1. Main points

Productivity measures based on the UK Tourism Satellite Account show that tourism productivity growth was higher than non-tourism productivity growth between 2008 and 2013.

Labour productivity measures based on jobs and hours worked for the accommodation industry show a rise in productivity in 2014 and 2015.

The labour productivity of sports activities peaks in Quarter 3 (July to Sep) 2012 which coincides with the Olympics.

Back to table of contents2. Introduction

What is productivity?

Productivity can be defined as the rate of output per unit of input used, expressed as a ratio of the 2 components. Productivity is an important metric in formulating and assessing government policy, as it helps define both the scope for raising living standards and the competitiveness of the economy.

Based on the above definition, each productivity statistic has 2 components: an input and an output. The input is usually one of labour (for example, the number of jobs), raw materials (in some industries), capital or a combination of all three. The output is usually either: total output (in manufacturing this could be the number of products produced); gross value added (GVA); or gross domestic product (GDP).

The changes in productivity over time are typically shown using calculated indices of productivity. The charts in this article will also show productivity growth using calculated indices. The base year of the index will be stated in each chart.

The productivity of tourism

Previous estimates of productivity in tourism (and creative industries) produced by the Department for Culture, Media and Sport (DCMS), found that between 2000 and 2007 there had been productivity growth in the tourism and leisure industries. This resulted from increased output (GVA) for the combined sector and by steady employment levels (input). There was little information within the report on the different industries that make up the tourism sector, however, and this article aims to address this. The DCMS report is available on the GOV.UK website. These estimates are no longer produced and there has been little independent research and analysis produced about the productivity of tourism in the UK since.

We aim to address this deficit of information about the productivity of tourism in the UK. The article details the estimates of tourism productivity produced by the Office for National Statistics (ONS) as part of this study, which was commissioned by DCMS.

Detailed in this article are 2 methods that can be used to produce estimates of the productivity of tourism in the UK:

annual productivity metrics based on the UK Tourism Satellite Account (UK-TSA), 2008 to 2013 using tourism direct gross value added (TDGVA) and tourism direct jobs

quarterly labour productivity metrics based on measures of labour productivity used by ONS, Quarter 1 (Jan to Mar) 2008 to Quarter 4 (Oct to Dec) 2015 for selected industry divisions (Standard Industrial Classification 2007 (SIC2007) 2 digit level); this does not include an overall index of productivity for tourism but does provide more detail on the industries that provide goods and services to tourists on a quarterly basis

This article will first outline the results of the productivity analysis based on these 2 measures, then compare and highlight the main differences in the 2 approaches and then further discuss the methodology behind both approaches of productivity estimates in more detail.

Back to table of contents3. Tourism Satellite Account productivity measures

The Tourism Intelligence Unit at the Office for National Statistics (ONS) has produced a UK-TSA for each year from 2008 to 2013. The latest release can be found on our website. The TSA consists of 7 tables containing important tourism aggregate measures for 11 tourism characteristic industries (as defined by the UN World Tourism Organisation; details can be found in Annex A, including their make-up of Standard Industrial Classification (SIC) codes), which can be used to produce an overall tourism productivity estimate.

A productivity statistic requires an input and an output. The components of this productivity estimate are the following:

- input: the number of jobs directly attributable to tourism (tourism direct jobs)

- output: the gross value added (GVA) directly attributable to tourism (tourism direct GVA (TDGVA))

For comparison purposes, estimates for non-tourism (or other) industries have been produced. The components for this measure are the number of jobs (input) and GVA (output) not attributable to tourism.

It should be noted that the TDGVA and GVA estimates used are in current prices and therefore are not adjusted for inflation.

Figure 1 compares tourism productivity with the productivity of non-tourism industries. The immediate effect of the economic downturn is seen in the slight decline in productivity of non-tourism industries between 2008 and 2009, whilst the productivity of tourism in the UK saw an increase over this period. The chart shows that the productivity of tourism increases more rapidly in comparison with other industries. However, the productivity of other industries grows sharply between 2012 and 2013 whereas tourism productivity growth decreases. The productivity of tourism in the UK was at its highest in 2012 – the year of the London Olympics, caused by a large increase in TDGVA and a steady increase in the number of jobs.

