Table of contents

- Main points

- Statistician’s comment

- Summary

- The UK economy grew by 0.4% in Quarter 4 2017, revised down from 0.5% in the preliminary estimate

- Production and services output expand in Quarter 4 2017, while construction falls for the third consecutive quarter

- Growth in household consumption and business investment slowed in Quarter 4 2017

- The evolution of real-time consensus forecasts

- Growth in CPIH remained at 2.7% in January 2018, growth in input and output PPI both fell to 4.7% and 2.8% respectively

- Unemployment and employment rose in the three months to December 2017

1. Main points

The second estimate of gross domestic product (GDP) shows that the UK economy grew by 0.4% in Quarter 4 (Oct to Dec) 2017, revised down from the preliminary estimate of 0.5%.

GDP is now estimated to have increased by 1.7% in 2017, following revisions to the quarterly path.

Production and services output expanded in Quarter 4 2017, while construction fell for the third consecutive quarter.

Growth in household consumption and business investment slowed in Quarter 4 2017.

Growth of Consumer Prices Index including owner occupiers’ housing costs (CPIH) remained at 2.7% in January 2018; growth of input and output Producer Price Indices (PPI) both fell, to 4.7% and 2.8% respectively.

Unemployment and employment rose in the three months to December 2017.

2. Statistician’s comment

Commenting on today’s GDP figures, Head of GDP Darren Morgan said:

“Services continued to drive growth at the end of 2017, but with a number of consumer-facing industries slowing, as price rises led to household budgets being squeezed.

“A number of very small revisions to mining, energy generation and services were enough to see a slight downward revision to quarterly growth overall, despite headline services output being unchanged."

Back to table of contents3. Summary

The UK economy grew by 0.4% in Quarter 4 (Oct to Dec) 2017, revised down from the preliminary estimate. Growth has been revised down to 0.2% in Quarter 1 (Jan to Mar), while it has been revised up to 0.5% in Quarter 3 (July to Sept). These changes have led to a downward revision to annual growth in 2017, from 1.8% to 1.7%, which is the slowest rate of annual growth since 2012.

Services and production increased in Quarter 4, while construction fell for the third consecutive quarter. Household consumption has been subdued through 2017. Growth has slowed further to 0.3% in Quarter 4 and is estimated to have increased by 1.8% in 2017, its joint weakest rate since 2012. The 12-month growth rate for the Consumer Prices Index including owner occupiers’ housing costs (CPIH) has remained, for the second month, at 2.7% in the 12 months to January 2018. Since the end of 2016, most of the increases in CPIH have been driven by the more import-intensive categories and energy. The price paths of the inputs used to produce commodity-based manufacturing products such as oil and metal goods continue to be associated with changes in the sterling exchange rate.

Over the course of 2017, house price growth has seen considerable regional variation.

In the three months to December 2017, unemployment and employment increased. Wage growth was sluggish despite recent unemployment, which is explained by higher wage growth rather than higher job creation amongst low median wage jobs. The rise in employment is driven by UK and EU nationals in 2017.

More detailed theme day economic commentary is available for:

Back to table of contents4. The UK economy grew by 0.4% in Quarter 4 2017, revised down from 0.5% in the preliminary estimate

Figure 1: Revisions to gross domestic product growth, quarter-on-quarter

UK, Quarter 1 (Jan to Mar) 2016 to Quarter 4 (Oct to Dec) 2017

Source: Office for National Statistics

Notes:

- Q1 refers to Quarter 1 (Jan to Mar), Q2 refers to Quarter 2 (April to June),Q3 refers to Quarter 3 (July to Sept), Q4 refers to Quarter 4 (Oct to Dec).

Download this chart Figure 1: Revisions to gross domestic product growth, quarter-on-quarter

Image .csv .xlsToday’s (22 February 2018) GDP release estimates that UK economic growth was 0.4% in Quarter 4 (Oct to Dec) 2017, revised down from the preliminary estimate of 0.5%. All of 2017 is open for revision in today’s estimates. Growth has been revised down to 0.2% in Quarter 1 (Jan to Mar), while it has been revised up to 0.5% in Quarter 3 (July to Sept) (Figure 1).

