Table of contents

- Main points

- Things you need to know about this release

- Real household disposable income grew for a second consecutive quarter with growth of 0.4%

- Households’ saving ratio increased to 3.9% in the latest quarter, up from 3.6% in the previous quarter

- What has happened to the net lending or borrowing positions of UK sectors?

- Summary of revisions to net lending or borrowing positions

- National accounts articles

- Links to related statistics

- Links to related analysis

- Changes to this bulletin

- Quality and methodology

- Appendix A: key economic indicators

- Acknowledgements

1. Main points

In Quarter 2 (Apr to June) 2018, real household disposable income grew for a second consecutive quarter, with growth of 0.4%, compared with an upwardly revised growth of 0.7% in the previous quarter.

Despite a marginal increase in the households’ saving ratio to 3.9%, in Quarter 2 2018, it remains historically low and is the fourth-lowest since records began in 1963.

Households were net borrowers for a seventh consecutive quarter (at £7.2 billion) in Quarter 2 2018 as they continue to spend and invest more than they received in income.

Corporations increased their net borrowing by £11.7 billion in Quarter 2 2018, to 2.2% of GDP.

Central government continues to show a decrease in their net borrowing, a trend that began in 2010.

2. Things you need to know about this release

National Statistics status

On 20 March 2018, the UK Statistics Authority published a letter confirming the designation of quarterly sector accounts statistics as National Statistics. National Statistics means that official statistics meet the highest standards of trustworthiness, quality and value. The letter praised the richer analysis on the households’ sector and the improvements in communicating technical concepts to a less technical audience.

We are keen to continue this type of analysis and we welcome feedback and suggestions for additional content for the bulletin or supplementary pieces.

Understanding the sector and financial accounts

This bulletin presents UK aggregate data for the main economic indicators and summary estimates from the institutional sectors of the UK economy: private non-financial corporations, public corporations, financial corporations, central and local government, households, non-profit institutions serving households (NPISH) and the rest of the world sector, that are presented in the UK Economic Accounts (UKEA) dataset.

This bulletin uses data from the UKEA and it provides detailed estimates of national product, income and expenditure, UK Sector, Non-financial and Financial Accounts, and UK Balance of Payments. These accounts are the underlying data that produce a single estimate of gross domestic product (GDP) using income, production and expenditure data.

Comparability

Data in this bulletin are internationally comparable. The UK National Accounts are compiled in accordance with the European System of Accounts 2010: ESA 2010, under EU law and in common with all other members of the European Statistical System. ESA 2010 is itself consistent with the standards set out in the United Nations System of National Accounts 2008: SNA 2008.

An explanation of the sectors and transactions described in this bulletin can be found in Chapter 2 of the ESA 2010 manual.

Estimates within this release

This bulletin includes new data for the latest available quarter, Quarter 2 (Apr to June) 2018 and revisions to data from Quarter 1 (Jan to Mar) 2017 to Quarter 1 2018.

This bulletin follows the National Accounts Revisions Policy.

All data within this bulletin are estimated in current prices (also called nominal prices), except for real household disposable income, which is estimated in chained volume terms.

Current price series are expressed in terms of the prices during the time period being estimated. These describe the prices recorded at the time of production or consumption and include the effect of price inflation over time. Chained volume series (also known as real terms) have had the effects of inflation removed.

All figures given in this bulletin are adjusted for seasonality, unless otherwise stated. Seasonal adjustment removes seasonal or calendar effects from data to enable more meaningful comparisons over time.

The Population estimates for the UK, England and Wales, Scotland and Northern Ireland used in this release are those published on 28 June 2018.

Real household disposable income (RHDI) explained

Household income is measured in two ways: in current prices (also called nominal prices) and in real terms, where the effect of price inflation is removed.

Gross disposable household income (GDHI) is the estimate of the total amount of income that households have available to either spend, save or invest. It includes income received from wages (and the self-employed), social benefits, pensions and net property income (that is, earnings from interest on savings and dividends from shares) less taxes on income and wealth. These are all given in current prices.

Therefore, GDHI tells us how much income households had to spend, save or invest in the time period being measured once taxes on income and wealth had been paid.

Adjusting GDHI to remove the effects of inflation gives another measure of disposable income called real household disposable income (RHDI). This is a measure of the real purchasing power of households’ income, in terms of the physical quantity of goods and services they would be able to purchase if prices remained constant over time. Further information on this calculation can be found in our Quality and Methodology Information.