Figure 1: Productivity of tourism and non-tourism industries, UK, 2008 to 2013 (base year 2008=100)

Source: UK Tourism Satellite Account, 2008-2013, Office for National Statistics

Notes:

- Current prices

Download this chart Figure 1: Productivity of tourism and non-tourism industries, UK, 2008 to 2013 (base year 2008=100)

Image .csv .xlsThe UK-TSA tables contain a breakdown of 11 tourism characteristic industries. The remainder of this section compares different tourism characteristic industries with the productivity of tourism as a whole and the productivity of non-tourism industries.

The productivity estimates for each tourism characteristic industry are calculated with the following components:

- input: the number of jobs directly attributable to the specific tourism characteristic industry

- output: the TDGVA directly attributable to the specific tourism characteristic industry

Figure 2 examines the productivity growth of 2 tourism sectors: accommodation services for visitors and food and beverage serving activities, in comparison with the productivity growth of tourism and non-tourism industries.

Food and beverage serving activities follow a similar productivity growth to the whole tourism sector, although there are slight fluctuations year on year.

However, the growth of productivity in accommodation services for visitors is not as straightforward. Productivity grows between 2008 and 2010, declines in 2011, increases again in 2012 – the year of the Olympics (although the peak is not as high as 2010), then declines to pre-downturn levels in 2013. From further exploring the data, TDGVA follows a general upwards trend (with the exception of a peak in 2009); however, the number of jobs directly attributable to tourism fluctuates year on year, which causes the peaks and troughs in the productivity of accommodation services for visitors. This could be due to the part-time nature of many jobs in this sector.

Figure 2: Productivity of accommodation services for visitors and food and beverage serving activities, UK, 2008 to 2013 (base year 2008=100)

Source: UK Tourism Satellite Account, 2008-2013, Office for National Statistics

Notes:

- Current prices

Download this chart Figure 2: Productivity of accommodation services for visitors and food and beverage serving activities, UK, 2008 to 2013 (base year 2008=100)

Image .csv .xlsFigure 3 shows the change in productivity of travel agencies and other reservation activities; exhibitions and conferences etc; cultural activities; and sport and recreation activities, compared with the productivity growth of tourism and non-tourism characteristic activities.

There is steady productivity growth of cultural activities until 2011 when productivity declines.

The productivity growth of travel agencies and other reservation activities steadily grows.

There is a slight growth in productivity of sport and recreation activities between 2008 and 2009, before a sharp decline in 2010. There is a slow increase in productivity after that. A sharper rise may have been expected given the Olympics in 2012, but instead growth remains fairly flat between 2011 and 2013 and productivity is lower than in 2008.

The productivity growth of exhibitions and conferences etc is at a lower level than tourism and non-tourism industries throughout the time period. Productivity declines between 2008 and 2010, increases in 2011 before steadily decreasing until 2013. Productivity in this industry was at its highest level in 2008, then falls following the economic downturn.

Figure 3: Productivity of travel agencies and other reservation services and leisure activities, UK, 2008 to 2013 (base year 2008=100)

Source: UK Tourism Satellite Account, 2008-2013, Office for National Statistics

Notes:

- Current prices

Download this chart Figure 3: Productivity of travel agencies and other reservation services and leisure activities, UK, 2008 to 2013 (base year 2008=100)

Image .csv .xlsFigure 4 shows the productivity over time of different modes of passenger transport used by tourists, compared with the growth of productivity of tourism and non-tourism industries. As seen in the chart, the productivity growth of transport passenger services is a different picture to growth in other tourism characteristic industries and indeed tourism as a whole.

The productivity of railway passenger transport services is generally increasing at a much faster rate in comparison with non-tourism and tourism industries as a whole, with the exception of a slight dip in 2012 which was caused by the number of tourism direct jobs increasing at a larger rate than the increase of TDGVA in this industry.

Road passenger transport services productivity increases and peaks in 2011, before declining in 2012 and returning to its highest level of productivity in 2013. Initially the productivity growth was caused by increasing TDGVA and a decrease in the number of tourism direct jobs, but in 2012 there was an increase in jobs directly attributable to tourism alongside a decrease in TDGVA, causing the decline in productivity. There was also a decrease in TDGVA in 2013 but a larger decrease in jobs in the industry, which caused productivity to increase. Growth of productivity in road passenger transport services was always at a faster rate in comparison with tourism as a whole.

