1. Introduction

This technical report is intended to provide further detail on how the effects of taxes and benefits on household income (ETB) estimates are produced. This report also provides further information on the measurement of income inequality.

From financial year ending (FYE) 2015 the ETB data are split into two annual statistical bulletins. The first release – Household Disposable Income and Inequality (HDII) – provides headline estimates from the ETB data, to disposable income, and has been designed to provide more timely figures of main indicators relating to the distribution of household income and inequality, ahead of the main article. The main ETB statistical bulletin is published later in the year, building on the first release, and includes indirect taxes (for example VAT) and imputed income from benefits in kind (for example NHS, Education). The first HDII bulletin is based on the same dataset as the main ETB release and the data are not revised on a scheduled basis, meaning that the figures in the first release are fully consistent with those in the full ETB publication.

Back to table of contents2. Redistribution of income

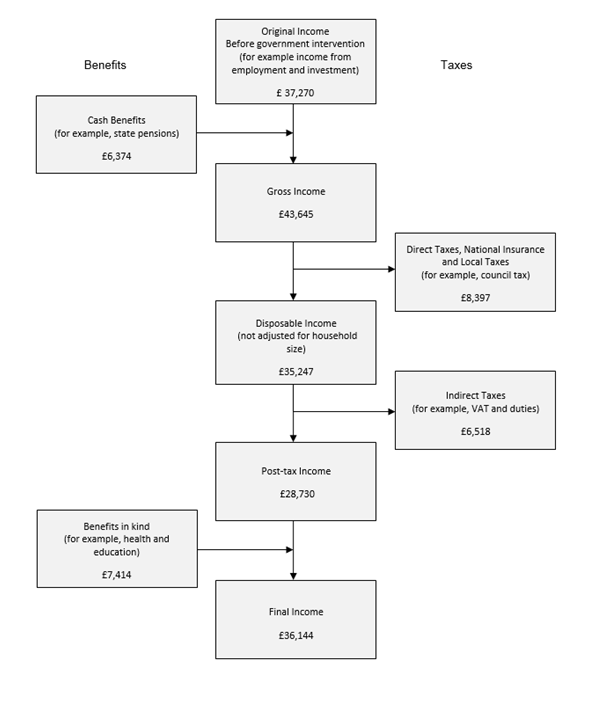

The five stages are: 1. Household members begin with income from employment, private pensions, investments and other non-government sources. This is referred to as “original income”

Households then receive income from cash benefits. The sum of cash benefits and original income is referred to as “gross income”.

Households then pay direct taxes. Direct taxes, when subtracted from gross income is referred to as “disposable income”

Indirect taxes are then paid via expenditure. Disposable income minus indirect taxes is referred to as “post-tax income”

Households finally receive a benefit from services (benefits in kind). Benefits in kind plus post-tax income is referred to as “final income”.

Note that at no stage are deductions made for housing costs.

Figure 1: Stages in the redistribution of income

Average household income, cash benefits and taxes, financial year ending 2017

Source: Office for National Statistics – The effects of taxes and benefits on household income

Download this image Figure 1: Stages in the redistribution of income

.png (53.1 kB){kind=link}

3. Original income

The starting point of the analysis is original income. This is the annualised income of all members of the household before the deduction of taxes or the addition of any state benefits. It includes income from employment, self-employment, investment income, private pensions and annuities which include all workplace pensions, individual personal pensions and annuities. This data is collected through the Living Costs and Food survey (LCF; see background notes for further information on data sources). The term “annualised” refers to the estimate of income expressed at an annual rate based on the respondent's assessment of their “normal” wage or salary, subject to their current employment status. Where a respondent has been unemployed for less than one year, their normal wage or salary (for their last job) is abated for the number of weeks absence. If a respondent has been unemployed for less than one year, their normal annual wage or salary they received in their last job is abated for the number of weeks of the last year since they last worked.

Similarly, for those in employment, this annualised estimate is “abated” for the number of weeks lost in the last 12 months due to sickness, maternity and so on. This is to avoid double counting wages and salaries and cash benefits. The abatement figure is taken as the number of weeks lost in the 12 months prior to interview.

About 98% of original income comes from earnings, private pensions (including annuities) and investment income. The very small amount remaining comes from a variety of sources: trade union benefits, income of children under 16, private scholarships, earnings as a mail order agent or baby-sitter, regular allowances from a non-spouse, allowances from an absent spouse and the imputed value of rent-free accommodation. Households living in rent-free dwellings are each assigned an imputed income (although this is counted as employment income if the tenancy depends on the job). This imputed income is estimated based on mortgage interest payment data for each of the regions and UK countries.

In addition to a wage or salary, some employees receive fringe benefits as part of their income such as company cars and rent-free accommodation. The company car benefit, together with the benefit from fuel for personal use, has been included in the analysis since 1990. Company car benefit and car fuel benefit together make up more than half of the total taxable value of all benefits in kind, considerably higher than the proportion of recipients who received these benefits, according to the latest (February 2018) HM Revenue and Customs’ (HMRC) statistics, due to the higher average taxable value for these benefits.

The imputed income allocated to households is the taxable value of the benefit in accordance with HMRC rules. Since 2002, tax charges on company cars have been based on the car’s list price and official CO2 emission figure. The CO2 figure is converted to a percentage multiplier and applied to the list price for tax purposes. This determines the taxable benefit charge for the year. In financial year ending (FYE) 2013, the tax bands were amended to reflect falling average emissions for new cars in the UK. It should be noted that while the benefit is not taxable for those earning below £8,500, here the benefit has been allocated to all those with a company car regardless of the level of earnings or Income Tax band, as the benefit experienced by company car users is independent of these.

It is recognised that the current modelling in relation to the list price of a vehicle does not accurately estimate the tax banding and is not flexible enough to accommodate emerging technologies and changes to taxes and benefits relating to these. A work package is planned to review the current methodology to identify where development is needed, either to keep pace with the changing economic and policy environment, or where existing assumptions risk becoming outdated. This review will aim to address current issues with the estimation of imputed income allocated for company cars.

Further, future work plans, aim to investigate the inclusion of other potential fringe benefits as part of income such as private medical and dental insurance.

Care should be taken in interpreting changes over time in the individual components of original income for each decile/quintile. Components such as self-employment income can be affected by both the amount earned by those who are self-employed, and the number of self-employed people with an equivalised disposable income1 in a given range in the sample, which can vary from year to year.

Notes for: Original income

- See Disposable Income section for the definition of equivalised disposable income.

4. Gross income

The next stage of the analysis is to add cash benefits and tax credits to original income to obtain gross income. This is slightly different from the “gross normal weekly income” used in the Living Costs and Food Survey (LCF) report “Family spending”, as the gross income measure in “the effects of taxes and benefits on household income” analysis makes adjustments to abate for weeks of work lost for reasons discussed in the original income section.

Prior to financial year ending (FYE) 2014, cash benefits and tax credits were categorised as contributory or non-contributory. Contributory benefits, which include State Pension, widows’ benefits and Statutory Maternity Pay or Allowance, depend on the amount of National Insurance contributions that have been paid by, or on behalf of, the individual. Non-contributory benefits do not depend on National Insurance contributions. These include Income Support, Child Benefit, Housing Benefit, Statutory Sick Pay, Carer’s Allowance, Attendance Allowance, Disability Living Allowance, war pensions, Severe Disablement Allowance, Industrial Injury Disablement Benefits, Child Tax Credit and Working Tax Credit, Pension Credit, over 80-years-old pension, Christmas bonus for pensioners, Government Training Scheme Allowances, student support, and Winter Fuel Payments. Some benefits or tax credits include both contributory and non-contributory elements, for example Jobseeker’s Allowance and Employment and Support Allowance (which is gradually replacing Incapacity Benefit and Income Support). From FYE 2014, while it remained possible to identify the contributory and non-contributory elements of Jobseekers’ Allowance, this was no longer possible for Employment and Support Allowance, preventing the continued sub-division of benefits into these categories.

