1. Main points

We provide new detailed experimental statistics on firm-level productivity of the non-financial business economy, expanding the coverage to 1998 to 2018 and increasing the level of detail published on the distribution of firm-level productivity for different groups of industry aggregation and size band.

Dispersion in productivity has widened over the period 1998 to 2018, driving growth; while median productivity of the non-financial business economy grew by 4% in real terms between 1998 and 2018, the 90th percentile grew by 18% over the same period.

Services, but not manufacturing, has increased in dispersion of productivity; the manufacturing sector has shrunk, falling by 32% in terms of workforce between 1998 and 2018, but manufacturing productivity was higher in 2018 across the productivity distribution.

On average, foreign-owned firms were more productive than equivalent, domestically owned businesses between 1998 and 2018; EU-owned and non-EU-owned firms were more productive than domestically owned firms by 14% and 19%, respectively.

2. Introduction

Weak productivity growth has been one of the defining characteristics of the UK's economic performance over the last decade. Average annual labour productivity growth between 2009 and 2019 was 0.3%, which compares with around 2% over the decade prior to 20081.

As productivity growth is the main source of improving living standards in the long-term, understanding the UK's ongoing poor productivity performance is important for policymakers and researchers. This article uses data from the Annual Business Survey (ABS) to explore productivity trends and distributions for British businesses.

This article is part of a series published by the Office for National Statistics (ONS) providing Experimental Statistics on firm-level productivity2. We extend previously published time series beginning in 2006 back to 1998 and add the latest survey data for 2018. We also provide new detailed statistics at different levels of industry aggregation and firm size-band.

This article covers the parts of the economy surveyed in the Annual Business Survey - the business sector excluding finance and agriculture, comprising approximately two-thirds of the UK economy.

Consistent with our previous analyses3 and the wider literature, our analysis shows that levels of productivity vary widely across businesses. Roughly 4.5% of the workforce included are in businesses that recorded negative gross value added (GVA) per worker in 2018. The most productive 10% of workers recorded GVA per worker of more than £100,000 per worker per year. Median gross value added per worker per year was around £28,600 in 2018, which is close to median earnings.

Conditional analysis of business-level labour productivity confirms many of our earlier findings: firms that are larger - in terms of employment - are more productive. This effect is clearer once controls are added for the industry of a business. We find that older businesses also have higher levels of productivity, but the largest productivity gains occur in the early years of a business' life.

We have expanded our analysis of foreign ownership to isolate the differential effect of being owned by a parent company based in the EU (EU-ownership) as opposed to being owned by a parent company from outside the EU. In 2018, EU owned businesses were almost 70% more productive than domestically owned firms on average, while non-EU-owned firms were more than twice as productive. These premiums fall to 12% and 18% for EU and non-EU-owned firms respectively in our conditional analysis, suggesting that ownership was highly correlated with other factors that drive positive productivity effects.

The Office for National Statistics (ONS) publishes various productivity measures such as macro-economic labour productivity, multi-factor productivity (MFP), public sector and so forth. They differentiate from each other for two reasons: its purpose and the availability of data4. The firm-level labour productivity measure in this release may be compared with multi-factor productivity (MFP) because of its similar coverage of the economy.

Along with this article, we have also published a dataset of the productivity distribution at the two-digit Standard Industrial Classification (SIC) level and size-band.

Notes for: Introduction

Labour productivity refers to output per worker and the periods covered are Quarter 1 (Jan to Mar) 1998 to Quarter 1 2008 and Quarter 3 (Oct to Dec) 2009 to Quarter 3 2019: Labour productivity, UK: October to December 2019

Office for National Statistics (2019), 'Firm-level labour productivity measures from the Annual Business Survey, Great Britain: 2017'

Office for National Statistics (2017), 'Labour productivity measures from the Annual Business Survey: 2006 to 2015'

The ABS excludes self-employed. Macro-economic labour productivity figures are based on GDP, which includes self-employed and the public sector. MFP covers only the UK market sector - excluding public sector and non-profit institutions.

3. Data source and quality

The Annual Business Survey (ABS, called the Annual Business Inquiry before 2008) is the main structural business survey of the Office for National Statistics (ONS). We present consistent Experimental Statistics for 1998 to 2018, the latest available data.

The ABS covers the non-financial business economy of Great Britain, which is approximately two-thirds of the UK economy. The survey comprises approximately 46,000 representative sample observations per year.

Firm-level approximate gross value added (aGVA) is calculated from the data collected on ABS survey forms, and employment is as recorded on the Inter-Departmental Business Register at the time of survey selection. Labour productivity is derived as the firm's aGVA divided by employment.

The full set of experimental firm-level productivity statistics is available in the accompanying dataset. Building on data given in previous publications we have extended the back-series to 1998. We have increased the level of detail significantly in many places, now including increased breakdowns of firm-level productivity by foreign ownership, firm size-band, two-digit industry and also many three-digit industry groups. The information on the distribution of productivity over different groups of firms is also expanded, with percentiles given at more levels of details, and full kernel and cumulative densities of productivity for breakdowns of industry section and firm size-band. A selection of these new Experimental Statistics is excerpted in this article.

The statistics presented in this article are in constant prices, deflated using deflators at the industry level.

Finally, in this article we use survey design and employment weights to give statistics that are representative of the whole workforce: the median worker works in a firm where labour productivity is £28,600 in aGVA per worker per year1.

Notes for: Data source and quality

- The median firm labour productivity is £26,000; however, this number is calculated treating a firm that employs 10,000 workers with the same weight as a company with 10. To be representative of the business economy as it exists, we weight labour productivity by the size of the firm. (Statistics calculated without employment weighting are still given in the accompanying dataset.)

4. Changes to the productivity distribution

This section presents kernel densities for labour productivity for different industry groups and employment sizes. Kernel densities are a statistical estimation technique that shows how data are distributed - in this case, approximate gross value added (aGVA) per worker at the firm level. Because we weight by employment, the kernel densities approximately represent the labour productivity distribution of workers across the business economy workforce.

