Table of contents

- Main points

- Things you need to know about this release

- Summary of net lending or borrowing positions by sector

- Real household disposable income

- Households’ saving ratio

- Links to related statistics

- Links to related analysis

- Upcoming changes to this bulletin

- Upcoming articles

- Quality and methodology

- Appendix A: key economic indicators

- Appendix B: additional information on the alternative measures of households’ income and savings

- Acknowledgements

1. Main points

In Quarter 1 (Jan to Mar) 2019, UK net borrowing from the rest of the world increased slightly to 5.6% of gross domestic product (GDP), the highest position since Quarter 3 (July to Sept) 2016.

In the latest quarter, financial corporations, government and households experienced increases in their net borrowing positions, offset by a reduction in private non-financial corporations’ net borrowing.

Quarter 1 2019 was an unprecedented 10th consecutive quarter of households being net borrowers; households saw their net borrowing increase to 1.3% of GDP from 0.8% in the previous quarter.

Households’ saving ratio decreased to 4.1%, compared with 4.5% in the previous quarter, as growth of household expenditure outpaced household incomes.

The households’ saving ratio remained historically low and was the joint fourth-lowest quarterly saving ratio since records began in 1963.

Including this quarter, six of the seven lowest households’ saving ratios have been recorded since Quarter 1 (Jan to Mar) 2017; the exception being the saving ratio of 3.6% recorded in Quarter 2 (Apr to June) 1963.

2. Things you need to know about this release

This bulletin includes new data for the latest available quarter, Quarter 1 (Jan to Mar) 2019. There are no revisions to previously published data in this quarter. This bulletin follows the National Accounts Revisions Policy.

The alternative measures of households’ income and saving

Following changes introduced in our previous bulletin, this release now incorporates the alternative measures of real households’ disposable income and saving.

This decision was made as a result of growing user interest in the Alternative measures of households’ income and saving experimental statistics since their launch in August 2015.

In effect, the underlying data has been moved into the Households chapter (Chapter 6) of the UK Economic Accounts and the accompanying analysis onto this bulletin. They are both released on the same day. Previously, the alternative measures of real household disposable income and households’ saving ratio were released roughly a week later.

We hope users find this timelier analysis of households’ financial situation useful and helpful, and we continue to welcome feedback by email at sector.accounts@ons.gov.uk.

Understanding the sector and financial accounts

This bulletin presents analysis on UK aggregate data for the main economic indicators and summary estimates from the institutional sectors of the UK economy that are presented in the UK Economic Accounts (UKEA) dataset:

- public corporations

- private non-financial corporations

- financial corporations

- households

- non-profit institutions serving households (NPISH)

- central government

- local government

- rest of the world

This bulletin uses data from the UKEA and it provides detailed estimates of national product, income and expenditure, UK sector, non-financial and financial accounts, and UK Balance of Payments. These accounts are the underlying data that produce a single estimate of gross domestic product (GDP) using income, production and expenditure data.

Further information on the calculation of some of our main economic indicators can be found in the Quality and methodology section of this bulletin.

Estimates within this release

All data within this bulletin are estimated in current prices (also called nominal prices), except for real household disposable income, which is estimated in chained volume terms.

Current price series are expressed in terms of the prices during the time period being estimated. These describe the prices recorded at the time of production or consumption and include the effect of price inflation over time. Chained volume series (also known as real terms) have had the effects of inflation removed.

All figures given in this bulletin are adjusted for seasonality, unless the financial accounts are under discussion or otherwise stated. Seasonal adjustment removes seasonal or calendar effects from data to enable more meaningful comparisons over time.

The Population estimates for the UK, England and Wales, Scotland and Northern Ireland used in this release are those published on 28 June 2018.

Back to table of contents3. Summary of net lending or borrowing positions by sector

Figure 1: UK net borrowing from the rest of the world increased to 5.6% of GDP in the latest quarter; the highest position since Quarter 3 (July to Sept) 2016

Net lending (+) or borrowing (-) position as a percentage of gross domestic product, non-financial account, seasonally adjusted, UK, Quarter 1 (Jan to Mar) 1987 to Quarter 1 (Jan to Mar) 2019

Source: Office for National Statistics

Notes:

- Sum of net lending or borrowing positions may not sum to zero in later years due to unbalanced Supply and Use tables in the compilation of GDP. To find out more see: Balancing the Three Approaches to Measuring Gross Domestic Product, 2012.

Download this chart Figure 1: UK net borrowing from the rest of the world increased to 5.6% of GDP in the latest quarter; the highest position since Quarter 3 (July to Sept) 2016

Image .csv .xlsThe UK was a net borrower from the rest of the world in Quarter 1 (Jan to Mar) 2019, with net borrowing at 5.6% of gross domestic product (GDP); up from 4.6% in the previous quarter and the highest since Quarter 3 (July to Sept) 2016 when they were net borrowers of 6.5% of GDP. This means that the UK spent and invested more than it received in incomes, suggesting a need to sell off assets or build up further liabilities. It is the 82nd consecutive quarter starting in Quarter 3 1998 in which the UK has been a net borrower.