These changes to the quarterly path have led to a downward revision to annual growth in 2017, from 1.8% to 1.7%, which is the slowest rate of annual growth since 2012. Compared with the same quarter a year ago, gross domestic product (GDP) increased by 1.4% in Quarter 4 2017, which is the slowest rate since Quarter 2 (Apr to June) 2012 (Figure 2).

Figure 2: Gross domestic product growth, quarter-on-quarter and quarter on same quarter a year ago growth rate

UK, Quarter 1 (Jan to Mar) 2008 to Quarter 4 (Oct to Dec) 2017

Source: Office for National Statistics

Notes:

- Q1 refers to Quarter 1 (Jan to Mar), Q2 refers to Quarter 2 (April to June),Q3 refers to Quarter 3 (July to Sept), Q4 refers to Quarter 4 (Oct to Dec).

Download this chart Figure 2: Gross domestic product growth, quarter-on-quarter and quarter on same quarter a year ago growth rate

Image .csv .xls5. Production and services output expand in Quarter 4 2017, while construction falls for the third consecutive quarter

In addition to the second estimate of gross domestic product (GDP), new data on services output in December 2017 have been published today (22 February 2018). Services output is estimated to have increased by 0.6% in Quarter 4 (Oct to Dec) 2017, unrevised to one decimal place from the preliminary estimate. However, revisions to two decimal places were sufficient to lead to a downward revision to GDP in Quarter 4. Table 1 compares the new estimates of growth in services output with the preliminary estimates.

Table 1: Revisions to Index of Services in Quarter 4 2017

| % and percentage points | |||

| Preliminary estimate (%) | Second estimate (%) | Revision (percentage points) | |

|---|---|---|---|

| Distribution, hotels and restaurants | 0.1 | -0.2 | -0.3 |

| Transport, storage and communication | 0.8 | 1.1 | 0.3 |

| Business services and finance | 0.8 | 0.9 | 0.1 |

| Government and other services | 0.4 | 0.2 | -0.2 |

| Total services | 0.6 | 0.6 | 0.0 |

| Source: Office for National Statistics | |||

Download this table Table 1: Revisions to Index of Services in Quarter 4 2017

.xls (32.8 kB)Services output grew by an unrevised 1.6% in 2017 – the weakest annual growth since 2011. Business services and finance increased by 1.8%, in line with the preliminary estimate. Growth in transport, storage and communication has been revised up to 3.6%, while there were downward revisions to growth in distribution, hotels and restaurants (from 2.1% to 1.7%) and growth in government and other services (from 0.4% to 0.2%).

Previous analysis showed that the slowdown in services has been driven largely by consumer-focused industries, reflecting the squeeze on household real incomes over the last year. While total services output growth remained unchanged for the second estimate, Figure 3 shows a similar weak consumer-focused services path in 2017.

Figure 3: Growth rate of consumer-focused services output and total services output, quarter-on-quarter a year ago

UK, Quarter 1 (Jan to Mar) 2016 to Quarter 4 (Oct to Dec) 2017

Source: Office for National Statistics

Notes:

Q1 refers to Quarter 1 (Jan to Mar), Q2 refers to Quarter 2 (April to June),Q3 refers to Quarter 3 (July to Sept), Q4 refers to Quarter 4 (Oct to Dec).

"Consumer-focused" services defined here include retail trade (Standard Industrial Classification (SIC) 2007 codes 45 and 47), food and beverage (SIC code 56), publishing, audiovisual and broadcasting activities (SIC codes 58 to 60; including motion pictures), and arts, entertainment and recreation (SIC codes 90 to 93).