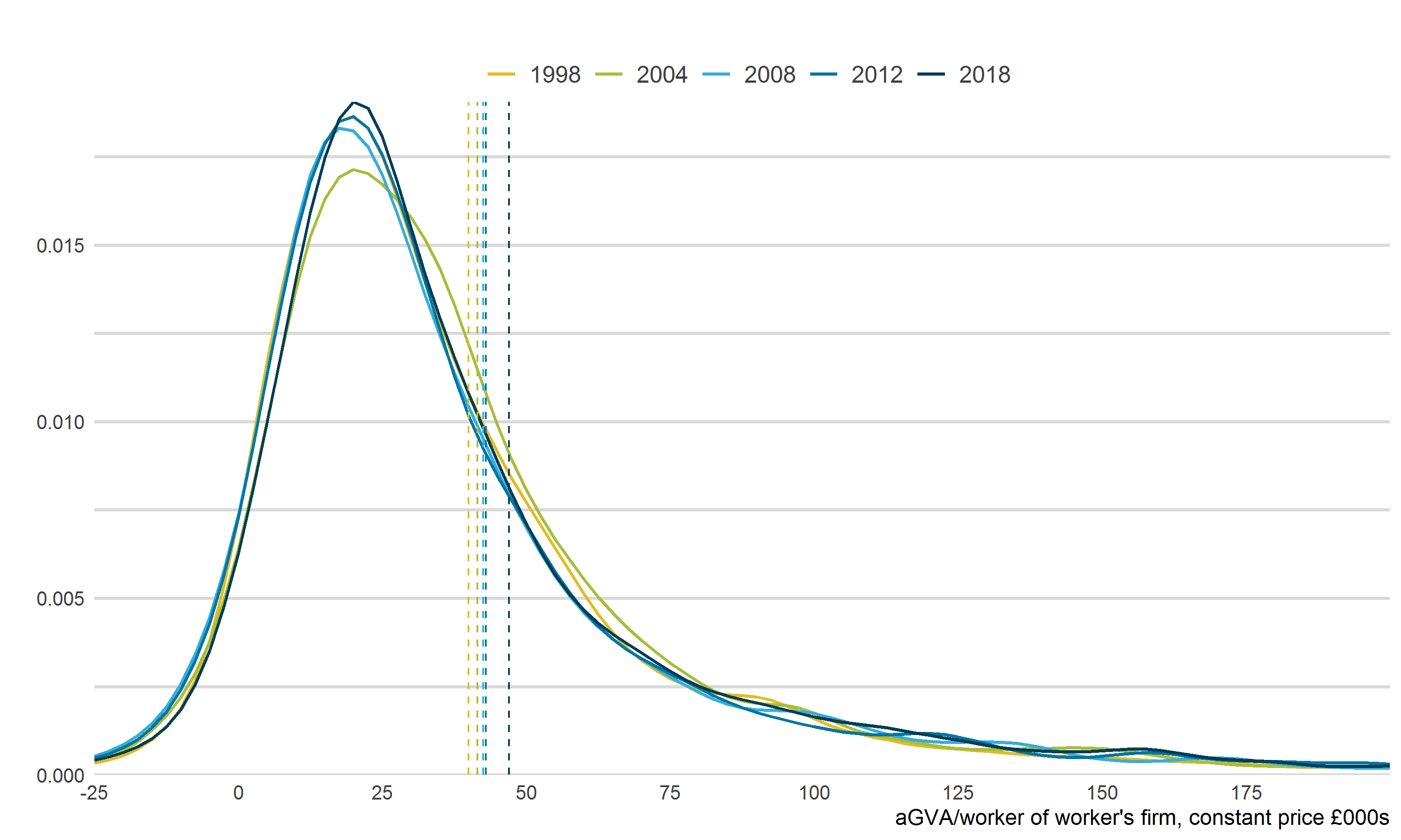

In Figure 1, the kernel densities represent the proportion of employees over the total workforce for each level of productivity - in this case for the whole Annual Business Survey (ABS). The total area under the distribution should be equal to 1, and the median will be where the 50% of the accumulated area is. Productivity is not distributed according to a normal distribution; the mean is not necessarily the same as the median.

Figure 1 shows that for most of the distribution there is relatively little change in constant price terms (equivalent to real prices). For the economy covered by the ABS, although mean productivity has been increasing for the last 20 years in constant prices, the distribution of productivity has remained consistent. The median increased by just 4%, from £27,500 output per person in 1998 to £28,500 in 2018.

Instead there is increasing dispersion. The overall productivity growth is driven by changes in the relative weight of the tails of the distribution, not the centre. In the same period the productivity of the 90th percentile increased by 18%, 14 percentage points more than the median. The coefficient of variation, the ratio of the standard deviation to the mean, which gives a separate measure of dispersion, increased from 1.10 to 1.52.

Figure 1: Workforce by labour productivity of the workers' business by selected years

Kernel density, constant prices, 1998 to 2018, Great Britain, business economy excluding agriculture and finance

Source: Office for National Statistics - Annual Business Survey (ABS), Inter-Departmental Business Register (IDBR)

Notes:

- Each dotted line shows the mean by year.

Download this image Figure 1: Workforce by labour productivity of the workers' business by selected years

.png (42.4 kB) .xlsx (36.7 kB){kind=link}

| GVA per worker (£000) | |||

|---|---|---|---|

| Year | Mean | Median | Coefficent of variation |

| 1998 | 40.0 | 27.5 | 1.10 |

| 2004 | 41.5 | 31.0 | 1.06 |

| 2008 | 42.5 | 27.0 | 1.35 |

| 2012 | 43.0 | 27.5 | 1.36 |

| 2018 | 47.0 | 28.5 | 1.52 |

Download this table Table 1: The largest increase in productivity has been from 2012 onwards

.xls .csvIndustry group

| GVA per worker (£000) | ||||

|---|---|---|---|---|

| Manufacturing | Non-Financial Market Services | |||

| Year | Mean | Median | Mean | Median |

| 1998 | 42.5 | 34.0 | 38.5 | 24.0 |

| 2008 | 56.5 | 44.0 | 41.0 | 26.0 |

| 2018 | 61.0 | 47.0 | 47.5 | 28.0 |

| Construction | Non-Market Services | |||

| Year | Mean | Median | Mean | Median |

| 1998 | 57.5 | 43.0 | 22.5 | 17.0 |

| 2008 | 56.0 | 41.0 | 20.0 | 16.5 |

| 2018 | 66.0 | 43.5 | 22.0 | 19.0 |

Download this table Table 2: Manufacturing has observed the largest improvement in productivity

