Table of contents

- Main points

- Labour productivity

- How to interpret the different measures of productivity published today

- Multi-factor productivity still below the level in 2008

- Missing multi-factor productivity is the biggest contributor to below trend productivity growth

- Unit labour costs growth above 2% for the fifth consecutive quarter compared with a year ago

- Experimental estimates of public service productivity suggest 2018 was the first annual fall since 2010

- Exploring productivity growth for English local enterprise partnerships (LEPs)

- Developing experimental estimates of investment in intangibles

- Opportunity to catch-up on our productivity forum

- Links to related statistics

1. Main points

UK labour productivity in Quarter 4 (Oct to Dec) 2018, as measured by output per hour, fell by 0.1% compared with the same quarter a year ago; this continues a decade of weak productivity growth referred to as the “productivity puzzle”.

Unit labour costs (ULCs), a leading indicator of inflation, grew by 3.1% in the year to Quarter 4 2018, and has averaged 2.1% growth for the previous two years; this increase broadly reflects higher hourly labour cost growth, with relatively little offsetting productivity growth.

Compared with the same quarter in 2017, multi-factor productivity (MFP) in Quarter 4 2018 is estimated to have decreased by 0.6%; this contrasts with trend growth in MFP of around 1% per year prior to the financial crisis.

Our new MFP quarterly estimates for the manufacturing industries show noticeable variation in their multi-factor productivity performance; transport equipment experienced the largest growth in MFP for the period 2007 to 2018.

For Quarter 4 2018 public service productivity decreased by 0.5% compared with the same quarter in 2017, this is despite a relatively strong performance in the latest quarter; in Quarter 4 2018, public service productivity increased by 0.8% on the previous quarter; driven by unusually strong growth in output (1.3%).

2. Labour productivity

Compared with the same quarter a year ago, labour productivity, on an output per hour basis fell by 0.1% in Quarter 4 (Oct to Dec) 2018. This is the second consecutive quarterly fall in labour productivity as estimates for the previous quarter have been revised downwards.

For 2018 as a whole labour productivity grew by 0.5% compared with the previous year, which is well below the annual average of 2% experienced before the 2008 economic downturn.

Figure 1: Productivity, as measured by output per hour, was 18.3% beneath its pre-downturn trend, UK

Seasonally adjusted, Quarter 4 (Oct to Dec) 2018

Source: Office for National Statistics

Download this chart Figure 1: Productivity, as measured by output per hour, was 18.3% beneath its pre-downturn trend, UK

Image .csv .xlsOutput per hour in the services industries compared with the same period a year ago, increased by 0.4% in the latest quarter (Quarter 4 (Oct to Dec) 2018), with output increasing faster than hours worked. In manufacturing over the year labour productivity fell by 1.1%, with both output and hours worked falling.

Back to table of contents3. How to interpret the different measures of productivity published today

We now publish labour productivity, multi-factor productivity and public service productivity for the same time period. But how do these different estimates relate to one another, and importantly where do they differ?

The economy, and therefore productivity measures, can be sub-divided into “market sector” and “non-market sector” components. The market sector encompasses all activity where output is sold for economically meaningful prices – this is primarily the private sector, but also includes public corporations, which, despite being publicly owned, operate for profit. The market sector produces around 80% of total output in the economy, while the non-market sector (primarily government, but also non-profit institutions, such as charities) makes up the remaining 20%.

Table 1 compares the market and non-market sector along with their relative weights.

Experimental multi-factor productivity estimates are only calculated for the market sector due to challenges in measuring inputs and output in the non-market sector. Growth accounting de-composes the growth in market sector output per hour into that attributable to changes in: labour composition (the skills of the workforce), capital deepening (capital per hour worked) and multi-factor productivity (a residual, encompassing spillovers and improvements in technology).

However, public service productivity estimates, as published alongside this release, are different to those for the non-market sector in Table 1. Public service productivity is precisely named, as it measures the productivity of providing public services, not the productivity of the public sector; these differences were explained in more detail in October's productivity economic commentary. This means the public service productivity estimate should not be expected to align to that of the non-market sector, as it includes some market sector activity.

| Sector | Share of the economy | UK labour productivity in Quarter 4 (Oct to Dec) 2018 (quarter on a year ago) % |

|---|---|---|

| Whole Economy | 100% | -0.1 |

| Market sector | c80% | -0.3 |

| Non-market sector | c20% | 0.6 |

Download this table Table 1: UK labour productivity by sector of the economy

.xls .csvNotes for: How to interpret the different measures of productivity published today

- The estimate for productivity growth for the market sector is not fully consistent with that used in our multi-factor productivity (MFP) estimates, which differs from those in our labour productivity bulletin due to differences in methods and calculation. We intend to align these in future.

