Table of contents

- Main points

- Things you need to know about this release

- Summary of net lending or borrowing positions by sector

- Real household disposable income

- Households saving ratio

- Non-financial corporations

- Summary of other sector accounts

- Summary of revisions to net lending or borrowing positions

- Links to related statistics

- Links to related analysis

- Changes to this bulletin

- Quality and methodology

- Appendix A: key economic indicators

- Appendix B: additional information on the alternative measures of households’ income and savings

- Acknowledgements

1. Main points

In Quarter 3 (July to Sept) 2018, real household disposable income showed no growth, as inflation and increased payments of self-employment tax offset strong wage growth.

In Quarter 3 (July to Sept) 2018, the households saving ratio fell to its joint third lowest on record to 3.8%, down from 4.1% in the previous quarter; while the 2017 saving ratio has been revised from 4.1% to 3.9%

UK sectors were net borrowers of 5.1% of GDP in Quarter 3 2018; this is higher than the previous quarter (3.9%) and the highest since Quarter 3 2016 (6.5%).

Driving UK net borrowing in the latest quarter were non-financial corporations, who were net borrowers of 2.2% of GDP, as a result of foreign investors in the UK receiving a greater return on their investments as UK profitability trends up in 2018.

Non-financial corporations have seen their financial debt levels remain at near records high in the last few quarters, though they do compare favourably against other advanced economies as a proportion of GDP.

Households were net borrowers at 1.6% of GDP in Quarter 3 2018; their highest net borrowing position since Quarter 1 (Jan to Mar) 2017 and an unprecedented eighth consecutive quarter of net borrowing.

The rest of the world sector continues to be a net lender to the UK at 5.1% of GDP; this is an increase from the previous quarter’s 3.9%, as the UK’s current account deficit widened to in Quarter 3 (July to Sept) 2018.

2. Things you need to know about this release

This bulletin includes new data for the latest available quarter, Quarter 3 (July to Sept) 2018, and revisions to data from Quarter 1 (Jan to Mar) 2017 to Quarter 2 (Apr to June) 2018.

This bulletin follows the National Accounts Revisions Policy.

The alternative measures of households income and saving

From this release onwards we will be incorporating the alternative measures of real households disposable income and saving.

This follows growing user interest in the Alternative measures of households income and saving experimental statistics since their launch in August 2015.

In effect, the underlying data will be moved into the Households chapter (Chapter 6) of the UK Economic Accounts and the accompanying analysis will move to this bulletin. They are both released on the same day. Previously, the alternative measures of real household disposable income and households’ saving ratio were released roughly a week later.

We hope users find this more timely analysis of households’ financial situation useful and helpful, and we continue to welcome feedback.

Understanding the sector and financial accounts

This bulletin presents UK aggregate data for the main economic indicators and summary estimates from the institutional sectors of the UK economy: private non-financial corporations, public corporations, financial corporations, central and local government, households, non-profit institutions serving households (NPISH) and the rest of the world sector, that are presented in the UK Economic Accounts (UKEA) dataset.

This bulletin uses data from the UKEA and it provides detailed estimates of national product, income and expenditure, UK sector, non-financial and financial accounts, and UK Balance of Payments. These accounts are the underlying data that produce a single estimate of gross domestic product (GDP) using income, production and expenditure data.

Further information on the calculation of some of our main economic indicators can be found in the Quality and Methodology section of this bulletin.

Estimates within this release

All data within this bulletin are estimated in current prices (also called nominal prices), except for real household disposable income, which is estimated in chained volume terms.

Current price series are expressed in terms of the prices during the time period being estimated. These describe the prices recorded at the time of production or consumption and include the effect of price inflation over time. Chained volume series (also known as real terms) have had the effects of inflation removed.

All figures given in this bulletin are adjusted for seasonality, unless otherwise stated. Seasonal adjustment removes seasonal or calendar effects from data to enable more meaningful comparisons over time.

The Population estimates for the UK, England and Wales, Scotland and Northern Ireland used in this release are those published on 28 June 2018.

Back to table of contents3. Summary of net lending or borrowing positions by sector

UK sectors were net borrowers of 5.1% of GDP in Quarter 3 (July to Sept) 2018; this is higher than the previous quarter (3.9%) and the highest since Quarter 3 2016 (6.5%).

In Quarter 3 2018, UK sectors were net borrowers of 5.1% of gross domestic product (GDP), meaning that they spent and invested more than they received in incomes. This was the UK’s highest net borrowing position since Quarter 3 2016 when they were net borrowers of 6.5% of GDP.

The largest net borrowing sector in Quarter 3 2018 were non-financial corporations at 2.2% of GDP, an increase from 1.1% in the previous quarter, as Figure 1 shows. Non-financial corporations have now been net borrowers for all but one of the last 26 quarters since Quarter 2 (Apr to June) 2012, with the latest quarter being their highest net borrowing position as a proportion of GDP since Quarter 3 2016.

Households were the second largest net borrowing sector in Quarter 3 2018 at 1.6% of GDP, up from 1.2% in the previous quarter. This was their highest net borrowing position since Quarter 1 (Jan to Mar) 2017 when they were net borrowers of 1.8% of GDP. In the latest quarter, a rise in expenditure (£3.6 billion) and a rise in the payments of self-employment tax (£1.4 billion), partly offset by a £2.9 billion increase in wages and salaries, caused the increase in households net borrowing position. Quarter 3 2018 was an unprecedented eighth consecutive quarter of net borrowing by households who have historically been net lenders (see Figure 17).

General government’s net borrowing position has improved significantly since its 2009 peak and remains low in the latest quarter at 1.2% of GDP. This was their lowest Quarter 3 net borrowing position as a percentage of GDP since Quarter 3 2001. Their net borrowing position in the latest quarter was a slight increase, however, compared with the previous quarter where it was 1.0% of GDP.

