Table of contents

- Main points

- Statistician’s comment

- Summary

- The preliminary estimate of GDP shows that the UK economy grew by 0.5% in Quarter 4 2017

- Services output grew by 0.6% in Quarter 4 2017

- Production output increased by 0.6% in Quarter 4 2017, buoyed by continued strength in manufacturing

- Construction continued to weigh on growth in Quarter 4 2017 with a third consecutive quarterly decline

- Growth in CPIH fell to 2.7% in December 2017

- Full-time workers are driving the increase in employment

1. Main points

The preliminary estimate of gross domestic product (GDP) shows that the UK economy grew by 0.5% in Quarter 4 (Oct to Dec) 2017, following growth of 0.4% in the previous quarter.

Quarter 4 2017 growth was driven by an expansion in production and services output, while construction output fell for the third consecutive quarter.

Growth in the Consumer Prices Index including owner occupiers’ housing costs (CPIH) fell to 2.7% in December 2017 having been 2.8% for the preceding three months; growth in input Producer Price Indices (PPI) also fell in December 2017 while that of output PPI grew slightly.

The UK unemployment rate remained at 4.3% in the three months to November 2017, which represents the joint lowest unemployment rate since 1975.

At 810,000, the number of vacancies in October to December 2017 was the highest since comparable records began in 2001.

2. Statistician’s comment

Commenting on today’s GDP figures, Head of GDP Darren Morgan said:

“Despite a slight uptick in the latest quarter, the underlying picture is of slower and uneven growth across the economy.

“The boost to the economy at the end of the year came from a range of services including recruitment agencies, letting agents and office management. Other services – notably consumer-facing sectors – showed much slower growth. Manufacturing also grew strongly but construction again fell.”

Back to table of contents3. Summary

The UK economy grew by 0.5% in Quarter 4 (Oct to Dec) 2017, marking the strongest quarterly growth in 2017. Following a slow start to the year, the economy strengthened through the year to record annual growth of 1.8% in 2017 – marginally below the 1.9% growth seen in 2016. However, the underlying picture is of slower and uneven economic growth. Growth in the latest quarter was driven by strength in services and production output – particularly manufacturing – while construction fell for the third consecutive quarter.

The Consumer Prices Index including owner occupiers’ housing costs (CPIH) 12-month growth rate fell to 2.7% in December 2017 having been 2.8% for each of the preceding three months. Over the course of the year, one of the biggest drivers of CPIH was transport, which made the highest contribution to the change in the 12-month growth rate for 10 months of 2017.

In the three months to November 2017, the UK unemployment rate remained at 4.3%, which is the joint lowest rate since 1975. The number of people in work reached an all-time high, driven mainly by an increase in full-time employees. At 810,000, the number of vacancies in October to December 2017 was also at its highest since comparable records began in 2001.

More detailed theme day economic commentary is available for:

Back to table of contents4. The preliminary estimate of GDP shows that the UK economy grew by 0.5% in Quarter 4 2017

Today’s gross domestic product (GDP) release contains new information regarding UK economic growth in Quarter 4 (Oct to Dec) 2017. Within this release is an early indication of output growth in production, construction and services in December 2017. In addition, data on services output in November 2017 have been published.

The preliminary estimate of GDP shows that the UK economy grew by 0.5% in Quarter 4 2017, the strongest quarterly growth rate in 2017 (Figure 1). This was driven by solid expansions in both production and services output (both up by 0.6%), while the construction industry continued its decline with a third consecutive quarterly fall in output (down by 1.0%).

Figure 1: Gross domestic product growth, quarter-on-quarter and quarter on same quarter a year ago growth rate

UK, Quarter 1 (Jan to Mar) 2008 to Quarter 4 (Oct to Dec) 2017

Source: Office for National Statistics

Notes:

- Q1 refers to Quarter 1 (Jan to Mar), Q2 refers to Quarter 2 (Apr to June), Q3 refers to Quarter 3 (July to Sept), and Q4 refers to Quarter 4 (Oct to Dec).