4. Multi-factor productivity still below the level in 2008

In Quarter 4 (Oct to Dec) 2018, multi-factor productivity (MFP) in the UK market sector is estimated to have decreased by 0.6% compared with the same quarter in 2017.

Estimates of MFP augment our labour productivity estimates by taking account of movements in productive capital (such as machinery and software) and compositional developments in the labour market (for example, an increase in the number of workers with university degrees), as well as hours worked. This is explained in our simple guide to MFP.

More than 10 years on, since the 2008 financial crisis, labour productivity (as measured by output per hour worked) is only just ahead of its level at the end of 2007 and MFP is still 4 percentage points lower, having grown only slowly and intermittently since 2009. This contrasts with trend growth in MFP of over 1% per year prior to the financial crisis.

For the first time this quarter, we have provided more granular estimates for the manufacturing industry. This is part of our development plan to expand our statistics to encompass 64 separate industries. We will decide on the level of granularity of the published estimates based on careful assessment of the quality of the expanded dataset. Figure 2 shows annual multi-factor productivity (MFP) results for 13 two-letter manufacturing sub-sectors such as CA (food products, beverages and tobacco) and CH (basic metals and metal products).

For the manufacturing industry as a whole, MFP in 2018 was just 0.3% higher than in 2007. But this masks large positive and negative movements in MFP across different sub-sectors. The best performing sub-sector in terms of MFP is CL (transport equipment), while other sub-components with strong positive MFP growth include CE (chemicals and chemical products), CM (other manufacturing), and CI (computer, electronic and optical products). The worst performer in terms of MFP is CF (basic pharmaceutical products and preparations), with CJ (electrical equipment), CH (basic metals and metal products) and CK (machinery and equipment not elsewhere classified) not far behind.

Figure 2: Multi-factor productivity across manufacturing has varied

Decomposition of cumulative growth of output per hour worked, 2007 to 2018, UK, manufacturing sub-sectors and total manufacturing

Source: Office for National Statistics

Notes:

1. CA is: Food products, beverages and tobacco.

2. CB is: Textiles, wearing apparel and leather products.

3. CC is: Wood and paper products and printing.

4. CD is: Coke and refined petroleum products.

5. CE is: Chemicals and chemical products.

6. CF is: Basic pharmaceutical products and preparations.

7. CG is: Rubber and plastic products and non-metallic mineral products.

8. CH is: Basic metals and metal products.

9. CI is: Computer, electronic and optical products.

10. CJ is: Electrical equipment.

11. CK is: Machinery and equipment not elsewhere classified.

12. CL is: Transport equipment.

13. CM is: Other manufacturing.

14. TOTAL C is all manufacturing.

Download this chart Figure 2: Multi-factor productivity across manufacturing has varied

Image .csv .xls5. Missing multi-factor productivity is the biggest contributor to below trend productivity growth