The productivity of UK-based water passenger transport services (for example, inland and coastal passenger ferry services) declines in 2009 which was due to a large decrease of TDGVA produced by this industry. However, productivity recovers and grows extremely quickly, mostly caused by increasing TDGVA which is matched by only a slight increase in tourism direct jobs in this industry. Between 2008 and 2011, the productivity growth of this specific tourism industry is below the tourism industries as a whole, but in 2012 productivity grows and increases at a faster rate than the productivity of tourism. Between 2008 and 2013, the productivity of water passenger transport services had grown by over 86%, despite the initial decrease.

The productivity in air passenger transport services fluctuates. There is a decline in productivity in 2009, and then productivity grows until 2011, before there is a decline in 2012 and a final increase in 2013. Over the time period there is a slight increase in productivity growth of 14.6%, almost exactly the same as the overall productivity growth of tourism as a collection of industries. The fluctuations in productivity are caused by changes year on year in the number of tourism direct jobs and TDGVA.

Figure 4: Productivity of transport services, UK, 2008 to 2013 (base year 2008=100)

Source: UK Tourism Satellite Account, 2008-2013, Office for National Statistics

Notes:

- Current prices

Download this chart Figure 4: Productivity of transport services, UK, 2008 to 2013 (base year 2008=100)

Image .csv .xls4. Labour productivity measures

The following productivity measure is indexed to 2012=100, in line with published labour productivity metrics. Conclusions drawn, therefore, reflect the productivity growth (also referred to as output per job or hour worked) before and after 2012.

A productivity statistic requires an input and an output. The components of this productivity estimate are the following:

- input: “productivity jobs” or “productivity hours worked”

- output: the gross value added (GVA) attributable to the tourism characteristic industry (2 digit SIC)

This produces 2 measures: output per job and output per hour worked. As stated in Labour Productivity: Oct to Dec 2015 release, the output per hour worked is the preferred productivity measure. This is because the productivity hours component is more comprehensive compared with productivity jobs as it is able to reflect full- and part-time working, which jobs is not.

The estimates presented here are for industry divisions that cover the industries that provide goods and services to tourists, for example, accommodation services, food and drink serving activities, and passenger transport services. All estimates in this section are seasonally adjusted.

Please also note that throughout this section, Q1 refers to Quarter 1 January to March, Q2 Quarter 2 April to June, Q3 Quarter 3 July to September and Q4 Quarter 4 October to December.

Figure 5 shows the output per job of accommodation services for visitors and food and beverage serving activities.

The output per job in food and beverage serving activities is at the highest point in 2008 Q1, then it decreases (with some fluctuation) until 2010 Q1, which could be the effect of the economic downturn. Output per job then begins to increase (from 2010 Q1) with a sharp peak in 2010 Q3 and a steady upwards growth to peaks in 2012 Q2 and Q3, coinciding with the Olympics. Productivity largely declines through 2013. In 2015, the output per job in the sector continues to decline, due to increases in employment not matched by growth in GVA.

However, it is a different story for accommodation services for visitors. Between 2008 and 2012, there is a general increase in the output per job, with a sharp productivity peak in 2010 Q1 (caused by an increase in GVA and decrease in jobs). There is a decline in output per job in 2012 Q2 but then output per job increases, with a sharp peak in 2013 Q2 (caused by an increase in GVA) followed by a dip to 2014 Q1, then output per job continues to grow, with a sharp increase between Q2 and Q4 of 2015.

Figure 5: Output per job by tourism characteristic industry, UK, Quarter 1 (Jan to Mar) 2008 to Quarter 4 (Oct to Dec) 2015

Source: Office for National Statistics

Notes:

- Seasonally adjusted.

Download this chart Figure 5: Output per job by tourism characteristic industry, UK, Quarter 1 (Jan to Mar) 2008 to Quarter 4 (Oct to Dec) 2015

Image .csv .xlsFigure 6 shows the output per hour worked of accommodation services for visitors and food and beverage serving activities. The growth in both industries is broadly similar to the growth of output per job. The main difference occurs in food and beverage serving industries when at the end of 2015, output per hour worked increases but the general trend is downwards from 2012 overall.