Despite overall reductions in the annual net borrowing position of general government in the last decade, all other UK sectors have experienced a movement in the opposite direction over the same period. Private non-financial corporations returned to being annual net borrowers in 2012, after being net borrowers in only 2 of the 10 years before that (2006 and 2007). Furthermore, households became annual net borrowers in 2017 for the first time since 1988 and have continued to be net borrowers into 2019.

As a result, UK net borrowing from the rest of the world has been 4% of GDP (or higher) in five of the last six years (since 2013). Before 2013, the UK had only experienced a net borrowing position greater than 4% of GDP on two occasions (1989 and 2008) since records began in 1987.

Figure 2: UK net borrowing was driven by greater net borrowing by financial corporations and households, offset by a fall in non-financial coporations' net borrowing

Net lending (+) or borrowing (-) position by sector as a percentage of gross domestic product, seasonally adjusted, UK, Quarter 1 (Jan to Mar) 2012 to Quarter 1 (Jan to Mar) 2019

Source: Office for National Statistics

Notes:

- NPISH = Non-profit institutions serving households. 2. Sum of net lending or borrowing positions may not sum to zero in later years due to unbalanced Supply and Use tables in the compilation of GDP. To find out more see: Balancing the Three Approaches to Measuring Gross Domestic Product, 2012

Download this chart Figure 2: UK net borrowing was driven by greater net borrowing by financial corporations and households, offset by a fall in non-financial coporations' net borrowing

Image .csv .xlsFinancial corporations

In the latest quarter, financial corporations were the main contributor to the UK’s net borrowing position. In Quarter 1 2019, their net borrowing position increased to 1.8% of GDP, up from 1.0% of GDP in the previous quarter.

The cause of this quarterly increase in their net borrowing position was an increase of £8.5 billion in the acquisition less disposal of valuables, compared with their net disposal of valuables in the previous quarter. Particularly, financial corporations acquired unspecified goods, which includes non-monetary gold (NMG).

Offsetting the acquisition of valuables, financial corporations saw a fall in the amount of reinvested earnings on direct foreign investment they paid of £2.7 billion and in the amount of dividend income they paid to shareholders of £2.3 billion.

In their financial account, financial corporations increased their issuance by £9.3 billion of net loans (loan assets minus loan liabilities) in Quarter 1 2019 compared with an increase of £147.7 billion of net loans issued in the previous quarter. Therefore, financial corporations saw a fall in net loans of £138.5 billion in Quarter 1 2019. This was the largest quarterly decrease since Quarter 1 2014 and reflects a fall in the amount of short-term foreign currency loans issued by UK banks to other institutions in the UK financial sector and to the rest of the world.

The fall in short-term loans is related to a widespread fall in sale and repurchase agreements, also known as “repos”, this quarter. A repo is an agreement made between two parties whereby the buyer of the repo (the borrower) sells securities to another party (the lender) with a legally binding agreement that they will repurchase the securities at a later date.

General government

General government (which includes both central and local government) was the second-largest contributor to the UK’s net borrowing position.

In Quarter 1 2019, general government net borrowing marginally increased to 1.7% of GDP, from 1.5% in the previous quarter. Both the central and local government sectors saw a 0.1% increase in their net borrowing in the latest quarter.

Local government

Quarter 1 2019 saw an increase in local government’s net borrowing position to 0.4% of GDP, compared with 0.3% in the previous quarter.

Driving this movement was a £0.7 billion increase in subsidies paid out by local government to public corporations. These subsidies relate to injections into the Housing Revenue Account.

Further analysis on local government can be found in Public sector finances, UK: May 2019.

Central government

Quarter 1 2019 saw an increase in central government’s net borrowing position to 1.3% of GDP, compared with 1.2% in the previous quarter. The main cause of this movement was a rise in final consumption expenditure by central government.

Offsetting increased expenditure was an increase in taxes on income received by central government. This is due mainly to a rise in self-assessment Income Tax receipts. The Office for Budget Responsibility (OBR) has linked this latest increase to new tax rules on dividends introduced in 2017. The OBR notes that in 2017 dividend payments were brought forward ahead of the introduction of these new tax rules. Consequently, this resulted in a fall in self-assessment tax receipts in Quarter 1 2018 but an increase in the same quarter of 2019 as the impact of the introduction of the new tax rules unwound.

Further analysis on central government can be found in Public sector finances, UK: May 2019.

Private non-financial corporations

In the latest quarter, private non-financial corporations (PNFCs) saw an improvement in their net borrowing position. This decreased to 1.5% of GDP, from 2.0% in the previous quarter. PNFCs saw gross operating surplus (GOS) rise by £2.8 billion in Quarter 1 2019 compared with the previous quarter, with the services industry performing particularly well.

Offsetting this, PNFCs saw a fall of £0.9 billion on the balance of investment income on financial assets and liabilities they hold (net property income). PNFCs earned £3.0 billion more on their direct investments abroad in Quarter 1 2019 than they did in the previous quarter. However, they paid £2.8 billion more in dividends in Quarter 1 2019. This suggests that PNFCs looked to their overseas investments to pay shareholders this quarter.