Download this chart Figure 1: Gross domestic product growth, quarter-on-quarter and quarter on same quarter a year ago growth rate

Image .csv .xlsOn a calendar-year basis, the economy grew by 1.8% in 2017 – slightly below the 1.9% seen in 2016. This is well above growth expectations in the immediate aftermath of the EU referendum vote in June 2016. In 2016, the average independent forecast and the Bank of England (BoE) predicted calendar year growth of 0.8% in 2017, while the Office for Budget Responsibility (OBR) forecast predicted 1.4%1.

Despite surpassing these expectations, 2017 growth in the UK economy was still below its five-year average annual growth rate, primarily reflecting a slowdown in services growth, which has gradually declined since 2014. The annual growth contribution of the services industry has fallen from 2.7 percentage points in 2014 to 1.3 percentage points in 2017 (Figure 2), with the industry growing by only 1.6% in 2017 – its weakest annual rate since 2011.

Figure 2: Contribution to annual growth in output gross value added by sector

UK, 2007 to 2017

Source: Office for National Statistics

Notes:

- Components may not sum due to rounding.

Download this chart Figure 2: Contribution to annual growth in output gross value added by sector

Image .csv .xlsNotes for: The preliminary estimate of GDP shows that the UK economy grew by 0.5% in Quarter 4 2017

- These forecasts refer to the first published figure following the EU referendum vote – July 2016 for independent forecasts, August 2016 for the Bank of England and November 2016 for the Office for Budget Responsibility.

5. Services output grew by 0.6% in Quarter 4 2017

Despite a relatively weak rate of annual growth, services output grew by a solid 0.6% in Quarter 4 (Oct to Dec) 2017, following growth of 0.4% in Quarter 3 (July to Sept) 2017. Quarter 4 marked the strongest quarterly growth for services in 2017, with the industry contributing 0.4 percentage points to quarterly gross domestic product (GDP) growth.

Services growth in Quarter 4 2017 was broad-based across the industry, with output in all four main components increasing in the quarter. The largest contributor was the business services and finance sector, which contributed 0.3 percentage points towards total services growth and was the strongest contributor for the second consecutive quarter. This is in line with the Bank of England’s Agents’ summary of business conditions for Quarter 4 2017, which noted that professional services firms across law, accountancy and consultancy were experiencing robust demand for advice related to the acquisition of UK assets, and from EU clients on the establishment of UK operations to retain market access.

In other sectors, transport, storage and communication, and government and other services each contributed 0.1 percentage points to total services growth in Quarter 4 2017, while distribution, hotels and restaurants made zero contribution (to one decimal place). Quarter-on-year growth in distribution, hotels and restaurants fell to 0.5% in Quarter 4 2017 – the equal lowest rate since Quarter 4 2010.

Together with transport, storage and communication, the distribution, hotels and restaurants sector has been one of the main drivers of the slowdown in the growth of total services output since late 2016. Several industries within these two sectors, such as retail trade, are “consumer-focused” industries, which have seen a notable slowdown over the past year (Figure 3). Output in consumer-focused service industries has fallen from a quarter-on-year growth rate of 6.6% in Quarter 3 2016 to negative 0.2% in Quarter 4 2017.

Figure 3: Growth rate of consumer-focused services output and total services output, quarter-on-quarter a year ago

UK, Quarter 1 (Jan to Mar) 2015 to Quarter 4 (Oct to Dec) 2017

Source: Office for National Statistics

Notes:

"Consumer-focused" services defined here include retail trade (Standard Industrial Classification (SIC) 2007 codes 45 and 47), food and beverage (SIC code 56), publishing, audiovisual and broadcasting activities (SIC codes 58 to 60; including motion pictures), and arts, entertainment and recreation (SIC codes 90 to 93).

Q1 refers to Quarter 1 (Jan to Mar), Q2 refers to Quarter 2 (Apr to June), Q3 refers to Quarter 3 (July to Sept), and Q4 refers to Quarter 4 (Oct to Dec).

