related to the change in industrial classification from the 2003 to the 2007 Standard Industrial Classification1. Lastly, in this release, we go beyond comparing levels and growth rates of labour productivity, to analyse the distribution and composition of firms and workers by levels of real productivity and productivity growth.

Our analysis shows that over the period 2006 to 2015, levels of labour productivity in capital-intensive industries remain higher than in labour-intensive ones. However, we find the gap closing, with some services industries having higher productivity levels than manufacturing industries. Over the same period, we find a marginal increase in the share of firms with higher levels of productivity. We also find a modest rate of increase in the share of workers working at more productive firms since the recovery. While the gap in the level of productivity has closed between micro-firms (1 to 9 employment) and medium (50 to 249 employment) or large firms (250 or more employment), this increase has not resulted in a spurring growth in aggregate productivity at the whole economy.

This article is structured as follows: section 2 describes the data sources used for the analysis, section 3 discusses quality issues of the data sources used, and section 4 presents the results of the analysis, including distributions of firms and workers by productivity. The conclusions and next steps are outlined in section 5.

Notes for: Introduction

- This was achieved by converting businesses in earlier years from the 2003 Standard Industrial Classification to the 2007 update, through a probability matching exercise.

2. Data sources

The Annual Business Survey (ABS), formerly the Annual Business Inquiry part 2 (ABI/2) is the main structural business survey conducted by the Office for National Statistics (ONS), which collects business and financial information of firms in the production, construction, distribution and services industries, representing approximately two-thirds of the UK economy1. The ABS is conducted by ONS for businesses in Great Britain, and separately by the Department of Finance Northern Ireland for businesses in Northern Ireland. For the first time, we present detailed analysis in this ABI/ABS labour productivity series that covers businesses in the UK as a whole2. The ABS provided the financial data on turnover, intermediate purchases and “approximate gross value added” (aGVA) for calculating labour productivity for our analysis.

We used employment as our measure of labour input in calculating labour productivity. Employment includes employees and working proprietors, and was obtained from the Inter-Departmental Business Register (IDBR) at the time of sample selection of the ABS. It should be noted that employment from the IDBR is derived from a number of different sources (such as the Business Register Employment Survey (BRES), HM Revenue and Customs (HMRC) records or imputed), and some of the employment information especially for small businesses may be several years old. Despite this limitation, the IDBR is at present the most comprehensive source of employment information for firm-level analysis due to its coverage. Accompanying analysis of rural and urban labour productivity uses BRES data, as it offers an advantage below the firm-level.

In this release, we used an experimental set of implied industry deflators to derive constant price gross value added (GVA). These deflators were derived by weighting national accounts product level deflators to industries using the supply-use framework. These experimental deflators are available on the ONS website.

Our measure of labour productivity (GVA per worker) was calculated as aGVA at basic prices over employment. This measure differs from the ONS headline labour productivity measure, which is on an GVA per hour worked basis. Aggregate GVA from the ABS is referred to as aGVA to differentiate from the national accounts measure, of which aGVA is a component. The difference between aGVA and the national accounts measure of GVA is discussed in Ayoubkhani (2014). All data in this article are based on the 2007 Standard Industrial Classification of business activities.

Notes for: Data sources

- The ABS covers the non-financial business economy, which excludes financial services.

- Previous publications in this series used ABI/ABS collected by ONS, covering businesses in Great Britain.

3. Quality issues

The Annual Business Survey (ABS) covers the non-financial business economy of the UK, with partial coverage of firms in financial industries. We therefore exclude industries in section K – financial and insurance activities from our analysis. We also exclude industries in section L – real estate activities, as data for this industry requires further investigation.

The industry deflators used in this analysis were derived from national accounts product deflators. They are therefore consistent with those used to produce national aggregates. There are ongoing reviews of the national accounts deflators, and improvements made to these deflators will result in some changes to the trends shown in the article.

In our analysis of productivity growth, we limit the sample to those firms that are sampled for the ABS for at least two consecutive years, to allow for calculation of firm-level growth rates. These firms tend to be large, as smaller firms are more frequently rotated from the sample. This and the relatively static employment numbers from the Inter-Departmental Business Register (IDBR) for some firms (see section 2) means some caution should be exercised in interpreting the growth rates presented in this article.

Despite these limitations, the analyses presented in this article show patterns that are consistent with the literature and with trends observed at the whole economy level using macro-datasets.

Back to table of contents4. Results

The timeframe for this analysis is 2006 to 2015, and covers the period leading up to the economic downturn, which started in 2008, and the post-recovery period – the latter of which is characterised by relatively stagnant productivity growth known as the “productivity puzzle”. Our results begin by setting out labour productivity at the section and 2-digit industry (division) levels, based on the 2007 Standard Industrial Classification (SIC 2007), before turning to an analysis of productivity trends and distributions across this period.

4.1 Current and constant price productivity for detailed industry groups

Previous work in this series (Goodridge 2007, Long 2010, Franklin and Murphy 2014) showed that in current prices, levels of labour productivity (and growth in constant prices) were higher in capital-intensive industries, that is, production1, than in labour-intensive industries, that is, services. In Table 1, we disaggregate these broad industry groups and find that although this difference still remains, there is considerable variation among lower-level industries. We find that the high productivity levels in the production sector are largely accounted for by non-manufacturing production and in particular the “extraction of crude petroleum and natural gas industry”. However, and more importantly, the levels of productivity in this industry have been in constant decline over the years, partly reflecting the long-term decline in output from the UK’s North Sea oil and gas reserves.

We also observe that the level of productivity in some services industries, notably transport, storage and communication is higher than for manufacturing and closing the gap with non-manufacturing production.

In constant price terms (Table 2) we find that while non-manufacturing production experienced negative average productivity growth (negative 5.6%) in the 9 years to 2015, business services at 2.1% and transport, storage and communication at 1.8% have had relatively stronger productivity growth over this period. Productivity in manufacturing also grew by 2.0% over the same period.

It should be noted that labour productivity in current prices is comparable across industries but they do not distinguish between real productivity and price movements over time. As such, it should not be used to compare year-on-year productivity movements of a single industry over time, but should be used to analyse differences in the productivity levels between industries within the same period. These current price tables should therefore be read vertically. Conversely, labour productivity in constant prices has been deflated to account for relative price changes over time. These data should be read horizontally and show productivity movements of single industries over time, as well as how different industries fared over the same period.