In their financial account, PNFCs saw a fall of £50.0 billion in the total deposits they made in Quarter 1 2019 in comparison with Quarter 4 (Oct to Dec) 2018. However, total assets fell only £11.8 billion as PNFCs shifted to other asset types, including debt securities. PNFCs also reduced their financial liabilities by £14.3 billion in Quarter 1 2019.

Households

Quarter 1 (Jan to Mar) 2019 was the 10th consecutive quarter in which households were net borrowers in the non-financial account; a trend that began in Quarter 4 2016 (see Figure 3).

Between Quarter 1 1997 and Quarter 3 2016, households experienced an average net lending position of 2.6% of GDP. Since Quarter 4 2016, households have switched to an average net borrowing position of 1.2% of GDP. In the latest quarter, households experienced a net borrowing position of 1.3% of GDP; an increase from 0.8% of GDP in the previous quarter.

The reason for this increase in net borrowing was an increase in households’ expenditure of £2.3 billion, of which £0.8 billion is attributable to net tourism, as expenditure in the UK by foreign residents fell whilst expenditure abroad by UK residents rose. There was also a £0.7 billion increase in expenditure on life insurance.

These were partly offset by a £0.5 billion fall in expenditure on financial intermediation services indirectly measured (FISIM). FISIM is an indirect measure of the value of financial intermediation services provided but for which financial institutions do not charge explicitly.

Households built up gross capital formation (GCF) by £1.8 billion in Quarter 1 2019 in comparison with their capital formation in the previous quarter. Within GCF, households increased their net acquisitions of valuables by £0.8 billion and their holdings of inventories, including finished goods and work in progress, by £0.6 billion.

These negative contributions were partly offset by an increase in dividend income from the holding of shares of £1.1 billion.

Growth of £1.0 billion in compensation of employees was the lowest since Quarter 4 2016 (negative £0.5 billion) as a result of the weak growth in Quarter 1 2019 private sector average weekly earnings of 7.7%. This was the weakest Quarter 1 growth in the private sector since 2009 (6.6%). However, labour market conditions remain strong, as the unemployment rate fell to 3.8% in Quarter 1 2019 (it had not been lower since Quarter 4 1974) and the employment rate increased to 76.1% (the joint-highest rate since records began in 1971). To further explore the latest labour market statistics, see Labour market overview, UK: June 2019.

Figure 3 captures the deterioration of households’ finances that began in Quarter 4 2015, a deterioration that has now stabilised. Households saw a squeeze in their incomes throughout 2016 as gross disposable income grew at its weakest rate (1.3%) since 2010, while household spending on all goods and services grew at its fastest (4.8%) since 2005 – due partly to inflationary pressures pushing up the price of the same basket of goods and services.

As a result of this, households’ surplus income after expenditure shifted the sector towards deficit. The latest quarter, Quarter 1 2019, was an unprecedented 10th consecutive quarter of net borrowing for households; meaning that they either had to sell off their assets or build up further liabilities to fund their day-to-day economic activity.

In 2016, evidence suggests that households turned toward long-term loans (such as credit cards) and the disinvestment in mutual funds to fund growing expenditure during the squeeze on disposable incomes. 2017 and 2018 signalled a sharp drop in deposits made to UK banks by households, as they returned to pre-2016 levels. However, the net acquisition of long-term loans and the disinvestment in mutual funds continued throughout this period.

Figure 3: Households' net borrowing increased to 1.3% of GDP, up from 0.8%; they remain net borrowers and now for a 10th consecutive quarter

Households net lending (+) or borrowing (-) position as a percentage of gross domestic product, UK, Quarter 1 (Jan to Mar) 1997 to Quarter 1 (Jan to Mar) 2019

Source: Office for National Statistics

Download this chart Figure 3: Households' net borrowing increased to 1.3% of GDP, up from 0.8%; they remain net borrowers and now for a 10th consecutive quarter

Image .csv .xlsNon-profit institutions serving households (NPISH)

The NPISH sector (which includes, for example, charities, universities and religious organisations) is by far the smallest private sector, but it is nevertheless an important one due to the social benefits it offers UK society.

In Quarter 1 2019, NPISH saw their net lending position remain at 0.2% of GDP. It was the 17th consecutive quarter since Quarter 4 2014 in which NPISH were net lenders.

There was a slight improvement in NPISH’s net lending position in £ billion terms increasing to £1.1 billion in Quarter 1 2019 from £1.0 billion in the previous quarter. This was due mainly to a £0.5 billion rise in capital grants received from other sectors, partially offset by a £0.4 billion rise in gross capital formation.

UK activity with the rest of the world

The UK’s current and capital account deficit with the rest of the world (that is, its net borrowing position) widened in the latest quarter to 5.6% of GDP; up from 4.6% in Quarter 4 2018. The last time it was higher was in Quarter 3 2016 when the UK was a net borrower from the rest of the world at 6.5% of GDP.

