Table of contents

- Main points

- Things you need to know about this release

- What is average disposable income?

- How are figures compared over time?

- Private pensions are the main reason for the rising disposable income of retired households

- Inequality of disposable income has increased slightly in recent years

- Households in receipt of a private pension had disposable incomes that were 1.6 times higher than households that were not

- What do we know about those currently saving for retirement using workplace pensions?

- Definitions

1. Main points

In 1977, only around one-fifth (21%) of retired households had an annual disposable income of over £10,000 (after accounting for inflation and household composition) but by financial year ending (FYE) 2016, this had increased to 96% of retired households.

Over half of the increase in the income of retired households between 1977 and FYE 2016 can be attributed to increased private pension income alone, which has increased nearly sevenfold over the period.

Despite the growth in the average disposable income of retired households, inequality between retired households has shown increases in recent years, though they remain small relative to increases in income inequality for retired households seen throughout the 1980s.

In FYE 2016, retired households in receipt of a private pension had disposable incomes that were 1.6 times higher than households that were not.

Although since FYE 2011 the average value of cash benefits for retired households has generally been increasing, those without any form of private pension income are not having their incomes supplemented enough by these cash benefits amounts to reduce overall inequality in income.

2. Things you need to know about this release

In this release, private pensions include all workplace pensions, individual personal pensions and annuities. The State Pension has been classified as a cash benefit.

The inequality measure used is the Gini coefficient, which varies between 0 and 100. The lower the value, the more equally household income is distributed.

A retired person is defined as anyone who describes themselves (in the Living Costs and Food Survey) as “retired” or anyone over minimum National Insurance pension age describing themselves as “unoccupied” or “sick or injured but not intending to seek work”. A retired household is defined as one where the combined income of retired members accounts for the majority of the total gross income of the household.

This article looks at changes in the income and inequality of retired households over time. To make robust comparisons, historic data have been adjusted for the effects of inflation using the Consumer Prices Index including owner occupiers' housing costs (CPIH), excluding Council Tax, and income is expressed in financial year ending 2016 prices, referred to also as changes “in real terms”.

This publication requires a deflator that dates back to 1977. The CPIH, excluding Council Tax, is currently available from January 2005. The Consumer Prices Index (CPI) dates back to 1996, but a modelled historical series is available dating back to 1950. For this analysis, the owner occupiers’ housing costs (OOH) component was estimated using the actual rental series available from the Retail Prices Index (RPI). The OOH component was factored into the CPI (and modelled CPI prior to 1996) using the average OOH weight. Prior to 2005 this series is experimental.

Pension income amounts depend on an individual’s decisions throughout their working lives, and therefore changes in data in recent years could be as a result of decisions taken decades ago about pension participation and investment.

Back to table of contents3. What is average disposable income?