Figure 1: Net lending (positive) or borrowing (negative) positions of UK sectors and the rest of the world in the non-financial account,

as a percentage of UK gross domestic product, seasonally adjusted , Quarter 1 (Jan to Mar) 1987 to Quarter 3 (July to Sept) 2018

Source: Office for National Statistics

Notes:

- Sum of contributions to real household disposable income may not add to growth rate due to rounding.

Download this chart Figure 1: Net lending (positive) or borrowing (negative) positions of UK sectors and the rest of the world in the non-financial account,

Image .csv .xlsFinancial corporations were net borrowers of 1.1% of GDP in Quarter 3 2018, compared with 1.3% in the previous quarter. Financial corporations are traditionally net borrowers, and their current net borrowing position of 1.1% of GDP is their quarterly average net borrowing position over the last four years.

Non-profit institutions serving households (NPISH) were the only net lending sector in the UK in Quarter 3 2018 at 0.3% of GDP. This is their highest net lending position since Quarter 3 2015 when they were also net lenders at 0.3% of GDP. The NPISH sector, which includes trade unions, charities and religious organisations, more often than not live within their means – meaning that they usually have surplus income after expenditure and investment.

For analysis on the main drivers behind these movements in UK sectors, please see later sections of this bulletin. Deeper analysis on the government and rest of the world sectors are available in Public sector finances, UK: August 2018 and the Balance of payments bulletin, respectively.

Back to table of contents4. Real household disposable income

Real household disposable income (RHDI) in Quarter 3 (July to Sept) 2018 was flat compared with the previous quarter, as growth in nominal gross disposable income was completely offset by price rises (see Figure 2). This slow down followed a relatively strong Quarter 2 (Apr to June) 2018 when it grew 0.9%; the fastest quarter on previous quarter growth since Quarter 2 2017.

Figure 2: Contributions to real household disposable income growth, quarter on previous quarter, percentage points, seasonally adjusted

UK, Quarter 1 (Jan to Mar) 2015 to Quarter 3 (July to Sept) 2018

Source: Office for National Statistics

Notes:

- Sum of contributions to real household disposable income may not add to growth rate due to rounding.

Download this chart Figure 2: Contributions to real household disposable income growth, quarter on previous quarter, percentage points, seasonally adjusted

Image .csv .xlsNominal gross disposable household income (GDHI) increased by £2.0 billion and was mainly driven by strong growth in wages and salaries of £2.9 billion. This partly reflects strong growth in nominal average weekly earnings (including bonuses); the last time it grew at a faster rate than in Quarter 3 2018 was almost four years ago, as Figure 3 shows (see UK labour market: December 2018).

Figure 3: Average weekly earnings (nominal), total pay, Great Britain, £, seasonally adjusted

Quarter 4 (Oct to Dec) 2014 to Quarter 3 (July to Sept) 2018, UK

Source: Office for National Statistics

Download this chart Figure 3: Average weekly earnings (nominal), total pay, Great Britain, £, seasonally adjusted

Image .csv .xlsHowever, offsetting the growth in wages and salaries in the latest quarter was an unusually large increase in taxes on income paid by households (£2.3 billion) as a result of higher returns from self-employment tax. Taxes on income paid by households have only ever increased by more than £2 billion quarter on previous quarter in five of the last 87 quarters, since Quarter 1 (Jan to Mar) 1997, highlighting the unusually high increase.

Revisions to real household disposable income

This bulletin includes revisions to data from Quarter 1 2017 in line with the National Accounts Revisions Policy.

In the six quarters open to revision, RHDI was revised up by an average of £2.6 billion per quarter or, in terms of quarter on previous quarter growth rates, it was revised up by an average of 0.2 percentage points per quarter.

As Figure 4 shows, revisions stem from other social insurance benefits received by households; revised up by an average of £2.4 billion a quarter. These revisions are due to updated financial inquiry survey data replacing forecasts and the fixing of an operational issue highlighted in our previous publication.

Figure 4: Impact of revisions to real household disposable income, £ billions, seasonally adjusted

UK, Quarter 1 (Jan to Mar) 2017 to Quarter 2 (April to June) 2018

Source: Office for National Statistics

Notes:

- Sum of contributions to real household disposable income may not add to RHDI due to rounding.

Download this chart Figure 4: Impact of revisions to real household disposable income, £ billions, seasonally adjusted

Image .csv .xlsAs a result of these revisions, latest estimates now state that real household disposable income grew by 0.5% in 2017. Previous estimates suggested a fall in RHDI of 0.1% in 2017.

Nevertheless, despite revisions, latest estimates still suggest that growth in households purchasing power have more or less stalled since 2016, while the wider economy experienced moderate growth of 1.8%, in real terms, as seen in Figure 5.

Figure 5: Comparison between real household disposable income and gross domestic product growth, annual, percentage (%), seasonally adjusted

UK, 2008 to 2017

Source: Office for National Statistics

Download this chart Figure 5: Comparison between real household disposable income and gross domestic product growth, annual, percentage (%), seasonally adjusted

Image .csv .xlsAlternative measure of real household disposable income (experimental)

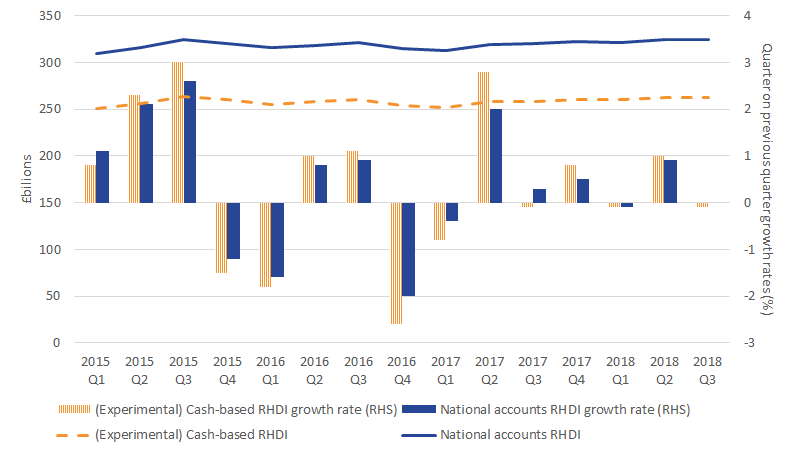

From this release onwards, analysis on the alternative measure of RHDI will be included in this release. This alternative (and experimental) measure removes imputed transactions from real household disposable income to better represent the economic experience of UK households. In other words, it captures the immediately accessible and directly observed “cash” available to households to spend or save at that given time point if they so wished to. Deeper detail on methodology can be found in the Alternative measures of UK households' income and saving: April to June 2018 article.