In the latest quarter, the increase in the UK’s net borrowing with the rest of the world is due mainly to the widening of the UK’s trade deficit, which grew by £10.8 billion to £20.3 billion. The trade in goods deficit was particularly affected by the import of unspecified goods, which includes non-monetary gold.

Also contributing to the rise in imports in the latest quarter was an increase in trading activity of key commodities ahead of the initial deadline for the UK to leave the European Union on 31 March 2019. Finished and unfinished manufactured products saw large increases in activity in Quarter 1 2019; particularly imports of medicinal and pharmaceutical products, cars, mechanical machinery, materials manufactures and jewellery. This unusually high increase in imports in Quarter 1 2019 may suggest consumers and producers brought forward purchases that would have otherwise been spread over future period. For greater analysis on the UK’s economic activity with the rest of the world, please refer to the Balance of payments bulletin.

Back to table of contents4. Real household disposable income

Real household disposable income (RHDI) grew by 0.5% in Quarter 1 (Jan to Mar) 2019; this means that after considering price rises experienced by households, incomes after tax grew by 0.5% in the latest quarter, slowing from 1.0% growth seen by households in Quarter 4 (Oct to Dec) 2018.

Growth in nominal gross disposable household income (GDHI) contributed all of the 0.5 percentage points to RHDI growth this quarter, with a minimal contribution from inflation, as Figure 4 shows. Please note: the sum of contributions may not add to RHDI growth due to rounding.

Figure 4: Real household disposable income grew by 0.5% in the latest quarter

Real household disposable income, quarter on previous quarter growth, seasonally adjusted, UK, Quarter 1 (Jan to Mar) 1997 to Quarter 1 (Jan to Mar) 2019

Source: Office for National Statistics

Download this chart Figure 4: Real household disposable income grew by 0.5% in the latest quarter

Image .csv .xlsThe slower growth in GDHI is attributed mainly to an increase in taxes on income and wealth paid by households of £1.2 billion. This is due mainly to a rise in self-assessment Income Tax receipts.

This negative contribution to growth was offset partly by an increase in dividend income from the holding of shares of £1.1 billion.

Subdued growth of £1.0 billion in compensation of employees was the lowest since Quarter 4 2016 and contributed to lower GDHI growth. To further explore the latest labour market statistics, see Labour market overview, UK: June 2019.

Growth in the household implied deflator in Quarter 1 2019 was relatively low at 0.1% as a result of falls in the prices of financial and insurance services offset by rises in other goods and services.

Alternative measure of real household disposable income (experimental)

The alternative (and experimental) measure of RHDI removes imputed transactions from real household disposable income to better represent the economic experience of UK households. In other words, it captures the immediately accessible and directly observed “cash” available to households to spend or save at that given time point if they so wished to. Deeper detail on methodology can be found in the Alternative measures of UK households' income and saving: April to June 2018 article.

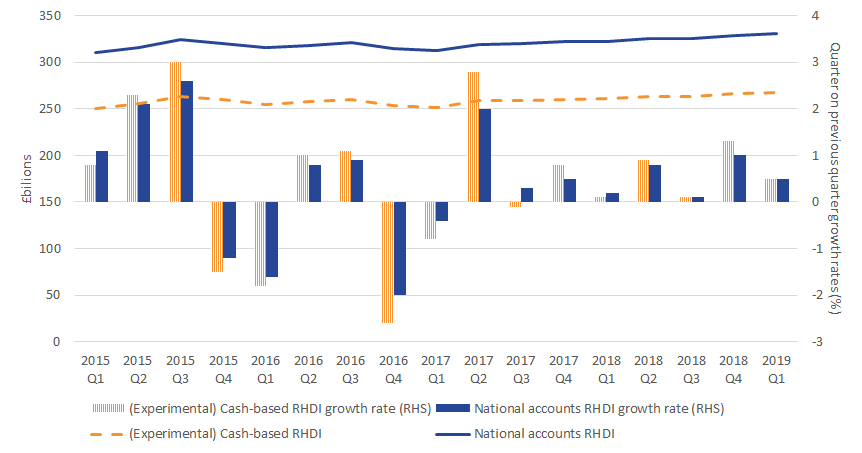

In this cash-based approach, RHDI is estimated to have increased by 0.5% in Quarter 1 2019, compared with the previous quarter. This is in line with the 0.5% RHDI growth on a national accounts basis, as Figure 5 shows.

It is also worth noting that the level of RHDI on a cash basis is approximately 19% lower than the level of RHDI on a national accounts basis. That is a difference equivalent to 12% of gross domestic product (GDP), meaning that households have 12% of GDP less to spend or save when we remove incomes not immediately accessible or directly observed.

Per head, cash-based RHDI stood at £4,013 in the latest quarter, up 0.3% from the previous quarter.

Figure 5: In the latest quarter, real households’ disposable income on a cash basis grew at the same rate as RHDI on a national accounts basis

Real households’ disposable income on a cash basis and on a national accounts basis, £ billions and growth rates, seasonally adjusted, UK, Quarter 1 (Jan to Mar) 2015 to Quarter 1 (Jan to Mar) 2019

Source: Office for National Statistics

Notes:

- RHS = Right-hand side axis.