Download this chart Figure 3: Growth rate of consumer-focused services output and total services output, quarter-on-quarter a year ago

Image .csv .xlsFigure 4 shows the revisions to components of the output approach to GDP between the preliminary estimate of GDP and the second estimate published today. Output in the production sector increased by 0.5% in Quarter 4 2017, revised down by 0.1 percentage points. Production output eased in the quarter, reflecting the unexpected shutdown of the Forties Pipeline System (FPS) for several weeks during December. This led to a 4.7% fall in mining and quarrying output, its largest quarterly fall since Quarter 4 2016.

This was more than offset by continued strength in manufacturing, which grew by 1.3% in the quarter. Manufacturing output increased for the eighth consecutive month in December 2017, for the first time since January 1988, which was the main driver for production output increasing by 2.1% in 2017. This is the strongest annual growth rate since 2010.

In contrast, output in the construction sector declined by 0.7% in Quarter 4, which has been revised up by 0.3 percentage points since the preliminary estimate of GDP. The decline marks the third consecutive quarterly fall in construction output, which last occurred between Quarter 1 (Jan to Mar) 2012 and Quarter 3 (July to Sept) 2012. Despite these three consecutive quarterly falls, construction rose by 5.1% in 2017 due to a historically high level of output in Quarter 1 2017.

Figure 4: Revisions to gross domestic product, output measure

UK, Quarter 1 (Jan to Mar) 2017 to Quarter 4 (Oct to Dec) 2017

Source: Office for National Statistics

Notes:

- Q1 refers to Quarter 1 (Jan to Mar), Q2 refers to Quarter 2 (April to June),Q3 refers to Quarter 3 (July to Sept), Q4 refers to Quarter 4 (Oct to Dec).

Download this chart Figure 4: Revisions to gross domestic product, output measure

Image .csv .xls6. Growth in household consumption and business investment slowed in Quarter 4 2017

The second estimate of gross domestic product (GDP) includes the first detailed picture of expenditure in Quarter 4 (Oct to Dec) 2017. This shows that private consumption, government consumption and gross capital formation contributed positively to GDP growth in Quarter 4, while net trade subtracted from growth. On a calendar-year basis, all components made positive growth contributions, with private consumption and net trade being the largest contributors (1.1 and 0.4 percentage points respectively) (Figure 5).

Figure 5: Contributions to gross domestic product growth, expenditure component, quarter-on-quarter, chained volume measure

UK, Quarter 1 (Jan to Mar) 2016 to Quarter 4 (Oct to Dec) 2017

Source: Office for National Statistics

Notes:

Components may not sum to total gross domestic product due to rounding and loss of additivity in data prior to open period. The statistical discrepancy is also not displayed.

Q1 refers to Quarter 1 (Jan to Mar), Q2 refers to Quarter 2 (April to June),Q3 refers to Quarter 3 (July to Sept), Q4 refers to Quarter 4 (Oct to Dec).

Download this chart Figure 5: Contributions to gross domestic product growth, expenditure component, quarter-on-quarter, chained volume measure

Image .csv .xlsHousehold consumption has been subdued through 2017, with today’s (22 February 2018) revised figures showing that it has increased by 0.3% to 0.4% in each quarter. This is weaker than the recent underlying trend, where quarterly growth has been 0.8% on average in the previous two years. There have been upward revisions in the first half of 2017 but a downward revision to 0.4% in Quarter 3 (July to Sept), while growth has slowed further to 0.3% in Quarter 4. Household consumption is estimated to have increased by 1.8% in 2017, its joint weakest rate since 2012.

Gross fixed capital formation (GFCF) has been revised up in each of the first three quarters of 2017 and is estimated to have increased by 3.9% in 2017. GFCF increased by 1.1% in Quarter 4, driven by a 5.6% increase in government investment – in part driven by increased capital investment in health and education. In contrast, business investment was flat in Quarter 4, slowing from the revised 0.9% growth recorded in the previous quarter. There was a slowing in dwellings investment by the private sector, which increased by 1.4% in Quarter 4 – its slowest rate in 2017.