.xls .csv

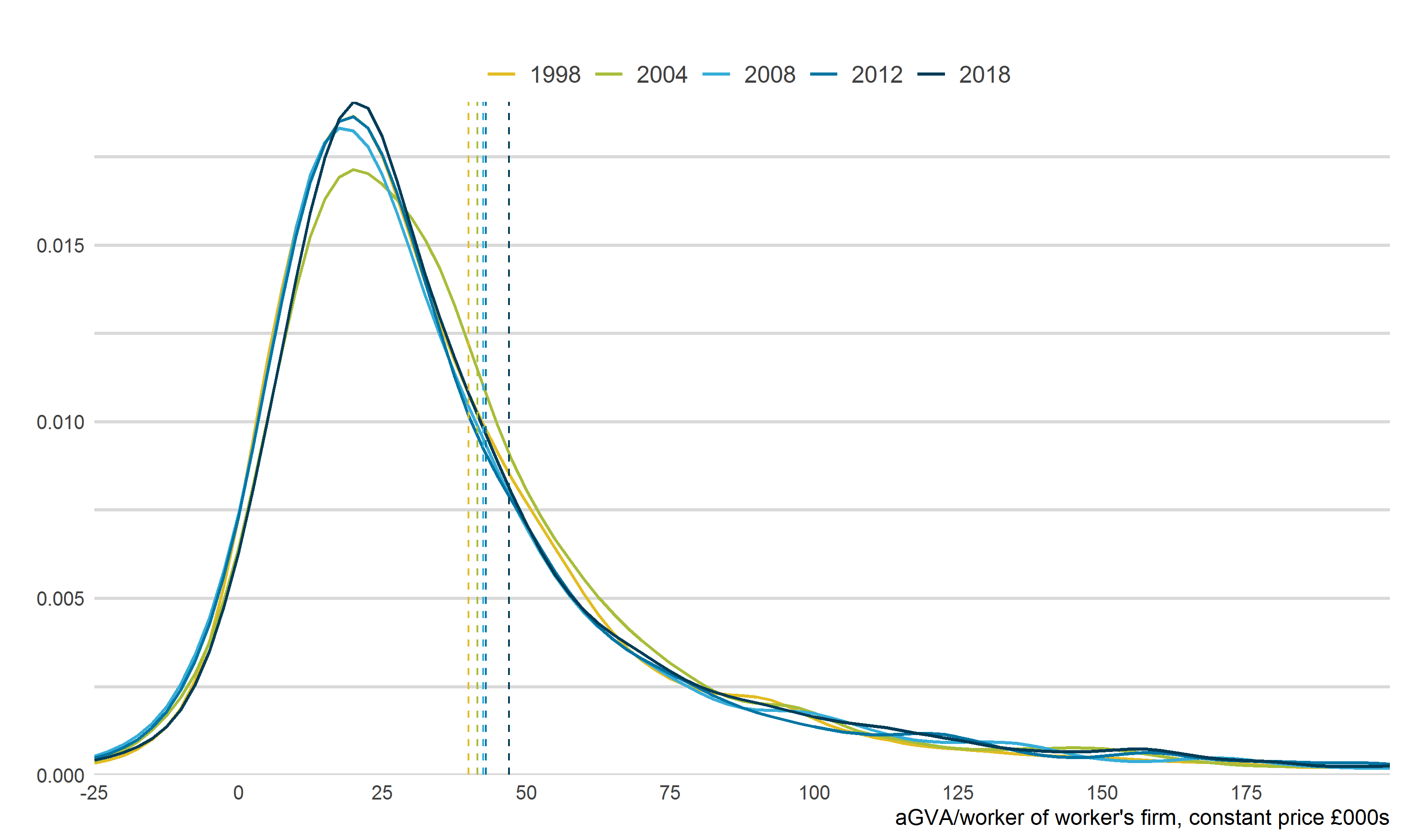

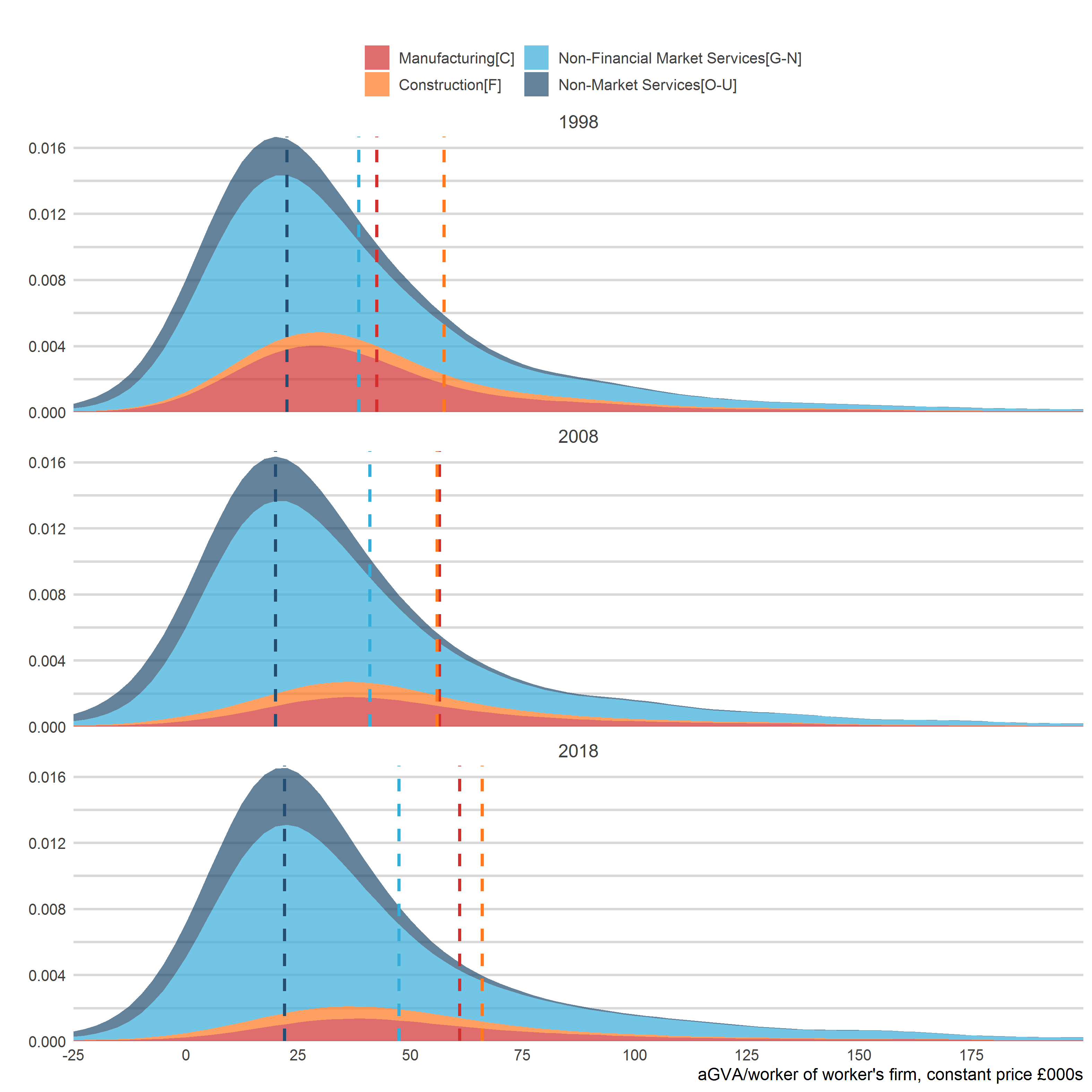

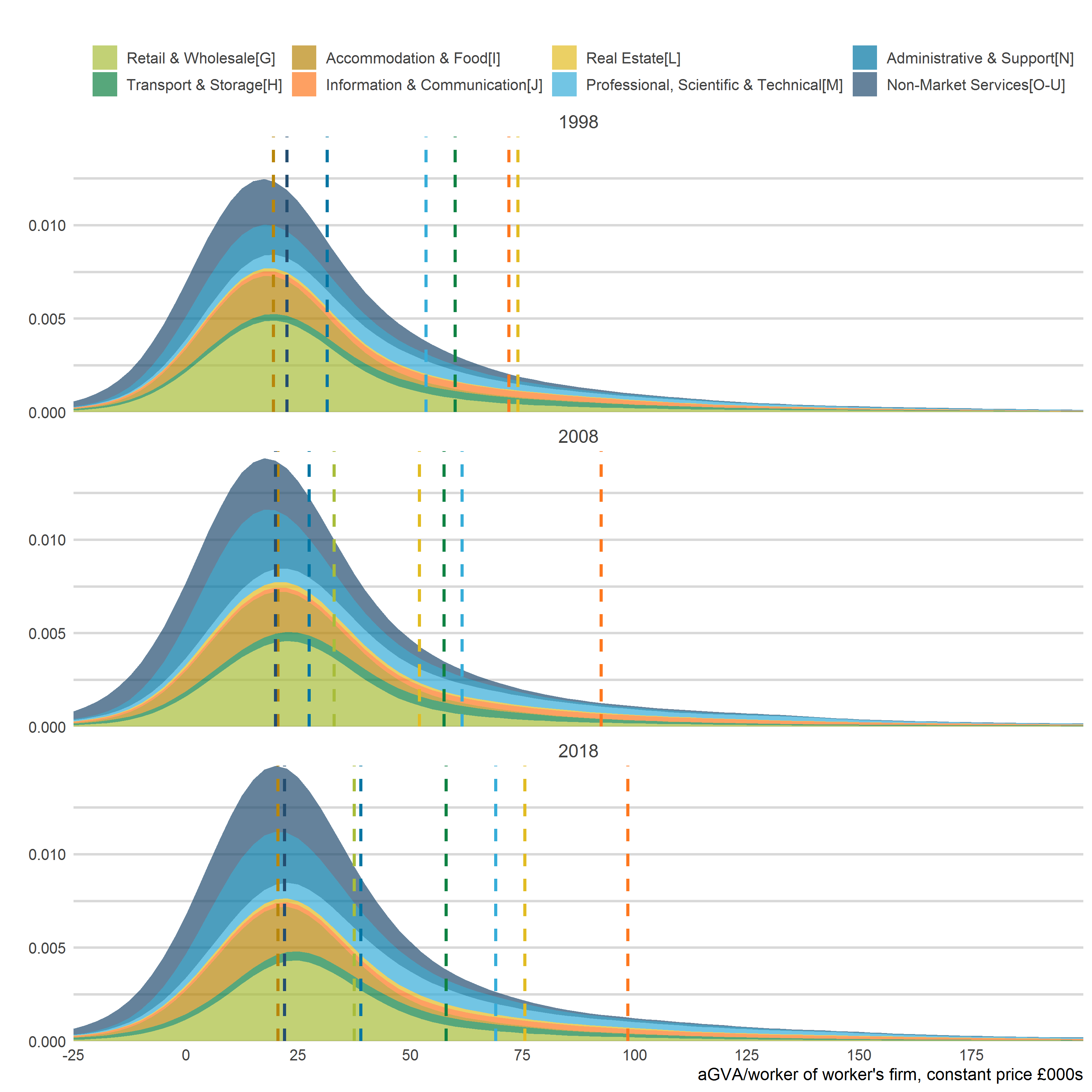

Figure 2: Workforce by labour productivity of the workers' business by selected years and high level industry

Kernel density, constant prices, 1998 to 2018, Great Britain, business economy excluding agriculture and finance by high level industry

Source: Office for National Statistics - Annual Business Survey (ABS), Inter-Departmental Business Register (IDBR)

Notes:

- Each dotted line shows the mean by year and high level industry.

Download this image Figure 2: Workforce by labour productivity of the workers' business by selected years and high level industry

.png (72.2 kB) .xlsx (58.0 kB){kind=link}

Figure 2 disaggregates the total ABS distribution by high-level industry classification to illustrate the changes of the industry composition during the last 20 years. This figure and the following kernel densities are different from Figure 1. The whole ABS distribution is drawn, and the different industries are stacked underneath as shown by the coloured areas, representing the proportion of employees in their respective industry at certain levels of productivity.

Manufacturing has evolved in the opposite direction to services. The sector has shrunk, driven by a relative decline in those manufacturing firms demonstrating lower levels of productivity. Figure 2 shows that the mean labour productivity for the manufacturing sector has increased by 43.5% from £42,500 to £61,000 of output per person since 1998.