The roll out of Universal Credit (UC) continued during FYE 2016 and FYE 2017. When fully rolled out, UC will replace the following six means tested benefits and Tax Credits with a single integrated benefit for working age people:

- Income Support

- Income-based Jobseekers’ Allowance (JSA)

- Income-based Employment and Support Allowance (ESA)

- Housing Benefit

- Working Tax Credit

- Child Tax Credit

From 11 April 2016, the childcare costs element of UC increased from 70% to 85% of registered childcare costs, up to a monthly limit of £646.35 for one child or £1,108.04 for two or more children.

Since the UC pilot and initial roll out in 2013, although UC has been rolled out more widely, its impact remains limited on ETB estimates.

Claimants of UC and Job Seeker’s Allowance (JSA) are subject to the Claimant Commitment, which outlines specific actions that the recipient must carry out in order to receive benefits. This may also have impacted on the number of households in receipt of these benefits. From FYE 2017 to FYE 2020 certain working-age benefits such JSA, Income Support, Universal Credit and Employment Support Allowance (work-related activity group) are frozen at FYE 2016 cash values.

Student loans are not included within the effects of taxes and benefits (ETB) analysis, therefore, income received and repayments made are excluded. A revised approach is being considered for future years analysis for which the details are still being worked through, in collaboration with other statistical producers.

Figure 2 shows the extent to which cash benefits increase incomes, from the bottom fifth to the top fifth of households. It can also be seen that the majority of cash benefits go to the bottom two-fifths of households. In FYE 2017, the average amount of cash benefits received by households was £6,374 per year, 14.6% of the average gross income.

Figure 2: Gross income by quintile groups of all households UK, financial year ending 2017

Average income per household (£ per year)

Source: Office for National Statistics – The effects of taxes and benefits on household income

Notes:

- Households are ranked by equivalised disposable income, using the modified-OECD scale.

Download this chart Figure 2: Gross income by quintile groups of all households UK, financial year ending 2017

Image .csv .xlsThe phasing out of Incapacity Benefit, Severe Disablement Allowance and Income Support paid because of illness or disability and transfer of recipients to Employment and Support Allowance (ESA) has seen average amounts received from the former benefits fall in recent years, while average amounts received from ESA have risen, reflecting the increased number of claimants. The roll-out of Personal Independence Payment (PIP), which is replacing Disability Living Allowance (DLA) for adults aged under 65, also continued in FYE 2017.

In FYE 2017, the average combined amount of contribution-based and income-based Jobseeker’s Allowance (JSA) received by the bottom two quintile groups decreased compared with FYE 2016. This is largely due to fewer households receiving this benefit, consistent with a fall in unemployment between these years, as well as the ongoing implementation of the Universal Credit (UC) system.

Since 7 January 2013, where at least one spouse or partner in a household has income in excess of £50,000, a High Income Child Benefit charge has been applied. For incomes above £60,000 the High Income Child Benefit charge is equal to the amount of Child Benefit received. Those affected by the charge can either elect to stop getting Child Benefit (“opt out”) or pay any tax charge through self-assessment.

In line with national accounts, Child Tax Credit (CTC) and Working Tax Credit (WTC) are recorded as cash benefits. Statutory Maternity Pay and Statutory Sick Pay are also classified as cash benefits even though they are paid through the employer.

Income from short-term benefits (for example Jobseeker’s Allowance) is taken as the product of the last weekly payment and the number of weeks the benefit was received in the 12 months prior to interview. Income from long-term benefits (for example Personal Independence Payment) and from Housing Benefits is based on current rates. In this analysis the State Pension is considered a cash benefit. As a result, for retired households (see Glossary in the Supporting information section), on average the State Pension accounted for 82% of the total cash benefits received in FYE 2017.

Most benefits, particularly Income Support, income-based Jobseeker’s Allowance, tax credits and Housing Benefit, are income-related and so payments are concentrated in the two lowest quintile groups. However, the presence of some individuals with low incomes in high-income households means that some payments are recorded further up the income distribution. Of the total amount of Income Support, income-based Jobseeker’s Allowance, tax credits and Housing Benefit paid to non-retired households, 41% goes to households in the bottom quintile group in FYE 2017. As households at the lower end of the distribution tend to have more children, we also see higher levels of Child Benefit at this end of the distribution.

In FYE 2017 cash benefits provided 40% of gross income for non-retired households in the bottom quintile group, while they account for just 2% of gross income in the top quintile. The payment of cash benefits therefore results in a significant reduction in income inequality.

Back to table of contents5. Disposable income

Income Tax, Council Tax and Northern Ireland rates and employees' and self-employed National Insurance contributions are grouped as direct taxes. When direct taxes are subtracted from gross income it forms disposable income. Taxes on capital, such as capital gains tax and inheritance tax, are not included in these deductions because there is no clear conceptual basis for doing so and the relevant data are not available from the Living Costs and Food Survey (LCF).

Figures for “Council Tax and Northern Ireland rates” include Council Tax (for households in Great Britain) and domestic rates (for households in Northern Ireland). Council Tax is shown after discounts, for example, the discount of 25% for single adult households. All Council Tax and Northern Ireland rates are shown after the deduction of Council Tax Support (formerly called Council Tax Benefit) and rate rebates. This is in line with the UK National Accounts which treat such rebates as revenue foregone. Up to and including financial year ending (FYE) 1996, these rebates were included as part of housing benefits.

Up to and including FYE 2002, the figures for local taxes also included charges made by water authorities for water, environmental and sewerage services. From FYE 2003, charges made by water authorities were treated as charges for a service rather than a tax, so the figures for Council Tax and Northern Ireland rates from FYE 2003 onwards are not strictly comparable with those for local taxes up to and including FYE 2002.

The tax estimates are based on the amount deducted from the last payment of employment income and pensions and on the amount paid in the last 12 months in respect of income from self-employment, interest, dividends and rent. The Income Tax payments recorded therefore take account of a household's tax allowances. Life assurance premium relief was deducted prior to FYE 2012. However, from FYE 2012 it was no longer possible to identify life assurance payments eligible for tax relief.

Households with higher incomes paid both higher amounts of direct tax and higher proportions of their income in direct tax. The richest fifth of households paid on average £21,357 per year in direct taxes in FYE 2017. In contrast, the direct tax bill for the poorest fifth of households was £1,940 per year. These amounts are equivalent to 23% of gross income in direct taxes for the richest fifth compared with 13% for the poorest fifth of households. As a result, direct taxes reduce inequality of income, that is, they are progressive.

The progressive nature of direct taxes as a whole are due in part to the progressive nature of Income Tax, with households at the lower end of the income distribution paying smaller amounts of Income Tax, as a proportion of gross income, compared with higher income households. This is because this tax is not paid at all on the first part of income and higher rates of Income Tax are paid on higher incomes.

In FYE 2016 for the first time, since the decision to phase out age-related personal allowances, those born between 6 April 1938 and 5 April 1948 received the same tax-free personal allowance as those born after 5 April 1948, increasing to £10,600 for both groups. There was no change to the personal allowance for those born before 6 April 1938, which remained at £10,660. There was also a reduction in the higher rate band for Income Tax, from £31,866 in FYE 2015 to £31,786. Combined with the personal allowance, this meant that people paid the higher rate of 40% on any taxable income above £42,385, up from £41,865 in FYE 2015. In FYE 2017, the income tax personal allowance increased by £400 to £11,000. The threshold for the 40% higher rate of income tax increased to £43,000 from £42,385. The 45% additional rate of income tax, paid on taxable incomes above £150,000 remains at 45%.

The increase in the Personal Allowance between FYE 2016 and FYE 2017 is estimated to have had a relatively small impact on the bottom fifth of households due to the smaller proportion of people with taxable incomes over the previous Personal Allowance in that group. Also, in higher income households there are more individuals with two or more people with taxable incomes, meaning that more than one person in the house will potentially be affected by the increased allowance. The decrease in the threshold for higher rate Income Tax contributed to higher income individuals receiving a smaller benefit from this change, relative to the size of their income.