Download this image Figure 5: In the latest quarter, real households’ disposable income on a cash basis grew at the same rate as RHDI on a national accounts basis

.png (21.5 kB) .xls (46.1 kB){kind=link}

Throughout 2018, gross operating surplus (which is made up of imputed rentals – that is, what households would pay themselves if they were to rent their own property to themselves) had been the main driver of the difference as Figure 6 shows. Any residual difference between the two series in Quarter 1 2019 is explained mainly by the removal of non-life insurance claims from the national accounts measure of GDHI offset by the removal of gross operating surplus.

Figure 6: The main difference in growth between gross disposable household income on a cash basis and a national accounts basis is non-life insurance claims

Contributions to the difference in growth rates between gross disposable household income on a cash basis and a national accounts basis, £ million, seasonally adjusted, UK, Quarter 1 (Jan to Mar) 2017 to Quarter 1 (Jan to Mar) 2019

Source: Office for National Statistics

Download this chart Figure 6: The main difference in growth between gross disposable household income on a cash basis and a national accounts basis is non-life insurance claims

Image .csv .xlsThere are six transactions that explain the differences between GHDI on a cash-basis and a national accounts basis. See Table 2 in the appendix for a list of transactions removed from the national accounts measure of RHDI to calculate the cash-based RHDI. A cash-based deflator is also applied to cash-based GHDI to remove the effect of price changes experienced by households to calculate real household disposable income on a cash-basis.

Back to table of contents5. Households’ saving ratio

The households’ saving ratio fell to 4.1% in Quarter 1 (Jan to Mar) 2019, compared with 4.5% in the previous quarter, as shown in Figure 7.

The households’ saving ratio remains historically low and is the joint fourth-lowest quarterly saving ratio since records began in 1963. Including this quarter, six of the seven-lowest households’ saving ratios have been recorded since Quarter 1 2017. The exception being the saving ratio of 3.6% recorded in Quarter 2 (Apr to June) 1963.

Figure 7: Households' saving ratio decreased to 4.1%, compared with 4.5% in the previous quarter, remaining at historically low levels

UK households saving ratio, quarterly, seasonally adjusted, Quarter 1 (Jan to Mar) 1963 to Quarter 1 (Jan to Mar) 2019

Source: Office for National Statistics

Download this chart Figure 7: Households' saving ratio decreased to 4.1%, compared with 4.5% in the previous quarter, remaining at historically low levels

Image .csv .xlsThe saving ratio captures the income households have available to save as a proportion of their total available resources (that is, current and deferred incomes). Figure 8 breaks down how much of that available income was set aside as pension savings and how much more income is available to be used for other forms of savings (for example, investment in financial and non-financial assets).

Figure 8 shows that the slight decrease in the saving ratio in Quarter 1 2019 was due to households experiencing a decrease in both pension and non-pension income available for saving. The latter was a consequence of final consumption expenditure rising more than gross disposable income.

Figure 8: Pension and non-pension savings drops in the latest quarter, as does the total income available to save

Contributions to households’ saving ratio, seasonally adjusted, UK, Quarter 1 (Jan to Mar) 1997 to Quarter 1 (Jan to Mar) 2019

Source: Office for National Statistics

Notes:

- Non-pension savings are calculated as (Gross disposable income minus households’ consumption expenditure) divided by gross disposable income.

- Pension saving is calculated as the residual between the saving ratio and non-pension savings.

Download this chart Figure 8: Pension and non-pension savings drops in the latest quarter, as does the total income available to save

Image .csv .xlsIn Quarter 1 2019, households’ expenditure rose by £2.3 billion (0.7%), of which £0.8 billion is attributable to net tourism as expenditure in the UK by foreign residents fell whilst expenditure abroad by UK residents rose. There was also a £0.7 billion increase in expenditure on life insurance.

These were offset partly by a £0.5 billion fall in expenditure on financial intermediation services indirectly measured (FISIM). Further detail on households’ final consumption expenditure, including a breakdown of households’ spending by product, can be found in the Consumer trends bulletin.

Households’ pension savings (income set aside in pension plus any change in the value of pension entitlements) fell by £1.1 billion in the latest quarter, the largest fall since Quarter 1 2017. Since Quarter 1 2017, pension savings have contributed around 3 percentage points to the saving ratio, on average. In the decade to 2017 (that is, 2007 to 2016), they contributed 5.3 percentage points on average. In the decade to 2007 (that is, 1997 to 2006), they contributed almost 6.5 percentage points on average, signalling a gradual fall in households’ pension savings over time.

Households’ non-pension savings (income available to save, other than pension) contributed an average of 1.2 percentage points to the quarterly saving ratio since Quarter 1 2017. In the decade to 2017 (that is, 2007 to 2016), they contributed 3.5 percentage points on average, higher than the decade to 2007 (that is, 1997 to 2006) where they contributed 2.0 percentage points on average.

Revisions to the saving ratio

This bulletin has no revisions to data in line with the National Accounts Revisions Policy.