Figure 6: Output per hour worked by tourism characteristic industry, UK, Quarter 1 (Jan to Mar) 2008 to Quarter 4 (Oct to Dec) 2015

Source: Office for National Statistics

Notes:

- Seasonally adjusted

Download this chart Figure 6: Output per hour worked by tourism characteristic industry, UK, Quarter 1 (Jan to Mar) 2008 to Quarter 4 (Oct to Dec) 2015

Image .csv .xlsFigure 7 shows the output per job of the following industries: creative, arts and entertainment activities; libraries, archives, museums and other cultural activities; gambling and betting activities; and sport activities and amusement and recreation activities.

The productivity of creative, arts and entertainment activities generally increases from 2008 to 2012, with peaks and troughs – the highest peak being in 2011 Q2 and the lowest trough in 2008 Q4 (where the effects of the economic downturn would be most prevalent). Since 2012, there has been a general decline in productivity growth, again with a few peaks and troughs. However, in 2015 there was an increase in productivity. Overall this suggests that over 2011 and 2012, productivity in this industry was at its highest. There are, however, signs of productivity growth in 2015, returning to 2010 levels.

Libraries, archives, museums and other cultural activities have a steady increase (with fluctuations) in productivity between 2008 and 2012, with the lowest productivity being in 2008 Q1. There was a slight dip in 2008 Q4 (downturn effects can be seen) but the industry then recovers and continues the upwards trend. In 2013, the growth of productivity sharply increases until 2013 Q3 when a decline in productivity growth appears, although the industry has a higher level of productivity (compared with 2012) until 2014 Q4. A decline is evident between 2013 Q3 until 2015 Q2, however, throughout the rest of 2015 the industry sees a further growth in productivity.

Productivity in gambling and betting activities declines until 2012, after which growth remains fairly flat until it begins to increase again in 2013. Productivity growth slows in 2015. This increase could be due to an increase in online sport betting since 2012.

The productivity growth of sports activities and amusement and recreation activities fluctuates between increases and decreases until a sharp peak in 2012 Q3, expected due to the London Olympics. In 2012 Q4, productivity decreased and has remained fairly steady at that level, until further decreasing in 2014 Q4.

Figure 7: Output per job by tourism characteristic activity, UK, Quarter 1 (Jan to Mar) 2008 to Quarter 4 (Oct to Dec) 2015

Source: Office for National Statistics

Notes:

- Seasonally adjusted.

Download this chart Figure 7: Output per job by tourism characteristic activity, UK, Quarter 1 (Jan to Mar) 2008 to Quarter 4 (Oct to Dec) 2015

Image .csv .xlsFigure 8 shows the output per hour worked of the following industries: creative, arts and entertainment activities; libraries, archives, museums and other cultural activities; gambling and betting activities; and sport activities and amusement and recreation activities. The trends are largely the same as with the output per job in these industries.

Figure 8: Output per hour worked by tourism characteristic activity, UK, Quarter 1 (Jan to Mar) 2008 to Quarter 4 (Oct to Dec) 2015

Source: Office for National Statistics

Notes:

- Seasonally adjusted

Download this chart Figure 8: Output per hour worked by tourism characteristic activity, UK, Quarter 1 (Jan to Mar) 2008 to Quarter 4 (Oct to Dec) 2015

Image .csv .xlsOutput per job and output per hour worked in transport services (road, rail, air, water and transport rental) are not examined in the content of this release. This is because a large proportion of their output is related non-tourism activity, for example, freight activities. Therefore, drawing conclusions based on the high-level aggregates would not be a sound conclusion on the productivity of the tourism-related travel industry (largely passenger services).

However, the Tourism Satellite Account provides an estimate of GVA for the transport industries, which is directly attributable to tourism. These estimates were used in the previous section to produce productivity estimates for the services that transport industries provide to passengers.

Back to table of contents5. A comparison of tourism productivity measures

This section aims to compare the 2 productivity methodologies and highlight the main differences.

The most noticeable difference is that the Tourism Satellite Account (TSA) productivity measure uses components that are directly attributable to tourism, whereas the labour productivity estimates are based on inputs and outputs of tourism industries.

Also, the labour productivity estimates are non-additive (cannot be summed together), so a whole tourism productivity figure is not straightforward to calculate, which is a disadvantage in terms of deriving a single measure of the productivity of tourism. The industry classes we have data for (SIC 2 digit) also include non-tourism activities and are therefore not wholly tourism related industries. This is not an issue for the TSA-based methodology.

Using the TSA productivity methodology, a whole tourism productivity figure can be calculated and compared with a non-tourism industries figure, calculated using the same methodology. This enables a comparison and puts the metrics into context.