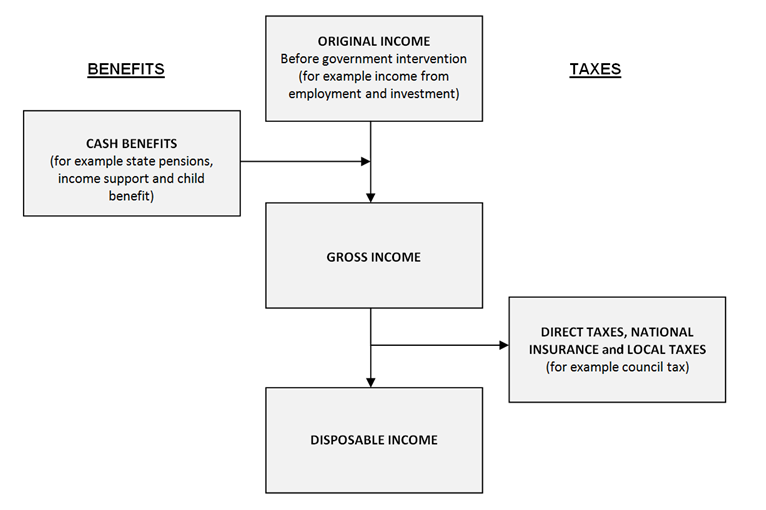

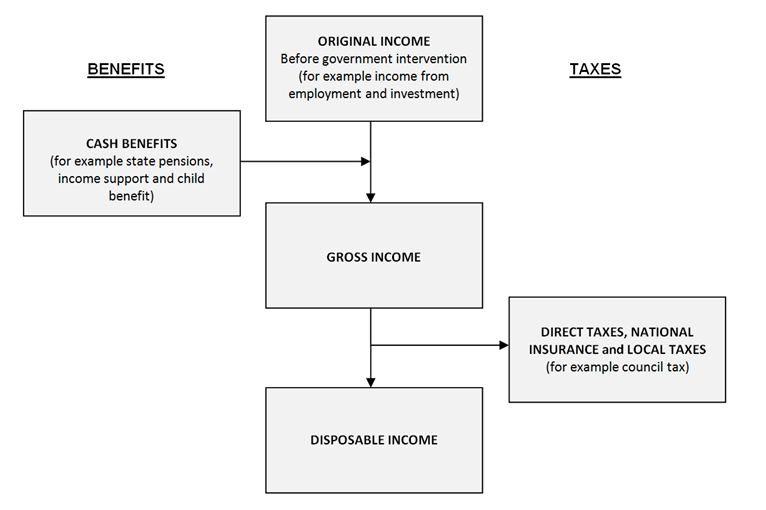

This article uses three main measures of income. While disposable income is arguably the most widely used household income measure, the use of original and gross income enables comparison of the effects of different stages of the taxes and benefits system (Figure 1). Disposable income is the amount of money that households have available for spending and saving after direct taxes (such as Income Tax and Council Tax) have been accounted for. It includes earnings from employment, private pensions and investments, as well as cash benefits provided by the state.

Figure 1: Redistribution of Income

Source: Office for National Statistics

Download this image Figure 1: Redistribution of Income

.PNG (62.3 kB){kind=link}

Two main measures of average household disposable income are used in this article: the mean and the median. The median is used when looking at the average income of a particular group of households, while the mean is used when looking at the sources of earnings, benefits and taxes that make up the overall income measures.

The mean simply divides the total income of households by the number of households. A limitation of using the mean for this purpose is that it can be influenced by just a few households with very high incomes and therefore does not necessarily reflect the standard of living of the “typical” household.

Many researchers argue that growth in median household incomes provides a better measure of how people’s well-being has changed over time. The median household income is the income of what would be the middle household, if all households in the UK were sorted in a list from poorest to richest. As it represents the middle of the income distribution, the median household income provides a good indication of the standard of living of the “typical” household in terms of income.

Back to table of contents4. How are figures compared over time?

This article looks at changes in the income and inequality of retired households over time. To make robust comparisons, historic data have been adjusted for the effects of inflation and income is expressed in financial year ending 2016 prices, referred to also as changes “in real terms”.

Household incomes have also been equivalised to take account of changes in household composition over time. Equivalisation is the process of accounting for the fact that households with many members are likely to need a higher income to achieve the same standard of living as households with fewer members. Equivalisation takes into account the number of people living in the household and their ages, acknowledging that whilst a household with two people in it will need more money to sustain the same living standards as one with a single person, the two-person household is unlikely to need double the income.

This analysis uses the modified-Organisation for Economic Co-operation and Development (OECD) equivalisation scale.

Back to table of contents5. Private pensions are the main reason for the rising disposable income of retired households

Since 1977, the income of retired households has grown considerably. Recent analysis has shown that between 1977 and financial year ending (FYE) 2016, the disposable income of retired households increased at an average annual rate of 2.8% after accounting for inflation and changes to household composition. This compares to average annual growth in non-retired households of 2.1%.

Furthermore, the economic downturn had a smaller effect on retired households, with median income in FYE 2016 at 13.0% higher than pre-downturn levels in FYE 2008, while the income for non-retired households decreased by 1.2% over the same period.

Figure 2: Distribution of disposable income

UK, 1977 and financial year ending 2016

Source: Office for National Statistics

Notes:

- 1977 refers to the calendar year, while FYE 2016 refers to the financial year ending 2016 (April 2015 to March 2016).

Download this chart Figure 2: Distribution of disposable income

Image .csv .xlsIn 1977 only around one-fifth (21%) of retired households had a disposable income over £10,000 a year (after accounting for inflation and household composition), but by FYE 2016, this had increased to 96% (Figure 2).

The mean gross income of retired households (which includes cash benefits but before direct taxes) was £29,000 in FYE 2016, almost three-times higher in real terms than in 1977 (£10,500). This compares with the gross income of non-retired households, which just over doubled over the same time period (from £20,200 in 1977 in real terms to £41,900 in FYE 2016).

Figure 3: Average gross incomes of retired households by component type

UK, 1977 to financial year ending 2016

Source: Office for National Statistics

Notes:

Years are calendar years until 1993 and financial years thereafter. Therefore, 1995 refers to financial year ending 1995 (April 1994 to March 1995) through to 2016, which refers to financial year ending 2016 (April 2015 to March 2016).