Table 1: Gross value added (GVA) per worker by broad industry groups in current prices, UK, 2006 to 2015

| £, thousands | |||||||||||

| Sector | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | |

| UK, Whole Economy | 40 | 42 | 43 | 40 | 43 | 44 | 44 | 46 | 49 | 51 | |

| Non-Manufacturing Production | 197 | 199 | 216 | 187 | 180 | 182 | 172 | 166 | 155 | 144 | |

| Manufacturing | 48 | 53 | 55 | 51 | 60 | 63 | 63 | 65 | 65 | 67 | |

| Construction | 51 | 53 | 56 | 48 | 50 | 54 | 58 | 61 | 66 | 68 | |

| Services: Distribution, hotels and restaurants | 29 | 30 | 30 | 28 | 30 | 29 | 28 | 30 | 34 | 35 | |

| Services: Transport, storage, and communication | 59 | 65 | 65 | 63 | 68 | 69 | 72 | 74 | 77 | 83 | |

| Services: Business | 38 | 43 | 45 | 43 | 46 | 48 | 48 | 53 | 56 | 57 | |

| Services: Other | 18 | 18 | 18 | 19 | 20 | 20 | 19 | 21 | 23 | 25 | |

| Source: Annual Business Survey (ABS), Inter-Departmental Business Register (IDBR) – Office for National Statistics (ONS) | |||||||||||

| Notes: | |||||||||||

| 1. Key: | |||||||||||

| Non-Manufacturing Production equals Section A (Agriculture, Forestry and Fishing), B (Mining and Quarrying), D (Electricity, Gas, Steam and Air Conditioning Supply) and E (Water Supply; Sewerage, Waste Management and Remediation Activities). | |||||||||||

| Manufacturing equals Section C (Manufacturing). | |||||||||||

| Construction equals Section F (Construction). | |||||||||||

| Services: Distribution, hotels and restaurants equals Sections G (Wholesale and Retail Trade; Repair of Motor Vehicles and Motorcycles) and I (Accommodation and Food Service Activities). | |||||||||||

| Services: Transport, storage, and communication equals Sections H (Transportation and Storage) and J (Information and Communication). | |||||||||||

| Services: Business equals Sections M (Professional, Scientific and Technical Activities) and N (Administrative and Support Service Activities). | |||||||||||

| Services: Other equals Sections P (Education), Q (Human Health and Social Work Activities), R (Arts, Entertainment and Recreation) and S (Other Service Activities). | |||||||||||

Download this table Table 1: Gross value added (GVA) per worker by broad industry groups in current prices, UK, 2006 to 2015

.xls (31.2 kB)

Table 2: Gross value added (GVA) per worker by broad industry groups in 2015 constant prices, UK, 2006 to 2015

| £, thousands | |||||||||||

| Sector | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | Mean growth (%) |

| UK, Whole Economy | 48 | 49 | 47 | 44 | 46 | 45 | 44 | 46 | 48 | 51 | 0.7 |

| Non-Manufacturing Production | 247 | 244 | 210 | 194 | 174 | 154 | 147 | 141 | 138 | 144 | -5.6 |

| Manufacturing | 57 | 61 | 60 | 54 | 63 | 63 | 62 | 63 | 64 | 67 | 2.0 |

| Construction | 61 | 61 | 62 | 53 | 57 | 61 | 63 | 64 | 67 | 68 | 1.4 |

| Services: Distribution, hotels and restaurants | 34 | 35 | 33 | 31 | 31 | 30 | 28 | 29 | 33 | 35 | 0.5 |

| Services: Transport, storage, and communication | 71 | 76 | 74 | 71 | 75 | 74 | 75 | 75 | 78 | 83 | 1.8 |

| Services: Business | 47 | 49 | 49 | 46 | 48 | 50 | 49 | 53 | 57 | 57 | 2.1 |

| Services: Other | 23 | 22 | 22 | 22 | 22 | 22 | 20 | 22 | 23 | 25 | 1.0 |

| Source: Annual Business Survey (ABS), Inter-Departmental Business Register (IDBR) – Office for National Statistics (ONS) | |||||||||||

| Notes: | |||||||||||

| 1. Key: | |||||||||||

| Non-Manufacturing Production equals Section A (Agriculture, Forestry and Fishing), B (Mining and Quarrying), D (Electricity, Gas, Steam and Air Conditioning Supply) and E (Water Supply; Sewerage, Waste Management and Remediation Activities). | |||||||||||

| Manufacturing equals Section C (Manufacturing). | |||||||||||

| Construction equals Section F (Construction). | |||||||||||

| Services: Distribution, hotels and restaurants equals Sections G (Wholesale and Retail Trade; Repair of Motor Vehicles and Motorcycles) and I (Accommodation and Food Service Activities). | |||||||||||

| Services: Transport, storage, and communication equals Sections H (Transportation and Storage) and J (Information and Communication). | |||||||||||

| Services: Business equals Sections M (Professional, Scientific and Technical Activities) and N (Administrative and Support Service Activities). | |||||||||||

| Services: Other equals Sections P (Education), Q (Human Health and Social Work Activities), R (Arts, Entertainment and Recreation) and S (Other Service Activities). | |||||||||||

Download this table Table 2: Gross value added (GVA) per worker by broad industry groups in 2015 constant prices, UK, 2006 to 2015

.xls (31.7 kB)4.2. Industry rankings in terms of gross value added (GVA) per worker, 2006 to 2015

Table 3 presents the top five and bottom five industries in terms of labour productivity (GVA per worker) in current prices. The data show that the difference in current price GVA per worker between the highest and lowest industries has been closing since 2008.