The total trade deficit widened from 1.4% of GDP in Quarter 3 to 2.1% in Quarter 4. This widening was driven primarily by an increase in the import of unspecified goods (mainly non-monetary gold) and fuels, which was accentuated by rising oil prices. In volume terms, exports fell by 0.2% in Quarter 4, while imports rose by 1.5%. The fall in exports was driven primarily by a 21.6% decline in fuel exports. This decline in fuel may reflect the sharp decline in domestic oil production in December 2017 due to the unexpected shutdown of the Forties Pipeline System for emergency repair. However, trade in fuels can be volatile and the monthly decline of 11.4% in December is not unusual.

Despite the quarterly fall in exports, the underlying picture for exports is still one of strength. Excluding oil and erratic commodities, the volume of goods exports increased by 1.1% in Quarter 4, marking the fifth consecutive quarterly rise. Exports of services also increased in Quarter 4 (0.4%).

Back to table of contents7. The evolution of real-time consensus forecasts

Figure 6 shows the consensus forecasts for gross domestic product (GDP) growth in 2017 and how they have evolved in response to the vote to leave the EU1. Before the referendum, the average independent forecast for annual GDP growth in 2017 was 2.1%, which would have been conditional on the UK voting to remain in the EU. The median forecast was revised down to 0.8% following the vote to leave the EU, reflecting the consensus views on the anticipated effects.

Over the last 18 months, these consensus forecasts have been gradually revised upwards, in part reflecting the stronger-than-expected outturns. GDP is now estimated to have increased by 1.7% in 2017, although this is lower than the pre-referendum consensus forecast of 2.1% and is the lowest annual GDP growth since 2012.

Figure 6: Real-time consensus forecasts of 2017 gross domestic product growth

UK, February 2016 to December 2017

Source: HM Treasury and Office for National Statistics calculations

Download this chart Figure 6: Real-time consensus forecasts of 2017 gross domestic product growth

Image .csv .xlsFigure 7 shows how the consensus 2017 forecasts of the expenditure components have evolved before and after the referendum, compared with the first 2017 expenditure estimates published today (22 February 2018). The consensus forecast for growth in private consumption in 2017 was 2.2% in April 2016. This was expected to slow to 1.3% based on the consensus forecasts in October 2016, driven by the effect of the fall in the exchange rate on real household income. The official estimates published today show that growth in private consumption slowed to 1.7% in 2017.

The median forecast for growth in fixed investment following the referendum was for it to fall by 1.9%, as heightened uncertainty was expected to weigh on capital expenditure. However, today’s estimates show that fixed investment increased by 3.9% in 2017, only marginally lower than the forecast published in April 2016.

Figure 7: Snapshots of gross domestic product, expenditure measure, consensus forecasts versus outturns

UK, annual 2017 growth

Source: HM Treasury and Office for National Statistics calculations

Download this chart Figure 7: Snapshots of gross domestic product, expenditure measure, consensus forecasts versus outturns

Image .csv .xlsNotes for: The evolution of real-time consensus forecasts

- The figures refer to forecasts that have been updated within the previous three months at each specific point in time.

8. Growth in CPIH remained at 2.7% in January 2018, growth in input and output PPI both fell to 4.7% and 2.8% respectively