FYE = financial year ending

Download this chart Figure 3: Average gross incomes of retired households by component type

Image .csv .xlsThe majority of the income of retired households comes from state and private pensions (Figure 3). Over half of the increase between 1977 and FYE 2016 can be attributed to increased private pensions income alone, which has increased nearly sevenfold over the period (from £1,800 in 1977 to £12,400 in FYE 2016). This is due to both an increase in the proportion of households receiving private pension income, and also increases in the amounts they receive.

Income from State Pensions also increased, almost doubling between 1977 (£5,600) and FYE 2016 (£11,000), with the effect of the “triple lock”1 maintaining growth in recent years.

Notes for: Private pensions are the main reason for the rising disposable income of retired households

- The “triple lock” guarantees to increase the basic State Pension by the higher of Consumer Prices Index (CPI) inflation, average earnings or a minimum of 2.5% every year.

6. Inequality of disposable income has increased slightly in recent years

Inequality of original income (income before cash benefits, including the State Pension, and direct taxes) has been on a downward trend since the 1980s (Figure 4). One reason for this fall is the increasing proportion of retired households receiving income from private pensions throughout this period, from 45% in 1977 to nearly 80% in financial year ending (FYE) 2016.

Inequality of gross income (income including cash benefits such as the State Pension) is much lower, showing that cash benefits have a significant role in reducing income inequality within retired households. Inequality is also lower for disposable income (which includes direct taxation) although in this case the reduction in the Gini coefficient between gross and disposable income is much smaller than that between original and gross income, indicating that direct taxes are having a much smaller effect on reducing income inequality of retired households.

Despite this, since FYE 2010, income inequality of gross and disposable income has shown an upward trend, though it remains small relative to larger increases seen in the 1980s. This indicates that cash benefits have become less effective at reducing inequality in recent years.

Figure 4: Inequality between retired households for different income measures

UK, 1977 to financial year ending 2016

Source: Office for National Statistics

Notes:

The inequality measure used is the Gini coefficient.

FYE = financial year ending

Download this chart Figure 4: Inequality between retired households for different income measures

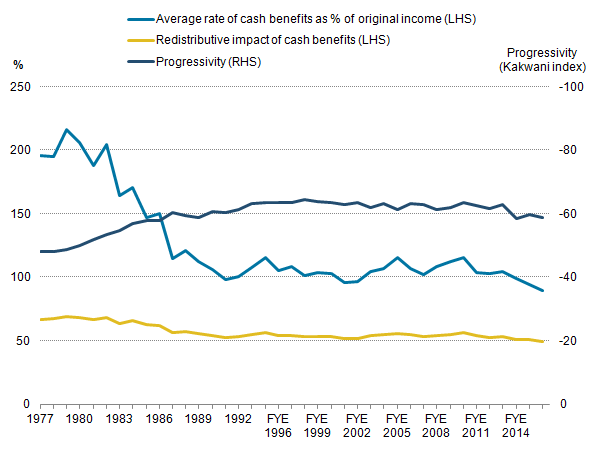

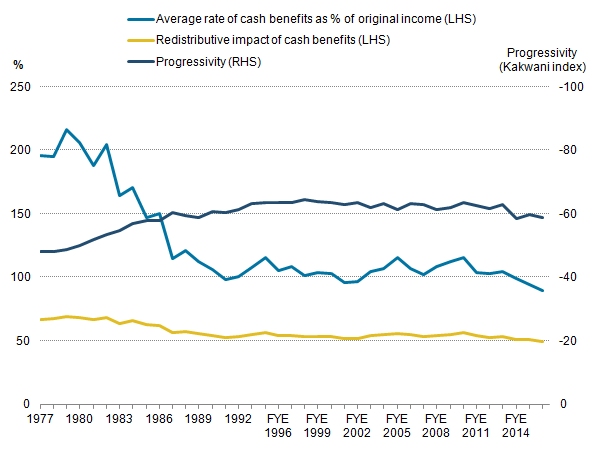

Image .csv .xlsThe effectiveness of cash benefits depends on two things: the average rate of the benefit (this represents how big the amount is relative to original income) and how targeted it is at reducing inequality; the latter is measured both by the degree to which it reduces the Gini coefficient and its progressivity1.