The households’ saving ratio explained

The saving ratio estimates the amount of money households have available to save (gross saving) as a percentage of their gross disposable income plus pension accumulations (total available resources).

Gross saving is the difference between households’ total available resources (that is, GDHI plus pension accumulations) and household expenditure on goods and services for consumption.

The saving ratio can be volatile and is sensitive to even relatively small movements in its components, particularly on a quarterly basis. This is because gross saving is a relatively small difference between two large numbers. It is therefore often revised at successive publications when there are revisions to data.

The saving ratio may be considered an indicator of households’ confidence as well as an indicator of households’ financial conditions.

A higher saving ratio may be the result of an increase in income, a decrease in expenditure, or some combination of the two. A rise in the saving ratio may be an indication that households are acting more cautiously by spending less. Conversely, a fall in the saving ratio may be an indication that households are more confident and spending more. Other factors such as interest rates and inflation should also be considered when interpreting the households saving ratio.

Net lending (+) or borrowing (-) positions explained

The net lending or borrowing of a sector represents the net resources that the sector makes available to the rest of the economy. It does not necessarily refer to actual lending or borrowing in the normal sense, rather, it means that either a sector has money left over after its spending and investment in a given period (net lending), or it has spent and invested more than it received and has a need for financing (net borrowing), which may be covered by borrowing, issuing shares or bonds, or by drawing on reserves.

The net lending or borrowing position is determined by gross saving (that is, the balance between gross disposable income and final consumption expenditure) and is reduced or increased by the balance of capital transfers and the change in non-financial assets. This final position is called the net lending (if positive) or borrowing (if negative) position.

In summary, if actual investment is lower than the amount available for investment, the balance will be positive and represents net lending. Alternatively, if actual investment is higher than the amount available for investment, net borrowing is represented.

Reliability

Estimates for the most recent quarters are provisional and are subject to revision in the light of updated source information. Our revisions to economic statistics page contains articles on revisions and revisions policies.

Revisions to data provide one indication of the reliability of main indicators. Revisions triangles were published for the households and non-profit institutions serving households saving ratio. However, following the separation of the households and NPISH sectors in September 2017, we have ceased production of the revision triangles for the households and NPISH saving ratio. In due course, we will reintroduce the revision triangle for the households-only saving ratio as and when meaningful analysis on revisions can be done.

Back to table of contents3. Real household disposable income grew for a second consecutive quarter with growth of 0.4%

Real household disposable income (RHDI) in Quarter 2 (Apr to June) 2018 increased by 0.4%, quarter on previous quarter, as gross disposable income increased at a faster pace than price rises. This is a slowdown compared with the previous quarter when RHDI grew by 0.7%.

Gross disposable household income (GDHI) increased by £1.9 billion in the latest quarter and contributed to RHDI growth (0.6 percentage points), as shown in Figure 1. Most of this growth was led by a £0.9 billion increase in social assistance benefits received and a £0.7 billion increase in wages and salaries. The increase in wages and salaries was a slowdown compared with the previous quarter’s increase of £2.3 billion. Part of this slowdown was due to the number of new people entering employment narrowing to approximately 42,000 compared with a much higher 197,000 in the previous quarter (see UK labour market: September 2018).

This growth in GDHI was partly offset by a 0.2% rise in prices affecting households. This was a sharp drop in the impact of inflation following two quarters of relatively large impacts (both at 0.9 percentage points).

Figure 1: Contributions to real household disposable income growth, quarter on previous quarter, percentage points

UK, Quarter 2 (Apr to June) 2013 to Quarter 2 (Apr to June) 2018

Source: Office for National Statistics

Notes:

- Sum of contributions to real household disposable income may not add to growth rate due to rounding.

Download this chart Figure 1: Contributions to real household disposable income growth, quarter on previous quarter, percentage points

Image .csv .xlsLong-term perspective

Figure 2 shows a smoother, long-term picture on the contributions to RHDI growth, using quarter on same quarter a year ago comparisons.

For five consecutive quarters between Quarter 3 (July to Sept) 2016 and Quarter 3 2017, real household disposable income (RHDI) fell by an average of 0.9% per quarter, when using this quarter on same quarter a year ago comparison.

The last time households saw their real disposable incomes fall for a similar length of time was for seven consecutive quarters between Quarter 2 2010 and Quarter 4 (Oct to Dec) 2011. However, then, the average quarter on same quarter a year ago growth rate fall was 1.6% per quarter. That fall in RHDI was more prolonged and more severe than the recent fall.