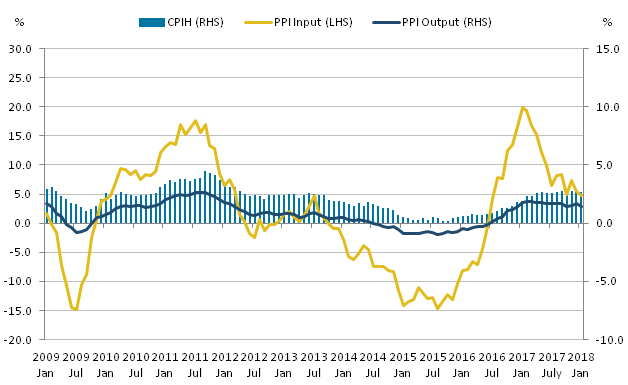

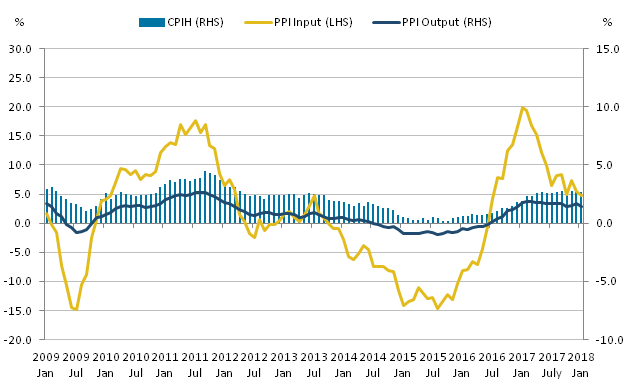

Figure 8 shows the 12-month growth in the Consumer Prices Index including owner occupiers’ housing costs (CPIH) remained at 2.7% in January 2018. The input Producer Prices Index (input PPI) grew by 4.7% in the 12 months to January 2018, down from growth of 5.4% in the 12 months to December 2017. The output Producer Prices Index (output PPI) grew by 2.8% in the 12 months to January 2018, down from growth of 3.3% in the 12 months to December 2017.

Figure 8: Annual growth rate for Producer Price Indices input (left hand side), PPI output and CPIH (right hand side)

UK, January 2009 to January 2018

Source: Office for National Statistics

Notes:

- These data are also available within the Dashboard: Understanding the UK economy.

Download this image Figure 8: Annual growth rate for Producer Price Indices input (left hand side), PPI output and CPIH (right hand side)

.png (19.6 kB) .xls (34.3 kB){kind=link}

In the January 2018 Economic Review, the methodology of calculating import intensity in CPIH was expanded from just direct import intensity to including both direct and indirect import intensity (that is, the imported content of goods and services that are produced in the UK for household consumption). For example, restaurants have 0% direct import intensity, but 15.1% indirect import intensity because of the imported content of the food and drink that they serve. The data sources were also reviewed and updated to include the most recent data. For more information around this methodology, including an overview of the caveats and assumptions you should be aware of before using these data, please see the full article in the Economic Review.

Figure 9: Growth in CPIH contributions by purchasers' price total import intensity groups and owner occupiers' housing costs (OOH) and energy

UK, January 2006 to January 2018

Source: Office for National Statistics

Notes:

- Contributions to CPIH may not sum due to rounding.

Download this chart Figure 9: Growth in CPIH contributions by purchasers' price total import intensity groups and owner occupiers' housing costs (OOH) and energy

Image .csv .xlsMost of the recent increases in the growth of CPIH since the end of 2016 have been driven by the more import-intensive categories and energy. For example, between August 2016 and January 2018, growth in CPIH increased from 1.0% to 2.7%, but 88.7% of that increase was driven by increases in the contributions of 25% to 40%, 40% and over, and energy import-intensity categories (Figure 9).