Figure 5 shows the average rate of cash benefits as a percentage of original income, their progressivity (measured using the Kakwani index) and the redistributive impact on the inequality (measured by the reduction in the Gini coefficient) between 1977 and FYE 2016. For all three measures an upward movement shows an increase in the effectiveness of cash benefits and vice versa.

Figure 5: Progressivity, average rate and overall redistributive impact of cash benefits

UK, 1977 to financial year ending 2016

Source: Office for National Statistics

Notes:

The redistributive impact of cash benefits is measured using the percentage reduction in the Gini coefficient as a result of accounting for cash benefits.

For progressivity (measured using the Kakwani index), a negative value indicates that cash benefits are progressive and acting to reduce the level of inequality. The larger the negative value, the more progressive the benefit is.

FYE = financial year ending

Download this image Figure 5: Progressivity, average rate and overall redistributive impact of cash benefits

.png (15.9 kB) .xls (27.6 kB){kind=link}

When considering an average household, in the late 1970s, cash benefit amounts for retired households were around twice the amount they received from original income. During the 1980s the rate declined and by the early 1990s, cash benefit amounts were at around the same level as original income. Following this was a period of fluctuation in which they were generally higher than original income, but since FYE 2013, they have fallen. This means that, as a proportion of household income, cash benefits now make up a smaller amount.

Similarly, since FYE 2013, the redistributive impact of cash benefits and their progressivity has also fallen. Combined, these measures show that the effectiveness of cash benefits in reducing income inequality has fallen in recent years, as more retired households increasingly rely on their private pension income to provide their income in retirement.

Notes for Inequality of disposable income has increased slightly in recent years

- Cash benefits are considered to be progressive where they account for a larger share of the income of low-income groups. Progressivity is measured using the Kakwani index (Kakwani, 1977). For benefits, a negative value indicates that the benefits are progressive and acting to reduce the level of inequality. The larger the negative value, the more progressive the benefit is.

7. Households in receipt of a private pension had disposable incomes that were 1.6 times higher than households that were not

The gap between the average amounts of household income for those with and without a private pension has been increasing since 1977, especially in recent years (Figures 6 and 7). In financial year ending (FYE) 2016, those with a private pension had average original income 14 times higher than those who did not receive any private pension income; that is, £19,000 compared with £1,300 respectively.

Figure 6: Average original income of those with and without private pensions

UK, 1977 to financial year ending 2016

Source: Office for National Statistics

Notes:

- FYE = financial year ending

Download this chart Figure 6: Average original income of those with and without private pensions

Image .csv .xlsCash benefits and direct taxes act to reduce the gap between those with and without private pensions, but the disposable income of retired households with a private pension in FYE 2016 on average was still 1.6 times higher than those without a private pension, at £27,800 compared with £17,200 respectively.

Figure 7: Average disposable incomes with and without private pensions

UK, 1977 to financial year ending 2016

Source: Office for National Statistics

Notes:

- FYE = financial year ending

- 9 August 2017 - 'Please note that the chart originally supplied was not shown in 15/16 prices. This has since been rectified

Download this chart Figure 7: Average disposable incomes with and without private pensions

Image .csv .xlsWhilst the majority of the gap in average incomes can be attributed to private pension income, households that are in receipt of private pension income also tend to have higher average income from employment and investment income than households that receive no private pension income.

Figure 8: Ratio of the average disposable income of those with private pensions to those without

UK, 1977 to financial year ending 2016

Source: Office for National Statistics

Notes:

- FYE = financial year ending

Download this chart Figure 8: Ratio of the average disposable income of those with private pensions to those without

Image .csv .xlsIn fact, cash benefits are the only income source that is higher for those who do not receive private pension income. For this reason, cash benefits have historically reduced the gap in average incomes between households with and without private pensions. However, since FYE 2011, despite annual increases in the rate of State Pension, the relative gap in disposable income has increased and is now at its largest since the series began (Figure 8). This shows that since FYE 2011, the growth in average income as a result of private pensions has outstripped the growth deriving from the State Pension.

Back to table of contents8. What do we know about those currently saving for retirement using workplace pensions?

The incomes of retired households now largely reflect both pension behaviour and pension policy in the past. Recent analysis of pension wealth show considerable changes over the past 40 years.

The Annual Survey of Hours and Earnings (ASHE) release shows that the largest category of workplace pensions in 2016 continued to be private occupational defined benefit schemes, which accounted for 43% of workplace schemes. This is considerably lower than in 1997 when records began, when they accounted for 83%. This suggests a shift from defined benefit to defined contribution schemes over the last 2 decades, as many defined benefit schemes are now closed to new members and newer schemes tend to be defined contribution. This change is reflected when looking at the proportion of employees with workplace pensions by age band and pension type. A higher proportion of those in age categories under 30 years are in defined contribution schemes, whereas a higher proportion of those in age categories 30 years and over are in defined benefit schemes (see Figure 4 from the Annual Survey of Hours and Earnings (ASHE) pension tables).