Table 3: Top and bottom five industries in terms of gross value added (GVA) per worker in current prices, UK, 2006 to 2015

| Top five | ||||||||||||

| Rank | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | ||

| Top | Industry | 6 | 6 | 6 | 6 | 6 | 6 | 6 | 6 | 6 | 6 | |

| GVA/Employment (£,000) | 1,901 | 1,859 | 2,565 | 1,566 | 1,668 | 2,012 | 1,464 | 1,126 | 727 | 480 | ||

| 2 | Industry | 37 | 19 | 60 | 35 | 36 | 36 | 36 | 36 | 36 | 60 | |

| GVA/Employment (£,000) | 237 | 235 | 246 | 219 | 212 | 216 | 252 | 255 | 253 | 329 | ||

| 3 | Industry | 35 | 36 | 36 | 36 | 19 | 19 | 19 | 35 | 35 | 19 | |

| GVA/Employment (£,000) | 306 | 299 | 290 | 255 | 163 | 130 | 117 | 182 | 181 | 297 | ||

| 4 | Industry | 19 | 35 | 35 | 60 | 21 | 60 | 60 | 60 | 60 | 36 | |

| GVA/Employment (£,000) | 204 | 201 | 204 | 172 | 194 | 204 | 189 | 173 | 169 | 241 | ||

| 5 | Industry | 36 | 50 | 9 | 19 | 35 | 21 | 35 | 11 | 50 | 37 | |

| GVA/Employment (£,000) | 157 | 142 | 180 | 161 | 176 | 172 | 187 | 145 | 158 | 204 | ||

| Bottom five | ||||||||||||

| Rank | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | ||

| 5 | Industry | 1 | 94 | 56 | 56 | 56 | 56 | 56 | 56 | 85 | 81 | |

| GVA/Employment (£,000) | 13 | 14 | 16 | 15 | 17 | 18 | 18 | 18 | 19 | 21 | ||

| 4 | Industry | 81 | 81 | 94 | 94 | 85 | 85 | 94 | 94 | 94 | 85 | |

| GVA/Employment (£,000) | 11 | 13 | 15 | 14 | 16 | 16 | 15 | 17 | 18 | 20 | ||

| 3 | Industry | 88 | 88 | 88 | 85 | 94 | 94 | 85 | 85 | 56 | 56 | |

| GVA/Employment (£,000) | 10 | 10 | 11 | 11 | 15 | 12 | 13 | 16 | 18 | 19 | ||

| 2 | Industry | 85 | 85 | 85 | 88 | 88 | 88 | 88 | 88 | 88 | 88 | |

| GVA/Employment (£,000) | 8 | 9 | 10 | 10 | 10 | 9 | 9 | 11 | 11 | 13 | ||

| Bottom | Industry | 91 | 91 | 91 | 91 | 91 | 91 | 91 | 91 | 91 | 91 | |

| GVA/Employment (£,000) | 4.7 | 7.1 | 0.2 | 1.6 | 2.1 | 1.1 | -0.1 | 3.6 | 3.9 | 7.5 | ||

| Source: Annual Business Survey (ABS), Inter-Departmental Business Register (IDBR) – Office for National Statistics (ONS) | ||||||||||||

| Notes: | ||||||||||||

| 1. See Annex 1 for industry key. | ||||||||||||

| 2. Labour productivity in current prices is comparable across industries but does not distinguish between price movements over time. As such, it should not be used to compare year on year productivity movements of a single industry over time, but should be used to analyse differences in the productivity levels between industries within the same period. These current price tables should therefore be read vertically. | ||||||||||||

Download this table Table 3: Top and bottom five industries in terms of gross value added (GVA) per worker in current prices, UK, 2006 to 2015

.xls (33.3 kB)Accounting for price changes in the measure of GVA, Table 4 presents GVA per worker at the 2-digit industry level in 2015 constant prices. This allows us to compare how different industries fared over time. We observe that for most of the period 2006 to 2015, there was little change in the top three industries in terms of GVA per worker, with the “extraction of crude petroleum and natural gas” industry outperforming all others. Some of the volatility observed in this detailed constant price series could be linked to the deflators used and our use of single rather than the preferred double deflation method.

Table 4: Top and bottom five industries in terms of gross value added (GVA) per worker in 2015 constant prices, UK, 2006 to 2015

| Top five | |||||||||||

| Rank | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | |

| Top | Industry | 6 | 6 | 6 | 6 | 6 | 6 | 6 | 6 | 6 | 6 |

| GVA/Employment (£,000) | 1847 | 1757 | 1706 | 1375 | 1104 | 977 | 707 | 552 | 412 | 480 | |

| 2 | Industry | 37 | 35 | 36 | 36 | 36 | 36 | 36 | 36 | 36 | 60 |

| GVA/Employment (£,000) | 356 | 300 | 290 | 255 | 244 | 240 | 266 | 259 | 251 | 329 | |

| 3 | Industry | 35 | 36 | 60 | 35 | 35 | 60 | 60 | 35 | 35 | 19 |

| GVA/Employment (£,000) | 306 | 299 | 286 | 238 | 205 | 207 | 198 | 182 | 181 | 297 | |

| 4 | Industry | 36 | 19 | 35 | 60 | 21 | 35 | 35 | 60 | 60 | 36 |

| GVA/Employment (£,000) | 222 | 247 | 241 | 197 | 191 | 183 | 192 | 181 | 171 | 241 | |

| 5 | Industry | 19 | 50 | 37 | 37 | 60 | 37 | 37 | 50 | 50 | 37 |

| GVA/Employment (£,000) | 218 | 174 | 205 | 183 | 182 | 177 | 157 | 144 | 167 | 204 | |

| Bottom five | |||||||||||

| Rank | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | |

| 5 | Industry | 56 | 94 | 81 | 56 | 56 | 56 | 56 | 56 | 85 | 81 |

| GVA/Employment (£,000) | 21 | 18 | 18 | 17 | 19 | 20 | 20 | 18 | 19 | 21 | |

| 4 | Industry | 81 | 81 | 94 | 94 | 85 | 85 | 94 | 94 | 94 | 85 |

| GVA/Employment (£,000) | 12 | 13 | 17 | 16 | 18 | 17 | 16 | 18 | 18 | 20 | |

| 3 | Industry | 88 | 85 | 88 | 85 | 94 | 94 | 85 | 85 | 56 | 56 |

| GVA/Employment (£,000) | 12 | 12 | 14 | 12 | 17 | 13 | 14 | 16 | 18 | 19 | |

| 2 | Industry | 85 | 88 | 85 | 88 | 88 | 88 | 88 | 88 | 88 | 88 |

| GVA/Employment (£,000) | 11 | 11 | 12 | 12 | 13 | 11 | 10 | 11 | 11 | 13 | |

| Bottom | Industry | 91 | 91 | 91 | 91 | 91 | 91 | 91 | 91 | 91 | 91 |

| GVA/Employment (£,000) | 5 | 8 | 0 | 2 | 2 | 1 | 0 | 4 | 4 | 7 | |

| Source: Annual Business Survey (ABS), Inter-Departmental Business Register (IDBR) – Office for National Statistics (ONS) | |||||||||||

| Notes: | |||||||||||

| 1. See Annex 1 for industry key. | |||||||||||

| 2. Labour productivity in constant prices have been deflated to account for relative price changes over time. These data should be read horizontally and show productivity movements of single industries over time, as well as how different industries fared over the same period. They do not however say anything about the absolute (nominal) levels of productivity between these industries. | |||||||||||

