Table of contents

- Main points

- Things you need to know about this release

- R&D expenditure continues long-term upward trend

- Pharmaceuticals R&D increases and leads the way for UK R&D

- UK civil and defence R&D expenditure rise

- Scientific R&D leads way for industry expenditure, but reduces share

- Employment in R&D increases to new high in 2017

- South East and East of England continue as largest spenders on performing R&D

- UK funding of business R&D continues to grow as overseas funding falls

- Over half of all UK business expenditure on performing R&D was by foreign-owned businesses

- Links to related statistics

- Quality and methodology

1. Main points

Expenditure on research and development (R&D) performed by UK businesses continued to grow, expanding by £1.1 billion to £23.7 billion in 2017, an increase of 4.9%.

Software development was the product group that had the largest growth in expenditure on R&D performed by UK businesses, of £358 million (34.7%).

London had the largest growth in regional business R&D expenditure, increasing by £448 million (19.1%) to £2.8 billion in 2017.

In 2017, total UK business employment in R&D grew by 7.4% to 231,000 full-time equivalents.

2. Things you need to know about this release

Business enterprise research and development (BERD) covers estimates of UK business expenditure and employment relating to research and development (R&D) performed in the UK in 2017.

The UK government’s Industrial Strategy includes a target to “raise investment on R&D to 2.4% of GDP by 2027”. UK R&D statistics are needed to assess how sectors of the economy are contributing towards reaching this policy goal. As the largest contributor to total UK R&D expenditure, the business sector is integral to achieving this objective. Progress to this target can be seen in the UK gross domestic expenditure on research and development: 2016 (GERD) statistical bulletin, which showed that GERD represented 1.67% of GDP in 2016. The business sector accounted for 1.1% of GDP in 2016.

In this statistical bulletin, R&D and related concepts follow internationally agreed standards defined by the Organisation for Economic Cooperation and Development (OECD), as published in the Frascati Manual (2015).

This release reports on R&D expenditure in UK businesses irrespective of the country of residence of the ultimate owner or users of the R&D produced.

R&D is measured by the expenditure on R&D performed by a business, or the funding received by a business for R&D work. These are often but not always the same. Performance is regarded as a more accurate measure than funding received by a business, as not all funds received may be used as intended.

Further information on business R&D estimates is available in the UK Business Enterprise Research and Development Quality and Methodology Information (QMI) report.

All figures quoted are in current prices unless otherwise stated.

Back to table of contents3. R&D expenditure continues long-term upward trend

Expenditure on research and development (R&D) performed by UK businesses was £23.7 billion in 2017. This was up from £22.6 billion in 2016, an increase of 4.9%. The average annual growth rate since 1993 was 4.3%.

A long-term upward trend is evident when considering R&D expenditure in constant price terms, with an average annual growth rate of 2.3% since 1993 levels (£13.7 billion; Figure 1). In constant price terms the increase from 2016 was 2.9%.

Figure 1: Expenditure by UK businesses on performing research and development, 1993 to 2017

Source: Office for National Statistics

Download this chart Figure 1: Expenditure by UK businesses on performing research and development, 1993 to 2017

Image .csv .xlsThe total business R&D expenditure in 2017 represented 1.1% of GDP. Since 1993, the estimate each year has been 1.0% or 1.1%.

Back to table of contents4. Pharmaceuticals R&D increases and leads the way for UK R&D

The term “product group” refers to the type of research and development (R&D) performed, in contrast to the industry classification of the business performing the R&D. The concept of “product groups” is described in more detail in the UK Business Enterprise Research and Development Quality and Methodology Information (QMI) report.