Further Information on Income Tax rates and allowances for FYE 2017 can be found on Gov.uk.

The proportion of gross income paid in National Insurance Contributions (NICs) generally rises with income. In FYE 2016 and FYE 2017, the rate at which employees’ NICs were levied remained at 12% on earnings between the Primary Threshold and Upper Earnings Limit (weekly earnings of £155 and £827) and 2% on earnings above the Upper Earnings Limit. Employees’ NICs remain progressive for the first four quintiles, while the fifth quintile pays a similar proportion of their gross income as the fourth quintile.

People in an occupational pension scheme, or with an appropriate stakeholder or personal pension scheme, could “contract out” of the additional state pension (also known as second State Pension or SERPs). This allowed those paying into a pension scheme to pay a reduced rate of National Insurance (NI), for employees this was a 1.4% (reduced from 1.6% in 2002) reduction (on a proportion of earnings). Employers also received a 3.4% rebate for any employees in contracted-out pension schemes. From 6 April 2016 contracting out ended and individuals are no longer able to contract out of the additional state pension. In FYE 2017 employees who previously qualified for a reduced rate would have seen an increase in their NI.

Additionally, the Class 2 NICs rate for the self-employed increased from £2.75 per week in FYE 2015 to £2.80 in FYE 2016 (remaining at this level in FYE 2017).

In contrast to Income Tax and employees’ NICs, Council Tax (and domestic rates in Northern Ireland) is regressive, with the amount paid as a proportion of gross income tending to fall as income rises, even after taking into account Council Tax Support and rates rebates. Council Tax in Great Britain (and domestic rates in Northern Ireland), after taking into account rebates, represented 5% of gross income for those in the bottom fifth but only 2% for those in the top fifth, in FYE 2017. However, households in the lower part of the income distribution pay smaller absolute amounts, with average net payments by the bottom fifth of households around half those of the top fifth.

A scheme was introduced in FYE 2012 in England to pay a grant to local authorities that froze or reduced their council tax in that year. Further schemes have been offered to authorities that froze or reduced their council tax in all subsequent years up to and including FYE 2016.

In FYE 2016, 57% of eligible local authorities in England benefited from a Council Tax freeze grant. The bottom fifth of households would have benefitted most, in relative terms, from the Council Tax freeze grant. However, the absolute savings will be higher at the top of the income distribution. There is no freeze grant in FYE 2017.

The average Band D council tax set by local authorities in England for FYE 2017 was £1,530, which was an increase of £46 or 3.1% on the FYE 2016 figure of £1,484. In FYE 2017, local authorities have been able to increase council tax by up to 2% to fund adult social care only. This is in addition to the usual funding of adult social care through council tax. This applies to London boroughs, county councils, metropolitan districts and unitary authorities.

From 1 April 2013 council tax benefit, the means of helping people on low incomes meet their council tax obligations, was replaced by new localised support schemes. Council tax bills have been frozen in Scotland since 2007, each local authority determines their own Band D rate of Council Tax as part of their budget setting process. The rate for other bands is then calculated as a set ratio of the Band D rate, resulting in each local authority having a different Council Tax rate.

The average band D council tax for Wales in FYE 2017 was £1,374, a 3.5% increase compared with 2015/16 (which increased 4.1% on FYE 2015).

In FYE 2016 domestic rates in Northern Ireland increased by 1.4%. For FYE 2017, the regional rate in Northern Ireland increased by 1.7% on its 2015/16 value.

Equivalised disposable income

Disposable income is equivalised to rank households from richest to poorest. Equivalisation is a process that makes adjustments to incomes, so that households with different compositions can be analysed in a sensible way. This reflects the common sense notion that, in order to enjoy a comparable standard of living, a household of, for example, three adults will need a higher level of income than a household of one person.

This analysis uses the modified Organisation for Economic Co-operation and Development (OECD) scale to equivalise household incomes. It was proposed by Hagenaars, De Vos and Zaidi in 1994 for use across the world and has been applied to a number of UK Government sources, such as the Households Below Average Income (HBAI) series. The modified-OECD scale usually assigns a weight of 1.0 for the first adult in a household, 0.5 for each additional adult and a weight of 0.3 for each child (aged 0 to 14 years).

However, in this analysis the modified-OECD scale has been rescaled so that a two adult household equivalence value is 1.0. This makes it easier to compare with data prior to FYE 2010 which uses the McClements equivalence scale, but makes no difference to the overall results. In any time series analysis that uses data prior to FYE 2010, these years have been recalculated using the rescaled modified-OECD scale.

| Type of household member | Modified-OECD Equivalence value |

|---|---|

| First adult | 0.67 |

| Second and subsequent adults | 0.33 (per adult) |

| Child aged 14 and over | 0.33 |

| Child aged 13 and under | 0.2 |

Download this table Table 1: The modified–OECD scale in effects of taxes and benefits analysis

.xls .csvThe values for each household member are added together to give the total equivalence number for that household. This number is then used to divide disposable income for that household to give equivalised disposable income. For example, take a household that has a married couple with two children (aged six and nine) plus one adult lodger. The household's equivalence number is 0.67 + 0.33 + 0.20 + 0.20 + 0.33 = 1.73. The household's disposable income is £20,000 and so its equivalised disposable income is £11,561 (£20,000/1.73).

Equivalised disposable income is used to produce the single ranking which is applied in all the tables in this analysis (apart from the Gini coefficients which have to be ranked afresh for each different definition of income).

Back to table of contents6. Top income adjustment

A further adjustment is applied to the data to adjust for the undercoverage and under-reporting of income of the richest individuals. Broadly, the approach, which is detailed in more depth in Top income adjustment in effects of taxes and benefits data: methodology, follows the methods first implemented in the UK by the Department for Work and Pensions (DWP) for the households below average incomes (HBAI) statistics, which are based on the Family Resources Survey (FRS). This method is often referred to as the "SPI adjustment" owing to its use of HM Revenue and Customs's (HMRC's) Survey of Personal Incomes (SPI); this is a microdataset containing taxable incomes based on a sample of administrative records from UK tax payers. The DWP approach involves replacing the incomes of the richest 0.32% and 1.16% of working-age people and pensioners, respectively, with cell-mean imputations based on corresponding observations in tax return data. The SPI adjustment also stratifies separately for Great Britain and Northern Ireland.

The approach used in effects of taxes and benefits (ETB) data further refines the DWP methodology, building on recommendations put forward by Burkhauser et al. (2018). Specifically, the steps taken are:

step one: estimate personal taxable income for individuals on ETB data

step two: add a dummy record to the SPI data to account for individuals who do not pay tax; their personal taxable income is set to zero, and their weight reflects the difference in population totals between the ETB and SPI datasets

step three: rank individuals in ETB and SPI data by personal taxable income

step four: allocate individuals above the 97th percentile of the SPI distributions, within 0.5% quantile bands, so that there are six groups of individuals at the top, each representing 0.5% of the population

step five: calculate the lower income boundaries for each of these quantile groups on the SPI data and create bands in the ETB data using these boundaries

step six: calculate the mean personal taxable income for each quantile group in the SPI data and impute this onto individuals in the equivalent survey bands

step seven: reweight the ETB bands so that their weights are the same as the SPI quantiles

step eight: reweight the unadjusted ETB data so that overall population totals for each weighting variable are maintained

step nine: add back several income components to the ETB cases not represented in the SPI data, such as individual savings accounts (ISAs) and intrahousehold transfers

step ten: re-calculate Income Tax and National Insurance contributions for the adjusted ETB cases based on new estimates of personal pre-tax income

step eleven: aggregate personal-level income across household members to estimate adjusted household disposable income

One of the challenges in implementing this adjustment is the reliance on SPI data, which are not typically made available to researchers until at least two years after the end of the income reference period. Therefore, it is necessary to use estimates provided by HMRC, which are based on projections from historical SPI datasets. These projections provide the lower income boundaries required in step five.