In this cash-based approach, real household disposable income (RHDI) is estimated to have fallen 0.2% in Quarter 3 (July to Sept) 2018, compared with the previous quarter. This is only marginally different to the flat growth in RHDI on a National Accounts basis.

Therefore, both the national accounts RHDI and the cash-basis RDHI were broadly flat in Quarter 3 2018, as seen in Figure 6. The main point, however, from the alternative measure of RHDI is that the level of RHDI on a cash-basis is approximately 20% lower than the level of RHDI on a national accounts basis. There’s a difference of £62.1 billion between the two measures, equivalent to 12% of gross domestic product (GDP), meaning that households have 12% of GDP less to spend or save when we remove incomes not immediately accessible or directly observed.

Per head, cash-based RHDI stood at £3,943 in the latest quarter. This is £933 lower than RHDI per head on a national accounts basis (£4,876).

Figure 6: Real households disposable income on a cash-basis and on a National Accounts basis, £ billions and growth rates, seasonally adjusted

Quarter 1 (Jan to Mar) 2015 to Quarter 3 (July to Sept) 2018

Source: Office for National Statistics

Notes:

- RHS = Right-hand side axis.

Download this image Figure 6: Real households disposable income on a cash-basis and on a National Accounts basis, £ billions and growth rates, seasonally adjusted

.png (19.8 kB) .xls (48.1 kB){kind=link}

The difference between the two series is mainly explained by the removal of gross operating surplus (which is made up of imputed rentals – that is, what households would pay themselves if they were to rent their own property to themselves) from the national accounts measure of GDHI. This has been the main driver of the difference throughout 2018 so far, as Figure 7 shows.

Figure 7: Contributions to the difference in growth between gross disposable household income on a cash basis and a national accounts basis, £ million, seasonally adjusted

Quarter 1 (Jan to Mar) 2017 to Quarter 3 (July to Sept) 2018

Source: Office for National Statistics

Download this chart Figure 7: Contributions to the difference in growth between gross disposable household income on a cash basis and a national accounts basis, £ million, seasonally adjusted

Image .csv .xlsThere are six transactions which explain the differences between GHDI on a cash-basis and a national accounts basis. Please see Table 2 in the appendix for a list of transactions removed from the national accounts measure of RHDI to calculate the cash-based RHDI. A cash-based deflator is also applied to cash-based GHDI to remove the effect of price changes experienced by households to calculate real household disposable income on a cash-basis.

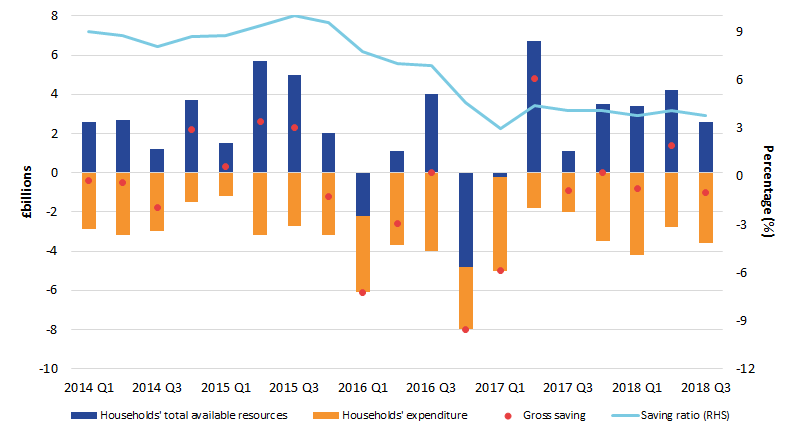

Back to table of contents5. Households saving ratio

As Figure 8 shows, the households’ saving ratio fell to 3.8% in the latest quarter and is the joint third-lowest since records began in 1963. Quarter 3 (July to Sept) 2018 is now the eighth consecutive quarter in which households have exhibited a historically low saving ratio.

Figure 8: UK households saving ratio, quarterly, percentage, seasonally adjusted

Quarter 1 (Jan to Mar) 1963 to Quarter 3 (July to Sept) 2018

Source: Office for National Statistics

Download this chart Figure 8: UK households saving ratio, quarterly, percentage, seasonally adjusted

Image .csv .xlsFigure 9 shows that the marginal fall in the saving ratio in Quarter 3 (July to Sept) 2018 was due to households’ expenditure increasing by £3.6 billion while the increase of households’ total available resources slowed to £2.6bn.

In Quarter 3 2018, households’ expenditure increased by £3.6 billion (or 1.1%) compared with the previous quarter and was mainly due to an increase of £1.1 billion in the service charge attributed to financial intermediation services (that is, the service for taking out a loan or having a deposit held). Housing costs also contributed to households’ expenditure, as it increased by £0.9 billion mainly due to actual rentals paid by tenants. Further detail on households’ final consumption expenditure, including a breakdown of households’ spending by product, can be found in the Consumer trends bulletin.

Households total available resources is made up of gross disposable household income (GDHI) and the adjustment for the change in households’ pension entitlements (in other words, the change in deferred savings). The latter increased by £0.6 billion in the latest quarter while GDHI made a larger contribution of £2.0bn.

Driving the increase in GDHI in Quarter 3 2018 was relatively strong growth in wages and salaries of £2.9 billion following a weak Quarter 2 (Apr to June) 2018. The slowdown in total available resources, however, stemmed from higher than usual taxes on income paid out by households as a result of higher payments in self-employment tax. See Section 4 for greater analysis on the drivers to GDHI.