Similarly, the median increased 38% from £34,100 to £47,000, while the workforce in manufacturing has fallen by 32.3% - the workforce accounted for by the manufacturing segment has fallen from 4,317,000 to 2,922,000. The decline in manufacturing employment continued from long before 1998, however, even after 1998, competitive pressures have had large effects.

A similar pattern is observed in the construction sector, but at a lower magnitude. Mean labour productivity increased by 14.8% from £55,000 to £64,700 of output per person since 1998. However, the decrease in the share of firms below the mean is not as substantial when compared with the manufacturing sector as the median remained effectively unchanged from £43,000 to £43,500.

Post-2008, the mean productivity of the non-financial market services increased from £38,500 to £47,500 of output per person, while the mean of the non-market services remained relatively stable and the density moved slightly upwards - an increase in the median from £17,000 to £19,000. These two services sectors combined dominate the whole economy, but with productivity below the mean with a mean productivity of £41,000 and a median of £25,200 of output per person in 2018. It may suggest that there is a lack of competition amongst service providers to drive up productivity.

Services breakdown

| GVA per worker (£000) | ||||

|---|---|---|---|---|

| Retail | Transport & Storage | |||

| Year | Mean | Median | Mean | Median |

| 1998 | 31.5 | 22.5 | 60.0 | 43.5 |

| 2008 | 33.0 | 25.5 | 57.5 | 38.5 |

| 2018 | 37.5 | 25.0 | 58.0 | 41.0 |

| Accommodation & Food | Non-Market Services | |||

| Year | Mean | Median | Mean | Median |

| 1998 | 19.5 | 16.0 | 22.5 | 17.0 |

| 2008 | 20.5 | 17.0 | 20.0 | 16.5 |

| 2018 | 20.5 | 18.0 | 22.0 | 19.0 |

| Information & Communication | Real Estate | |||

| Year | Mean | Median | Mean | Median |

| 1998 | 72.0 | 54.5 | 74.0 | 33.0 |

| 2008 | 92.5 | 78.5 | 52.0 | 31.0 |

| 2018 | 98.5 | 74.5 | 75.5 | 47.0 |

| Professional, Scientific and Technical | Administrative and Support Service | |||

| Year | Mean | Median | Mean | Median |

| 1998 | 53.5 | 42.5 | 31.5 | 18.0 |

| 2008 | 61.5 | 50.0 | 27.5 | 16.0 |

| 2018 | 69.0 | 48.0 | 39.0 | 20.0 |

Download this table Table 3: Information and Communication and Professional, Scientific and Technical have observed the largest improvement in productivity

.xls .csv

Figure 3: Workforce by labour productivity of the workers' business by selected years and services sectors excluding financial services

Kernel density, constant prices, 1998 to 2018, Great Britain, services sector excluding financial services

Source: Office for National Statistics - Annual Business Survey (ABS), Inter-Departmental Business Register (IDBR)

Notes:

- Each dotted line shows the mean by year and services sector.

Download this image Figure 3: Workforce by labour productivity of the workers' business by selected years and services sectors excluding financial services

.png (89.6 kB) .xlsx (94.0 kB){kind=link}

Figure 3 disaggregates the services sectors from Figure 2 in further detail. The two main non-financial services industries that are driving productivity growth are information and communication, and professional, scientific and technical activities. The whole distribution of information and communication has also shifted upwards, with mean productivity increasing by 36.8% – from £72,000 of output per person in 1998 to £98,500 in 2018 – and indicating an improvement of the median productivity from £54,500 in 1998 to £74,500 in 2018. In professional, scientific and technical activities, mean productivity grew by 29% and the distribution shifted towards the right-hand side as the median improved from £42,500 to £48,000 of output per worker.

Size-band

| GVA per worker (£000) | ||||

|---|---|---|---|---|

| Micro (<10) | Small (10-49) | |||

| Year | Mean | Median | Mean | Median |

| 1998 | 38.0 | 24.0 | 36.0 | 26.0 |

| 2008 | 39.0 | 25.0 | 40.0 | 29.5 |

| 2018 | 38.0 | 21.5 | 43.0 | 29.0 |

| Medium (50-249) | Large (>250) | |||

| Year | Mean | Median | Mean | Median |

| 1998 | 39.5 | 31.5 | 42.5 | 28.5 |

| 2008 | 44.5 | 32.5 | 42.5 | 26.0 |

| 2018 | 49.5 | 35.0 | 48.0 | 30.0 |

Download this table Table 4: Small and medium sized firms have observed the largest improvement in mean productivity

.xls .csv

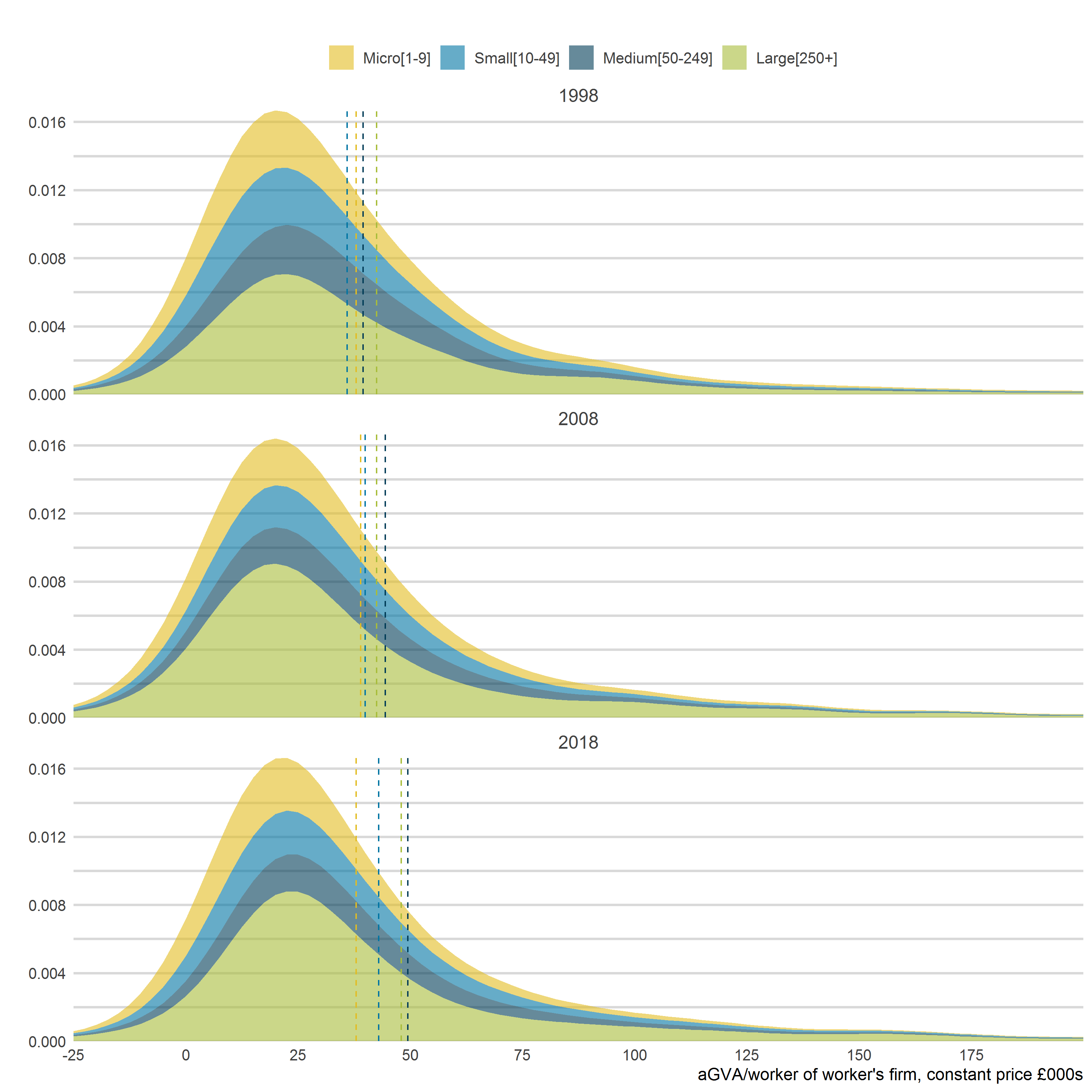

Figure 4: Workforce by labour productivity of the workers' business by selected years and employment size bands

Kernel density, constant prices, 1998 to 2018, Great Britain, business economy excluding agriculture and finance by employment size bands

Source: Office for National Statistics - Annual Business Survey (ABS), Inter-Departmental Business Register (IDBR)

Notes:

- Each dotted line shows the mean by year and employment size band.