These adjustments were first introduced for statistics covering the financial year ending (FYE) 2019 and extending back to the FYE 2002. Figure 3 highlights that broadly, the impact of the adjustment is to raise overall levels of income inequality. Further, the introduction of a top income adjustment increases the coherence of estimates of levels of income inequality reported by the Office for National Statistics (ONS) and DWP, while the trends seen in both series remain comparable. The average absolute deviation between the ONS and DWP measures of income inequality between the FYE 2002 and FYE 2018 narrowed from 1.9 percentage points before the top income adjustment is introduced to 0.8 percentage points after.

Figure 3: The introduction of a top income adjustment improves coherence with household below average income statistics

Gini coefficient of disposable income as measured on Living Costs and Food Survey, both adjusted and unadjusted, and households below average income, UK, 1977 to financial year ending 2019

Source: Office for National Statistics and Department for Work and Pensions

Notes:

- FYE 2019, which represents the financial year ending 2019, (April to March), and similarly for all other years expressed in this format.

Download this chart Figure 3: The introduction of a top income adjustment improves coherence with household below average income statistics

Image .csv .xls7. Post-tax income

The next step is to deduct indirect taxes to give post-tax income.

These types of taxes can be divided into two key types; those on final goods and services and those on intermediate goods. Final goods and services are those that are sold to final users (in this case household consumers), while intermediate goods are those that are used in the production of final goods. For example, in the case of a company importing washers to produce water taps to sell to consumers, the washer is the intermediate good and the tap is the final good. Throughout this analysis we assume that the incidence of intermediate taxes is born by the consumer who purchases the final good (in this case, households). We assume that companies pass on the full cost of intermediate taxes to the consumer in the price of the final good, although we make allowances for the proportion of the tax paid by public authorities and foreign consumers. In the above example the company would pass on any import duties on the washer to the consumer of the tap.

Indirect tax on final consumer goods and services include:

duties on alcoholic drinks, tobacco, petrol, oil, betting

Value Added Tax (VAT)

customs (import) duties

motor vehicle duties

Air Passenger Duty

Insurance Premium Tax

driving licences

television licences

stamp duties,

Camelot: payments to National Lottery Distribution Fund

Taxes levied on final goods and services are assumed to be fully incident on the consumer and can be imputed from a household's Living Costs and Food survey (LCF) expenditure record. For example, the amount of VAT that is paid by the household is calculated from the household's total expenditure on goods and services which are subject to VAT. Some goods and services are exempt, meaning they are out of the conceptual scope of vatable goods and services. There are three rates of VAT; standard, reduced and zero. Most goods and services are taxed at the standard rate of VAT whereas others, such as gas and electricity for the home, children's car seats and some energy-saving materials, are at a reduced rate. Some goods and services, which include most (but not all) foods, children's clothes and books, are zero-rated.

The rates of VAT applied during the FYE 2017 financial year are as follows: (unchanged on FYE 2016)

Standard rate: 20%\ Reduced rate: 5%\ Zero rate: 0%

To illustrate how VAT is calculated, here are three examples which could be taken from householders expenditure diaries:

Standard rate

A household spends £1250.00 on a new car which is at the standard rate of 20% VAT The cost of the car excluding VAT is therefore £1041.67 (1250.00/1.20). The VAT is £208.33 (1250.00-1041.67).

The household therefore pays £208.33 in VAT on this purchase.

Reduced rate

A household spends £1250.00 on a solar panel which is at the reduced rate of 5% VAT The cost of the solar panel excluding VAT is therefore £1190.48 (1,250.00/1.05) The VAT is £59.52 (£1250.00-1190.48).

The household therefore pays £59.52 in VAT on this purchase.

Zero rate

A household spends £1.20 (120 pence) on bread which is zero rated VAT The cost of the bread excluding VAT is £1.20 (120 /1.0) The VAT is £0 (£1.20-1.20)

The household therefore pays £0 in VAT on this purchase.

In the case of the purchase of second-hand cars, the price is in part determined by the prices of new cars because, as VAT is levied on new cars, VAT also affects the price of second-hand cars (and is therefore assumed to be incident on the purchasers of both).

In allocating taxes, expenditures recorded in the LCF on products such as alcoholic drinks, tobacco, ice cream, soft drinks and confectionery are grossed up to allow for the known under-recording of these items in the sample. The method for estimating the level of underreporting of alcohol expenditure was redeveloped in the FYE 2012 publication, although the assumption that the true expenditure in each case is proportional to the recorded expenditure remains. This assumption has its drawbacks because there is some evidence to suggest that heavy drinkers, for example, are under-represented in the LCF.

In FYE 2014 the VAT rates were reviewed in line with HMRC's VAT Theoretical Tax Liabilities Model. Applying these reviewed rates to FYE 2013 LCF data resulted in a 5% increase in total VAT. In FYE 2016 average VAT for all households decreased by 1% compared with 2014/15, however, this increased by 7.5% in FYE 2017. The FYE 2017 growth is accounted for by stronger growth in expenditure of VATable goods.

Machine Games Duty (MGD) is a tax on some games machines and, from February 2013, replaced Amusement Machine License Duty (AMLD) and VAT charged on the income from these machines. The criteria for whether a games machine is liable for MGD is different from that for AMLD, as are the rates at which duty is paid. MGD is an intermediate tax, which means that we assume a proportion of the duty paid by the business is passed on to the consumer, or in this case, the person who gambles on these machines, in the form of reduced odds. However, for the purposes of this analysis, it has been included within indirect taxes because most betting taxes are linked to a households' expenditure.

From 1 December 2014 HMRC changed how General Betting Duty (GBD), Pool Betting Duty (PBD) and Remote Gaming Duty (RGD) are taxed from a "place of supply" to a "place of consumption"; this was known as Gambling Tax Reform (GTR). At the same time, there were changes to the accounting periods for GBD and PBD returns which moved from monthly to quarterly. In addition, the first accounting period for GTR was 1 December 2014 to 31 March 2015, with first receipts received from April 2015. This contributed, in FYE 2016, to an overall increase of 19% for all households in the average amount paid on betting taxes. This increase is observed, in FYE 2016, for all except the poorest households. In FYE 2017 average betting taxes for all households increased by 2.7%.

In this analysis, the incidence of Stamp Duty on house purchase of an owner-occupying household has been taken as the product of the hypothetical duty payable on buying their current dwelling (estimated from valuations given in the LCF) and the probability of an owner-occupying household moving in a given year. Prior to FYE 2013, this was estimated from the General Lifestyle Survey. In FYE 2013, the English Housing Survey (EHS) was adopted due to its larger sample size, which made it a more suitable source.

House prices of an owner-occupying household are estimated by uprating council tax information provided in the LCF. From the FYE 2017 analysis a new data source, UK House Price Index (HPI), is used to uprate average house prices in the UK. The data are produced by Land Registry and ONS, the Average price seasonally adjusted is used to uprate the estimated house price obtained in the LCF to provide a more accurate estimate of UK house prices. Improved HPI methodologies include; cash sales and new dwellings to provide full coverage of the housing market and a more appropriate calculation of average price that is not sensitive to extreme valued properties. Whilst there are changes to the HPI data sources they show very similar trends over time. In previous years effects of taxes and benefits (ETB) estimated house prices were uprated using Ministry of Housing, Communities and Local Government data and ONS house price data.