Figure 9: Contributions to the households saving ratio, quarter on previous quarter, seasonally adjusted, £ billions

Quarter 1 (Jan to Mar) 2014 to Quarter 3 (July to Sept) 2018, UK

Source: Office for National Statistics

Notes:

- Saving ratio calculated as gross saving divided by total available resources.

- Gross saving calculated as total available resources minus households' final consumption expenditure.

- Total available resources calculated as gross disposable income plus adjustment to pension entitlements.

- Saving ratio (%) refers to the axis on the right-hand side (RHS). All others refer to the left-hand side axis.

Download this image Figure 9: Contributions to the households saving ratio, quarter on previous quarter, seasonally adjusted, £ billions

.png (23.5 kB) .xls (48.1 kB){kind=link}

Revisions to the saving ratio

This bulletin includes revisions to data from Quarter 1 (Jan to Mar) 2017 in line with the National Accounts Revisions Policy.

The saving ratio has been revised downward by an average of 0.1 percentage points per quarter in the six quarters open for revision, with the largest revisions occurring in Quarter 2 (Apr to June) 2017 and Quarter 3 (July to Sept) 2017, both of 0.4 percentage points.

As shown in Figure 10, most of the revisions in 2017 were due to upward revisions in households’ final consumption expenditure (£3.0 billion), in particular, expenditure on life insurance (plus £1.1 billion), medical services (plus £0.8 billion), pharmaceutical products (plus £0.5 billion).

As a result, the saving ratio in 2017 has been revised down from an already record low of 4.2% to 3.9%.

The revisions to the saving ratio in the first two quarters 2018 are mainly due to upward revisions of dividend income from corporations of £0.9 billion and £1.7 billion, respectively.

Figure 10: Impact of revisions to the UK households gross saving, quarterly, seasonally adjusted, £ billions

Quarter 1 (Jan to Mar) 2017 to Quarter 2 (Apr to June) 2018

Source: Office for National Statistics

Notes:

- Total available resources is calculated as gross disposable income plus the accumulation of pension entitlements.

- Sum of contributions to real household disposable income may not add to growth rate due to rounding.

Download this chart Figure 10: Impact of revisions to the UK households gross saving, quarterly, seasonally adjusted, £ billions

Image .csv .xlsAlternative measure of households’ saving ratio (experimental)

From this release onwards, analysis on the alternative measure of households saving ratio will also be included in this release. This alternative (and experimental) measure removes imputed transactions from the households saving ratio to better represent the economic experience of UK households. In other words, it captures the immediately accessible and directly observed “cash” available to households to spend or save at that given time point if they so wished to. Deeper detail on methodology can be found in the Alternative measures of UK households' income and saving: April to June 2018 article.

As Figure 11 shows, the cash-basis saving ratio was negative 0.2% in Quarter 3 2018, down 0.7 percentage points from positive 0.5% in the previous quarter. The national accounts saving ratio, on the other hand, fell only 0.3 percentage points to 3.8% compared with the previous quarter.

A negative saving ratio on a cash-basis is not unprecedented as it was often negative between 2003 and 2007. The cash-based saving ratio has therefore returned to levels last seen before the financial crisis. In contrast, though the national accounts saving ratio has also seen a recent decline, it is currently much lower than it was before the financial crisis. The next paragraph outlines the cause in the difference between these two measures of households saving ratio.

Figure 11: UK households cash-basis saving ratio and national accounts saving ratio, quarterly, seasonally adjusted, percent

Quarter 1 (Jan to Mar) 1997 to Quarter 3 (July to Sept) 2018

Source: Office for National Statistics

Download this chart Figure 11: UK households cash-basis saving ratio and national accounts saving ratio, quarterly, seasonally adjusted, percent

Image .csv .xlsIn the latest quarter, driving the difference in the change between the national accounts savings ratio and the cash-basis saving ratio is gross operating surplus (which is made up of imputed rentals) in gross disposable household income; and this has been the main driver of the difference throughout 2018 so far, as Figure 12 shows.

Figure 12: Contributions to the difference in growth between households’ gross savings on a cash basis and a national accounts basis, £ million, seasonally adjusted

Quarter 1 (Jan to Mar) 2017 to Quarter 3 (July to Sept) 2018

Source: Office for National Statistics

Download this chart Figure 12: Contributions to the difference in growth between households’ gross savings on a cash basis and a national accounts basis, £ million, seasonally adjusted

Image .csv .xls6. Non-financial corporations

Nominal debt levels of non-financial corporations have recently risen to record highs, but as a proportion of GDP, they compare favourably against other advanced economies.

The level of debt (that is, total debt securities and loans) held by UK non-financial corporations in 2017 has increased by 8.2% compared with 2008 levels. Most of this increase began in Quarter 2 (Apr to June) 2016, as a result of an increase of the accumulation of both debt securities and long-term loans.

In 2016, non-financial corporations’ saw their debt levels increase by £144 billion to £1,651 billion (83.8% of gross domestic product (GDP)); the largest increase in debt since 2008.

Debt levels have remained at record highs at around £1,750 billion in the first three quarters of 2018. This follows a period of relatively flat levels of debt at around £1,530 billion from 2009, as shown in Figure 13.

Figure 13: UK Non-financial corporations’ stock of debt, non-seasonally adjusted, £ billions

Quarter 1 (Jan to Mar) 2008 to Quarter 3 (July to Sept) 2018

Source: Office for National Statistics

Notes:

- Non-financial corporations' debt calculated as the sum of total debt securities (AF.3) and loans (AF.4).

Download this chart Figure 13: UK Non-financial corporations’ stock of debt, non-seasonally adjusted, £ billions

Image .csv .xlsHowever, as a percentage of GDP, non-financial corporations have seen their debt fall significantly compared with their debt levels in 2008. In 2017, their debt to GDP ratio was 86%; 17 percentage points lower than that in 2008. This means that over the last ten years, non-financial corporations accumulated debt (that is, debt securities and loans) at a slower rate than the rate of economic growth over that time.