In the latest quarter, RHDI was 0.6% higher compared with RHDI in the same quarter a year ago. This was the third consecutive quarter on same quarter a year ago growth following five quarters of zero or negative growth.

However, RHDI levels in Quarter 2 2018 were still below their recent Quarter 3 2015 peak, by £4.5 billion (1.4%).

Figure 2: Contributions to real household disposable income growth, quarter on same quarter a year ago, percentage points

UK, Quarter 2 (Apr to June) 1998 to Quarter 2 (Apr to June) 2018

Source: Office for National Statistics

Notes:

- Sum of contributions to real household disposable income may not add to growth rate due to rounding.

Download this chart Figure 2: Contributions to real household disposable income growth, quarter on same quarter a year ago, percentage points

Image .csv .xlsRevisions to real household disposable income

This bulletin includes revisions to data from Quarter 1 (Jan to Mar) 2017 in line with the National Accounts Revisions Policy.

In the five quarters open to revision, RHDI was revised up by an average of £1.2 billion per quarter.

Figure 3 shows that revisions to wages and salaries were the main source of these revisions. There was an average upward revision of £1.9 billion per quarter as new data for the public sector have been incorporated from Quarter 1 2017. The alignment of private sector wages and salaries to comparable labour market data has also been reviewed, resulting in upward revisions to wages and salaries in all quarters.

Revisions to the households’ expenditure deflator were on average zero throughout the five quarters, while other components of RHDI saw net downward revisions of an average £0.7 billion per quarter, due mainly to new data.

The largest impacts of these revisions on quarter on previous quarter growth rates were in Quarter 1 2017 and Quarter 1 2018; with an upward revision of 0.6 percentage points to negative 0.4% and an upward revision of 0.4 percentage points to positive 0.7%, respectively.

Figure 3: Impact of revisions to real household disposable income, £ billions

UK, Quarter 1 (Jan to Mar) 2017 to Quarter 1 (Jan to Mar) 2018

Source: Office for National Statistics

Download this chart Figure 3: Impact of revisions to real household disposable income, £ billions

Image .csv .xls4. Households’ saving ratio increased to 3.9% in the latest quarter, up from 3.6% in the previous quarter

As Figure 4 shows, the households’ saving ratio remained historically low at 3.9% in the latest quarter, the fourth-lowest since records began in 1963. There was, however, a marginal increase from 3.6% in the previous quarter, which was the joint second-lowest on record.

Figure 4: UK households’ saving ratio, quarterly, seasonally adjusted

Quarter 1 (Jan to Mar) 1963 to Quarter 2 (Apr to June) 2018

Source: Office for National Statistics

Download this chart Figure 4: UK households’ saving ratio, quarterly, seasonally adjusted