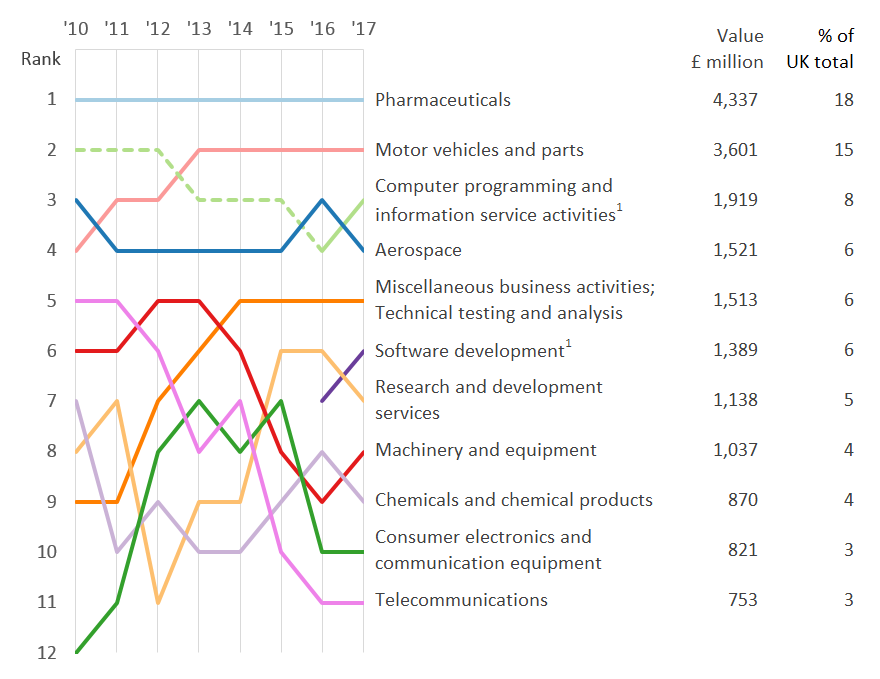

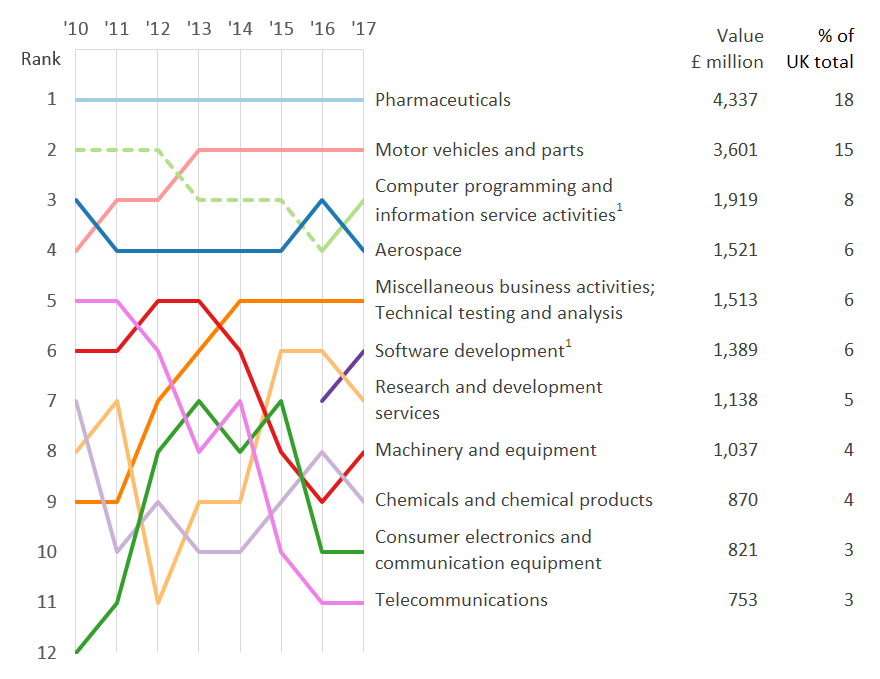

In 2017, pharmaceuticals continued to be the largest product group, with £4.3 billion expenditure, representing a 6.0% increase on 2016. This product group accounted for 18% of total expenditure on R&D performed in UK businesses, unchanged from 2016 (Figure 2).

The motor vehicles and parts group maintained its position as the second largest product group, continuing its long-term growth by increasing for an eighth successive year to £3.6 billion in 2017. This was an increase of £159 million (4.6%) from 2016 and still accounted for 15% of expenditure on R&D performed in UK businesses in 2017.

Figure 2: Expenditure by UK businesses on performing research and development in current prices, by largest product groups, 2010 to 2017

Source: Office for National Statistics

Notes:

- Prior to 2016, software development is included in the product group computer programming and information service activities.