In comparison with other advanced economies and euro area countries, the UK has seen the largest fall in non-financial corporations’ debt levels relative to GDP while the average across G7 countries has seen a rise in non-financial corporations’ levels of debt to GDP (see Figure 14).

Figure 14: International comparison of non-financial corporations stock of debt as % of GDP, indexed to Quarter 1 2018 = 100

Quarter 1 (Jan to Mar) 2008 to Quarter 3 (July to Sept) 2018

Source: Office for national Statistics, Eurostat, Statistics Canada, Bureau of Economic Analysis, Federal Reserve

Notes:

- Debt calculated as stock of loans and debt securities.

- All calculations are author’s own.

Download this chart Figure 14: International comparison of non-financial corporations stock of debt as % of GDP, indexed to Quarter 1 2018 = 100

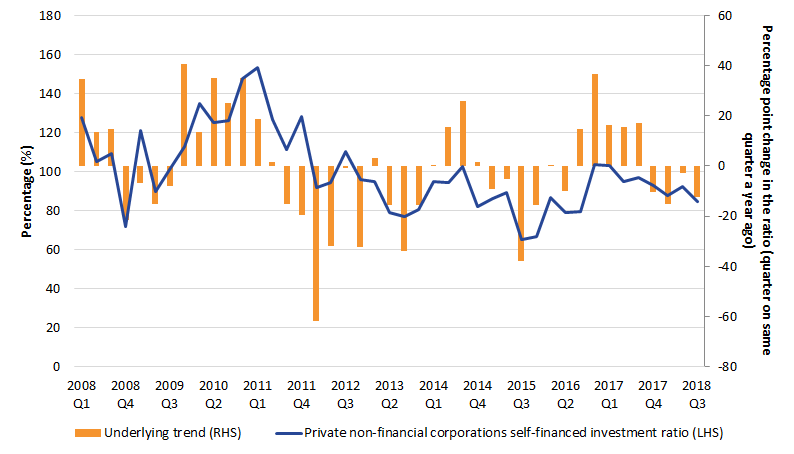

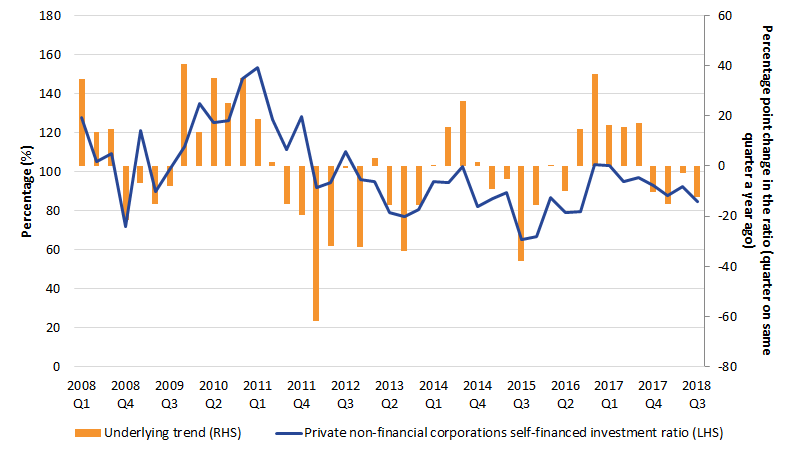

Image .csv .xlsFollowing user feedback, we have added to our dataset private non-financial corporations (PNFCs) self-financed investment ratio (on Table KEI). It captures the ability of PNFCs to finance their investment using their own income. A ratio of 1:1 (or 100% in percentage terms) means PNFCs could completely use up their gross savings to fund their investment. Anything above 100% implies gross savings were above their investment requirement, while anything below 100% implies a need to borrow or draw down on financial assets to cover investment.

Since Quarter 4 (Oct to Dec) 2016, PNFCs have seen a trend towards a need to borrow to invest. This is consistent with the recent increase in their stock of debt, as described earlier. See Figure 16 in Appendix A for a look at the ratio since Quarter 1 (Jan to Mar) 2008.

Back to table of contents7. Summary of other sector accounts

Financial corporations

In Quarter 3 (July to Sept) 2018, financial corporations remained net borrowers in the non-financial account for a second consecutive quarter. The sector is now at 1.1% of gross domestic product (GDP) compared with 1.3% in the previous quarter.

This slight narrowing of their net borrowing position (of £1.3 billion in current price terms) is mainly due to an increase in net reinvested earnings on foreign direct investment of £0.8 billion.

In the financial account, financial corporations (which consist of banks, insurance and pension companies, and other financial intermediaries) became net borrowers of £20.8 billion in the latest quarter, following a net lending position of £11.1 billion in the previous quarter. This was mainly due to a fall in net deposit transactions partly offset by a rise in net loans.

General government

General government sector is made up of central and local government.

In Quarter 3 2018, central government increased their net borrowing in the non-financial account to £7.6 billion, compared with £2.5 billion in the previous quarter. This movement was mainly driven by a £3.9 billion increase in current transfers within general government. The underlying series causing this change is grants between central government to local government. Historically, these are paid in Quarter 2 (Apr to June) of each year, but this year, the payments have been made in Quarter 3.

Further details on this sector can be found in Public sector finances, UK: October 2018. Note that although public sector finances and national accounts are compiled in accordance with the European System of Accounts: ESA 2010 and the Government Finance Statistics manual 2014, some differences remain.

Non-profit institutions serving households (NPISH)

Non-profit institutions serving households (NPISH) was the only net lending sector in the UK in Quarter 3 2018 at 0.3% of GDP (or £1.3 billion) in the non-financial account. Driving this net lending position was an increase of £0.6 billion in investment grants received and £0.2 billion in miscellaneous current transfers. This is its highest net lending positions since Quarter 3 2015 when it was also net lenders at 0.3% of GDP.

Rest of the world

The rest of the world is a net lender to UK sectors, and its net lending position increased by £6.7 billion in Quarter 3 2018 to £27.2 billion in the non-financial account.

This was mainly driven by a £4.4 billion increase in reinvested earnings on foreign direct investment received from UK private non-financial corporations. This is due to an upward trend in UK business profitability.