Download this table Table 4: Top and bottom five industries in terms of gross value added (GVA) per worker in 2015 constant prices, UK, 2006 to 2015

.xls (32.3 kB)4.3. Distribution of firms by productivity – GVA per worker, 2006 to 2015

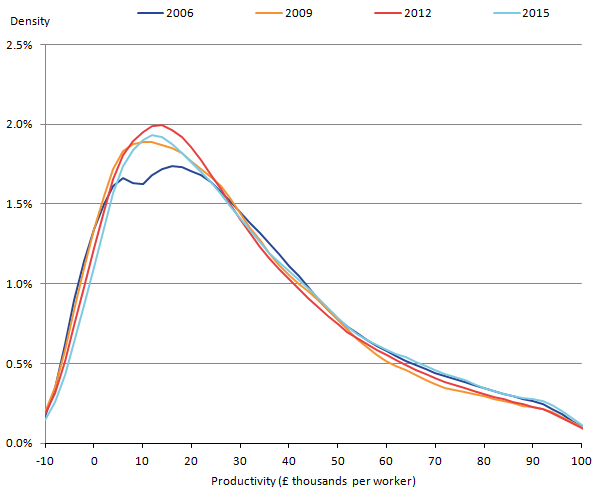

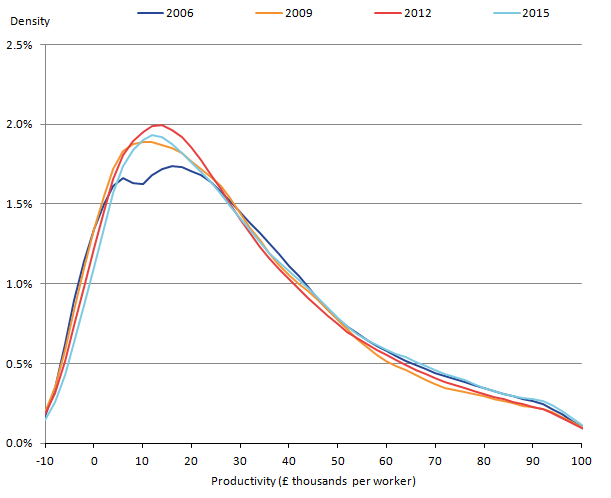

While there are clear differences in labour productivity between industries, analysis of the firm-level data collected as part of the Annual Business Survey (ABS) suggest that there are also considerable differences across firms and within industries. Figure 1 shows the distribution of firms by their productivity in 2015 constant prices. The shape of the distribution indicates a concentration of firms with annual GVA per worker within the £5,000 to £20,000 range, and a gradually falling share of firms with higher levels of productivity as the distribution moves to the right. The left of the distribution shows firms that report higher levels of purchases than their turnover within the year (reflecting operating losses), resulting in negative value added per worker.

For the selected years shown between 2006 and 2015, Figure 1 shows a noticeable rightward shift in the share of firms with negative GVA per worker, indicating the likely impact of unproductive firms ceasing to trade and/or of an improvement in productivity. However, it can be observed that this shift has resulted in greater clustering between the £5,000 to £20,000 GVA per worker region, while only modest gains are observed further right of the distribution where productivity is higher. This modest growth in the share of firms with high productivity is a likely factor in the sluggish rate of aggregate productivity growth in recent years, which defines the “productivity puzzle”.

Figure 1: Distribution of firm-level GVA per worker in constant prices

UK, 2006 to 2015

Source: Annual Business Survey (ABS), Inter-Departmental Business Register (IDBR) – Office for National Statistics (ONS)

Notes:

- Kernal Density, Bandwidth size equals 4.

- Firms can have negative levels of value added per worker in specific periods when they report larger values of purchases than their total turnover.

- Includes all firms covered by the Annual Business Survey (ABS) excluding sections K (Financial and Insurance Activities) and L (Real Estate Activities), weighted to reflect the population of firms.

Download this image Figure 1: Distribution of firm-level GVA per worker in constant prices

.png (23.4 kB) .xls (68.1 kB){kind=link}

As well as the changing distribution of firms illustrated in Figure 1, the ABS data allows us to observe how GVA per worker varies by firm size and how these evolved over the period. Figure 2 shows that in general, medium-sized (50 to 249 employment) and large firms (250 or more employment) have higher productivity levels compared with micro (1 to 9 employment) and small firms (10 to 49 employment). This is consistent with the expectations that the former groups may have more scope to benefit from specialisation of functions and economies of scope and scale.

However, the data show that the decline in the levels of productivity for all size groups except micro-firms began from 2007, prior to the economic downturn. Beyond the trough of the downturn in 2009, micro-firms were the first to register a productivity recovery – in 2012, while the largest businesses (250 or more employment) had a slower recovery and were last to show a noticeable positive productivity improvement in 2014. Furthermore, productivity of micro-firms has seen the second fastest growth since the trough of the downturn in 2009 – outperformed by medium-sized firms, but surpassing productivity levels for small firms and closing the gap with largest firms to some degree. The early productivity recovery of micro-firms could be a result of several factors such as changes to working patterns and practices, or of unproductive firms ceasing to trade – referred to in the literature as the “cleansing effect”2, but is also consistent with micro-firms being more flexible and adaptable in periods of economic shocks.

It should be noted that due to the potential lag in updating employment data especially for small firms on the Inter-Departmental Business Register (IDBR), we may not be allocating firms efficiently across the size groups. Developments in the use of more timely administrative data will help improve this allocation.