In the TSA productivity measure, the tourism direct gross value added (GVA) (output) component is in current prices. This means that it is not adjusted for inflation which would affect the tourism direct GVA (TDGVA) and thus impact the growth of productivity in tourism industries.

An advantage to using labour productivity estimates is the timeliness, in comparison with the TSA productivity measures. The TSA relies on data in the Blue Book, which is unavailable until 18 months after the reference year. This incurs a time delay in the production of the account and thus productivity measure. However, the labour productivity estimates can be produced 2 months after the latest quarter.

Back to table of contents6. Methodology of tourism satellite account productivity

As previously mentioned, the Tourism Satellite Account (TSA) consists of 7 tables. The tables contain metrics for 11 industries that are considered tourism characteristic industries (definition from the UN World Tourism Organisation); more detail of these industries can be found in Annex A. For further detail, the methodology behind the TSA can be found in the Tourism Satellite Account: Recommended Methodological Framework, 2008 . In terms of productivity estimates, the tables required are Tables 5, 6 and 7.

TSA Table 5 uses Input-Output Supply and Use Tables (from the National Accounts framework) to provide estimates of the total gross value added (GVA) for each tourism-related industry. TSA Table 6 provides tourism ratios: the proportion of a tourism-related industry’s output that is directly accounted for by the expenditure of tourists. The TSA Table 7 uses Workforce Jobs data to provide estimates of the total number of jobs in the 11 tourism characteristic industries and non-tourism industries.

The estimates provided in these tables can be used as statistics for each tourism characteristic industry separately and they can be summed to provide an estimate for tourism-related industries as a whole.

However, the GVA for each tourism industry (GVATI) does not differentiate between spend by residents or tourists. For example, residents use food and beverage serving activities (restaurants, pubs etc) as well as tourists. Applying the tourism ratio (from TSA Table 6) to the GVATI for each industry enables the calculation of TDGVA (tourism direct GVA, as mentioned previously).

Again, the Workforce Jobs estimates in Table 7 are calculated for each tourism characteristic industry. Applying the tourism ratio (from TSA Table 6) to these estimates gives the number of jobs in these industries that are directly attributable to tourism (tourism direct employment, as mentioned previously).

Note that the total employment in other (non-tourism) industries figures, found in TSA Table 7, for 2008, 2009, 2010, 2011 and 2012 have been revised to align with a new, more comprehensive methodology used to produce these estimates in 2013. This balances the totals to our preferred measure of jobs – the Workforce Jobs series rather than totals for individual components such as employees and self-employed from other ONS surveys. They were revised for the purpose of this article, to produce a consistent productivity measure. The total employment figures will therefore not match the figures in previous Tourism Satellite Accounts.

As stated before, please note that each TSA is produced with regards to a reference year so it should be noted that all GVA figures used are in current prices and therefore are not adjusted for inflation.

When calculating the productivity statistic using the TSA tables, there are 2 options for inputs and 2 options for outputs. These are displayed in Table 1.

Table 1: Components that could be used in a productivity measure

| Input | Output | |

| Measure 1 | Tourism direct (TD) jobs | Tourism direct GVA |

| Measure 2 | Tourism industries (TI) jobs | Tourism industries GVA |

| Source: Office for National Statistics | ||

Download this table Table 1: Components that could be used in a productivity measure

.xls (25.6 kB)The preferred measure is using tourism direct GVA and tourism direct employment, as this is based on GVA and jobs directly attributable to tourism, rather than to the industries it is compiled of.

Figure 9 shows the productivity over time of tourism industries’ jobs and GVA and tourism direct jobs and TDGVA. It can be seen that the measures broadly follow the same pattern. The estimates using the tourism industries (TI) measure has a sharper increase between 2008 and 2009 and the estimates using tourism direct (TD) figures show a decrease between 2012 and 2013. The dip in productivity using TD figures in 2013 is explained by a steady increase of tourism employment (4.7%) but the increase in TDGVA (2.9%) between 2012 and 2013 does not match this increase, causing a decline in productivity growth. Overall, these are only slight differences.