Download this chart Figure 3: Growth rate of consumer-focused services output and total services output, quarter-on-quarter a year ago

Image .csv .xlsNew data on services output in November 2017 have also been published today (26 January 2018). The latest figures show that services output rose by 0.4% in the three months to November 2017. Services also rose by 0.4% on a monthly basis in November 2017, which was the strongest monthly growth rate since August 2016 and above market expectations of 0.2% monthly growth. While the business services and finance sector was again the main driver of growth, growth was widespread across the services industries in November 2017, with 26 industries contributing positively to growth in the month.

Back to table of contents6. Production output increased by 0.6% in Quarter 4 2017, buoyed by continued strength in manufacturing

Output in the production sector rose by a solid 0.6% in Quarter 4 (Oct to Dec) 2017 to record an annual growth rate of 2.0% – its strongest annual growth since 2010. The quarterly growth primarily reflected a 1.3% rise in manufacturing, partly offset by a 3.9% fall in mining and quarrying. The energy supply and waste management industries both recorded modest growth in the quarter (0.4% and 0.3% respectively).

The fall in mining and quarrying in Quarter 4 2017 reflected the unexpected shutdown of the Forties pipeline system (FPS) due to emergency repair. The FPS, which carries oil from the North Sea oil rigs to the British mainland for processing, was shut for several weeks during the month of December 2017. With the FPS responsible for transporting around 40% of the UK’s total oil production, the resultant fall in mining and quarrying output in Quarter 4 2017 was the largest quarterly fall seen since Quarter 4 2016.

Even with the unexpected fall in mining, overall production increased by 0.6% in the quarter due to another strong performance in manufacturing. Following a weak start to 2017, manufacturing output has steadily recovered over the year and grew by 1.3% in Quarter 4 2017 – matching its performance in Quarter 3 2017. Index of Production figures released earlier this month showed that manufacturing output rose for the seventh consecutive month in November 2017, marking the longest run of expansion in two decades. The December 2017 forecast continues this run, marking the eighth consecutive month of positive growth in manufacturing. This consistent strength over the past two quarters saw manufacturing output rise by 2.7% in 2017 – stronger than annual growth in the overall UK economy.

On a sub-sector level, the production of metal products and pharmaceuticals accounted for over half of total manufacturing growth in Quarter 4 2017, contributing 0.5 and 0.3 percentage points respectively (Figure 4). Quarter 4 2017 growth in metal products (4.6%) was the strongest quarterly growth rate since Quarter 1 (Jan to Mar) 1998 and reflected increases in all components within metal products.

Meanwhile, production of motor vehicles fell by 1.6% in Quarter 4 2017 and has been relatively volatile on a quarter-on-quarter basis in 2017 – largely reflecting changes to the Vehicle Excise Duty (VED) in April 2017 and the rollout of new models by UK manufacturers in July 2017.

Figure 4: Contributions to quarter-on-quarter manufacturing growth

UK, Quarter 1 (Jan to Mar) 2016 to Quarter 4 (Oct to Dec) 2017

Source: Office for National Statistics

Notes:

Components may not sum to total manufacturing output due to rounding.

Q1 refers to Quarter 1 (Jan to Mar), Q2 refers to Quarter 2 (Apr to June), Q3 refers to Quarter 3 (July to Sept), and Q4 refers to Quarter 4 (Oct to Dec).

Download this chart Figure 4: Contributions to quarter-on-quarter manufacturing growth

Image .csv .xls7. Construction continued to weigh on growth in Quarter 4 2017 with a third consecutive quarterly decline

In contrast with the expansion in services and production, the preliminary estimate of construction shows that total output volumes fell by 1.0% in Quarter 4 (Oct to Dec) 2017. This marked the third consecutive quarterly decline in construction output, which has not been seen since Quarter 3 (July to Sept) 2012.

Despite three quarters of decline, construction output rose by 5.1% on an annual basis in 2017. This is due to a record-high level of construction output in Quarter 1 (Jan to Mar) 2017, with subsequent quarterly falls coming off this very high base (Figure 5). Levels of construction output remain elevated and well-above their pre-downturn peak in Quarter 1 2008, despite the recent falls.