Download this image Figure 2: Expenditure by UK businesses on performing research and development in current prices, by largest product groups, 2010 to 2017

.PNG (78.1 kB) .xls (28.7 kB){kind=link}

The product group with the largest increase was the software development group, which grew by £358 million (34.7%) to £1.4 billion in 2017. This group accounted for 6% of expenditure on R&D performed in UK businesses in 2017. Until 2016 software development was included in the computer programming and information services activities group. From 2016 they have been separated to be monitored individually.

In contrast, the largest decrease was in the aerospace group, which fell by £383 million (20.1%) in 2017. This decrease followed a rise in 2016 of £205 million (12.1%). In 2017, this group accounted for 6% of expenditure on R&D performed in UK businesses, down from 8% in 2016.

Other product groups reporting £1.0 billion or more R&D expenditure in the UK in 2017 were:

computer programming and information services activities (excluding software development), £1.9 billion (8% of total R&D expenditure)

miscellaneous business activities; technical testing and analysis, £1.5 billion (6%)

research and development, £1.1 billion (5%)

machinery and equipment, £1.0 billion (4%)

The top eight product groups reporting £1.0 billion or more on R&D expenditure accounted for 69% of the total UK business R&D expenditure in 2017.

Since 2016, two-thirds of all product groups experienced an increase in levels of R&D expenditure by UK businesses, with one-third decreasing.

More information on the UK Manufacturing and production industry and UK Businesses services is available.

Back to table of contents5. UK civil and defence R&D expenditure rise

Research and development (R&D) expenditure statistics can be split between the civil and defence sectors. Expenditure on R&D performed by UK businesses in the civil sector in 2017 (£22.1 billion) accounted for 93% of the total, with the remainder accounted for by defence (£1.6 billion). The values of R&D expenditure within the civil and defence sectors both grew in 2017, growing 5% and 2% respectively from 2016.

Further splits of civil and defence R&D, such as detailed product groups, sources of funds, capital expenditure and employment can be found in the 2017 datasets.

Back to table of contents6. Scientific R&D leads way for industry expenditure, but reduces share

Research and development (R&D) expenditure by industry, based on the Standard Industrial Classification 2007 (SIC 2007), were introduced in the 2011 Business enterprise research and development (BERD) statistical bulletin. These broaden the scope of the estimates (see Table 26 in the 2017 datasets).

It is important to note that estimates of R&D expenditure by industry and product group are not directly comparable. This is because businesses may report significant R&D in product groups that are different to the main classification of their business according to the SIC 2007. The concepts of product groups and SIC 2007 are described in more detail in the UK Business Enterprise Research and Development Quality and Methodology Information (QMI) report.

Businesses that were classified to the scientific research and development SIC 2007 had the highest level of expenditure on performing R&D in 2017 at £5.4 billion, up from £5.3 billion in 2016. This represented 23% of total expenditure, down from 24% in 2016 (Figure 3).

The industry with the largest increase was wholesale and retail trade; repair of motor vehicles and motorcycles which grew by £239 million (29%) in 2017. This industry accounted for 4% of expenditure on R&D performed in UK businesses in 2017.

The largest decrease by an industry, in contrast, was manufacture of other transport equipment which fell by £303 million (16.7%) in 2017. This industry also accounted for 6% of expenditure on R&D performed by UK businesses.

There are four other industries that had R&D expenditure of £1.0 billion or more:

manufacture of motor vehicles and trailers, £3.0 billion (13%)

computer programming, consultancy and related activities, £2.1 billion (9%)

architectural and engineering activities, £1.5 billion (6%)

manufacture of computer, electronic and optical products, £1.0 billion (4%)

These seven industries accounted for 66% of the total UK business R&D expenditure in 2017.

Figure 3: Percentage share of total expenditure by UK businesses on performing research and development, by largest industries, 2013 to 2017

Source: Office for National Statistics

Download this chart Figure 3: Percentage share of total expenditure by UK businesses on performing research and development, by largest industries, 2013 to 2017

Image .csv .xls7. Employment in R&D increases to new high in 2017

Estimates of employment in research and development (R&D) are produced on a full-time equivalent (FTE) basis, whereby businesses convert part-time employees’ hours into full-time employees’ equivalent. FTE estimates provide a better indication of total labour input than headcount.