From 4 December 2014, the way in which UK Stamp Duty Land Tax (SDLT) was levied changed. Prior to this date, if a property purchased was above the zero tax rate a single rate of tax was applied to the entire property price, dependent on the level of that price. From December 2014, different tax rates are payable on different parts of the property price within each tax band. This means that the effective rate of SDLT rises as property values increase. In Scotland, Land and Buildings Transaction Tax (LBTT) replaced SDLT from 1 April 2015. LBTT is applied in the same way as SDLT in that the percentage rate for each band in LBTT is applied only to the part of the price over the relevant threshold and up to the next threshold. In FYE 2016 and FYE 2017 the rate of tax is the same for SDLT and LBTT, however, the purchase price thresholds, which determines the rate of tax applied, are different. In April 2018, Land Transaction Tax (LTT) replaced SDLT in Wales, where it is now collected by the Welsh Revenue Authority.

For example, a house bought for £280,000 in England, Wales or Northern Ireland is charged at:

0% for the first £125,000, then

2% for the next £125,000

5% for the next £30,000 and

£4,000 must be paid in SDLT

A house bought for £280,000 in Scotland is charged at:

0% for the first £145,000, then

2% for the next £105,000

5% for the next £30,000 and

£3,600 must be paid in LBTT

A house bought for £280,000 in Wales is charged at:

0% for the first £180,000, then

3.5% for the next £70,000

5% for the next £30,000 and

£3,950 must be paid in LTT

The current method of allocating SDLT, LBTT and LTT to households uses the average amount of SDLT receipts data from the Stamp Duty Statistics, Revenue Scotland data for LBTT and Land Transaction Tax Statistics for LTT, by financial year, for residential property (individual buyers receipts). Some investors such as buy-to-lets and sole trader small developers will be included within this figure, therefore, a proportion of the receipts data are allocated to try and account for this. In FYE 2017 the allocation also considers the April 2016 surcharge of 3% on existing Stamp Duty Land Tax rates applied to those buying a second home and those investing in buy-to-let properties. This is referred to as the new rates of duty on additional residential dwellings (HRAD). Repayments of the additional dwellings rate are available to a purchaser who has sold their previous main residence within three years of paying the higher SDLT rates, repayments, in FYE 2017, are deducted from the amount of duty allocated to households. Further research and developments are planned to refine the methodology to allocate stamp duty to households. This will include exploring other potential data sources, and is hoped to be in place for FYE 2019 estimates.

In November 2015 the standard rate of Insurance Premium Tax (IPT) increased from 6% to 9.5 contributing to a 14% increase in the average amount paid in IPT for all households in FYE 2016. IPT increased by further 0.5 percentage points, to 10%, from 1 October 2016 contributing to a 36.1% (£26) increase in the average amount paid in IPT for all households in FYE 2017.

Indirect taxes on intermediate goods and services include:

rates on commercial and industrial property

motor vehicle duties

duties on hydrocarbon oils

employers' contributions to National Insurance, the National Health Service (NHS), the industrial injuries fund and the redundancy payments scheme

customs (import) duties

stamp duties

VAT (on the intermediate stages of exempt goods)

Independent Commission franchise payments

landfill tax

Consumer Credit Act fees

bank levy

As discussed above, the incidence of intermediate taxes are borne by the consumer of the final good. In this analysis only taxes on goods and services consumed by households are included. The allocations between different categories of consumers' expenditure are based on the relation between intermediate production and final consumption, using estimated input-output techniques. This process is not an exact science and many assumptions have to be made. Some analyses, such as that by Dilnot, Kay and Keen "Allocating taxes to households: A methodology", suggest that the taxes could be progressive rather than regressive if different incidence assumptions were to be used.

Because indirect taxes are taxes that are paid on items of expenditure, the amount of indirect tax each household pays is determined by their expenditure rather than their income. While the payment of indirect taxes can be expressed as a percentage of gross income, in the same way as for direct taxes, this can be potentially misleading. This is because some households have an annual expenditure that exceeds their annual income, particularly those towards the bottom of the income distribution. Stoyanova and Tonkin (2018) showed that in FYE 2017 the poorest 10% of households had expenditure more than twice the level of their income. In that sense, it can be argued that expenditure may be a better indicator of standard of living than income is. Therefore, payment of indirect taxes is presented as a percentage of expenditure to give a more complete picture of the impact of indirect taxes.

Carrera (2010) discussed some of the most common alternative methods used to fund expenditure in households whose expenditure was at least twice the level of their disposable income. For such households, the most common source of funds was savings, followed by credit or store cards and loans. There may be a number of reasons why households in the bottom income decile tend to have expenditure higher than their income. For example, such households often include people not currently in employment, students and some self-employed individuals, who have, or report, very little income. Some of these households may be at the bottom of the income distribution only temporarily, experiencing a short-term period of low earnings but still maintaining a steady level of consumption and thereby a fairly constant standard of living. In addition, some types of one-off receipts, such as inheritance and severance payments, are not included as income in this analysis. Income and expenditure data are measured in different ways in the Living Costs and Food Survey (LCF) and could be both be affected by measurement and sampling error. However, research suggests that expenditure tends to be measured more accurately than income towards the lower end of the income distribution, with evidence from both the United States and United Kingdom of under-reporting of certain forms of income, such as benefits (Brewer and O'Dea, 2017, Meyer and Sullivan, 2013).

When expressed as a percentage of expenditure the proportion paid in indirect tax tends to be lower for households at the top of the distribution, compared with those lower down (17.6% for the top fifth compared with 20.3% for the bottom fifth, in FYE 2017). The higher percentage of expenditure by low income groups on tobacco (1.6% of total expenditure for the bottom fifth compared with 0.3% for the top fifth, in FYE 2017) and on the "other indirect taxes", which include television licences, Stamp Duty on house purchases and the Camelot National Lottery Fund (7.0% compared with 5.8%, respectively, in FYE 2017), accounts for part of this difference.

On the other hand, the impact of indirect taxes, as a proportion of disposable income, declines much more sharply as income rises. For example, VAT accounted for 12.8% of disposable income for households in the bottom fifth, falling to 7.3% for households in the top fifth, in FYE 2017. There were similar patterns for the other indirect taxes. This is because those in higher income groups tend to channel a larger proportion of their income into places which do not attract indirect taxes, such as savings and mortgage payments. For this reason, and those already mentioned regarding high expenditure households, indirect taxes expressed as a proportion of income appear more regressive than when expressed as a proportion of expenditure.

The measure of expenditure used in this analysis has been calculated to be consistent with the definition of disposable income. For instance, because the imputed income from benefits in kind, such as company cars and rent-free accommodation, will have boosted the figure for disposable income, these items have been added to the expenditure measure as well. Expenditure on alcohol, tobacco and confectionery has been grossed up for under-recording in line with the treatment of the indirect taxes on these items. Payments, such as superannuation, regular savings, mortgage repayments and so on, have been included in expenditure and adjusted where necessary, but not items such as lump sum capital payments, in line with the exclusion of capital gains and windfalls from income.

Back to table of contents8. Final income

This analysis adds notional benefits in kind provided to households by the government for which there is a reasonable basis for allocation to households, to obtain final income. There are some items of government expenditure, such as capital expenditure and expenditure on defence and on the maintenance of law and order, for which there is no clear conceptual basis for allocation, or for which we do not have sufficient information to make an allocation. The benefits in kind allocated are:

National Health Service (NHS) (including Health and Social Care in Northern Ireland),

state education,

adult social care,

school meals and Healthy Start vouchers (including nursery milk and school milk, universal infant free school meals in England, free school meals for children in primary 1 to 3 in Scotland and the provision of free breakfast to all pupils in maintained primary schools in Wales),

housing subsidies,

railway travel subsidies,

bus travel subsidies (including concessionary fares schemes).

NHS

This benefit-in-kind is estimated using data available on the average cost to the Exchequer of providing the various types of health care - hospital inpatient and outpatient care, GP consultations, and pharmaceutical, dental and ophthalmic services. Each individual in the Living Costs and Food Survey (LCF) is allocated a benefit from the NHS according to the estimated average use made of the various types of health service by people of different age and sex groupings. Values are adjusted on a yearly basis to reflect changes in total NHS spending and the population make-up of the UK. The benefit from maternity services is assigned separately to those households containing children under the age of 12 months. No allowance is made for the use of private healthcare services.