Figure 5: Total construction output, chained volume measure, seasonally adjusted

UK, Quarter 1 (Jan to Mar) 2008 to Quarter 4 (Oct to Dec) 2017

Source: Office for National Statistics

Notes:

- Q1 refers to Quarter 1 (Jan to Mar), Q2 refers to Quarter 2 (Apr to June), Q3 refers to Quarter 3 (July to Sept), and Q4 refers to Quarter 4 (Oct to Dec).

Download this chart Figure 5: Total construction output, chained volume measure, seasonally adjusted

Image .csv .xlsThe preliminary estimate released today is based on forecasts and early responses to the December 2017 Monthly Business Survey and a breakdown of the components of construction is not available until 9 February 2018. The latest published monthly path for construction output shows a decline of 1.1% in October 2017 and a rise of 0.4% in November 2017.

In the three months to November 2017, construction output fell by 2.0%, marking the sixth consecutive three-monthly fall. This was driven by falls in private commercial new work, total housing repair and maintenance and infrastructure – partly offset by a 1.2% rise in private new housing. This is consistent with recent external surveys, which have highlighted the relative strength in private house building compared with weakness in commercial work and civil engineering projects.

Back to table of contents8. Growth in CPIH fell to 2.7% in December 2017

The 12-month growth in the Consumer Prices Index including owner occupiers’ housing costs (CPIH) fell to 2.7% in December 2017 from 2.8% in November 2017. The input Producer Price Index (input PPI) grew by 4.9% in the 12 months to December 2017, down from 7.3% in the 12 months to November 2017. The output Producer Price Index (output PPI) grew by 3.3% in the 12 months to December 2017, up from 3.1% in the 12 months to November 2017.

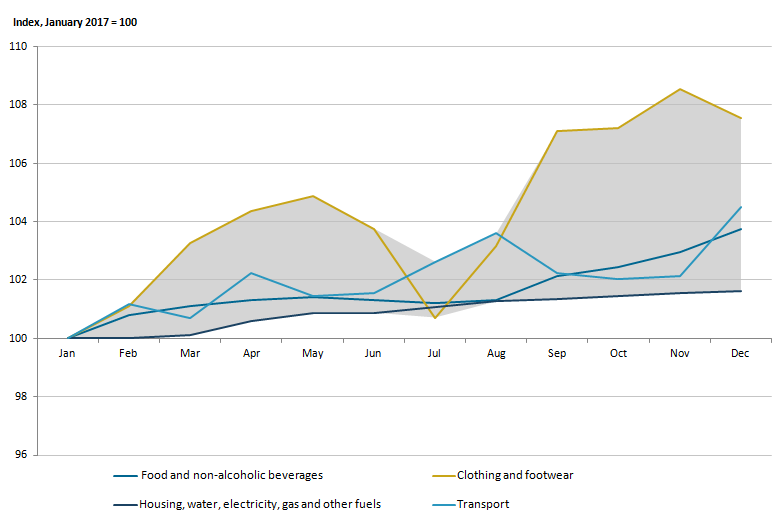

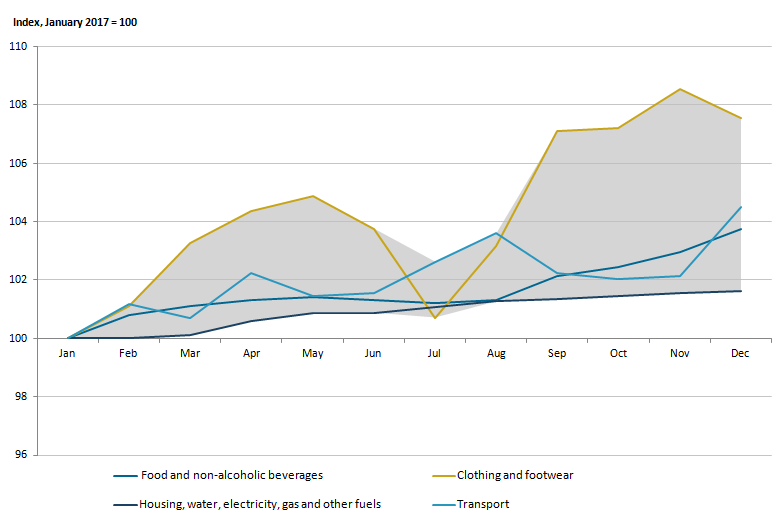

Figure 6 shows selected components of CPIH indexed to January 2017 equals 100 with the shaded area representing the difference between the highest and lowest component index for each month. All components have been trending upwards relative to January 2017 with some seasonal variation seen in transport, and clothing and footwear.