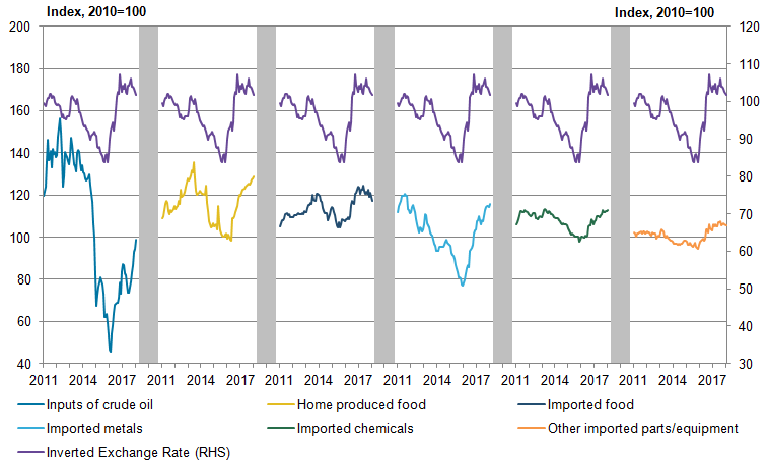

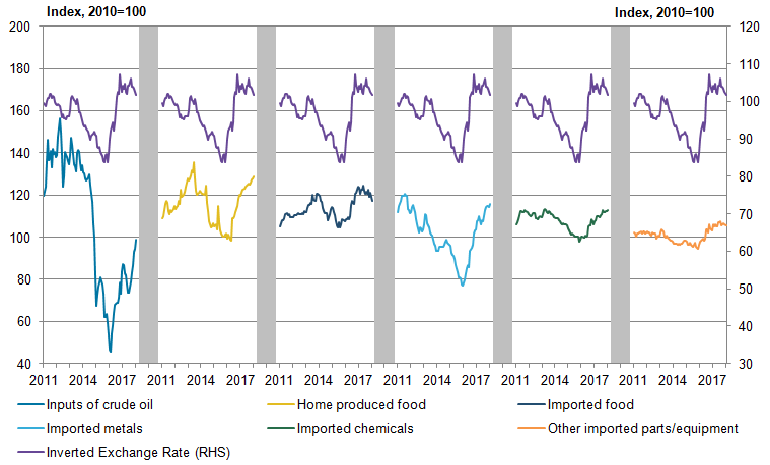

Figure 10 shows the inverted sterling effective exchange rate and six selected components of the input Producer Price Index, PPI. The price paths of the inputs, such as crude oil and metal goods, that are used to produce commodity-based manufacturing products have been trending more closely to changes in the exchange rate between January 2011 and January 2018 than prices faced by the producers of other parts and equipment. The UK input prices for these imported commodities reflect changes in both world prices and the exchange rate, as imported inputs make up around two-thirds of the aggregate input PPI series, the exchange rate has a relatively strong influence on overall input PPI.

Figure 10: Inverted sterling effective exchange rate and selected Input Producer Price Indices

UK, January 2011 to January 2018

Source: Office for National Statistics and Bank of England

Download this image Figure 10: Inverted sterling effective exchange rate and selected Input Producer Price Indices

.png (37.4 kB) .xls (27.1 kB){kind=link}

There was considerable variation in regional house price growth over the course of 2017. London has had one of the lowest growth rates, experiencing only 1.8% growth between January and December 2017. In contrast, the West Midlands and East Midlands have typically had amongst the highest growth rates; growing by 7.0% and 7.4% respectively over the course of the year (Figure 11).

Figure 11: The House Price Index for selected English regions

January 2017 to December 2017

Source: HM Land Registry, Office for National Statistics

Download this chart Figure 11: The House Price Index for selected English regions

Image .csv .xlsThe high growth rates of house prices seen in these regions between January and December 2017 can be partially attributed to the growth rates of house prices in specific local authorities. For example in the West Midlands, Sandwell and Coventry experienced average 12-month growth in house prices of 6.7% and 8.0% respectively, while in the East Midlands, Leicester and Corby saw average 12-month growth in house prices of 6.5% and 10.7% across the same period. Previous analysis has noted that the housing market in London has not recovered as well as the rest of the country following the Stamp Duty change in March 2016 and had lower house price growth than the rest of Great Britain throughout 2017.

Back to table of contents9. Unemployment and employment rose in the three months to December 2017

Latest estimates from the Labour Force Survey show that following a period of continuous decline, the number of unemployed people increased by 46,000 to 1.47 million in the three months to December 2017 when compared with July to September 2017 (Figure 12). As a result, the unemployment rate rose by 0.1 percentage points to 4.4% in the three months to December 2017, compared with the three months to September 2017.