Download this image Figure 4: Workforce by labour productivity of the workers' business by selected years and employment size bands

.png (77.4 kB) .xlsx (57.5 kB){kind=link}

Figure 4 presents the total ABS kernel density by four size-bands based on the firms' level of employment: micro firms (fewer than 10 employees), small firms (10 to 49 employees), medium size firms (50 to 249 employees) and large firms (more than 250 employees).

The proportion of small and medium-sized enterprises (SMEs) in the lower levels of productivity has decreased relative to big firms. This result is mainly driven by the increase in the mean productivity of small and medium size firms over the last 20 years - 19.4% and 25.3%, respectively. The concentration of less productive firms has decreased for micro, small and medium size firms since 1998, whilst it has remained relatively constant for larger firms. The median productivity for larger firms has experienced a small increase from £28,500 to £30,000 of output per work since 1998, despite an increase of 13.0% in its mean.

Notes for: Changes to the Productivity Distribution

- Since aGVA per person is a ratio that often has a small denominator, errors and outliers on either side can produce extreme productivity values for a small number of firms that create extremes for the distributions. The graphs are truncated to negative £25,000 to positive £200,000 aGVA per person.

5. Firm-level productivity by firm characteristics

Firms that are larger, that are older, or that are foreign-owned are generally more productive.

| GVA per worker (£000) | ||

|---|---|---|

| Employment band | Mean | Median |

| 1 to 9 | 38 | 21.5 |

| 10 to 49 | 43 | 29 |

| 50 to 99 | 47.5 | 34 |

| 100 to 249 | 50.5 | 36 |

| 250 to 999 | 55 | 36.5 |

| 1,000 and over | 45 | 27.5 |

| GVA per worker (£000) | ||

| Age band | Mean | Median |

| 2 years or younger | 41 | 24.5 |

| 3 to 5 years | 50 | 28 |

| 6 to 10 years | 49.5 | 25.5 |

| 11 to 20 years | 52 | 29.5 |

| 21 years or older | 49 | 31.5 |

| GVA per worker (£000) | ||

| Ownership | Mean | Median |

| Domestic | 41 | 25.5 |

| EU Owned | 66 | 40.5 |

| Non-EU Owned | 79 | 42.5 |

Download this table Table 5: In 2018, businesses that were larger, older and foreign-owned were more productive, on average

.xls .csvFirms that are larger - in terms of employment - are more productive on average. Mean labour productivity at businesses with between 250 and 999 workers was around 45% higher than that of the smallest businesses in 2018, and around 70% higher at the median.

Firms with more than 1,000 employees are less productive than those with 250 to 999 workers largely because of composition effects from being in industries with more part-time workers. In 2018, around 40% of total businesses in this size bracket and around 52% of total employment were in the five lowest productivity industries. These industries were retail trade (Standard Industrial Classification (SIC) Division 47), employment activities (Division 78), food and beverage service activities (Division 56), education (Division 85), and services to buildings and landscape activities (Division 81). The largest high employment industries have lower average hours worked per employee than the average for the whole economy (ONS 2020) with employees in SIC Division 56 working 83% of the average hours for the whole economy.

Table 5 also shows that there is a productivity premium for older and foreign-owned firms. In 2018, mean labour productivity at businesses older than 21 years was around 20% higher than the youngest businesses and around 29% higher at the median. This relationship is analysed in greater detail later in this section.

EU-owned firms had mean labour productivity roughly 61% higher than their domestically owned counterparts while non-EU owned firms were 93% more productive. These productivity premiums are 51% and 67%, respectively, at the median. As barriers and costs to entry may have been lower, EU-owned firms may have been willing to take greater risk in acquiring firms with lower productivity, which could be partly explained by the difference in premia. Apart from this, foreign-owned businesses might also have access to cheaper inputs through economies of scale in purchasing, more structured management practices or access to more advanced technologies or processes, which all allow them to be more productive.

To assess the strength and robustness of the previous findings, we combine the full range of firm-level characteristics to which we have access in a single regression framework, the results of which are set out in this section. In these regressions, we increase the number of variables included in our analysis across the specifications to identify the strongest correlates with productivity.

These results show that the relationships found in the previous descriptive work hold even when controlling for other firm characteristics. We find a positive, but concave, relationship between size (employment) and productivity as we further analyse in the following charts. We find a similar relationship between age and productivity, as we observe in Figure 7. We also find a significant, positive productivity premium associated with foreign-owned businesses: this result suggests that a foreign-owned business is around 14% more productive than an equivalent, domestically owned business.

Our regressions only explain roughly a quarter of the variation in productivity (25.7%) even when regressing on size, age, foreign ownership with controls for year, industry and location. This highlights that although our analysis has identified several significant relationships, productivity variation is the result of myriad factors. A large bank of productivity literature has suggested several potential reasons for the high degree of productivity dispersion within industry such as idiosyncratic productivity shocks, friction and economies of scope.

| Log GVA per worker | ||||

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| Log Employment | 0.124*** | 0.1*** | ||

| (0.004) | (0.004) | |||

| Log Employment Squared | -0.007*** | -0.0055*** | ||

| (0.0004) | (0.0004) | |||

| Age | 0.024*** | 0.015*** | ||

| (0.0016) | (0.002) | |||

| Age Squared | -0.0004*** | -0.0003*** | ||

| (0) | (0) | |||

| EU Owned | 0.234*** | 0.137*** | ||

| (0.0156) | (0.016) | |||

| Non-EU Owned | 0.280*** | 0.186*** | ||

| (0.01) | (0.011) | |||

| 2-digit Industry Controls | Yes | Yes | Yes | Yes |

| Region Controls | Yes | Yes | Yes | Yes |

| Year Controls | Yes | Yes | Yes | Yes |

| Observations | 933,852 | 933,705 | 933,852 | 933,705 |

| R-squared | 0.252 | 0.241 | 0.240 | 0.257 |

Download this table Table 6: Businesses that are larger, older and foreign-owned are more productive, on average