Alternative measure of households’ saving ratio (experimental)

This alternative (and experimental) measure removes imputed transactions from the households’ saving ratio to better represent the economic experience of UK households. In other words, it captures the immediately accessible and directly observed “cash” available to households to spend or save at that given time point if they so wished to. Deeper detail on methodology can be found in the Alternative measures of UK households' income and saving: April to June 2018 article.

As Figure 9 shows, the cash-basis saving ratio was 1.1% in Quarter 1 2019, down 0.1 percentage points from 1.2% in the previous quarter. The national accounts saving ratio, on the other hand, decreased 0.4 percentage points to 4.1% compared with the previous quarter.

Figure 9: UK households’ cash-basis and the national accounts saving ratio both decreased in the latest quarter

UK households’ cash-basis saving ratio and national accounts saving ratio, quarterly, seasonally adjusted, percentage, Quarter 1 (Jan to Mar) 1997 to Quarter 1 (Jan to Mar) 2019

Source: Office for National Statistcs

Download this chart Figure 9: UK households’ cash-basis and the national accounts saving ratio both decreased in the latest quarter

Image .csv .xlsIn the latest quarter, driving the difference in the change between the national accounts savings ratio and the cash-basis saving ratio is the adjustment for the change in pension entitlements, as shown in Figure 10. The national accounts make this adjustment to give back to households pension income deferred for future use.

Figure 10: The main difference in growth between households' gross savings on a cash basis and a national accounts basis is the adjustment for the change in pension entitlements

Contributions to the difference in growth between households gross savings on a cash basis and a national accounts basis, £million, seasonally adjusted, Quarter 1 (Jan to Mar) 2017 to Quarter 1 (Jan to Mar) 2019

Source: Office for National Statistics

Download this chart Figure 10: The main difference in growth between households' gross savings on a cash basis and a national accounts basis is the adjustment for the change in pension entitlements

Image .csv .xls8. Upcoming changes to this bulletin

Accounting for student loans in the accounts

The implementation date for including this change in the national accounts has yet to be decided and further methodological work is required to establish the exact size of the impact on the government and household accounts. However, when it is implemented we will observe a significant increase in the amount of capital transfers payable from central government to households and a reduction in the amount of interest receivable by central government from households.

There will also be a reduction in the stock of loan assets held by central government and an equivalent reduction in loan liabilities of households. For more information, see the announcement on: How we are improving the recording of student loans in government accounts.

If you have any suggestions, please contact us by email at sector.accounts@ons.gov.uk.

Gross value added (GVA) at factor cost

Withdrawal of series

Within the UK Economic Accounts (UKEA) we publish four series presenting GVA at factor cost (identifiers KGN7, KGN6, KGN5 and YBHH). In the March Quarterly National Accounts release we announced that we are considering withdrawing these series from publication. This is because GVA at factor cost is not recognised with the UN System of National Accounts 2008 (SNA08) framework, therefore we have concerns over the methodology used to calculate these estimates. We have received a small amount of user feedback and we welcome further user feedback around our proposal to remove these series from the UKEA publication from the September 2019.

Back to table of contents9. Upcoming articles

Each year we produce an annual update to the UK National Accounts in the Blue Book and Pink Book and the associated releases. As already announced, the Blue Book and Pink Book 2019 consistent datasets will be published on 30 September 2019. Details have already been provided on the scope in the article Latest developments and changes to be implemented in Blue Book and Pink Book 2019 and indicative impacts on headline gross domestic product (GDP) components for the years 1997 to 2016 were published on 27 June 2019 in the article National Accounts articles: Blue Book 2019 indicative impacts on GDP current price and chained volume measure estimates: 1997 to 2016.

This year, due to the very demanding set of changes being put through in the annual update, we are exceptionally not going to fully reconcile 2017 annual GDP data, instead producing an indicative balance to allow further time for final quality assurance of the data. As a consequence, the reference year and last base year for all chained volume measure series will remain as 2016. Further articles are planned ahead of the 30 September 2019 releases as detailed in Table 1.

| Content of article | Provisional date of publication |

|---|---|

| Impact of Blue Book 2019 changes on GDP current price and chained volume measure annual and quarterly estimates: 1997 to 2016 and associated methods articles | Aug-19 |

| Detailed assessment of changes to Sector and Financial Accounts, 1997 to 2016 | Aug-19 |

| Detailed assessment of changes to Balance of Payments annual estimates, 1997 to 2016 | Aug-19 |

| Publication of Blue Book and Pink Book 2019 consistent Quarterly National Accounts, Quarterly Sector Accounts and Balance of Payments | 30-Sep-19 |

| Alignment between public sector finances and national accounts article | Sep-19 |

| Publication of Blue Book 2019 and Pink Book 2019 | 31-Oct-19 |

Download this table Table 1: Provisional publication schedule for Blue Book and Pink Book 2019

.xls .csv10. Quality and methodology

National Statistics status

On 20 March 2018, the UK Statistics Authority published a letter confirming the designation of quarterly sector accounts statistics as National Statistics. National Statistics means that official statistics meet the highest standards of trustworthiness, quality and value. The letter praised the richer analysis on the households’ sector and the improvements in communicating technical concepts to a less technical audience.