The assigned benefit is relatively high for young children and falls towards later childhood. Through the adult years, it begins to rise, increasing further from late middle age onwards. For all individuals and households, this benefit is lower in the top two income quintiles. This pattern reflects the demographic composition of households. Studies by Sefton (2002) have attempted to allow for variations in the use of the health service according to socio-economic characteristics. A study by Asaria et al. (2016) at the University of York Centre for Health Economics looked at hospital admissions data for England to show how NHS spending varies according to regional deprivation levels. Using this work as a basis, deprivation weights for age and sex groupings in different regions have been applied in the calculation of the benefit-in-kind from the NHS for the financial year ending (FYE) 2017 onwards. Future work will investigate how to apply deprivation weights to the NHS benefit-in-kind for earlier years of effects of taxes and benefits (ETB).

In addition to the use of deprivation weights from the FYE 2017 onwards, another methodological change was implemented in the FYE 2012 and as such, the NHS figures from before the FYE 2012 are not fully comparable with those from after. Since the FYE 2012, separate values for the benefit-in-kind of the NHS have been calculated for each devolved administration using regional spending data from HM Treasury. This change, combined with improvements in the measurement of GP, dental and ophthalmic services and the measurement of the distribution of healthcare services by age and sex, has improved the estimates of the distribution of the NHS benefit-in-kind by level of income.

Education

The benefit from state-provided education is estimated from information provided by the Department for Education, Department for Business, Innovation and Skills (BIS), Welsh Government and local authorities, HM Treasury, the Higher Education Funding Council for England, Department of Education Northern Ireland, Scottish Government, Scottish Funding Council (SFC) and the Higher Education Statistics Agency. These sources provide the costs per full-time equivalent pupil or student in maintained special schools, nursery, primary and secondary schools, universities, and other further education establishments.

The value of the benefits attributed to a household depends on the number of people in the household recorded in the LCF as receiving each kind of state education (students away from the household are excluded). The estimates serve as a proxy for the unit cost per full-time equivalent pupil per year in the UK. There is just one estimate for secondary school children available, although it is conceded that the cost climbs steeply with the age of the pupil. Therefore, in this analysis, there is a split in the allocation of per capita expenditure on children between those aged 11 and 15 at the beginning of the school year, and those 16 and over at secondary schools. No benefit is allocated for pupils attending private schools, those receiving home schooling or for nursery pupils under the age of three, who are not eligible for state funding.

The methodology behind the benefit from education has undergone several improvements in recent years. Improvements in the FYE 2012 analysis included new sources for further and higher education, along with the benefits received by households from nursery, primary, secondary and higher education, estimated separately for each devolved administration.

Non-retired households in the lower quintile groups received, in FYE 2017, the highest benefit from education. This is due to the relatively high number of children in this part of the distribution. In addition, children in households in the higher quintiles are more likely to be attending private schools and an allocation is not made in these cases. The benefit given to households for education is estimated to be equivalent to 11% of the average post-tax income for non-retired households, or an average of £3,462 per year, in FYE 2017. For retired households, education benefits-in-kind are negligible.

Adult social care

In 2018, the Office for National Statistics (ONS) commissioned the National Institute of Economic and Social Research (NIESR) to develop a new method for measuring the distribution of adult social care in the UK. These measures were implemented and reported in effects of taxes and benefits (ETB) for the financial year ending (FYE) 2018.

Adult social care is defined as the personal care and practical support provided to adults with physical or learning disabilities, or physical or mental illnesses, as well as support for their carers. This could be for personal care (such as eating, washing or getting dressed) or for domestic routines (such as cleaning or going to the shops). This support is provided in various ways. It can be provided through formal care services, including residential care homes or a carer helping in the home.

Broadly, the approach aims to allocate actual spending on adult social care, using data from NHS Digital, to people on the LCF dataset for England. Data on spending in Scotland are used from Scottish Government and data for Wales from StatsWales. As comparable data are not available from Northern Ireland, it requires further work to gross up to a UK total.

While the preferred approach would have been to adopt an insurance-based allocation, similar to the NHS, the nature of adult social care provision makes this more complicated. Unlike health care, social care services in the UK are not provided free of charge for everyone. In England, local authorities provide assistance to adults who have insufficient financial means to fund their own use of care services. In particular, a person will have to pay the full cost of their care if they have more than £23,250 in savings. Unless they are going into a care home, this amount does not include the value of the person's property. If savings are less than £23,250 but more than £14,250, then the local council will pay for care, but the person will have to contribute £1 to the fees for every £250 of savings they have. If a person has less than £14,250 in savings, their care will be fully paid for by the council. Local authorities also take a person's income into account during the financial assessment. This financial assessment means those with sufficient financial resources are unlikely to be eligible for publicly funded social care even if they require support, so that the insurance value approach will need to be modified somewhat.

The consequence of the means-tested arrangement for adult social care funding is that detailed information on people's assets are required to understand which people are not covered under an insurance-style allocation. Unfortunately, the LCF does not currently contain the required level of detail to estimate the value of household assets. As such, the methodology recommended by the NIESR is to adopt a hybrid of the insurance and consumption approach where 20% of adult social care is allocated via an insurance approach and 80% via the consumption. This 80-to-20 split was recommended by the NIESR to ensure that there is not too much weight given to the insurance aspect because of the lack of household asset information.

The LCF does not currently contain any information on whether a respondent has been a recipient of adult social care provision. Therefore, we allocate the consumption element of adult social care spending to individuals based on the LCF according to whether they receive any of Attendance Allowance, Incapacity Benefit, Carer's Allowance, Severe Disablement Allowance or Disability Living Allowance. Future developments will explore the potential of adding new questions on the LCF to improve our understanding of which individuals use publicly provided adult social care.

Another consideration in developing this methodology is that residential care (for example, people living in institutional households, such as residential care homes and prisons) accounts for just under half of total spending on adult social care in England. However, ETB distributional statistics are based on the LCF, which is a sample of private households. As such, this methodology does not allocate spending on people living in institutional households to people in the LCF.

Summarising all of this, the methodology to allocate adult social to individuals in ETB statistics in the FYE 2018 was:

construct totals for non-residential spending by age group and NUTS1 region in England using data from NHS Digital, and calculate the adult population total by NUTS1 region in England using data from the ONS; this is repeated for Scotland and Wales using their respective data sources

allocate 20% of totals to be distributed by insurance method and 80% for consumption method

allocate insurance amount by applying per person amount to every adult on the LCF, by region

allocate regional consumption total, by distributing total to all adults who receive either Attendance Allowance, Incapacity Benefit, Carer's Allowance, Severe Disablement Allowance or Disability Living Allowance

to gross up to the UK total, spending in Northern Ireland is given as an average of spending in England, Scotland and Wales and is allocated to individuals within Northern Ireland

sum the receipt of adult social care of individuals within households to estimate the household spending on adult social care

School meals and Healthy Start vouchers

The allocation of School meals has changed in FYE 2016 to that of the method applied in previous years.

Prior to FYE 2016 the value of free school meals was based on their costs to the public authorities. Taking administrative data on the quantity of school meals and the cost per unit, an aggregate cost was calculated. This aggregate cost was then divided amongst those children who were identified in the Living Costs and Food survey (LCF) as being eligible for free school meals (FSM). From FYE 2014, local authorities no longer provided the Department for Education with details of expenditure on free school meals and, in order to provide a consistent time series, the FYE 2013 figures for total expenditure on school meals and nursery milk were adjusted using a deflator based on the change in expenditure on school canteens from the Consumer Price Index. This adjustment and methodology was applied from FYE 2013 to FYE 2015.