Employment on R&D reached its highest level to date in 2017 at 231,000 (Figure 4). The number of FTEs employed on R&D rose by 7.4% from 215,000 in 2016. The number of researchers remained at 114,000, although their share of the total number of R&D FTEs, at 49% was down 4 percentage points since 2016. An increase of 31.6% in the number of “other supporting staff” accounted for the majority of the overall increase in FTEs in 2017. The increase in the total number of FTEs working on R&D continues the trend of steady growth since the last recorded decline in 2008.

While there has been growth in recent years in the number of people working on R&D, this should be seen in the context of a rise in the total employment in the UK labour market. Therefore, part of the growth in employment on R&D may reflect the wider growth in total employment in the economy. See our labour market statistics for more information on total employment levels.

The 2017 estimate comprised:

114,000 researchers (49%)

67,000 technicians (29%)

50,000 other supporting staff (22%)

Figure 4: Employment in UK businesses on performing research and development, 1993 to 2017

Source: Office for National Statistics

Download this chart Figure 4: Employment in UK businesses on performing research and development, 1993 to 2017

Image .csv .xls8. South East and East of England continue as largest spenders on performing R&D

Analysis of research and development (R&D) expenditure by country and region is also possible. In this context, “region” refers to the location where a business performs R&D, not the location of either the business’ headquarters or that of any external funders.

The South East and East of England continue to dominate where R&D expenditure takes place in the UK. These two regions combined accounted for 40% of UK business R&D expenditure in 2017. Together they also employed 82,000 full-time equivalent (FTE) staff, which made up 35% of total R&D employment in 2017.

The regions or countries with the lowest levels of employment on performing R&D were the North East, employing 5,000 FTEs and Wales and Northern Ireland employing 6,000 and 7,000 FTE R&D staff respectively. These regions or countries also have the lowest corresponding totals of expenditure on business R&D.

The majority (91%) of UK R&D expenditure was carried out in England in 2017. Businesses in England spent the equivalent of £386 per head of population on performing R&D, more than the other countries of the UK, with Northern Ireland spending £274, Scotland spending £230 and Wales spending £146.

The largest overall increase in expenditure by region since 2016 was in London, which rose by £448 million (19.1%) from £2.3 billion in 2016.

In terms of percentage growth since 2016, the largest increases by region were the North East (24.7%) and Yorkshire and the Humber (21.7%).

In contrast, two regions experienced a decrease in expenditure since 2016. North West fell by £203 million (8.5%) and East Midlands fell £155 million (9.2%).

Table 1 shows the change in expenditure on performing R&D by UK businesses between 2016 and 2017 for all regions of the UK.

Table 1: Regional expenditure on research and development performed in UK businesses, 2016 to 2017

| £ million | ||||||

|---|---|---|---|---|---|---|

| 2016 | 2017 | % change | ||||

| UK | 22,587 | 23,685 | 4.9 | |||

| North East | 308 | 384 | 24.7 | |||

| North West | 2,377 | 2,174 | -8.5 | |||

| Yorkshire and the Humber | 771 | 938 | 21.7 | |||

| East Midlands | 1,676 | 1,521 | -9.2 | |||

| West Midlands | 2,345 | 2,467 | 5.2 | |||

| East of England | 4,519 | 4,677 | 3.5 | |||

| London | 2,348 | 2,796 | 19.1 | |||

| South East | 4,730 | 4,860 | 2.7 | |||

| South West | 1,516 | 1,652 | 9.0 | |||

| Wales | 440 | 457 | 3.9 | |||

| Scotland | 1,075 | 1,247 | 16.0 | |||

| Northern Ireland | 481 | 512 | 6.4 | |||

| Source: Office for National Statistics | ||||||

| Notes: | ||||||

| 1. Differences may occur between totals and the sum of their independently rounded components. | ||||||

Download this table Table 1: Regional expenditure on research and development performed in UK businesses, 2016 to 2017

.xls (36.9 kB)9. UK funding of business R&D continues to grow as overseas funding falls

The largest source of research and development (R&D) funding in 2017 was businesses’ own funds at £17.7 billion, which increased by £1.1 billion (6.7%) from 2016. Businesses’ own funds accounted for 75% of total business R&D expenditure in 2017 compared with the 2016 estimate of 74%.