Figure 6: Headline Consumer Prices Index including owner occupiers' housing costs for selected components

UK, January 2017 to December 2017

Source: Office for National Statistics

Download this image Figure 6: Headline Consumer Prices Index including owner occupiers' housing costs for selected components

.png (24.0 kB){kind=link}

One of the biggest drivers of CPIH in the UK over the course of 2017 has been transport, which made the highest contribution to the change in the 12-month growth rate for 10 months of 2017. The price changes for transport seen over 2017 are largely driven by seasonal variation in air fares, with prices for most other components of transport remaining fairly flat over the period. Although air fares have risen over the course of 2017 – in keeping with seasonal trends – they have recently been contributing negatively to the 12-month growth rate in both transport and overall CPIH due to a change in the CPIH weights, which has been explored more in this month’s Prices economic commentary.

The housing, water, electricity, gas and other fuels component has seen the lowest overall growth in prices in 2017. This is due to price changes in owner occupier’s housing costs (OOH) moving in the opposite direction to price changes for electricity, gas and other fuels. OOH has seen a gradual decline throughout 2017, whilst both gas and electricity have seen price increases, with electricity prices increasing more sharply, especially towards the end of 2017. These offsetting effects have resulted in a relatively flat index for housing, water, electricity, gas and other fuels over 2017.

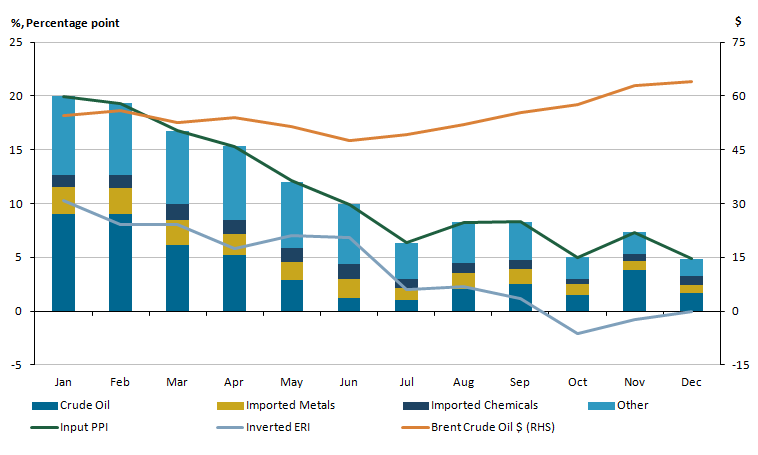

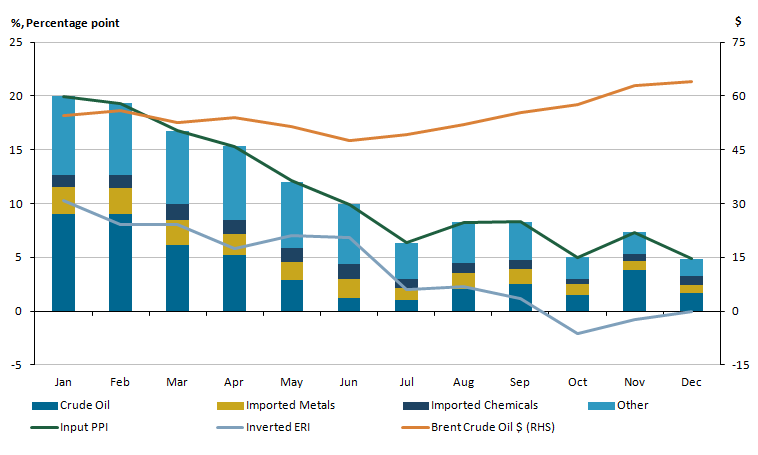

Figure 7 shows the contribution that components of the input PPI have made to the headline 12-month growth rate for each month in 2017. The figure also shows 12-month growth rates in the inverted sterling effective exchange rate (ERI) and the US dollar price of Brent crude oil over the same period.