The number of employees enrolled into workplace pension schemes is at a record high, due in part to the effect of automatic enrolment since October 2012. The largest increases in participation between 2015 and 2016 were in defined contribution pension schemes. In these schemes, employer and employee pension contributions tend to be lower than for defined benefit schemes, and the effect of automatic enrolment has shown a step change in the data as the majority of employees have moved to paying greater than 0% but less than 4% of their pensionable income. This contrasts with the majority of employees in defined benefit schemes paying 7% of more of their pensionable income.

The Wealth and Assets Survey (WAS) also collects data on whether individuals are contributing to private pensions, but in addition estimates the value of these current pension pots as well as the value of any retained pension pots that the individual is no longer contributing to. Looking at wealth held by individuals in private pensions1 from which they were not yet drawing an income (accumulated wealth), the median amount of wealth in pensions that are not yet in payment is much higher for defined benefit pension schemes than defined contribution schemes (£63,400 and £15,000 respectively – see Table 6.8 from Wealth in Great Britain 2012 to 2014).

Between July 2010 to June 2012 and July 2012 to June 2014, the median for defined benefit schemes increased considerably for all age categories. The age group with the highest value of defined benefit pension wealth was those aged 55 to 64 years (with a median of £161,600 in July 2012 to June 2014 compared with £117,200 in July 2010 to June 2012). Over the same period there was no growth in the median value of the accumulated wealth in defined contribution schemes (£15,000 for all age groups in both periods and £25,000 for those aged 55 to 64 years).

The increase in the wealth of defined benefit schemes is driven by a decrease in annuity rates – which are collected from financial markets and change over time – between waves 3 (July to June 2012) and waves 4 (July to June 2014) of the Wealth and Assets Survey. The higher the annuity rate the greater the annual retirement income that can be bought with a fixed amount of defined contribution pension wealth (pension pot). If annuity rates increase then the defined benefit wealth calculated using those annuity rates will decrease. The opposite is also true; if annuity rates decrease, then the defined benefit wealth calculated using those annuity rates will increase. More information on the methodology, as well as further information on pensions, can be found in our Wealth in Great Britain Wave 4 release.

Notes for: What do we know about those currently saving for retirement using workplace pensions?

- This includes pension wealth in current and retained pensions from both occupational and personal pensions. Defined benefit (DB) type pension wealth comprises current DB and retained rights in DB pensions. Defined contribution (DC) type pension wealth comprises current DC occupational pensions, current personal pensions, AVCs, retained rights in DC pensions, and retained pensions for drawdown.

9. Definitions

Automatic enrolment

Under reforms brought in by the Pensions Act 2008, with updates in the Pensions Act 2011 and Pensions Act 2014, employers must enrol all eligible employees into a qualifying private pension. Workers can opt out but will be re-enrolled every 3 years and need to opt out each time. Automatic enrolment has a staged implementation to 2018 and started with the larger employers in 2012. (See also the section Workplace pension reforms, Pension Trends, Chapter 6: Private Pensions, 2013 edition, and Department for Work and Pensions: Automatic Enrolment Evaluation Report 2016).

Defined benefit scheme

A pension scheme in which the rules specify the rate of benefits to be paid. The most common defined benefit scheme is a salary-related scheme in which the benefits are based on the number of years of pensionable service, the accrual rate and either the final salary, the average of selected years’ salaries or the best year’s salary within a specified period before retirement.

Defined contribution scheme

A pension scheme in which the benefits are determined by the contributions paid into the scheme, the investment return on those contributions, and the type of annuity (if any) purchased upon retirement. It is also known as a money purchase scheme. Defined contribution pensions may be private, personal or stakeholder pensions.

Private pension scheme

An arrangement (other than accident or permanent health insurance) organised by an employer (or on behalf of a group of employers) to provide benefits for employees on their retirement and for their dependants on their death. In the private sector, private schemes are trust-based. Private pension schemes are a form of workplace pension.

Workplace pension

A workplace pension is a pension that is provided or facilitated by a workplace, principally for employees. It includes both private pension schemes and all forms of group personal and group stakeholder pensions. Further definitional information is available in our Annual Survey of Hours and Earnings publication.

Back to table of contents