In the financial account, the rest of the world sector increased its net lending position by £23.7 billion to £34.1 billion. This movement was driven by a £38.0 billion improvement in their net equity position.

Further details of the UK Balance of Payments position can be found in the Balance of payments bulletin.

Back to table of contents8. Summary of revisions to net lending or borrowing positions

A summary of revisions in the quarters open to revisions (Quarter 1 (Jan to Mar) 2017 to Quarter 2 (Apr to June) 2018) can be seen in Table 1.

In both the non-financial and financial accounts, the largest of the revisions are between non-financial corporations and rest of the world. These are due to revisions to foreign direct investment following results from the annual Foreign Direct Investment (FDI) survey.

Revisions to general government are mainly due to the incorporation of new taxes in to the National Accounts, most notably the Apprenticeship Levy from Quarter 2 2017. This improves the alignment between National Accounts and Public Sector Finances and revisions improve government’s net borrowing in 2017.

Table 1: Summary of revisions to main economic indicators in the UK Quarterly sector accounts, Quarter 1 (Jan to Mar) 2017 to Quarter 2 (Apr to June) 2018

| Quarter 1 (Jan to Mar) 2017 to Quarter 2 (Apr to June) 2018 | ||||||

| Revisions to Net lending (+) borrowing (-) positions of UK sectors, £ billions | ||||||

| Non-financial account (B.9n) | ||||||

| Non- financial corporations | Financial corporations | General government | Households | NPISH1 | Rest of the world | |

| 2017 Q1 | 1.1 | 1.3 | 0.0 | -0.6 | 0.0 | -1.4 |

| 2017 Q2 | 3.2 | 0.2 | 0.6 | -1.2 | 0.1 | -2.2 |

| 2017 Q3 | 2.5 | 1.8 | -0.2 | -1.4 | 0.1 | -1.7 |

| 2017 Q4 | 2.3 | 1.6 | 0.7 | -0.4 | -0.3 | -2.8 |

| 2018 Q1 | -2.1 | 0.0 | 0.2 | 1.1 | -0.3 | 2.3 |

| 2018 Q2 | 0.1 | -1.2 | 1.5 | 0.7 | -0.1 | -0.4 |

| Revisions to Net lending (+) borrowing (-) positions of UK sectors, £ billions | ||||||

| Financial account (B.9f) | ||||||

| Non- financial corporations | Financial corporations | General government | Households | NPISH1 | Rest of the world | |

| 2017 Q1 | -2.4 | 5.3 | 0.0 | -3.4 | 0.0 | 0.4 |

| 2017 Q2 | 1.8 | 4.3 | 0.5 | -7.7 | 0.1 | 1.1 |

| 2017 Q3 | 2.8 | -5.3 | -0.1 | -6.6 | 0.0 | 9.2 |

| 2017 Q4 | -18.5 | 6.5 | 0.2 | -1.5 | 0.6 | 12.8 |

| 2018 Q1 | 6.4 | -2.9 | 0.6 | -6.1 | 0.0 | 2.1 |

| 2018 Q2 | -9.3 | 13.8 | 1.9 | -1.8 | -0.7 | -4.0 |

| Revisions to other key economic indicators | ||||||

| Households sector | ||||||

| RHDI2 growth rate (quarter on previous quarter, %) | Saving ratio (%) | HHFCE3 Deflator (index points) | ||||

| 2017 Q1 | 0 | -0.2 | 0.0 | |||

| 2017 Q2 | 0.3 | -0.4 | -0.1 | |||

| 2017 Q3 | 0 | -0.4 | 0.0 | |||

| 2017 Q4 | 1.2 | -0.1 | -0.1 | |||

| 2018 Q1 | -0.8 | 0.2 | 0.0 | |||

| 2018 Q2 | 0.5 | 0.2 | 0.1 | |||

| Source: Office for National Statistics | ||||||

| Notes | ||||||

| 1. Non-profit institutions serving households | ||||||

| 2. Real households' disposable income | ||||||

| 3. Households' final consumption expenditure deflator | ||||||

Download this table Table 1: Summary of revisions to main economic indicators in the UK Quarterly sector accounts, Quarter 1 (Jan to Mar) 2017 to Quarter 2 (Apr to June) 2018

.xls (31.2 kB)11. Changes to this bulletin

Changes to Quarterly sector accounts datasets

We will be incorporating the alternative measures of real households disposable income and saving ratio from this release onwards.

This follows growing user interest in the Alternative measures of households income and saving experimental statistics since their launch in August 2015.

In effect, the underlying data will be moved into the Households chapter (Chapter 6) of the UK Economic Accounts and the accompanying analysis will move to this release. They are both released on the same day. Previously, the alternative measures of real household disposable income and saving ratio were released a week later.

We hope users find this more timely analysis of households’ financial situation useful, and we continue to welcome feedback.

To improve the user’s experience, we have added the self-financed investment ratio of private non-financial corporations in table “KEI” (key economic indicators) of the Quarterly Sector Accounts dataset. This follows on from the addition of households’ debt to income ratio.

As we plan on adding further indicators that are not part of the European System of Accounts 2010: ESA 2010 when they pass our quality assurance tests, we have renamed the "PH – Per head" table "KEI – Key economic indicators" so that users will be able to find these and future indicators under a clear heading.

Finally, both Welsh and Scottish registered providers of social housing have now been reclassified from the public to the private non-financial corporation sector.

Public corporation debt fell by £3.0 billion in June 2018 (reclassification of Welsh housing associations ) and by £4.2 billion in September 2018 (reclassification of Scottish housing associations). These estimates are derived from forecasts produced by the Office for Budgetary Responsibility that will be replaced when updated data becomes available. This reclassification has already been implemented in the Public Sector Finances.