Figure 7: Contributions to input Producer Price Index (PPI) and the 12-month growth rate of sterling effective exchange rate (ERI) (left-hand side) and Brent crude oil (US dollars) (right-hand side)

UK, January 2017 to December 2017

Source: Office for National Statistics

Notes:

- Contributions may not sum exactly due to rounding.

Download this image Figure 7: Contributions to input Producer Price Index (PPI) and the 12-month growth rate of sterling effective exchange rate (ERI) (left-hand side) and Brent crude oil (US dollars) (right-hand side)

.png (26.1 kB) .xls (28.7 kB){kind=link}

Since its 2017 peak of 19.9% in January, the 12-month growth rate of input PPI has generally been weakening, to a low of 4.9% in December 2017. These recent changes are driven mainly by the contributions of crude oil, which fell over much of the first half of 2017 – reflecting a gradual strengthening of sterling and gradually falling world prices for Brent crude oil – but started to increase again in the second half of 2017. Much of the change seen in both headline input PPI and the specific crude oil component over the course of 2017 is attributable to base effects.

Back to table of contents9. Full-time workers are driving the increase in employment

Latest estimates from the Labour Force Survey show that there were 32.21 million people in work in the three months to November 2017, which is 415,000 more than the same time a year earlier and 102,000 more than the previous quarter. The UK unemployment rate was 4.3% in the three months to November 2017, the joint lowest unemployment rate since 1975.

The increase in the number of people in work was driven by a rise in full-time employees, whose number increased by 173,000 in the three months to November 2017 when compared with the previous quarter, to a record high of 20.25 million people. In contrast with the overall growth, the number of employees working part time fell by 7,000 during the same period.

Figure 8: Percentage contribution change in employment level by working pattern

UK, seasonally adjusted, September to November 2001 to September to November 2017

Source: Office for National Statistics

Notes:

- Full time defined as employees working more than 30 paid hours per week.

Download this chart Figure 8: Percentage contribution change in employment level by working pattern

Image .csv .xlsWhile employment is at a record-high level, the total number of self-employed workers decreased by 82,000 in the three months to November 2017. As a result, the number of people in self-employment is 4,000 lower compared with the same time a year earlier. Overall, 2017 has seen a change in the longer-term trend of increasing self-employment.

Figure 9: Quarterly percentage change in employment rate and self-employment level

UK, seasonally adjusted, September to November 2001 to September to November 2017

Source: Office for National Statistics

Download this chart Figure 9: Quarterly percentage change in employment rate and self-employment level

Image .csv .xlsIn the October to December 2017 period, the number of vacancies reached 810,000, an all-time high since comparable records began in 2001. Vacancies are the positions for which employers are actively seeking to recruit outside their business or organisation. This commentary looks at the vacancy data in some detail and explains some of the basic facts that these data can tell about the UK labour market.

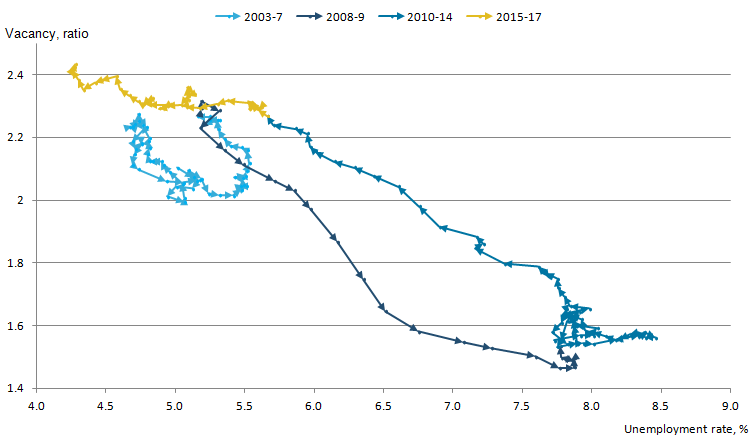

The vacancy rate is often considered in conjunction with the rate of unemployment. The negative relationship between the two is shown in Figure 10. This graph, known as the Beveridge curve, shows that when demand for goods and services, and subsequently labour falls, as was the case in 2008 to 2009, the vacancy rate decreases and the unemployment rate increases.