Figure 2: Gross value added (GVA) per worker by firm size

UK, 2006 to 2015

Source: Annual Business Survey (ABS), Inter-Departmental Business Register (IDBR) – Office for National Statistics (ONS)

Notes:

- Includes all firms covered by the Annual Business Survey (ABS) excluding sections K (Financial and Insurance Activities) and L (Real Estate Activities), and weighted to reflect the population of workers within each type of firm.

- The share of firms and workers in the size bands presented above can be found in annex 3 and 4.

Download this chart Figure 2: Gross value added (GVA) per worker by firm size

Image .csv .xls4.4. Distribution of workers by their productivity

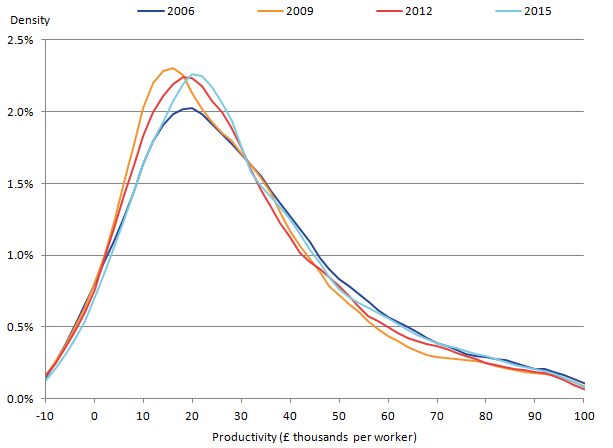

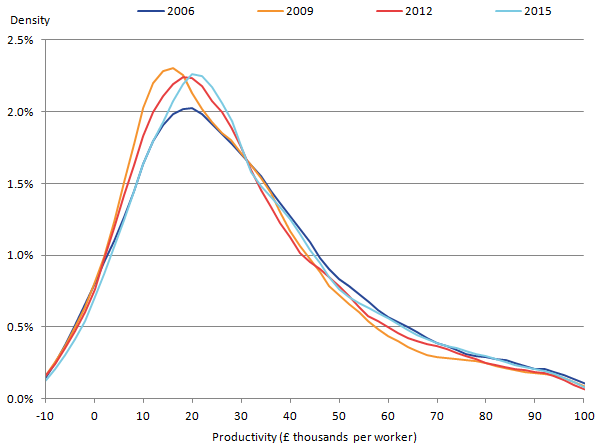

Figure 3 provides a different perspective to the distribution of businesses in Figure 1 by weighting this distribution by their employment, resulting in a distribution of workers by their productivity. In this presentation, each worker is allocated the level of productivity at their firm and given equal weight. Compared with Figure 1, this distribution of workers is more balanced, with greater weight on the right hand side, indicating that more productive firms account for a larger share of workers, and conversely, the share of firms with zero or negative productivity – left tail in Figure 1 – account for a relatively small share of workers.

In this distribution, there is a noticeable mass in the share of workers with productivity of around £20,000, for most of the selected periods shown. The effect of the downturn can be seen in a leftward shift of the mass of the distribution in 2009, then recovering and appearing to shift further to the right in 2015, suggesting an improvement in productivity of the median UK worker in 2015 compared with previous years.

Figure 3: Labour productivity distribution in terms of workers, constant prices

UK, 2006 to 2015

Source: Annual Business Survey (ABS), Inter-Departmental Business Register (IDBR) – Office for National Statistics (ONS)

Notes:

- Kernal Density, Bandwidth size equals 4.

- Firms can have negative levels of value added per worker in specific periods when they report larger values of purchases than their total turnover.

- Includes all firms covered by the Annual Business Survey (ABS) excluding sections K (Financial and Insurance Activities) and L (Real Estate Activities), weighted to reflect the population of workers within firms.

Download this image Figure 3: Labour productivity distribution in terms of workers, constant prices

.png (30.6 kB) .xls (68.1 kB){kind=link}

4.5. Share of firms and workers with zero or negative productivity

The strength of this lower-level analysis is that it permits a more detailed examination of firm-level trends at different points of the productivity distribution. Figure 4 presents one such analysis, showing the share of firms and workers with zero or negative levels of productivity, which are at the left-hand tail of Figures 1 and 3, respectively.

Although the share of firms in this segment is consistently higher than the share of workers in these firms, both show a decline over the period 2006 to 2015 – reflecting firms getting more productive, or less productive firms ceasing to exist. However, the share of firms has declined faster than the share of workers over the same period, with 6.5% of firms and 5.3% of workers having zero or negative GVA per worker in 2015. This is consistent with Figures 1 and 3, which together indicate that many of the most unproductive firms are relatively small in employment terms.

Figure 4: Proportion of firms and workers in firms with zero or negative productivity

UK, 2006 to 2015

Source: Annual Business Survey (ABS), Inter-Departmental Business Register (IDBR) – Office for National Statistics (ONS)

Notes:

- Includes all firms covered by the Annual Business Survey (ABS) excluding sections K (Financial and Insurance Activities) and L (Real Estate Activities), weighted to reflect the population of firms and workers, respectively.

Download this chart Figure 4: Proportion of firms and workers in firms with zero or negative productivity

Image .csv .xls4.6. Industry distribution of top 10% of firms in terms of GVA per worker

The ABS data also allows us to explore in detail the broad industry groups represented by the top 10% of firms in terms of GVA per worker – these are the firms that make up the right-hand tail of the distribution in Figure 1. These highly productive firms consistently represent a broad range of industries across the period 2006 to 2015. In broad terms in each year, around three-quarters of these firms were in services industries, while firms in the remaining quarter were in either production or construction.

At the more detailed industry level, several industries have increased their share within the top 10%. Firms in Professional, Scientific and Technical industries account for 3 in every 10 firms in 2015 up from around 23% in 2006 (Figure 5). This was at the expense of firms in Distribution, hotels and restaurants declining from 16.8% in 2006 to 10.6% in 2015, Other services from 9.2% to 6.7% and Production from 6.7% to 5.8% over the same period.