Upcoming changes: Accounting for student loans in the accounts

The implementation date for including this change in the National Accounts has yet to be decided and further methodological work is required to establish the exact size of the impact on the government and household accounts. However, when it is implemented we will observe a significant increase in the amount of capital transfers payable from central government to households and a reduction in the amount of interest receivable by central government from households. There will also be a reduction in the stock of loan assets held by central government and an equivalent reduction in loan liabilities of households. For more information, see the announcement on: How we are improving the recording of student loans in government accounts.

If you have any suggestions please contact us by email at sector.accounts@ons.gov.uk.

Back to table of contents12. Quality and methodology

National Statistics status

On 20 March 2018, the UK Statistics Authority published a letter confirming the designation of quarterly sector accounts statistics as National Statistics. National Statistics means that official statistics meet the highest standards of trustworthiness, quality and value. The letter praised the richer analysis on the households sector and the improvements in communicating technical concepts to a less technical audience.

We are keen to continue this type of analysis and we welcome feedback and suggestions for additional content for the bulletin or supplementary pieces.

Reliability

Estimates for the most recent quarters are provisional and are subject to revision in the light of updated source information. Our revisions to economic statistics page contains articles on revisions and revisions policies.

Revisions to data provide one indication of the reliability of main indicators. Revisions triangles were published for the households and non-profit institutions serving households saving ratio. However, following the separation of the households and non-profit institutions serving households (NPISH) sectors in September 2017, we have ceased production of the revision triangles for the households and NPISH saving ratio. In due course, we will reintroduce the revision triangle for the households-only saving ratio as and when meaningful analysis on revisions can be done.

Comparability

Data in this bulletin are internationally comparable. The UK National Accounts are compiled in accordance with the European System of Accounts 2010: ESA 2010, under EU law and in common with all other members of the European Statistical System. ESA 2010 is itself consistent with the standards set out in the United Nations System of National Accounts 2008: SNA 2008.

An explanation of the sectors and transactions described in this bulletin can be found in Chapter 2 of the ESA 2010 manual.

Methodology

This section summarises the methodology behind some of our main economic indicators: real household disposable income, households saving ratio and net lending or borrowing positions

Real household disposable income (RHDI) explained

Household income is measured in two ways: in current prices (also called nominal prices) and in real terms, where the effect of price inflation is removed.

Gross disposable household income (GDHI) is the estimate of the total amount of income that households have available to either spend, save or invest. It includes income received from wages (and the self-employed), social benefits, pensions and net property income (that is, earnings from interest on savings and dividends from shares) less taxes on income and wealth. These are all given in current prices.

Therefore, GDHI tells us how much income households had to spend, save or invest in the time period being measured once taxes on income and wealth had been paid.

Adjusting GDHI to remove the effects of inflation gives another measure of disposable income called real household disposable income (RHDI). This is a measure of the real purchasing power of households’ income, in terms of the physical quantity of goods and services they would be able to purchase if prices remained constant over time. Further information on this calculation can be found in our Quality and Methodology Information.

The households’ saving ratio explained

The saving ratio estimates the amount of money households have available to save (gross saving) as a percentage of their gross disposable income plus pension accumulations (total available resources).

Gross saving is the difference between households’ total available resources (that is, GDHI plus pension accumulations) and household expenditure on goods and services for consumption.

The saving ratio can be volatile and is sensitive to even relatively small movements in its components, particularly on a quarterly basis. This is because gross saving is a relatively small difference between two large numbers. It is therefore often revised at successive publications when there are revisions to data.

The saving ratio may be considered an indicator of households’ economic confidence as well as an indicator of households’ financial conditions.

A higher saving ratio may be the result of an increase in income, a decrease in expenditure, or some combination of the two. A rise in the saving ratio may be an indication that households are acting more cautiously by spending less. Conversely, a fall in the saving ratio may be an indication that households are more confident and spending more. Other factors such as interest rates and inflation should also be considered when interpreting the households saving ratio.

Net lending (+) or borrowing (-) positions explained

The net lending or borrowing of a sector represents the net resources that the sector makes available to the rest of the economy. It does not necessarily refer to actual lending or borrowing in the normal sense, rather, it means that either a sector has money left over after its spending and investment in a given period (net lending), or it has spent and invested more than it received and has a need for financing (net borrowing), which may be covered by borrowing, issuing shares or bonds, or by drawing on reserves.

The net lending or borrowing position is determined by gross saving (that is, the balance between gross disposable income and final consumption expenditure) and is reduced or increased by the balance of capital transfers and the change in non-financial assets. This final position is called the net lending (if positive) or borrowing (if negative) position.

In summary, if actual investment is lower than the amount available for investment, the balance will be positive and represents net lending. Alternatively, if actual investment is higher than the amount available for investment, net borrowing is represented.

Note that, theoretically, the sum of net lending or borrowing positions of UK sectors must equal that of the rest of the world. However, this is only currently true up to 2016 data. From 2017 onwards, unbalanced supply use tables (SUT) in the compilation of gross domestic product (GDP) are unbalanced and it can take approximately 18 months after the end of the latest balanced year (currently 2016) for balanced SUTs to become available.

Quality and Methodology Information report

The Quarterly sector accounts Quality and Methodology Information report contains important information on:

- the strengths and limitations of the data and how it compares with related data

- uses and users of the data

- how the output was created

- the quality of the output including the accuracy of the data

The Quarterly sector accounts and the UK Economic Accounts are published at quarterly, pre-announced intervals alongside the Quarterly national accounts and Quarterly balance of payments statistical bulletins.