Approximately two-thirds of the net increase in unemployment can be attributed to the people in the younger age groups, namely 16 to 17 and 18 to 24-year-olds. On the one hand, these age groups exhibit higher volatility. On the other, the direction of the change was consistent across all age groups, which raises a question of whether unemployment reached its minimum and will either grow or remain at a broadly stable level in 2018. It is worth remembering that the unemployment rate is still 0.4 percentage points lower than in the three months to December 2016.

Figure 12: Quarterly changes in unemployment, seasonally adjusted

UK, October to December 2006 to October to December 2017

Source: Office for National Statistics

Download this chart Figure 12: Quarterly changes in unemployment, seasonally adjusted

Image .csv .xlsEmployment

Despite the slight rise in unemployment, employment continued to grow. In the three months to December 2017, there were 32.15 million people in work, which was 321,000 more than for the same period a year earlier and 88,000 more than the previous quarter.

This increase was driven by full-time employees, whose number rose by 136,000 to 20.20 million in the three months to December 2017, when compared with the previous quarter. In contrast with the overall growth in employment, the number of employees working part-time fell by 51,000 during the same period. The decreasing part-time employment was concentrated in specific groups of occupations rather than felt by the entire labour market.

While employment increased, the total number of self-employed workers continued to fall. The net fall of 31,000 in the three months to December 2017 compared with the previous quarter includes a 41,000 decrease in the number of full-time self-employed and a positive change in part-time self-employment. In other words, the working patterns among the self-employed exhibit the opposite trend to that seen among the employees.

Overall, the number of people in self-employment was 18,000 lower in the three months to December 2017 compared with the same period a year earlier. It may be too early to speculate whether this indicates the end of a period of prolonged growth in self-employment, as it is not uncommon for self-employment to be lower in some quarters before continuing to grow.

Figure 13: Employment and unemployment rate

UK, seasonally adjusted, October to December 2001 to October to December 2017

Source: Office for National Statistics

Download this chart Figure 13: Employment and unemployment rate

Image .csv .xlsEmployment by nationality and country of birth

A rather expected development in the labour market over the course of 2017 was a slowdown in the growth of the number of EU workers. At this point it is worth stressing that these data do not show recent migration. Nor do they show new jobs. Rather, the figures show the net effect of people entering employment less the people leaving employment, in each of the categories by nationality. The number of people entering or leaving employment is much larger than the net changes.

Figure 14: Changes in employment by nationality, non-seasonally adjusted

UK, 2006 to 2017

Source: Office for National Statistics

Notes:

The total series includes people who do not state their country of birth or nationality.

EU14 Includes Austria, Belgium, Denmark, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, Netherlands, Portugal, Spain and Sweden.

EU8 includes Czech Republic, Estonia, Hungary, Latvia, Lithuania, Poland, Slovak Republic and Slovenia.

EU2 includes Romania and Bulgaria.

EU other consists of Cyprus, Croatia and Malta.

The estimates shown in this table relate to the number of people in employment and should not be used as a proxy for flows of foreign migrants into the UK.

Download this chart Figure 14: Changes in employment by nationality, non-seasonally adjusted

Image .csv .xlsIn the three months to December 2017, the number of workers in the EU8 countries by nationality fell slightly compared with the same three months in 2016, from 1,015,000 to 961,000 (1,033,000 to 995,000 respectively by country of birth). The number of workers in both the EU14 and EU2 continued increasing, albeit at a slower pace than before. Figure 14 shows the average annual change in the number of workers (quarterly estimates are subject to seasonality). The most interesting observation is that in 2017, just around a quarter of the net increase in employment came from the workers born in the EU. Just a year earlier, the share of EU-born workers exceeded 54%.