The cost allocated per free school meal has changed in FYE 2016 to use the allocation the Education Funding Agency makes for universal infant free school meals (UIFSM), an allocation of £2.30 per free school meal. The allocation of free school meals assumes that if a child is eligible and is identified, from the LCF, as receiving free school meals the uptake of these meals is for five days a week for 39 weeks of the year. The amount is only allocated to those who have reported, in the LCF, as receiving free school meals, acknowledging that not all eligible children uptake free school meals. This is a change to the methodology as prior to FYE 2016 the amount allocated for free school meals was allocated to all those identified as eligible.

From FYE 2016 universal infant free school meals (UIFSM) in England and free school meals for children in primary 1 to 3 in Scotland are included within the allocation. This policy was introduced from September 2014 in England and January 2015 in Scotland. Eligibility for universal infant free school meals and free school meals for children in primary 1 to 3 in Scotland is based on children who are identified in the LCF as eligible. After identifying eligible children only those recorded, in the LCF, as receiving a free school meal are assigned a value, acknowledging that not all eligible children uptake free school meals. The value allocated is calculated using the same method applied to free school meals.

Should children meet the eligibility criteria for free school meals and universal infant free school meals in England (school meals for children in primary 1 to 3 in Scotland), and respond to the LCF as up-taking free school meals, the higher value would be allocated. However, as there is currently no difference between the values of meals this makes no difference to the estimates from FYE 2016 onwards.

From FYE 2016 the provision of free breakfast to all pupils in maintained primary schools in Wales are included within the estimates. The allocation made is based on children who are identified, in the LCF, as eligible. Eligible children are defined as being in a state-run/maintained primary or state run special school in Wales. It’s not possible, from the LCF, to obtain information on the number of children up-taking free breakfasts and it’s also not possible to obtain a cost per breakfast, therefore, from the FYE 2016 allocation estimates of the cost and uptake are applied.

The estimates also include the imputed value of Healthy Start vouchers (from FYE 2010) and Nursery and School milk, as reported in the LCF. School milk has only been included within the allocation from FYE 2016.

Prior to FYE 2016 free school meals predominantly went to lower income groups, where children were more likely to have school meals provided free of charge, however, as a result of the changes applied in FYE 2016 there is an increase in the average amount received by the richest households. Further refinement of the methodology applied to allocate free school meals is scheduled in FYE 2019, this will aim to explore other data sources and further improve the allocation in future releases.

Housing subsidies

In this analysis, public sector tenants are defined to include the tenants of local authorities, Scottish Homes, Northern Ireland Housing Executive (NIHE), housing associations and registered social landlords.

Prior to FYE 2013 the total housing subsidy allocated included the contribution from Central Government to the housing revenue accounts of local authorities and grants paid to Scottish Homes, the NIHE, housing associations and registered social landlords. In March 2012 the Housing Revenue Account Subsidy (HRAS) system was abolished and replaced with a self-financing system. This involved transfers of assets and liabilities between central and local government. There remains a Housing Revenue Account (HRA) which is a record of revenue expenditure and income relating to an authority’s own housing stock. The HRA is a ring-fenced account, ensuring that rents paid by local authority tenants make a fair contribution to the cost of providing the housing service. Rent levels can therefore not be subsidised by increases in the council tax and equally, local authorities are prevented from increasing rents in order to keep council tax levels down. The HRA is a local authority statutory account.

From the FYE 2013 analysis the HRA imputed subsidy is obtained from National Accounts (NA) data (series: GNM2), which is based on data provided by local authorities via the Ministry of Housing, Communities and Local Government (MHCLG) and the devolved administrations. Each public-sector tenant, identified in the Living Costs and Food Survey (LCF), has been allocated a share of the HRA imputed subsidy by the following country and regions: Greater London, the rest of England, Wales, Scotland and Northern Ireland (NI). The allocation is based on the council tax band (rates in NI) of the dwelling and the weighted average (by type of property) property price within each country or region.

The HRA is classified as a public quasi-corporation1, an imputed subsidy is allocated in this analysis that accounts for where the HRA balance is negative (thus local authorities making up the shortfall as an equity injection). The HRA balance can be positive (thus a theoretical dividend paid from the HRA to Local Authorities), however, as this would be a negative subsidy this is not included within the allocation. Rent rebates and allowances or local tax rebates are also not included within the allocation of housing subsidies.

Travel subsidies

Travel subsidies cover the support payments made to bus and train operating companies. The use of public transport by non-retired households is partly related to the need to travel to work and, therefore, to the number of economically active people in a household. This results in estimates of these subsidies being higher for households in higher income quintiles. This pattern is also due to London and the South East having higher levels of commuting by public transport together with higher than average household incomes.

Rail subsidy is allocated to households based on their spending on rail travel taken from the LCF. The level of subsidy to those living in London and the South East is calculated separately from the rest of the UK, reflecting higher levels of subsidy for London transport and the assumption that a higher number of households in the South East will commute into London and thus benefit from this subsidy. In making these allocations, allowances are also made for the use of rail travel by the business sector, tourists and the institutional part of the personal (household) sector (for example, people who do not live in private households; for instance, prisoners or people in care homes).

Bus travel subsidy is calculated in a similar way to rail travel subsidy; however, additional levels of benefit are allocated to those households containing individuals who indicate in the LCF that they hold a concessionary bus pass.

Since FYE 2011 figures for rail travel subsidy have taken into account the government grant to the infrastructure operator Network Rail, which enables Network Rail to lower the charges levied on each train operating company, using data supplied and published by the Department for Transport (DfT). This grant was apportioned regionally according to the benefit the train operating companies gained from reduced fees. Support to passenger transport executives are also included in the figures and this, along with the network grant figures, results in a more comprehensive value of the total rail subsidy. The allocation also takes into account the Government subsidy per passenger kilometre by train operating company – Table 1.7 from the office of Rail and Road (ORR). The methodology does not include direct DfT grants to capital projects.

Methodological improvements to the rail subsidy allocation mean that estimates are not directly comparable with years’ prior to FYE 2011.

The average value attributed to households for rail and bus travel subsidies, in FYE 2017, was £173.

Notes for: final income

- A quasi-public corporation is a privately operated corporation with some form of government backing, and specifically mandated responsibilities that are stated in the corporation's legal charter.

Back to table of contents

9. Measuring inequality

There are a number of different ways in which inequality of household income can be presented and summarised. Detailed analysis of income inequality from the effects of taxes and benefits (ETB) estimates was published on 8 April 2016 in the “effects of taxes and benefits on income inequality, 1977 to financial year ending 2015”.

Presenting income inequality: Lorenz curve and income shares

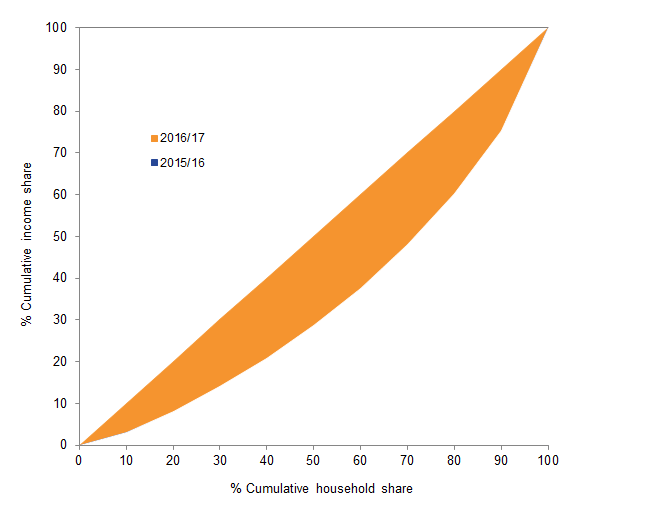

Income inequality can be illustrated graphically using a Lorenz curve. A Lorenz curve is created by ranking households from poorest to richest and graphing the cumulative share of household income and the cumulative share of households, as proportions of the total household income and the total number of households, respectively. The cumulative share of households gives a 45 degree line. When the cumulative share of income also gives a 45 degree line, this represents a situation where income is equally divided amongst all households. Higher income inequality is represented by an increase in the area between the cumulative share of household income curve and the cumulative share households curve. Where all the area under the 45 degree line is shaded, income is at its most unequal – all income is held by one household.