Back to table of contents13. Appendix A: key economic indicators

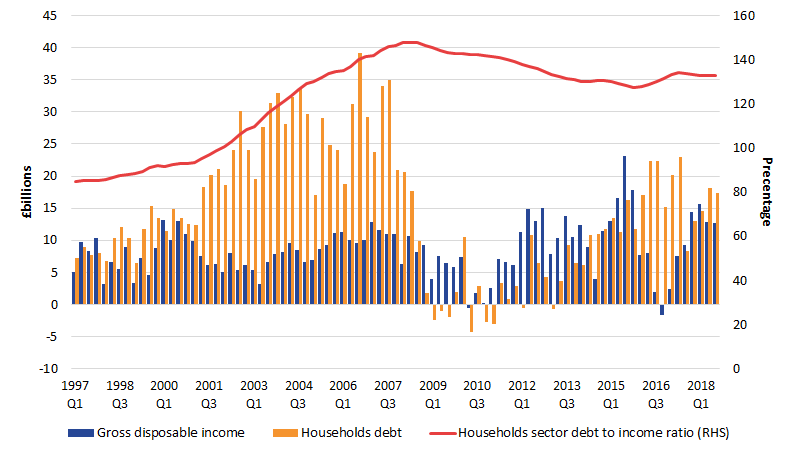

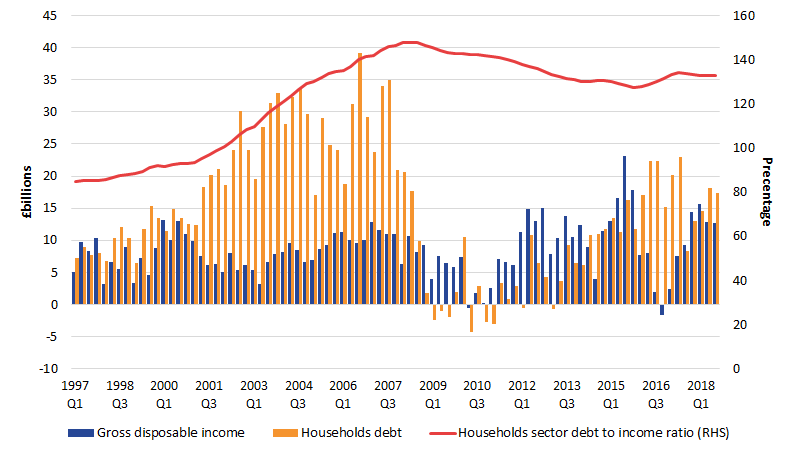

Figure 15: UK Households debt to income ratio, percentage

Quarter 1 (Jan to Mar) 1997 to Quarter 3 (July to Sept) 2018

Source: Office for National Statistics

Notes:

- Gross disposable income calculated as the four-quarter rolling sum.

- Households debt calculated as total loans held by households.

- Households debt to income ratio calculated as gross disposable income divided by household debt.

Download this image Figure 15: UK Households debt to income ratio, percentage

.png (17.3 kB) .xls (50.7 kB){kind=link}

Figure 16: Private non-financial corporations self-financed investment ratio, percentage

Quarter 1 (Jan to Mar) 2008 to Quarter 3 (July to Sept) 2018

Source: Office for National Statistics

Download this image Figure 16: Private non-financial corporations self-financed investment ratio, percentage

.png (30.8 kB) .xls (46.6 kB){kind=link}

Figure 17: UK households’ net lending (plus) or borrowing (minus) position, quarterly, seasonally adjusted

Quarter 1 (Jan to Mar) 1987 to Quarter 3 (July to Sept) 2018

Source: Office for National Statistics

Download this chart Figure 17: UK households’ net lending (plus) or borrowing (minus) position, quarterly, seasonally adjusted

Image .csv .xls14. Appendix B: additional information on the alternative measures of households’ income and savings

Table 2: Quarterly change in the value of transactions removed from the national accounts methodology to calculate cash basis gross disposable household income and the saving ratio

| Quarter 3 (July to Sept) 2018 | ||

|---|---|---|

| Transactions | CDID | Quarterly change, £ million |

| Transaction removed from the National Accounts measure of Gross disposable income | ||

| Gross operating surplus (B.2g) | CAEO | 1,516 |

| Employers' social contributions* (D.12r) | DTWP | 792 |

| Financial Intermediation Services Indirectly Measured (FISIM) (P.119r) | CRNC | 1247 |

| Investment income payable on pension entitlements* (D.442r) | KZL5 | -71 |

| Retained earnings attributable to collective investment fund shareholders (D.4432r) | MN7M | 22 |

| Financial Intermediation Services Indirectly Measured (FISIM) (P.119u) | CRNB | -1333 |

| Employers' imputed social contributions (D.612r) | L8RQ | -3 |

| Non-life insurance claims (D.72r) | RNLU | 23 |

| Employers' actual social contributions* (D.611u) | L8NM | 845 |

| Employers' imputed social contributions* (D.612u) | MA4B | -53 |

| Households' social contribution supplements* (D.614u) | L8QA | -71 |

| Further transaction removed from the National Accounts measure of Households saving ratio | ||

| Adjustment for the change in pension entitlements (D.8r) | RNMB | 622 |

| Imputed rental for housing (removed from cash basis final consumption expenditure) | GBFJ | 225 |

| Financial Intermediation Services Indirectly Measured (FISIM) (removed from cash basis final consumption expenditure) | C68W | 1100 |

| Source: Office for National Statistics | ||

| Notes: | ||

| 1. Transactions marked with an asterisk (*) are those whose values, in accordance with the European System of Accounts 2010 (ESA10), net to 0. | ||

| 2. The removal of the transactions in the table not marked with an asterisk (*) explain the difference between gross disposable income, gross saving and final consumption expenditure on a cash basis. | ||

| 3. Codes (in brackets) used in Table 2 are European System of Accounts 2010 (ESA 2010) codes | ||

| 4. CDIDs are unique random identifiers for individual time series. They do not themselves have any specific meaning but enable users to reference this table with the accompanying data tables provided. | ||

Download this table Table 2: Quarterly change in the value of transactions removed from the national accounts methodology to calculate cash basis gross disposable household income and the saving ratio

.xls (43.0 kB)15. Acknowledgements

The author, Michael Rizzo, would like to express his thanks to Freddy Farias Arias at Office for National Statistics for his contributions to this work.

Back to table of contentsContact details for this Statistical bulletin

Related publications

- Balance of payments, UK: July to September 2018

- Consumer trends, UK: July to September 2018

- Business investment in the UK: July to September 2018 revised results

- GDP quarterly national accounts, UK: July to September 2018

- Public sector finances, UK: November 2018

- Quarterly economic commentary: July to September 2018