Figure 9: Comparison of productivity measures: tourism industry versus tourism direct values (base year 2008=100), UK, 2008 to 2013

Source: UK Tourism Satellite Account, 2008-2013, Office for National Statistics

Download this chart Figure 9: Comparison of productivity measures: tourism industry versus tourism direct values (base year 2008=100), UK, 2008 to 2013

Image .csv .xlsAs seen in Figure 9 both measures follow broadly the same pattern. Therefore the measure used as the Tourism Satellite Account productivity measure is made up of the following components:

- input: the number of jobs directly attributable to tourism

- output: the GVA directly attributable to tourism

7. Methodology of labour productivity

The basic definition of labour productivity can be summarised as follows:

Productivity = Output / Input

Or expressed in formula:

{kind=link}

Inputs can be of capital, raw materials and labour or a combination of the three. The latter, in its most basic form, is easier to measure; this means that many headline productivity statistics use it alone, giving figures for labour productivity. A more complete picture of labour input can be provided by adjustments to the data to take account of the fact that quality of labour inputs might be very varied, from surgeons to manual workers for example.

This section lists the regular productivity releases by the Office for National Statistics (ONS), focusing mainly on the Labour Productivity: Quarterly Statistical Bulletin. In particular this release highlights the broad industry groups for which data are available, which include tourism characteristic activities (as defined by the UN World Tourism Organisation). The section provides a background to the development of measures of productivity for more tightly defined tourism activities.

Our regular releases include straightforward labour productivity statistics and more complex data that include adjustments and capital input. Our regular releases are listed below.

- Labour Productivity: Quarterly Statistical Bulletin Statistics: measures the amount of economic output that is produced by a unit of labour input

- Multi-factor Productivity (MFP) – Indicative Estimates: growth in output decomposed into the relative contributions of capital and labour inputs

- Estimates of Quality-Adjusted Labour Input: labour data that feeds into the MFP estimates

- Volume of Capital Services: capital data that feeds into the MFP estimates

- Public Sector Productivity releases: a range of measures and articles that use different methodology to the labour productivity release

- International Comparisons of Productivity: compares levels and growth rates for the G7 countries

- Regional Labour Productivity Annual data: included within each quarterly bulletin

- Sub-regional Labour Productivity Experimental estimates: part of the series of ONS articles entitled Regional Economic Analysis

Quarterly labour productivity statistical bulletin: content of the release

Labour productivity measures the amount of economic output that is produced by a unit of labour input. In our quarterly bulletin the output is gross value added (in current prices, chained volume measure (CVM)) and the labour input is measured in terms of the number of jobs, workers or hours worked.

The release includes measures of productivity, referred to as output per job, hour worked and worker for the economy as a whole. However, where an industry breakdown is required, the last of these is not available. The bulletin includes output per job and output per hour worked for individual service sections and manufacturing sub-sections of the economy.

When considering tourism, the following sections are most relevant:

H = Transport & Storage

I = Accommodation & Food Services

R = Arts, entertainment and recreation.

Two further sections contain small proportions of tourism activities:

L = Real Estate Activities (only those relating to holiday and second homes)

N = Admin & Support Services (only travel agencies, related services and specific rental activities).

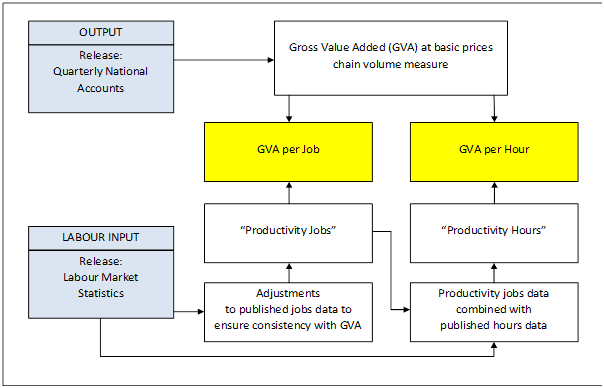

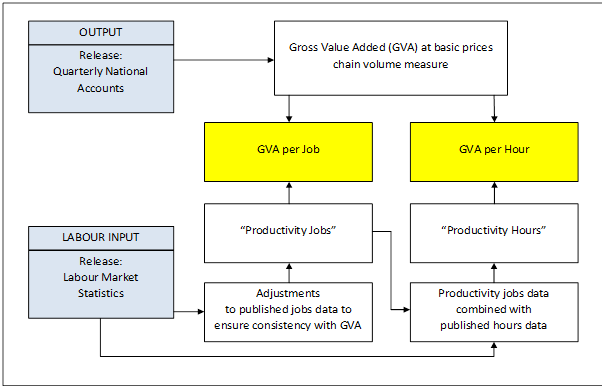

The data are presented as indices referenced to a specific year for which the value is set as 100 (the latest estimates use 2012). Figure 10 is a summary of the process of converting the economic output and labour input into productivity measures.