Figure 5: Industry distribution of the top 10% of firms by productivity

UK, 2006 to 2015

Source: Annual Business Survey (ABS), Inter-Departmental Business Register (IDBR) – Office for National Statistics (ONS)

Notes:

- Includes all firms covered by the Annual Business Survey (ABS) excluding sections K (Financial and Insurance Activities) and L (Real Estate Activities).

- Key:

Production equals Sections A (Agriculture, Forestry and Fishing), B (Mining and Quarrying), C (Manufacturing), D (Electricity, Gas, Steam and Air Conditioning Supply) and E (Water Supply; Sewerage, Waste Management and Remediation Activities).

Construction equals Section F (Construction).

Services: Administration equals Section N (Administrative and Support Service Activities).

Services: Professional equals Section M (Professional, Scientific and Technical Activities).

Services: Distribution, hotels and restaurants equals Sections G (Wholesale and Retail Trade; Repair of Motor Vehicles and Motorcycles) and I (Accommodation and Food Service Activities).

Services: Transport, storage, and communication equals Sections H (Transportation and Storage) and J (Information and Communication).

Services: Other equals Sections P (Education), Q (Human Health and Social Work Activities), R (Arts, Entertainment and Recreation) and S (Oter Service Activities).

Download this chart Figure 5: Industry distribution of the top 10% of firms by productivity

Image .csv .xlsThe distribution of the top 10% of businesses in terms of productivity presented in Figure 5 is somewhat different from the overall distribution of businesses in the ABS population (Figure 6). In 2015 for instance, we observe that businesses in professional, scientific and technical industries, which account for a large share of the top 10% of the most productive firms (30.7%), only account for 20.8% of the overall population of firms. This suggests a concentration of highly productive firms in these industries, also evidenced by their increasing share of the overall population over the period to 2015. In contrast, businesses in distribution, hotels and restaurants account for a larger share of the population, but are less well represented at the top of the productivity distribution. This industry group has a declining share of the population over the same period.

In general, across the industry groups, there seems to be some correlation between growth in the share of top 10% of productive firms and growth in the share of firms in the population for that industry.

Figure 6: Industry distribution of businesses in the ABS population

UK, 2006 to 2015

Source: Annual Business Survey (ABS), Inter-Departmental Business Register (IDBR) – Office for National Statistics (ONS)

Notes:

- Includes all firms covered by the Annual Business Survey (ABS) excluding sections K (Financial and Insurance Activities) and L (Real Estate Activities).

- Key:

Production equals Sections A (Agriculture, Forestry and Fishing), B (Mining and Quarrying), C (Manufacturing), D (Electricity, Gas, Steam and Air Conditioning Supply) and E (Water Supply; Sewerage, Waste Management and Remediation Activities).

Construction equals Section F (Construction).

Services: Administration equals Section N (Administrative and Support Service Activities).

Services: Professional equals Section M (Professional, Scientific and Technical Activities).

Services: Distribution, hotels and restaurants equals Sections G (Wholesale and Retail Trade; Repair of Motor Vehicles and Motorcycles) and I (Accommodation and Food Service Activities).

Services: Transport, storage, and communication equals Sections H (Transportation and Storage) and J (Information and Communication).

Services: Other equals Sections P (Education), Q (Human Health and Social Work Activities), R (Arts, Entertainment and Recreation) and S (Oter Service Activities).

Download this chart Figure 6: Industry distribution of businesses in the ABS population

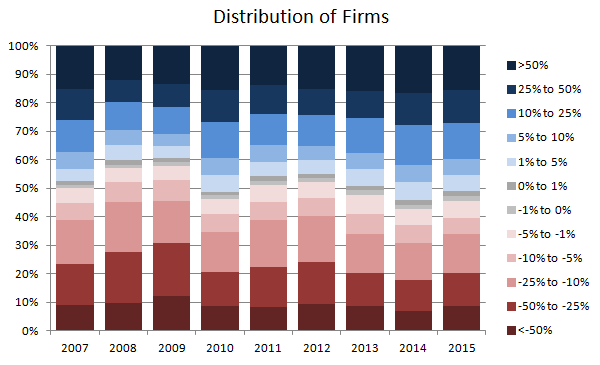

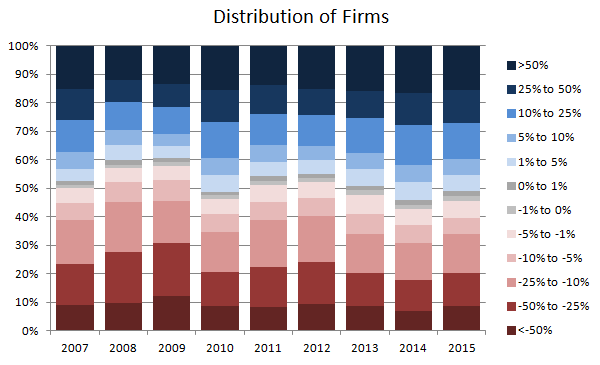

Image .csv .xls4.7. Distribution of firms by growth in GVA per worker

The detailed analysis set out in the previous sections provides some indication of how the distribution of labour productivity has varied in the UK over time. Movements in average UK productivity reflect these changing conditions, and in particular will capture the effects of: (a) the relative productivity of new entrants to the market (firm “births”), (b) the relative productivity of firms which exit (firm “deaths”), and (c) changes in the rates of productivity growth and the market shares of continuing firms. A large academic literature has examined how these different effects have delivered productivity growth over recent years (such as Riley and Bondibene (2016)), often using large administrative datasets (see, for example, Foster, Haltiwanger and Syverson (2008), Garicano, Lelarge and Van Reenen (2016) and Haltiwanger, Jarmin and Miranda (2010)).

Figures 6 and 7 examine one of these effects: the rate of within firm productivity growth. In these charts, we restrict our sample to those businesses that were sampled in two consecutive years of the ABS, and calculate their rates of productivity growth from one period to the next. This enables us to construct a distribution of firm-level productivity, which gives some sense of how widespread changes in labour productivity are within firms. As the ABS is a sample survey rather than an exhaustive administrative dataset, this work necessarily focuses on the panel component of the ABS. These firms who fall into the panel component tend to be large – limiting their representativeness for the business population as a whole – but they account for at least 60% of total UK approximate gross value added (aGVA) in each year (See Annex 2).