We are keen to continue this type of analysis and we welcome feedback and suggestions for additional content for the bulletin or supplementary pieces.

Reliability

Estimates for the most recent quarters are provisional and are subject to revision in the light of updated source information. Our revisions to economic statistics page contains articles on revisions and revisions policies.

Revisions to data provide one indication of the reliability of main indicators. Revisions triangles were published for the households and non-profit institutions serving households’ saving ratio. However, following the separation of the households and non-profit institutions serving households (NPISH) sectors in September 2017, we have ceased production of the revision triangles for the households and NPISH saving ratio.

In due course, we will reintroduce the revision triangle for the households-only saving ratio as and when meaningful analysis on revisions can be done.

Comparability

Data in this bulletin are internationally comparable. The UK National Accounts are compiled in accordance with the European System of Accounts 2010: ESA 2010, under EU law and in common with all other members of the European Statistical System. ESA 2010 is itself consistent with the standards set out in the United Nations System of National Accounts 2008: SNA 2008.

An explanation of the sectors and transactions described in this bulletin can be found in Chapter 2 of the ESA 2010 manual.

Methodology

This section summarises the methodology behind some of our main economic indicators: real household disposable income, households’ saving ratio and net lending or borrowing positions.

Real household disposable income (RHDI) explained

Household income is measured in two ways: in current prices (also called nominal prices) and in real terms, where the effect of price inflation is removed.

Gross disposable household income (GDHI) is the estimate of the total amount of income that households have available to either spend, save or invest. It includes income received from wages (and the self-employed), social benefits, pensions and net property income (that is, earnings from interest on savings and dividends from shares) less taxes on income and wealth. These are all given in current prices.

Therefore, GDHI tells us how much income households had to spend, save or invest in the time period being measured once taxes on income and wealth had been paid.

Adjusting GDHI to remove the effects of inflation gives another measure of disposable income called real household disposable income (RHDI). This is a measure of the real purchasing power of households’ income, in terms of the physical quantity of goods and services they would be able to purchase if prices remained constant over time. Further information on this calculation can be found in our Quality and Methodology Information.

The households’ saving ratio explained

The saving ratio estimates the amount of money households have available to save (gross saving) as a percentage of their gross disposable income plus pension accumulations (total available resources).

Gross saving is the difference between households’ total available resources (that is, GDHI plus pension accumulations) and household expenditure on all goods and services for consumption.

The saving ratio can be volatile and is sensitive to even relatively small movements in its components, particularly on a quarterly basis. This is because gross saving is a relatively small difference between two large numbers. It is therefore often revised at successive publications when there are revisions to data.

The saving ratio may be considered an indicator of households’ economic confidence as well as an indicator of households’ financial conditions.

A higher saving ratio may be the result of an increase in income, a decrease in expenditure, or some combination of the two. A rise in the saving ratio may be an indication that households are acting more cautiously by spending less. Conversely, a fall in the saving ratio may be an indication that households are more confident and spending more. Other factors such as interest rates and inflation should also be considered when interpreting the households’ saving ratio.

Net lending (+) or borrowing (-) positions explained

The net lending or borrowing of a sector represents the net resources that the sector makes available to the rest of the economy. It does not necessarily refer to actual lending or borrowing in the normal sense, rather, it means that either a sector has money left over after its spending and investment in a given period (net lending), or it has spent and invested more than it received and has a need for financing (net borrowing), which may be covered by borrowing, issuing shares or bonds, or by drawing on reserves.

The net lending or borrowing position is determined by gross saving (that is, the balance between gross disposable income and final consumption expenditure) and is reduced or increased by the balance of capital transfers and the change in non-financial assets. This final position is called the net lending (if positive) or borrowing (if negative) position.

In summary, if actual investment is lower than the amount available for investment, the balance will be positive and represents net lending. Alternatively, if actual investment is higher than the amount available for investment, net borrowing is represented.

Note that, theoretically, the sum of net lending or borrowing positions of UK sectors must be offset by that of the rest of the world. However, this is only currently true up to 2016 data. From 2017 onwards, unbalanced supply use tables (SUT) in the compilation of gross domestic product (GDP) are unbalanced and it can take approximately 18 months after the end of the latest balanced year (currently 2016) for balanced SUTs to become available.

Quality and Methodology Information report

The Quarterly sector accounts Quality and Methodology Information report contains important information on:

the strengths and limitations of the data and how it compares with related data

uses and users of the data

how the output was created

the quality of the output including the accuracy of the data

The Quarterly sector accounts and the UK Economic Accounts are published at quarterly, pre-announced intervals alongside the Quarterly national accounts and Quarterly balance of payments statistical bulletins.