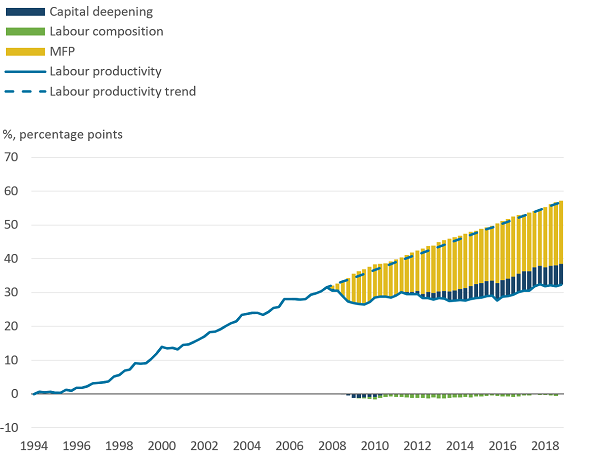

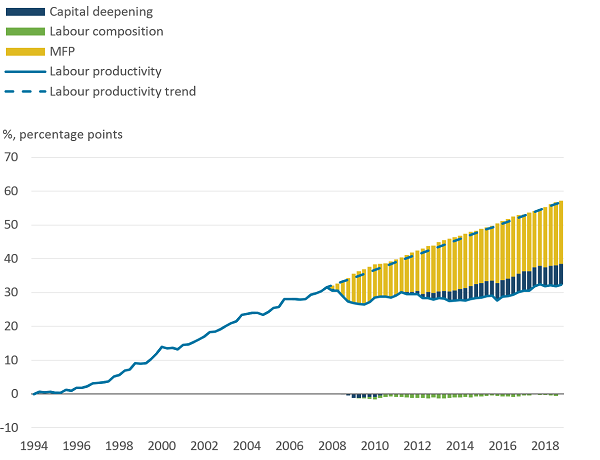

The figure representing the productivity puzzle is well-cited, where output per hour is presented alongside its projected pre-downturn trend. For the first time we have decomposed the gap of market sector labour productivity into contributions from changes in labour composition, capital per hour and the remaining part; multi-factor productivity (MFP). In simple terms, MFP “explains” the portion of growth of labour productivity that cannot be attributed to improvements in capital or labour.

As shown in Figure 3, most of the gap is from MFP, which is still about 4% below the level in 2008, whereas if the pre-downturn trend had continued, MFP would now be about 14% above the level in 2008. In the real world, changes in MFP can arise for several reasons including technological progress, economies of scale, changes in management techniques and business processes or more efficient use of factor inputs. MFP is linked, therefore, not to an increase in the quantity or quality of measured factor inputs but rather to how they are employed. In practice, MFP may also reflect measurement error of inputs and outputs and missing factors of production.

For the most recent periods the weakness in capital services per hour worked relative to its pre-downturn trend also emerges as part of the explanation for the below-trend performance in productivity. Only improving labour composition has kept pace with pre-downturn growth, reflecting continuing growth in the share of hours worked by workers with above-average qualifications.

Figure 3: Multi-factor productivity estimated to be the largest explanation for the productivity gap

Growth in output per hour from 1994 and contribution to productivity gap from 2008, UK market sector

Source: Office for National Statistics

Download this image Figure 3: Multi-factor productivity estimated to be the largest explanation for the productivity gap

.png (43.9 kB) .xlsx (13.9 kB){kind=link}

6. Unit labour costs growth above 2% for the fifth consecutive quarter compared with a year ago

Labour is the largest domestic cost facing most businesses in the UK, and so rising labour costs are an important indicator of domestic inflationary pressures. The extent to which changes in the cost of labour affect companies’ production costs, and hence inflation, depends on growth in unit labour costs (ULCs) — how wages and other labour costs facing companies are growing relative to productivity.

ULCs represent the full labour costs, wages and salaries as well as social security and pension contributions paid by employers, incurred in the production of a unit of output.

ULCs grew by 3.1% in the year to Quarter 4 (Oct to Dec) 2018, following growth of 2.9% in the previous quarter. Following a period of low or negative growth, ULC growth has fluctuated around 2.1% for the past two years. This increase broadly reflects higher hourly labour cost growth, with relatively little offsetting output per hour growth.

Figure 4: Whole economy unit labour costs increased by 3.1% quarter on year ago

Seasonally Adjusted, UK, Quarter 1 (Jan to Mar) 2008 to Quarter 4 (Oct to Dec) 2018

Source: Office for National Statistics

Download this chart Figure 4: Whole economy unit labour costs increased by 3.1% quarter on year ago

Image .csv .xls7. Experimental estimates of public service productivity suggest 2018 was the first annual fall since 2010

Alongside our other measures of productivity, we also publish experimental quarterly measures of total public service productivity. While these are not consistent with our National Statistics annual publication, they offer a more timely measure, in an attempt to address the significant time lag associated with the annual Public service productivity: total, UK, 2016 release.

Compared with the same quarter in the previous year, productivity for total public services decreased by 0.5% in Quarter 4 (Oct to Dec) 2018.

Placing this in the context of a longer time series, Figure 5 combines the experimental quarterly data in this latest release, and the annualised versions of these for 2017 and 2018, with estimates between 1997 and 2016 taken from our latest annual release.

For 2018, public service productivity decreased by 0.3% compared with 2017; over this period inputs increased by 0.7% while output increased less (0.4%), causing productivity to fall.

The latest annualised quarterly data suggest that 2018 saw the first annual fall in public service productivity since 2010, but this should be treated with caution until the more robust annual estimate for 2018 is available. In particular, the experimental data in this release cannot adjust for changes in quality in the experimental period. Nonetheless, public service productivity is estimated to have increased by a total of 5.0% between 2010 and 2018 (an average of 0.6% per year).