Figure 7 shows that in 2007, half (50%) of this population had productivity growth of negative 1% or less. This share reached its peak in 2009, when almost 6 in every 10 firms in this population had productivity growth of negative 1% or less, reflecting the impact of the economic downturn. Since then, the share of firms with such negative productivity growth has declined, but not to a great extent. In 2015, in this population 46% of firms had productivity growth of negative 1% or less. While this is an improvement on 2009, it remains a large share of firms and exemplifies the very modest productivity gains observed at the whole economy level since the recovery.

Figure 7 also highlights the range of productivity outcomes at the firm-level: while a majority of firms experience productivity growth rates of between negative 25% and positive 25%, there are some firms with much more extreme productivity outcomes. This may point to some underlying volatility in the firm-level productivity measures – including the ability of the deflators to adequately capture quality change in services industries – but may also provide some indication of some strong underlying dynamics. Further work is needed to better understand the potential for measurement error and the dynamics of firm growth across different business characteristics – for example, industry, and firm size.

Figure 7: Percentage of firms by their rate of real productivity growth

UK, 2007 to 2015

Source: Annual Business Survey (ABS), Inter-Departmental Business Register (IDBR) – Office for National Statistics (ONS)

Notes:

- The chart uses data from firms which were sampled in two consecutive years of the ABS in order to calculate the growth rates.

Download this image Figure 7: Percentage of firms by their rate of real productivity growth

.png (20.4 kB) .xls (49.7 kB){kind=link}

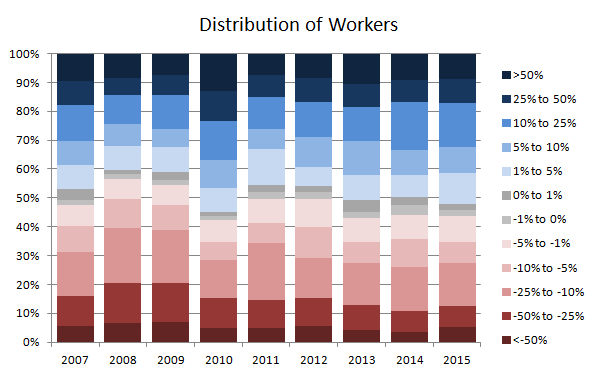

In Figure 8, we present the proportion of workers grouped by the growth rate of real GVA per worker of their firms between 2007 and 2015. Compared with Figure 7, we observe a fall in the prevalence of extreme productivity growth outcomes – consistent with smaller firms experiencing much larger proportional swings in labour productivity. We also observe a reduction of the share of workers in firms with negative productivity growth (of negative 1% or less) over this period, compensated by an increase in the share of workers in firms with positive productivity growth (of 1% and above) over the period. However, since 2013 there seems to be little change in this distribution, with a marginal gain in the proportion of workers in firms with positive productivity growth between 2013 and 2015 at just over 50%.

Figure 8: Percentage of workers by the rate of real productivity growth of their firms

UK, 2007 to 2015

Source: Annual Business Survey (ABS), Inter-Departmental Business Register (IDBR) – Office for National Statistics (ONS)

Notes:

- The chart uses data from firms which were sampled in two consecutive years of the ABS in order to calculate the growth rates.

Download this image Figure 8: Percentage of workers by the rate of real productivity growth of their firms

.png (20.8 kB) .xls (49.7 kB){kind=link}

4.7.1. Percentiles distribution

Figure 9 shows the distribution of real productivity growth by selected percentiles for the period 2007 to 2015. Over this period, there seems to be little evidence of a closing gap in productivity growth rates across the percentiles. The trend shows productivity growth rates declining for all percentiles shown after 2007 as a result of the downturn, with a more pronounced impact on firms at the lower end of the distribution – those in the 10th percentile. In 2010, there was a general recovery with higher productivity growth among the most productive firms – those in the 90th percentile. This increase seems to have tapered off for all percentiles shown, with a slightly downward trend in more recent periods. The rates of growth for all percentiles are almost unchanged in 2015 compared with 2007, with the median firm having zero productivity growth.

Figure 9: Growth of real gross value added (GVA) per worker by percentile

UK, 2007 to 2015

Source: Annual Business Survey (ABS), Inter-Departmental Business Register (IDBR) – Office for National Statistics (ONS)

Notes:

- The chart uses data from firms which were sampled in two consecutive years of the ABS in order to calculate the growth rates.

Download this chart Figure 9: Growth of real gross value added (GVA) per worker by percentile

Image .csv .xlsNotes for: Results

- Production industries include manufacturing and non-manufacturing production.

- Riley, R. et al. (2015) “Productivity dynamics in the wake of the financial crisis: evidence from UK businesses"

5. Conclusion

This article presents analyses of the productivity of businesses in the non-financial business economy of the UK between 2006 and 2015. The scope of this work allows for a comparison of the relative positions and trends of the business environment before and after the economic downturn of 2008.

In general, we find that between 2006 and 2015, firms in more capital-intensive sectors have higher levels of productivity compared with those in labour-intensive service sectors. However, further examination shows certain services industries having higher productivity levels compared with manufacturing industries. We also find over the same period a reduction in the share of firms with zero or negative gross value added (GVA) per worker, and a clustering of firms with labour productivity between £5,000 and £20,000. The data suggests a marginal gain in the share of firms with higher levels of productivity since 2006.

In line with the literature, we find a declining share of workers in firms with zero or negative productivity, possibly reflecting a reallocation of workers to firms with higher levels of productivity. However, we also observe that the increase in the share of workers in firms with the highest levels of productivity has been but modest over the period.

When looking at the distribution of firms for which we could observe their productivity growth, we find a large share of these firms record negative productivity growth in each year, with almost half of the population having negative productivity growth in 2015.

While this analysis is broadly consistent with the literature and the trends observed at the whole economy level, it points to a few areas where further investigation will increase our understanding. Consequently, further work in this area would examine productivity growth in detailed industries and sizes. We also plan to decompose productivity growth between growth in output and the decline in labour input.

Back to table of contents7. References

Ayoubkhani, D. (2014) “A comparison between Annual Business Survey and National Accounts of Value Added”, Office for National Statistics

Foster, L., Haltiwanger, J. and Syverson, C. (2008) "Reallocation, Firm Turnover, and Efficiency: Selection on Productivity or Profitability?" American Economic Review, 98(1): 394-425.