There tend to be wage differentials between domestic workers and the workers moving from other countries. It is often the case that workers from the countries with lower income levels could be willing to accept lower wages for the same skill content of a job than domestic workers. In that sense, the relatively higher net increase in the number of UK employees (by nationality and country of birth) accompanied by a slowdown in growth of the number of employees from the lower-income countries seen in the data might eventually push the median wage higher. Yet the real situation is significantly more complicated. Our earlier analysis showed that there exist significant differences between the skills, age profile, and occupations of UK and non-UK nationals in the workforce. In this context, it is also important to consider the wider characteristics of both the jobs being created, and the people occupying those positions – in other words, the composition effects.

Employment by occupation

The observed failure of the long period of low unemployment (despite the rise in October to December 2017, it remains very low) to be transmitted into higher wage growth raised the question about the possible role of the composition effects. The structure of the economy matters. When the growth in the number of jobs is concentrated in the industries that are generally associated with lower wages, one could expect the pressure on the average wage to be downward, despite fewer people looking for jobs. In the Labour Market Economic Commentary: November 2017, we explored the relationship between wages and employment across a number of industries. The analysis showed that between June 2016 and June 2017, most jobs have been created in the sectors with relatively weakly performing median wages.

Wages tend to respond to the situation in the wider labour market with a noticeable time lag. It is also important to understand that the structural changes themselves may be accumulating gradually and are unlikely to cause sudden shocks to headline statistics. For this reason, one needs to consider changes in the composition of the labour market at least several quarters before the period of interest.

This month’s commentary supplements the earlier industrial analysis by encompassing personal characteristics of those in employment as well as the type of job. Unlike the industrial classification, occupational classification accounts for skill level and skill content of the job, so that each major occupational group is associated with a certain general level of qualifications, training and experience. The advantage of using the occupational classification is that over time, technological changes may rebalance the composition of the labour force within a given industry. For instance, higher-skill level may be required to operate the new machinery or IT systems; or indeed, the opposite may also be true whereby automation could reduce the need for specialist skills.

Figure 15: Employees by occupation, non-seasonally adjusted

UK, January to March 2006 to October to December 2017

Source: Office for National Statistics

Download this chart Figure 15: Employees by occupation, non-seasonally adjusted

Image .csv .xlsFigure 15 shows the total number of employees in each major occupation group from January to March 2006. The number of employees associated with the lower-skill levels has not risen above the pre-downturn level, despite the overall growth in the number of employees. A similar observation can be made in the shorter-term, given that the more recent periods would be more informative in the context of wage growth. Still, the data corresponding to 2015, 2016 and 2017 do not support the hypothesis that the overall growth in the number of employees was dominated by lower-skill occupations. On the contrary, the growth in employment appears to have been more pronounced among associate professional and technical, professional, and managerial occupations, which exhibited overall growth of 6.62% across the three categories combined, between 2015 and the end of 2017. These occupations tend to be associated with higher wages but not necessarily higher growth in wages.

Figure 16: Average annual change in gross earnings of full-time employees per occupation

UK, 2015 to 2017

Source: Office for National Statistics, Monthly Wages and Salaries Survey

Download this chart Figure 16: Average annual change in gross earnings of full-time employees per occupation

Image .csv .xlsFigure 16 confirms that the average gross weekly earnings for skilled trades, associate professional and technical, and professional occupations over the three-year period grew at a slower pace than on average for all employees. On the other hand, those in elementary occupations; process, plant and machine operatives; sales and customer services, and caring, leisure and other services saw a proportionately higher average wage increase between January 2015 and December 2017. This can be explained partly by a larger proportion of people who benefitted from the rise of the National Minimum Wage and the introduction of the National Living Wage in these occupations.

So, rather than the growth in the number of jobs being skewed towards lower-skill occupations, the increase in gross wages was weaker among the faster-growing, higher-skilled occupational groups. This observation is consistent with the distributional analysis of the Annual Survey of Hours and Earnings (ASHE), which has been conducted on individual level data.

Back to table of contents