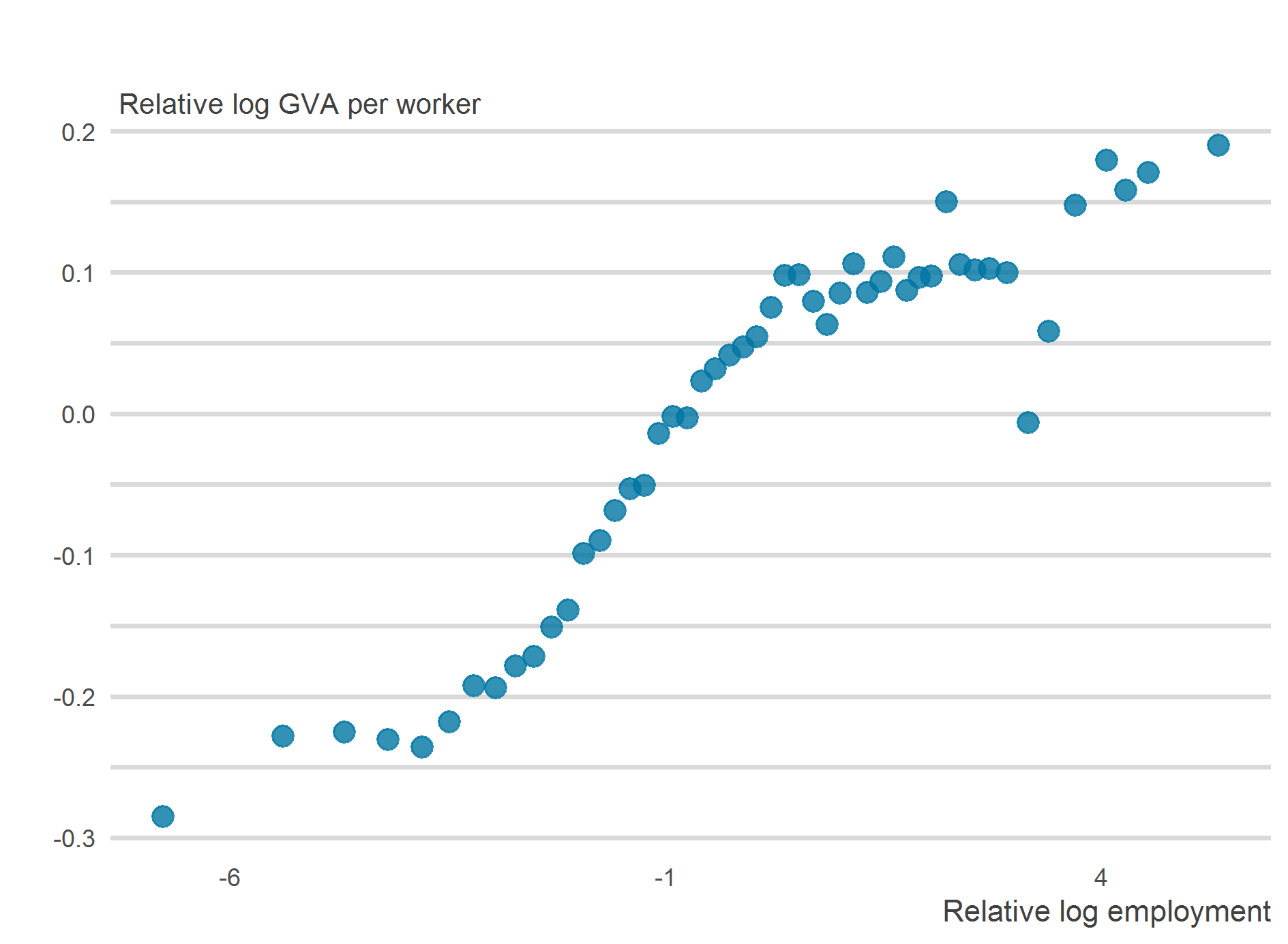

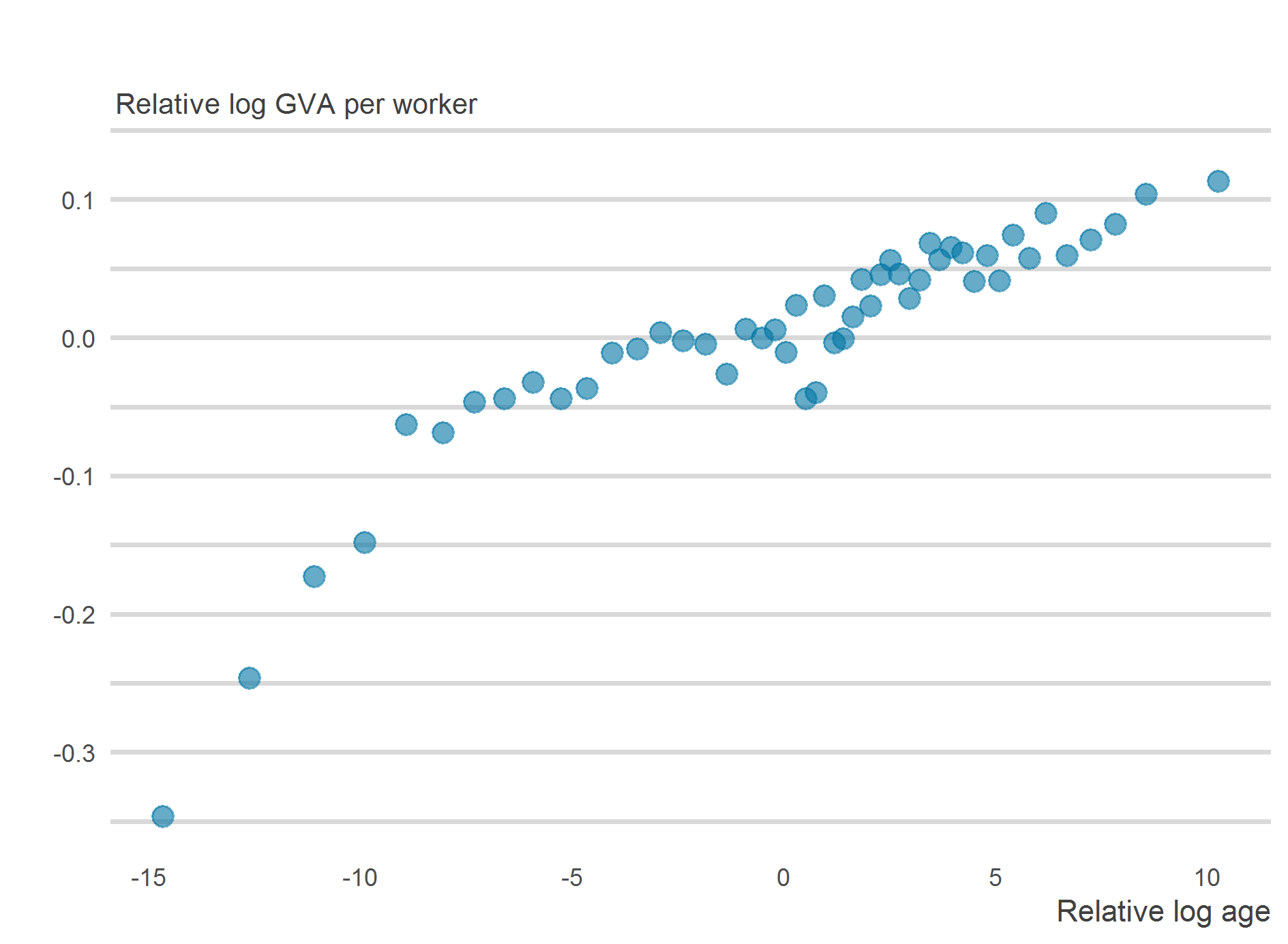

.xls .csvTo isolate the association between size and productivity more clearly, Figure 5 presents the results of conditional analysis, which compares the log size of businesses, after accounting for the effect of the control variables, with the log labour productivity of those same businesses, again after accounting for the effect of the control variables. This shows the relationship between the two key variables in the regression, but in a graphical way.

This depiction shows that, when industry, location, and survey year are controlled for, there is an S-shaped relationship between size and productivity. For most firms there are returns to scale, but the returns to scale are diminishing once the firm is large, after controlling for the variables. There is also a point at which the returns set in, and for the smallest firms after controlling for the variables, the relationship is similarly flat.

Economies of scale can be in terms of reduced average costs per unit, specialisation of the labour force or increased ability to invest in technology. However, these factors all have fixed costs and limits as the relationship shows.

Figure 5: Larger businesses are more productive than smaller businesses, on average

Binscatter, Constant Prices, Great Britain, 1998 to 2018

Source: Office for National Statistics - Annual Business Survey (ABS), Inter-Departmental Business Register (IDBR)

Notes:

- This chart shows the relationship between employment and labour productivity, after controlling for industry, location, and survey year. It was created using the ‘binscatter’ Stata package. This process first calculates the residuals of employment and log labour productivity after controlling for industry and survey year. It then splits observations into 50 bins according to age and calculates the mean residual of employment and mean residual of log labour productivity in each bin.

- Includes all businesses covered by the Annual Business Survey (ABS) excluding section K (Financial and insurance activities).

- The data exclude the top and bottom 1% of businesses in terms of productivity; businesses that record zero turnover and purchases in a period.

- The data are in 2016 constant prices and weighted by ABS sample weights and employment.