Franklin, M. and Murphy, J. (2014) “Labour Productivity Measures from the ABS: 2008 to 2012”, Office for National Statistics

Garicano, L., Lelarge, C. and Van Reenen, J. (2016) "Firm Size Distortions and the Productivity Distribution: Evidence from France." American Economic Review, 106(11): 3439-79.

Goodridge, P. (2007) “New labour productivity measures from the ABI – 1998 to 2005”, Office for National Statistics

Long, K. (2010) “Labour productivity measures from the ABS: 1998 to 2007”, Office for National Statistics

OECD (2016) “OECD Compendium on Productivity Indicators”

ONS (2015) “Economic Review”, March 2015 Edition

ONS (2016) “Economic Review”, January 2016 Edition

Riley, R., Rosazza Bondibene, C. and Young, G. (2014) "Productivity dynamics in the Great Stagnation: evidence from British businesses". CFM discussion paper series, CFM-DP2014-7. Centre For Macroeconomics, London, UK

Riley, R. and Rosazza Bondibene, C. (2016) “Sources of labour productivity growth at sector level in Britain, after 2007: a firm-level analysis”, Nesta Working Paper No. 16/01

Back to table of contents9. Annex 1: Sections and divisions in the 2007 Standard Industrial Classification (SIC 2007)

A AGRICULTURE, FORESTRY AND FISHING

01 Crop and animal production, hunting and related service activities

02 Forestry and logging

03 Fishing and aquaculture

B MINING AND QUARRYING

05 Mining of coal and lignite

06 Extraction of crude petroleum and natural gas

07 Mining of metal ores

08 Other mining and quarrying

09 Mining support service activities

C MANUFACTURING

10 Manufacture of food products

11 Manufacture of beverages

12 Manufacture of tobacco products

13 Manufacture of textiles

14 Manufacture of wearing apparel

15 Manufacture of leather and related products

16 Manufacture of wood and of products of wood and cork, except furniture; manufacture of articles of straw and plaiting materials

17 Manufacture of paper and paper products

18 Printing and reproduction of recorded media

19 Manufacture of coke and refined petroleum products

20 Manufacture of chemicals and chemical products

21 Manufacture of basic pharmaceutical products and pharmaceutical preparations

22 Manufacture of rubber and plastic products

23 Manufacture of other non-metallic mineral products

24 Manufacture of basic metals

25 Manufacture of fabricated metal products, except machinery and equipment

26 Manufacture of computer, electronic and optical products

27 Manufacture of electrical equipment

28 Manufacture of machinery and equipment not elsewhere classified

29 Manufacture of motor vehicles, trailers and semi-trailers

30 Manufacture of other transport equipment

31 Manufacture of furniture

32 Other manufacturing

33 Repair and installation of machinery and equipment

D ELECTRICITY, GAS, STEAM AND AIR CONDITIONING SUPPLY

35 Electricity, gas, steam and air conditioning supply

E WATER SUPPLY; SEWERAGE, WASTE MANAGEMENT AND REMEDIATION ACTIVITIES

36 Water collection, treatment and supply

37 Sewerage

38 Waste collection, treatment and disposal activities; materials recovery

39 Remediation activities and other waste management services

F CONSTRUCTION

41 Construction of buildings

42 Civil engineering

43 Specialised construction activities

G WHOLESALE AND RETAIL TRADE; REPAIR OF MOTOR VEHICLES AND MOTORCYCLES

45 Wholesale and retail trade and repair of motor vehicles and motorcycles

46 Wholesale trade, except of motor vehicles and motorcycles

47 Retail trade, except of motor vehicles and motorcycles

H TRANSPORTATION AND STORAGE

49 Land transport and transport via pipelines

50 Water transport

51 Air transport

52 Warehousing and support activities for transportation

53 Postal and courier activities

I ACCOMMODATION AND FOOD SERVICE ACTIVITIES

55 Accommodation

56 Food and beverage service activities

J INFORMATION AND COMMUNICATION

58 Publishing activities

59 Motion picture, video and television programme production, sound recording and music publishing

activities 60 Programming and broadcasting activities

61 Telecommunications

62 Computer programming, consultancy and related activities

63 Information service activities

M PROFESSIONAL, SCIENTIFIC AND TECHNICAL ACTIVITIES

69 Legal and accounting activities

70 Activities of head offices; management consultancy activities

71 Architectural and engineering activities; technical testing and analysis

72 Scientific research and development

73 Advertising and market research

74 Other professional, scientific and technical activities

75 Veterinary activities

N ADMINISTRATIVE AND SUPPORT SERVICE ACTIVITIES

77 Rental and leasing activities

78 Employment activities

79 Travel agency, tour operator and other reservation service and related activities

80 Security and investigation activities

81 Services to buildings and landscape activities

82 Office administrative, office support and other business support activities

P EDUCATION

85 Education

Q HUMAN HEALTH AND SOCIAL WORK ACTIVITIES

86 Human health activities

87 Residential care activities

88 Social work activities without accommodation

R ARTS, ENTERTAINMENT AND RECREATION

90 Creative, arts and entertainment activities

91 Libraries, archives, museums and other cultural activities

92 Gambling and betting activities

93 Sports activities and amusement and recreation activities

Contact details for this Article

Related publications

- UK productivity introduction: Oct to Dec 2016

- Labour productivity, UK: October to December 2016

- Quarterly public service productivity (Experimental Statistics): Oct to Dec 2016

- Exploring labour productivity in rural and urban areas in Great Britain: 2014

- International comparisons of UK productivity (ICP), final estimates: 2015

- Labour productivity measures from the Annual Business Survey: 2006 to 2015

- Introducing quarterly regional labour input metrics

- An initial assessment of regional management practices: 2015

You might also be interested in:

- Productivity Measures, Labour productivity measures from the Annual Business Inquiry, estimates for 1998 to 2000

- New labour productivity measures from the Annual Business Inquiry, 1998 to 2005

- Labour Productivity Measures from the Annual Business Inquiry, 1998 to 2007

- Labour productivity measures from the Annual Business Survey, 1998 to 2009

- Labour productivity measures from the Annual Business Survey, 2008 to 2012