The only decrease in a source of funds for UK businesses performing R&D was from overseas, which dropped £260 million (7.4%) from 2016. This consisted of a decrease of £214 million (6.2%) of other overseas sources and £47 million (50.5%) in European Commission (EC) grants. The fall in EC funding since 2016 should be seen in the context of fluctuating year on year levels of funding since 1993, with values ranging from £27 million to £137 million over this period.

Since 2010, UK funding of businesses’ expenditure on performing R&D has increased by £8.2 billion (66.6%) to £20.4 billion in 2017. Over the same period overseas funding has dropped by £518 million (13.7%) to £3.3 billion in 2017. As a proportion of total funding of UK business R&D, overseas funding has reduced by 10 percentage points, from 24% in 2010 to 14% in 2017 (Figure 5).

The UK government’s funding of businesses’ R&D in 2017 was £1.8 billion, an increase of £98 million (5.8%) from 2016, representing 8% of total business R&D. This increase reversed the recent two-year decline.

Historically UK government funding was most prominent in the defence sector. For the first time UK government funding of civil R&D has overtaken that of defence, with funding in 2017 of £978 million (54%) and £820 million (46%) respectively.

Figure 5: UK and overseas funding of expenditure by UK businesses on performing research and development, 1993 to 2017

Source: Office for National Statistics

Notes:

- Differences may occur between totals and the sum of their independently rounded components.

Download this chart Figure 5: UK and overseas funding of expenditure by UK businesses on performing research and development, 1993 to 2017

Image .csv .xls10. Over half of all UK business expenditure on performing R&D was by foreign-owned businesses

In 1993, when the Business enterprise research and development (BERD) survey began on an annual basis, 73% of UK business research and development (R&D) expenditure was by UK-owned businesses. The majority of UK business R&D expenditure continued to be performed by UK-owned businesses until 2011, when for the first time, just over half (50.8%) of business R&D expenditure in the UK was by foreign-owned businesses. This pattern of ownership continued until 2016 when the share was equal at 50% (Figure 6). In 2017 however, the proportion of R&D performed by foreign-owned businesses has again overtaken that of UK-owned businesses at 52.2% and 47.8% respectively.

On 15 March 2013, we published R&D expenditure by foreign-owned businesses, which contained more detailed analysis of the pattern of ownership of businesses that performed R&D between 1995 and 2011. This was based on the estimates that had been included in the 2011 BERD statistical bulletin. It should be noted that the original 2011 estimate of the proportion of R&D expenditure by foreign-owned businesses has been revised upwards from 50% to 51%.

Figure 6: Ownership of businesses who perform research and development in the UK, 1993 to 2017

Source: Office for National Statistics

Notes:

- Differences may occur between totals and the sum of their independently rounded components.

Download this chart Figure 6: Ownership of businesses who perform research and development in the UK, 1993 to 2017

Image .csv .xls12. Quality and methodology

The Business enterprise research and development Quality and Methodology Information report contains important information on:

the strengths and limitations of the data and how they compare with related data

uses and users of the data

how the output was created

the quality of the output including the accuracy of the data

About the data

These points should be noted when examining this bulletin or the data tables:

respondents were asked to make a return for the calendar year 2017 or the nearest 12-month period for which figures were available – data for all years published in this statistical bulletin were collected on the same basis

there may be differences between totals and the sum of their independently rounded totals

in some tables, entries have been aggregated to avoid disclosure of figures in which the returns of individual businesses could be identified – where this happens, footnotes have been added to the tables

it is sometimes necessary to suppress figures for certain items to avoid disclosing data from individual institutions – tables which contain data which are disclosive will contain a relevant footnote

note that £1.0 billion equals £1,000 million in this release

the 2015 and 2016 estimates have been revised where necessary to take account of businesses misreporting and late returns

gross domestic product (GDP) deflators at market prices, and money GDP used is non-seasonally adjusted. The GDP deflators at market prices, and money GDP: September 2018 (Quarterly National Accounts) can be viewed as a measure of general inflation in the domestic economy.