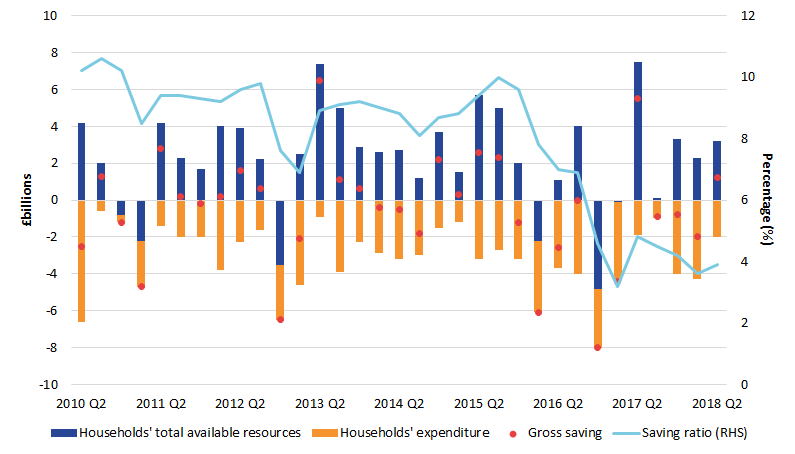

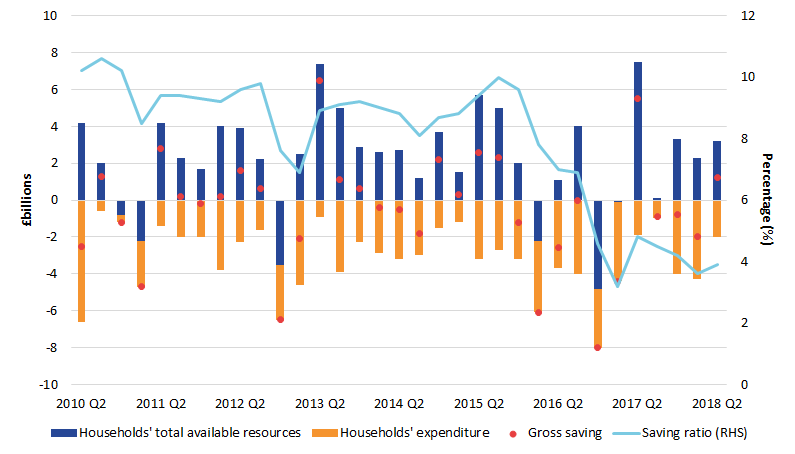

Image .csv .xlsFigure 5 shows that the marginal rise in the saving ratio was due to households’ total available resources increasing more than households’ expenditure in Quarter 2 (Apr to June) 2018.

The increase in households’ total available resources was driven by increased accumulation of pension entitlements (£1.3 billion), an increase in social assistance benefits received (£0.9 billion) and an increase in wages and salaries (£0.7 billion).

Households’ expenditure in the latest quarter increased by £2.0 billion and was mainly driven by a fall in life insurance claims (£0.7 billion), which are deducted from premium expenditure. This was a slowdown in households’ expenditure compared with last quarter’s increase of £4.3 billion, which helped dampen the downward effect households spending has on the saving ratio.

Figure 5: Contributions to the household's saving ratio, seasonally adjusted, £ billions

Quarter 2 (Apr to June) 2010 to Quarter 2 (Apr to June) 2018, UK

Source: Office for National Statistics

Notes:

- Saving ratio calculated as gross saving divided by total available resources.

- Gross saving calculated as total available resources minus households' final consumption expenditure.

- Total available resources calculated as gross disposable income plus adjustment to pension entitlements.

- Saving ratio (%) refers to the axis on the right-hand side (RHS). All others refer to the left-hand side axis.

Download this image Figure 5: Contributions to the household's saving ratio, seasonally adjusted, £ billions

.png (24.6 kB) .xls (43.5 kB){kind=link}

Long-term perspective

The saving ratio in Quarter 2 2018 was the fourth-lowest since records began in 1963. This follows a historically low period in the amount of income available to save since Quarter 3 (July to Sept) 2016.

In the Quarterly sector accounts, UK: January to March 2018 we highlighted the historical significance of the recent decline in the saving ratio, which is larger and more prolonged than previous drops in the saving ratio seen in the late 1980s and late 1990s.

Figure 6 highlights the significance of the slowdown in gross disposable household income (GDHI). GDHI began to plateau from Quarter 2 2015 and has just about kept up with the continued upward trend in spending. As a result of this narrowing gap between income and spending, little is left over to allow for saving, and hence the recent decline in the saving ratio (this is before we take accumulated pension entitlements into account which are essentially a measure of deferred saving).

Figure 6: UK households’ income and spending levels, quarterly, £billions, seasonally adjusted

Quarter 2 (Apr to June) 2007 to Quarter 2 (Apr to June) 2018

Source: Office for National Statistics

Download this chart Figure 6: UK households’ income and spending levels, quarterly, £billions, seasonally adjusted

Image .csv .xlsRevisions to the saving ratio

This bulletin includes revisions to data from Quarter 1 (Jan to Mar) 2017 in line with the National Accounts Revisions Policy.

The saving ratio has been revised downward by an average of 0.1 percentage points per quarter in the five quarters open for revision, with the largest revisions occurring in the last two quarters, Quarter 4 (Oct to Dec) 2017 and Quarter 1 (Jan to Mar) 2018, of negative 0.3 percentage points and negative 0.5 percentage points, respectively.

These two revisions to the saving ratio stemmed from upward revisions to households’ expenditure (of £0.6 billion and £0.7 billion, respectively) and downward revisions to total available resources (£0.4 billion and £1.0 billion, respectively), as shown in Figure 7.

The downward revision to total available resources was driven by the removal of the upwards balancing adjustments previously applied to employer’s contributions from Quarter 1 2017 to Quarter 1 2018 during the gross domestic product (GDP) production process. This reduces the amount accumulated in pension entitlement (a component of total available resources).

Offsetting these, was wages and salaries where, within it, new data for the public sector have been incorporated from Quarter 1 2017 and the alignment of private sector wages and salaries to comparable labour market data has been reviewed, resulting in upward revisions to wages and salaries in all quarters.

The upward revisions to households’ expenditure in Quarter 4 2017 and Quarter 1 2018 were predominantly driven by the take on of new data on households’ expenditure on motor cars. In Quarter 1 2018, new data on households’ expenditure on life insurance have also added to the revision.