Figure 10: Beveridge curve: vacancy and unemployment rate

UK, seasonally adjusted, April to June 2001 to September to November 2017

Source: Office for National Statistics

Download this image Figure 10: Beveridge curve: vacancy and unemployment rate

.png (36.7 kB) .xls (45.6 kB){kind=link}

In addition to the cyclical movement along the curve during the recession and a move in the opposite direction thereafter, there is another important observation to be made here. The post-economic downturn years have been associated with an outward shift of the Beveridge curve, in other words, a shift towards a higher vacancy rate for a given unemployment rate. Among the possible reasons, the skills mismatch is often considered an important factor1. This shift appears to have been reversed in recent years, as can be seen from the 2015 to 2017 segment of the curve.

Furthermore, the latest position on the graph is unprecedented even for the pre-downturn period. It is hard to measure skill mismatch and the precise impact it has on the Beveridge curve shifts. Compared with the years immediately after the downturn, the observable data, such as the educational attainment, may suggest an improved but nonetheless persistently high mismatch level2.

Figure 11 shows vacancy levels in a selection of industries associated with a variety of skill levels. The graph demonstrates that the longer-term trends have been varied. In most private sector industries, an initial steep fall in vacancies in 2008 to 2009 was followed by a broadly upward move but with considerably varying trajectories, with the vacancy levels in some industries remaining consistently below or close to the pre-downturn levels. However, as we turn to the recent periods, the upward trend becomes a common feature for the vast majority of industries.

Figure 11: Vacancy level by industry

UK, seasonally adjusted, September to November 2002 to October to December 2017

Source: Office for National Statistics

Download this chart Figure 11: Vacancy level by industry

Image .csv .xlsHealth and social work sector exhibited the most profound growth in vacancy levels, even though public sector policies softened the initial decline in vacancies during the crisis. Here, the growth in vacancies outpaced the increase in the number of jobs. From the previous peak rate of 2.1 in 2008, the vacancy rate rose to 3.2 in October to December 2017, which represents an all-time high since comparable records began in 2011. By way of context, the health and social work sector has a high concentration of high-skill workforce and the jobs in this sector are more likely to be occupied by women. The growing rate may reflect the constraints faced by the employers in meeting the demand for labour.

To take an opposite example, the number of vacancies in professional, scientific and technical services has also exhibited strong growth, with a rise in the vacancy level of 13.9% on the year in the October to December 2017 period. Since the end of 2014, the average quarterly number of vacancies in these industries has consistently exceeded that before the downturn. However, as evidenced by Figure 12, this increase was closely matched by the overall growth in the number of jobs in the sector. The vacancy rate, on the other hand, has not yet exceeded its 2008 value.

Various industries have persistently different average vacancy rates, making their direct comparison inappropriate. Rather than plotting the actual rates per industry, Figure 12 takes the pre-downturn rate in each selected industry as 100%.

Figure 12: Vacancy rate by industry

UK, seasonally adjusted, January to March 2008 to October to December 2017

Source: Office for National Statistics

Download this chart Figure 12: Vacancy rate by industry

Image .csv .xlsAlthough the lower unemployment means that there are fewer people looking for jobs in the economy, the tightening in the labour market is not felt in the same way across the entire economy. Rather, employers are finding it more difficult to fill specific, niche vacancies.

It should be remembered that the data on vacancies provide only some of the number of indicators of the labour market tightness, or indeed skill mismatches. In the December 2017 Labour market economic commentary, we published a brief overview of job-to-job moves and separations, which are equally useful in assessing the health of the labour market.

Notes for: Full-time workers are driving the increase in employment

A general discussion of the post-downturn situation in Europe (PDF, 793.1KB) is available.

For more information on certain dimensions of the skill mismatch in the UK, see Analysis of the UK labour market – estimates of skills mismatch using measures of over and under education: 2015.