Figure 10: Flow diagram showing calculation of gross value added per hour and gross value added per job

Source: Office for National Statistics

Download this image Figure 10: Flow diagram showing calculation of gross value added per hour and gross value added per job

.png (14.3 kB){kind=link}

In this analysis of tourism productivity, the components used in the formulation of productivity estimates, namely “productivity jobs”, “productivity hours”, and “GVA at basic prices (CVM)” (from Figure 10) have been produced at a more detailed industrial classification to more closely match the tourism characteristic industries that make up the tourism sector, as shown in Table 2.

Table 2: Industries used in tourism labour productivity

| SIC code | Description |

| 55 | Accommodation services for visitors |

| 56 | Food and beverage serving activities |

| 90 | Creative, arts and entertainment activities |

| 91 | Libraries, archives, museums, and other cultural activities |

| 92 | Gambling and betting activities |

| 93 | Sports activities and amusement and recreation activities |

| Source: Office for National Statistics | |

Download this table Table 2: Industries used in tourism labour productivity

.xls (17.4 kB)This more detailed industry breakdown allows for a thorough analysis of the productivity of these tourism-related industries. Even at this level, however, some non-tourism activity is included in this industry breakdown. For instance, the transport industries (rail, road, air and water) will also include freight activities as well as passenger services. This is normally removed from estimates of tourism output and employment produced by ONS, for example in the Tourism Satellite Account.

Annex A: The tourism industries (Standard Industrial Classification, 2007)

| Tourism Industries | SIC2007 code | Description |

| Accommodation for visitors | 55100 | Hotels and similar accommodation |

| 55202 | Youth hostels | |

| 55300 | Recreational vehicle parks, trailer parks & camping grounds | |

| 55201 | Holiday centres and villages | |

| 55209 | Other holiday and other collective accommodation | |

| 55900 | Other accommodation | |

| Food and beverage serving activities | 56101 | Licensed restaurants |

| 56102 | Unlicensed restaurants and cafes | |

| 56103 | Take-away food shops and mobile food stands | |

| 56290 | Other food services | |

| 56210 | Event Catering Activities | |

| 56301 | Licensed clubs | |

| 56302 | Public houses and bars | |

| Railway passenger transport | 49100 | Passenger rail transport, interurban |

| Road passenger transport | 49320 | Taxi Operation |

| 49390 | Other passenger land transport | |

| Water passenger transport | 50100 | Sea and coastal passenger water transport |

| 50300 | Inland passenger water transport | |

| Air passenger transport | 51101 | Scheduled passenger air transport |

| 51102 | Non-scheduled passenger air transport | |

| Transport equipment rental | 77110 | Renting & leasing of cars and light motor vehicles |

| 77341 | Renting & leasing of passenger water transport equipment | |

| 77351 | Renting & leasing of passenger air transport equipment | |

| Travel agencies & other reservation services activities | 79110 | Travel agency activities |

| 79120 | Tour operator activities | |

| 79901 | Activities of tour guides | |

| 79909 | Other reservation service activities n.e.c. | |

| Cultural activities | 90010 | Performing arts |

| 90020 | Support Activities for the performing arts | |

| 90030 | Artistic creation | |

| 90040 | Operation of arts facilities | |

| 91020 | Museums activities | |

| 91030 | Operation of historical sites & buildings & similar attractions | |

| 91040 | Botanical & zoological gardens and nature reserves activities | |

| Sporting & recreational activities | 92000 | Gambling & betting activities |

| 93110 | Operation of sports facilities | |

| 93199 | Other sports activities | |

| 93210 | Activities of amusement parks and theme parks | |

| 93290 | Other amusement and recreation activities nec | |

| 77210 | Renting and leasing of recreational and sports goods | |

| Country-specific tourism characteristic activities | 82301 | Activities of exhibition and fair organisers |

| 82302 | Activities of conference organisers | |

| 68202 | Letting and operating of conference and exhibition centres | |

| Source: Office for National Statistics | ||