Download this image Figure 5: Larger businesses are more productive than smaller businesses, on average

.png (21.3 kB) .xlsx (26.6 kB){kind=link}

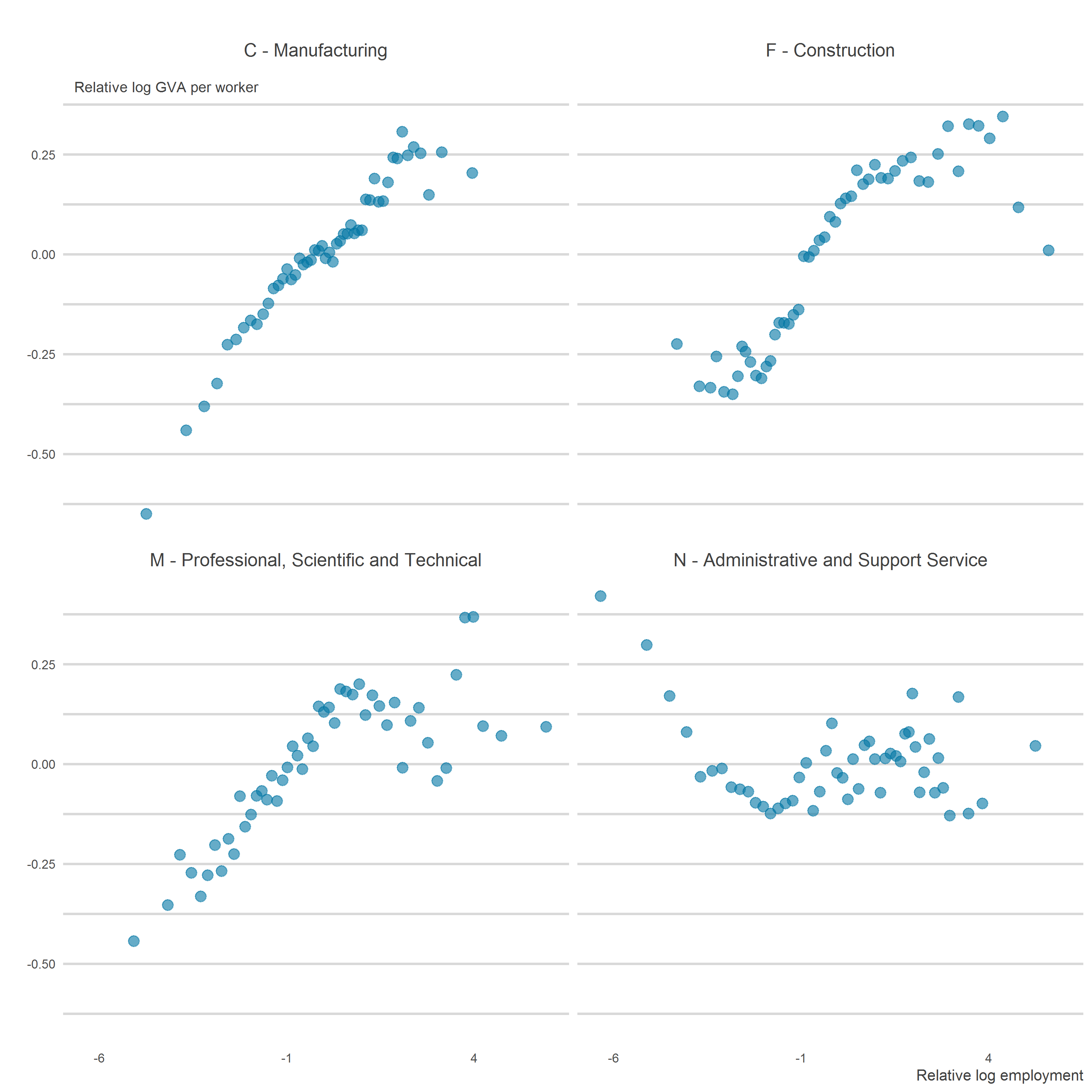

This relationship between firm size (employment) and productivity varies depending on industry. For example, manufacturing has a stronger positive relationship and less of a concave shape than other industries. This suggests that manufacturing has a greater capacity to benefit from economies of scale than services industries. This relationship also appears to be true for firms in the construction sector, although the productivity increase from more employees is smaller. In contrast, some services sector industries, particularly where there are in-person services, do not show economies of scale.

When replicating the regression specification in Table 6 for individual industries, manufacturing has the strongest economies of scale. A 1% increase in employment results in varying increases in productivity for different industry sections: 0.1% in manufacturing, 0.08% in construction, a 0.01% decrease in administrative and support services activities and a 0.1% increase in professional, scientific and technical activities.

For manufacturing the relationship is linear, while for the other sectors the employment squared term is negative, showing decreasing returns to scale. From a 1% increase in employment, the GVA per worker increases by 0.19% in construction while having a decrease of 0.01% from a 1% increase in employment squared. The results are similar for professional, scientific and technical activities firms with a 0.2% increase from employment and a 0.01% decrease from a 1% increase in employment squared. Full regression results are available in the accompanying dataset, while Figure 6 shows the graphical relationship.

Figure 6: Relationship between size and labour productivity for Manufacturing (SIC C), Construction (SIC F), Professional, Scientific and Technical Activities (SIC M) and Administrative and Support Service Activities (SIC N) firms

Binscatter, Constant Prices, Great Britain, 1998 to 2018

Source: Office for National Statistics - Annual Business Survey (ABS), Inter-Departmental Business Register (IDBR)

Notes:

- This chart shows the relationship between employment and labour productivity, after controlling for industry, location, and survey year. It was created using the ‘binscatter’ Stata package. This process first calculates the residuals of employment and log labour productivity after controlling for industry and survey year. It then splits observations into 50 bins according to age and calculates the mean residual of employment and mean residual of log labour productivity in each bin.

- Includes all businesses covered by the Annual Business Survey (ABS) excluding section K (Financial and insurance activities).

- The data exclude the top and bottom 1% of businesses in terms of productivity; businesses that record zero turnover and purchases in a period.

- The data are in 2016 constant prices and weighted by ABS sample weights and employment.

Download this image Figure 6: Relationship between size and labour productivity for Manufacturing (SIC C), Construction (SIC F), Professional, Scientific and Technical Activities (SIC M) and Administrative and Support Service Activities (SIC N) firms

.png (70.2 kB) .xlsx (33.3 kB){kind=link}

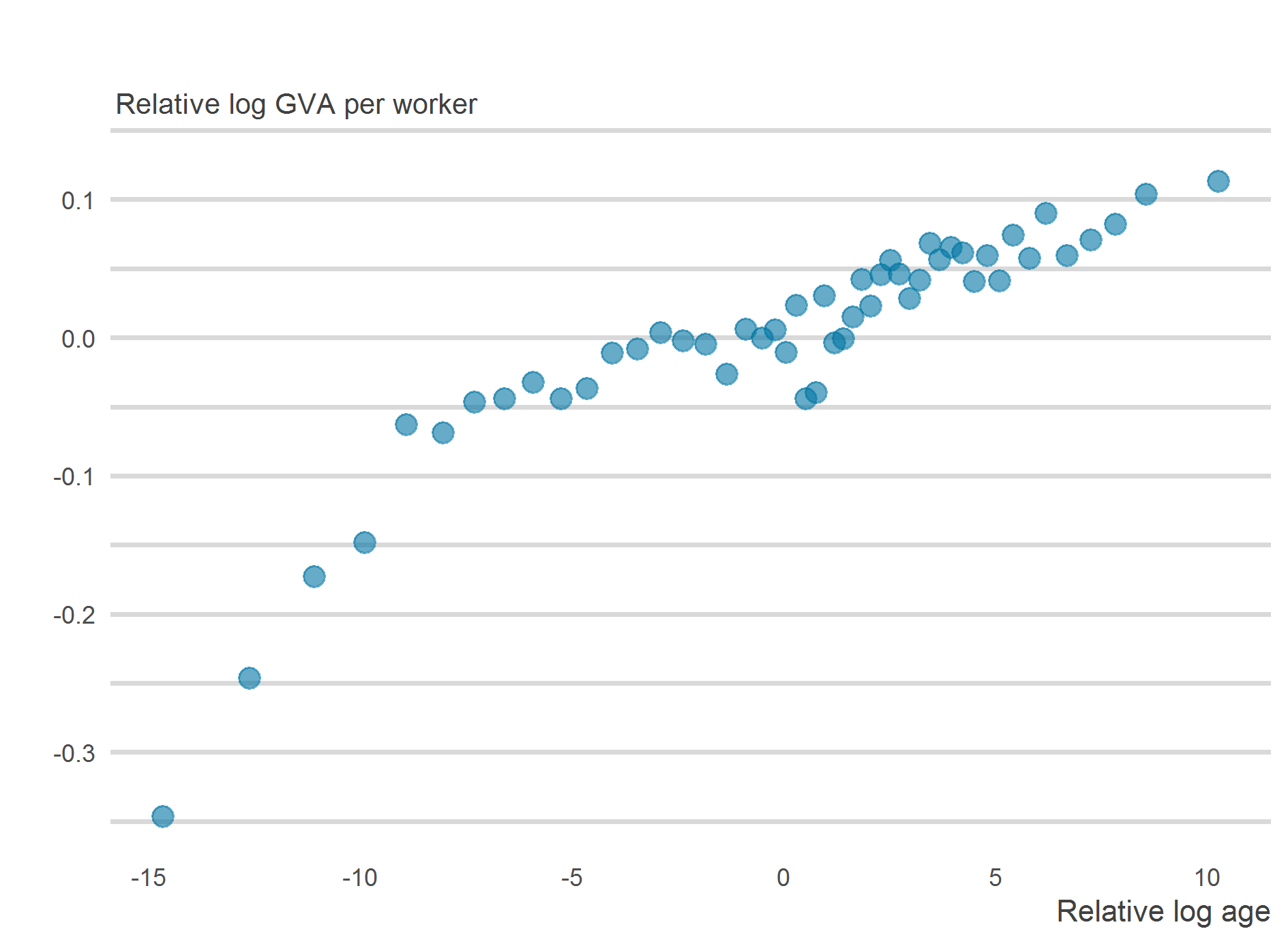

Older firms appear to be on average more productive than younger firms. Again, this relationship is robust to the inclusion of survey year and industry controls.