Figure 5: Strong productivity growth in Quarter 4 2018, but still falling over the year

Total public service productivity, UK, 1997 to 2018

Source: Office for National Statistics

Notes:

Estimates from 1997 to 2016 are based on the latest annual public service productivity release.

Estimates from Quarter 1 2017 to Quarter 4 2018 (in grey) are the experimental quarterly estimates in this article, and are annualised (in orange) for 2017 and 2018.

Estimates of productivity for the experimental period are indirectly seasonally adjusted, calculated using seasonally adjusted inputs and seasonally adjusted output.

Download this chart Figure 5: Strong productivity growth in Quarter 4 2018, but still falling over the year

Image .csv .xls8. Exploring productivity growth for English local enterprise partnerships (LEPs)

In February we released experimental statistics covering productivity estimates for 2017 for various levels of geography. This year “real” estimates of labour productivity data for LEPs were published for the first time. These constant price “real” data are most useful for assessing time series trends. They allow us to understand whether there has been any increase in volumes of goods and services per labour input, with the effects of changes in prices removed.

Local enterprise partnerships (LEPs) are partnerships in England between local authorities and businesses. They were created in 2011 and their role is to help shape local economic priorities and undertake activities to encourage local economic growth and the creation of jobs. There are currently 38 LEPs.

In terms of real productivity, 26 out of 38 LEPs experienced a growth in productivity in the period 2010 to 2017.

Figure 6 shows a scatter plot for real gross value added (GVA) growth and hours worked growth over the period 2010 to 2017 for the LEPs.

Coventry and Warwickshire had high productivity growth, as it had the largest output growth (28%) and this comfortably exceeded its growth in hours worked (16%). By contrast, London and South East Midlands also both had strong GVA growth, but this was accompanied by similarly high growth in hours worked, meaning that productivity growth was only 1.6% and 5.3% respectively. GVA growth was also strong in Oxfordshire and Hertfordshire, but in these areas growth in hours worked exceeded the growth in GVA leading to a reduction in productivity.

Out of the 38 LEPs in England, only Humber experienced negative GVA growth over the period 2010 to 2017. Humber’s negative GVA growth also led to it experiencing one of the highest declines in productivity.

Figure 6: Real gross value added growth compared with hours worked growth for local enterprise partnerships (LEPs), 2010 to 2017

Embed code

Source: Office for National Statistics

Notes:

- The chart excludes Dorset, due to a statistical discrepancy in the underlying data in the mining sector that is affecting the data for this LEP.

Full details of productivity for LEPs can be found in the accompanying dataset.

Back to table of contents9. Developing experimental estimates of investment in intangibles

In February we published an update on our workplan to review and improve the methodology used to estimate investment in intangible assets, as well as providing updated estimates of investment to 2016.

Intangible assets, also known as knowledge assets or intellectual capital, are assets that do not have a physical or financial embodiment. Not all intangible assets are included in the national accounts, but our broader definition encompasses assets such as software, reputation and branding, design, and research and development, which contribute to the long-term accumulation of a business’ knowledge capital. Such assets complement physical (tangible) capital, such as buildings, equipment and machinery, in driving economic growth.

Intangible investment in the market sector in the UK in 2016 was £134.3 billion, compared with £128.8 billion in 2015 in current price terms. This is the largest amount spent on intangible assets by the market sector over the period. In contrast, tangible investment was £148.5 billion in 2016, compared with £148.1 billion in 2015 in current price terms.

| £bn | |

|---|---|

| 2016 | |

| Training | 29.48 |

| Organisational Capital | 26.33 |

| Research and Development | 20.51 |

| Software | 19.32 |

| Branding | 15.20 |

| Design | 15.09 |

| Artistic Originals | 5.79 |

| Financial Product Innovation | 2.20 |

| Mineral Exploration | 0.36 |

| Total | 134.29 |

Download this table Table 2: Intangible investment, asset breakdown, market sector total, current prices, 2016, UK

.xls .csvRead the full Developing experimental estimates of investment in intangible assets in the UK: 2016 article.

Back to table of contents10. Opportunity to catch-up on our productivity forum

On 13 March 2019 we held a productivity forum to outline our key developments and core priorities for the future. Slides from the event are available. These also include a presentation from the Organisation for Economic Co-operation and Development (OECD) on measuring international productivity gaps.

If you would like any further information, please contact us at productivity@ons.gov.uk

Back to table of contents