Back to table of contents11. Appendix A: key economic indicators

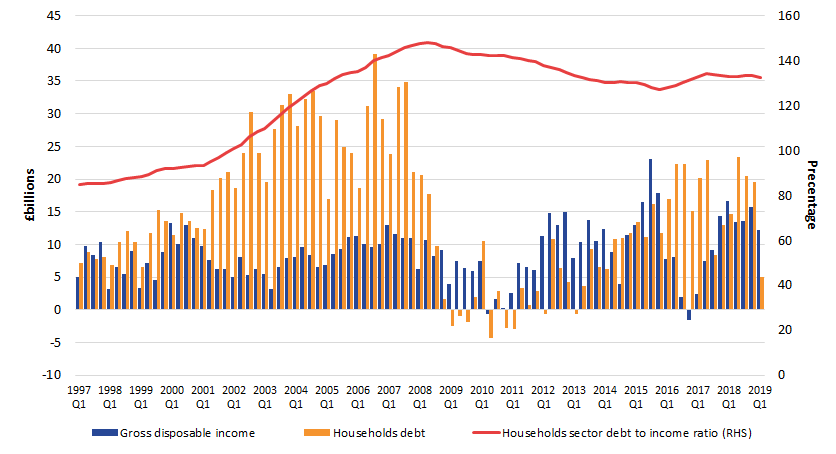

Households’ debt to income ratio

In both the Quarterly sector accounts, UK: July to September 2017 and Quarterly sector accounts, UK: April to June 2017 bulletins we introduced analysis on the households’ debt to income ratio and the type of household accumulated debt (that is, mortgages versus unsecured debt. The households’ debt to income ratio is now included as an appendix to this release.

The ratio increased in 2016 and 2017, although there was a slowdown in this growth in the latter half of 2017. The households' debt to income ratio has remained broadly flat at around 133% since the beginning of 2017. In Quarter 1 (Jan to Mar) 2019, it stands at 132.4, a decrease from 133.2 in Quarter 4 (Oct to Dec) 2018 (Figure 11), driven primarily by a slower rate of accumulated debt than recent income. This means that in the latest quarter, households have approximately £1.33 debt for every £1 of income they have earned over the past year.

Figure 11: Households' debt to income ratio remains broadly flat at around 133% since the beginning of 2017

Contributions to the change in households' debt to income ratio, percentage (right hand side), £ billions (left hand side), non-seasonally adjusted, UK, Quarter 1 (Jan to Mar) 1997 to Quarter 1 (Jan to Mar) 2019

Source: Office for National Statistics

Notes:

- Households debt to income ratio calculated as the four-quarter rolling sum of gross disposable income divided by quarterly household debt.

- Households debt calculated as total loans held by households.

- To show the contributions to the Households debt to income ratio, the four quarter growth (£ billion) in gross disposable income and the quarterly growth (£ billion) in total loans is used.

- If the four quarter growth (£ billion) in gross disposable income is greater than the quarterly growth (£ billion) in total loans, the Households debt to income ratio will increase.

- If the quarterly growth (£ billion) in total loans is greater than the four quarter growth (£ billion) in gross disposable income, the Households debt to income ratio will decrease.

Download this image Figure 11: Households' debt to income ratio remains broadly flat at around 133% since the beginning of 2017

.png (19.4 kB) .xls (56.3 kB){kind=link}

12. Appendix B: additional information on the alternative measures of households’ income and savings

| Transactions | CDID | Quarterly change, £ million |

|---|---|---|

| Transaction removed from the National Accounts measure of Gross disposable income | ||

| Gross operating surplus (B.2g) | CAEO | 216 |

| Employers' social contributions* (D.12r) | DTWP | 785 |

| Financial Intermediation Services Indirectly Measured (FISIM) (P.119r) | CRNC | -556 |

| Investment income payable on pension entitlements* (D.442r) | KZL5 | -894 |

| Retained earnings attributable to collective investment fund shareholders (D.4432r) | MN7M | 7 |

| Financial Intermediation Services Indirectly Measured (FISIM) (P.119u) | CRNB | 511 |

| Employers' imputed social contributions (D.612r) | L8RQ | 1 |

| Non-life insurance claims (D.72r) | RNLU | -307 |

| Employers' actual social contributions* (D.611u) | L8NM | 713 |

| Employers' imputed social contributions* (D.612u) | MA4B | 72 |

| Households' social contribution supplements* (D.614u) | L8QA | -894 |

| Further transaction removed from the National Accounts measure of Households saving ratio | ||

| Adjustment for the change in pension entitlements (D.8r) | RNMB | -1086 |

| Imputed rental for housing (removed from cash basis final consumption expenditure) | GBFJ | 404 |

| Financial Intermediation Services Indirectly Measured (FISIM) (removed from cash basis final consumption expenditure) | C68W | -507 |

Download this table Table 2: Change in the value of transactions removed from the national accounts methodology to calculate cash basis gross disposable household income and the saving ratio

.xls .csv13. Acknowledgements

The author, David Matthewson, would like to express his thanks to the Sector and Financial Accounts Team at the Office for National Statistics for their contributions to this work.

Back to table of contentsContact details for this Statistical bulletin

Related publications

- Balance of payments, UK: January to March 2019

- Business investment in the UK: January to March 2019 revised results

- GDP quarterly national accounts, UK: January to March 2019

- Quarterly economic commentary: January to March 2019

- Consumer trends, UK: January to March 2019

- Economic statistics sector classification – classification update and forward work plan: June 2019