The binscatter graph in Figure 7 indicates a positive relationship between age and productivity. In the initial phase of the firms’ formation, it shows that they experience an initial period of strong growth then stabilise. As with size, the relationship between labour productivity and age is concave – indicating that the positive association between age and productivity is weaker for older businesses. The extent to which this reflects learning – that businesses get more productive as they get older – or whether it reflects the closure of less-productive businesses over time is difficult to isolate. Both theories are plausible channels.

Figure 7: Older businesses are more productive than younger businesses, on average

Binscatter, Constant Prices, Great Britain, 1998 to 2018

Source: Office for National Statistics - Annual Business Survey (ABS), Inter-Departmental Business Register (IDBR)

Notes:

- This chart shows the relationship between age and labour productivity, after controlling for industry and survey year. It was created using the ‘binscatter’ Stata package. This process first calculates the residuals of age and log labour productivity after controlling for industry and survey year. It then splits observations into 50 bins according to age and calculates the mean residual of age and mean residual of log labour productivity in each bin.

- Includes all businesses covered by the Annual Business Survey (ABS) excluding section K (Financial and insurance activities).

- The data exclude businesses that are aged 25 or above; the top and bottom 1% of businesses in terms of productivity; businesses that record zero turnover and purchases in a period.

- The data are in 2016 constant prices and weighted by ABS sample weights and employment.

Download this image Figure 7: Older businesses are more productive than younger businesses, on average

.png (20.0 kB) .xlsx (28.7 kB){kind=link}

7. Appendix A – Data and methods

The Annual Business Survey (ABS) is the main structural business survey conducted by the Office for National Statistics (ONS), surveying around 62,000 businesses in the non-financial business economy, covering approximately two-thirds of the UK economy. Before 2008, the survey was called the Annual Business Inquiry, and we include data from the Annual Business Inquiry going back to 1998.

This analysis uses the microdata for Great Britain. Coverage varies over time; at different points elements of finance, insurance, general government schools and hospitals are captured in the data, which we exclude for consistency. With the response rate stable at 80%, this provides an average of around 46,000 business-level observations per year from 1998 to 2018.

The ABS provides information on turnover and intermediate purchases, which can be used to estimate businesses' approximate gross value added (aGVA). It is a measure of the income generated by those surveyed, less their intermediate consumption of goods and services used up in order to produce their output. (Full GVA would include slightly more expansive definitions of turnover and intermediate consumption, for example, including financial intermediation services indirectly measured - FISIM - for financial services consumed without direct payment.)

The measure of labour input we use is a simple employment headcount - including both employees and working proprietors, and covering both full-time and part-time workers. This was obtained from the Inter-Departmental Business Register (IDBR) at the time of sample selection for the ABS. Employment information from the IDBR is derived from a number of different sources (including the Business Register Employment Survey (BRES), HM Revenue and Customs (HMRC) records and some imputation) and some of the employment information - especially for small businesses - may be several years old. Despite this limitation, the IDBR is the most comprehensive source of employment information, although results generated from this source need to be treated with appropriate caution. The measure of labour productivity used in this analysis is simply the aGVA of a business divided by their employment.

A number of firm characteristics are also obtained from the IDBR. Business-level industry information (five-digit Standard Industrial Classification (SIC)) is taken from the IDBR, from which we construct more aggregated industry groupings. There have been employment-weighted modal SIC conversions applied for years prior to 2007. We derive the age of a business as the difference between the survey year and the business' birth date recorded on the IDBR. Finally, the IDBR provides a variable to identify firms that are foreign-owned. This differs from the measure used in ONS (2017c) in that it refers to ultimate foreign ownership - not immediate foreign ownership - and does not capture outward foreign direct investment (FDI) of British businesses.

In the dataset we present labour productivity in current and constant prices. We deflate aGVA from the ABS using a set of experimental industry deflators. These deflators were derived by allocating national accounts product-level deflators to industries, weighting them using information on industry-level output shares from the supply and use table. As such, these deflators are constant across businesses in the same industry and survey year, which introduces error when the firm's product mix is different from the product mix of the industry. The ways this bias can manifest is well-known in the literature on firm-level productivity1.

Unless otherwise stated, the results in this article are weighted using survey design and employment to reflect total employment. This has the effect of weighting larger businesses - those that employ more people - more heavily than smaller businesses. This approach is appropriate from the perspective of overall labour productivity, the average level of output per worker of the workforce of a section of the economy, rather than per business.

A sample change to the ABS in 2016 included all reporting units of an enterprise, which increased the number of micro firms surveyed. To assess the impact of this sample change, we have compared a range of treatment options. We have focussed the investigation on micro firms (those with fewer than 10 employees) where we see a large outlier proportion and greater impact on results. The time series for productivity of micro firms also changed at this point, and we have investigated how the sample methods change may have affected the results with different outlier treatments. Figure 8 shows the treatments to reduce the impact of the 2016 sample change on mean labour productivity figures for micro firms in the ABS.

Figure 8: Mean Gross Value Added per worker, micro firms (less than 10 employees)

Constant prices, 1998 to 2018, Great Britain

Source: Office for National Statistics - Annual Business Survey (ABS), Inter-Departmental Business Register (IDBR)

Download this chart Figure 8: Mean Gross Value Added per worker, micro firms (less than 10 employees)

Image .csv .xlsWe present two treatments in this section, with no treatment shown for comparison.

The standard approach to outliers, which is used in this article, is to trim 1% of observations at the top and bottom of the distribution. In further editing, marked outliers are given a weight of one, to limit their influence on survey estimates when weighting for population results. This produces a smaller decline of mean labour productivity in 2016, showing the drop is driven by outliers. Other statistical methods investigated but not presented here, such as Windsorizing, obtained similar results.

Because of the sample change in 2016, there are some reporting units in this size band that belong to a larger enterprise group. In the final treatment, we remove all reporting units belonging to a larger enterprise group from this size band for micro firms. The same 1% trim is applied to the remaining businesses, and all outliers are weighted to one. This produces a smaller decline of 11% in mean labour productivity in 2016 compared with a 16% fall in data with no treatment. A lower mean labour productivity is produced over the entire period, similar to the first treatment. The reporting units part of larger enterprise groups have masked the smaller decline of productivity in 2016 and the lower mean productivity of the micro firms. These results show that the reporting units part of larger enterprise groups should be treated as outliers in this size band for micro firms.

We are conducting further investigations into statistical outlier detection and data validation for the wider ABS productivity statistics.

Notes for: Data and methods

- Office for National Statistics (2019), 'Firm-level labour productivity measures from the Annual Business Survey, Great Britain: 2017'

- See the Annual Business Survey technical report: August 2018.

Contact details for this Article

Related publications

- Productivity flash estimate and overview, UK: January to March 2026 and October to December 2025

- How productive is your business?

- UK trade in goods and productivity: new findings

- Management practices and productivity in British production and services industries - initial results from the Management and Expectations Survey: 2016

- Foreign direct investment and labour productivity, a micro-data perspective: 2012 to 2015

- Understanding firms in the bottom 10% of the labour productivity distribution in Great Britain: “the laggards”, 2003 to 2015