If the lines for the respective years crossed the situation would be less clear from a visual inspection alone. At the points where the more recent line was closer to the 45 degree line than the earlier line it could be said that, for this section of the income distribution, inequality had increased over the time period. Similarly, where the more recent line was further away from the 45 degree line than the earlier line it could be said that, for this section of the income distribution, inequality had decreased. Thus, from a visual inspection it would not be clear whether overall inequality had reduced or increased over the time period.

Using data from this analysis, Figure 4 shows Lorenz curves for equivalised disposable income (using the modified-OECD scale). In the previous period (financial year ending (FYE) 2015 and FYE 2016) inequality decreased marginally. Figure 4 shows that in FYE 2016 and FYE 2017 income inequality remained unchanged, which previously occurred in the FYE 2013 to FYE 2015.

Figure 4: Lorenz curve by equivalised disposable income for all households1, UK, between financial year ending 2016 and financial year ending 2017

Source: Office for National Statistics – The effects of taxes and benefits on household income

Notes:

- Households are ranked by equivalised disposable income, using the modified–OECD scale.

Download this image Figure 4: Lorenz curve by equivalised disposable income for all households^1^, UK, between financial year ending 2016 and financial year ending 2017

.png (14.4 kB){kind=link}

Another way of presenting income inequality is to compare income shares for different deciles or quintiles of the population. Figure 5 shows the proportion of aggregate income held by each decile. Overall there was very little change between FYE 2016 and FYE 2017.

Figure 5: Percentage of equivalised disposable income held by each decile1, UK, between financial year ending 2016 and financial year ending 2017

Source: Office for National Statistics – The effects of taxes and benefits on household income

Notes:

- Households are ranked by equivalised disposable income, using the modified-OECD scale.

Download this chart Figure 5: Percentage of equivalised disposable income held by each decile^1^, UK, between financial year ending 2016 and financial year ending 2017

Image .csv .xlsSummary measures of income inequality

Gini Coefficient

It is possible to summarise a Lorenz curve in a single figure – a Gini coefficient. The Gini coefficient is probably the most commonly used measure of income inequality internationally and is effectively a summary of the differences between each household in the population and every other household in the population. Using the Lorenz curve, the Gini coefficient is calculated by taking the ratio of the shaded area and the area below the 45 degree line of perfect equality (the 45 degree line triangle). A distribution of perfectly equal incomes has a Gini coefficient of zero (or 0%). As inequality increases, and the Lorenz curve bellies out, so does the Gini coefficient, until it reaches its maximum value of 1 (or 100%).

One of the main strengths of the Gini is that it takes into account changes in relative incomes in all areas of the income distribution. It is always the case that an increase in the income of a household with an income greater than the median will lead to an increase in the Gini coefficient, as will a decrease in the income of a household whose income is below the median. The size of this increase in the coefficient will depend on the proportion of households that have an income between the median and that of the household whose income has changed.

An improved process for calculating the Gini Coefficient has been implemented from the FYE 2016 analysis which has resulted in a change to the levels of rounding applied. Although not significant, there are minor differences to previously published Gini estimates.

The Gini coefficient for disposable income in FYE 2017 was 32.2%, compared with the FYE 2016 value of 31.6%.

Original income is more unequal for retired households than for non-retired households (Gini coefficients of 58.0% and 42.9% respectively, in FYE 2017). This is because the majority of those who are retired have little income from wages and salaries as they are not active in the labour market. In contrast, the Gini coefficient for gross income is markedly reduced among retired households (29.8%) and is smaller than the equivalent Gini coefficient for non-retired households (35.4%), in FYE 2017. This is primarily because of the addition of the state pension and pension credit. Inequality, as measured by the Gini coefficient, is lower for retired households at both the disposable and post-tax income stages than for non-retired households. In recent years, there is evidence of an increase in inequality for retired households. Compared with the most recent low point, in FYE 2010, the Gini coefficient for disposable income amongst retired households has increased significantly by 3.7 percentage points. This in part reflects a growing gap between retired households in receipt of income from private pensions and those without private pensions (see What has happened to the income of retired households in the UK over the past 40 years?).

There has been more year-on-year variation in the Gini coefficients for retired households than for the overall population, though this is primarily a consequence of the smaller sample size on which these estimates are based.

In all Gini coefficients shown, income measures are equivalised using the modified-OECD scale. Strictly speaking, it could be argued that the equivalence scales used here are only applicable to disposable income because this is the only income measure relating directly to spending power. Since the scales are often applied, in practice, to other income measures, it is considered appropriate to use them to equivalise original, gross and post-tax income for the purpose of producing Gini coefficients. However, it is not felt to be appropriate to equivalise the final income measure because this contains notional income from benefits in kind (such as that from the NHS): the equivalence scales used in this analysis are based on actual household spending and do not, therefore, apply to such items as notional income.

The effectiveness of taxes and benefits in reducing inequality can be investigated by looking at the changes in the Gini coefficients at each stage of the redistributive process. As illustrated in Figure 6, cash benefits had the largest effect in reducing inequality of both retired and non-retired households, leading to a 28.2 and 7.5 percentage point reduction in the relative Gini coefficients, respectively. As stated above, the primary reason for the large effect on the inequality of incomes of retired households is the addition of income from the state pension and pension credits. Direct taxes reduced inequality for both retired and non-retired households by 1.8 and 2.9 percentage points, respectively. Indirect taxation increased inequality by 4.8 percentage points for retired and 3.9 percentage points for non-retired households. Measured in these terms, taken as a whole, in FYE 2017 the UK tax and benefits system reduced inequality. Progressive direct taxes and cash benefits outweighed slightly regressive indirect taxation.

Figure 6: Percentage point change in Gini coefficient resulting from cash benefits and taxes, UK, between financial year ending 2016 and financial year ending 2017

Source: Office for National Statistics – The effects of taxes and benefits on household income

Notes:

- Households are ranked by equivalised disposable income, using the modified-OECD scale.

Download this chart Figure 6: Percentage point change in Gini coefficient resulting from cash benefits and taxes, UK, between financial year ending 2016 and financial year ending 2017

Image .csv .xlsOther summary measures

The characteristics of the Gini coefficient make it particularly useful for making comparisons over time, between countries and before/after taxes and benefits. However, no indicator is completely without limitations and one drawback of the Gini is that, as a single summary indicator, it cannot distinguish between different shaped income distributions. For that reason, it is useful to look at this index alongside other measures of inequality. One such measure is the S80/S20 ratio, which is the ratio of the total income received by the 20% of households with the highest income to that received by the 20% of households with the lowest income. Another related measure is the P90/P10 ratio. This is the ratio of the income of the household at the bottom of the top decile to that of the household at the top of the bottom decile.

A relatively recently developed inequality measure, the Palma ratio, takes the ratio of the income share of the richest 10% of households to that of the poorest 40% of households. The idea behind using the Palma ratio is that middle 50% of households are likely to have a relatively stable share of income over time, and hence isolating them, should not lead to a substantial loss of information (Cobham and Sumner, 2013). Together these measures provide further evidence on how incomes are shared across households and how this is changing over time.

Figure 7 shows how each of these measures has changed over time in the UK, based on the effects of taxes and benefits on household income data.

Figure 7: Change in Gini coefficient, S80/S20 ratio, P90/P10 ratio and Palma ratio for equivalised disposable income, UK, 1977 to between financial year ending 2016 and financial year ending 2017

Source: Office for National Statistics – The effects of taxes and benefits on household income

Download this chart Figure 7: Change in Gini coefficient, S80/S20 ratio, P90/P10 ratio and Palma ratio for equivalised disposable income, UK, 1977 to between financial year ending 2016 and financial year ending 2017