Figure 7: Impact of revisions to the UK households’ gross savings, quarterly, seasonally adjusted

Quarter 1 (Jan to Mar) 2017 to Quarter 1 (Jan to Mar) 2018

Source: Office for National Statistics

Notes:

- Total available resources is calculated as gross disposable income plus the accumulation of pension entitlements.

Download this chart Figure 7: Impact of revisions to the UK households’ gross savings, quarterly, seasonally adjusted

Image .csv .xlsOther key economic indicators

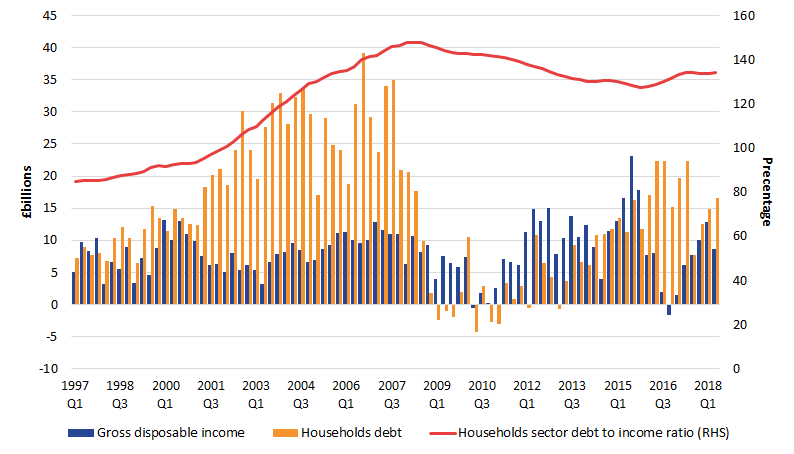

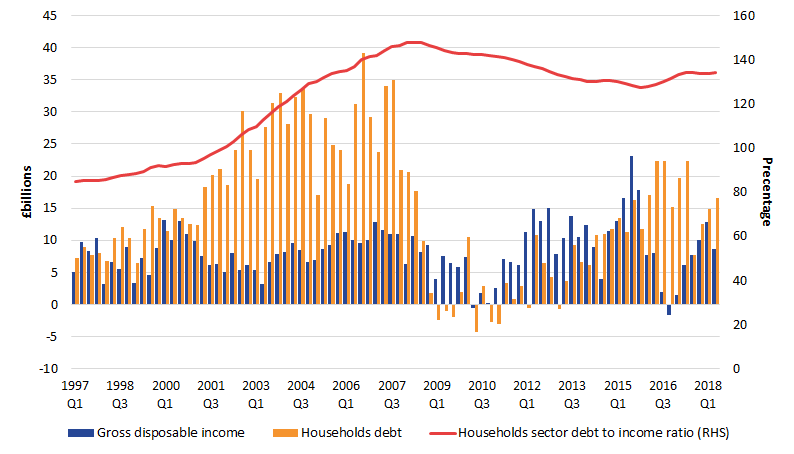

The households sector’s debt to income ratio remained broadly flat in the latest quarter as it only marginally increased to 134.1%, from 133.7% in the previous quarter. This is because the stock of households’ debt increased at a faster rate than gross disposable income (calculated as the sum of the latest four quarters).

For the first time, this series is now officially produced and can now be found in our new “Table KEI” in the Quarterly sector accounts dataset, published alongside this bulletin. This has been done following user feedback and the growing interest in important economic indicators related to households. See Appendix A, Figure 9, for a representation of the ratio and its drivers.

Another important economic indicator is real household disposable income per head, which also remained flat. Further analysis on this indicator will be published on 8 October 2018 in the Economic well-being, UK: April to June 2018 bulletin alongside Alternative measures of UK households' income and saving: April to June 2018.

Back to table of contents5. What has happened to the net lending or borrowing positions of UK sectors?

The net lending or borrowing positions of UK sectors and the rest of the world must sum to zero, as total borrowing must be matched by total lending.

The only UK sector in Quarter 2 (Apr to June) 2018 in a net lending position was the non-profit institutions serving households sector (albeit by a very small amount at 0.1% of gross domestic product (GDP)). All other UK sectors were net borrowers in the non-financial account.

Figure 8 summarises the net lending (positive) or borrowing (negative) positions of UK sectors and the rest of the world, according to the non-financial account, as a percentage of UK GDP. Following Figure 8 is further analysis on each sector’s position.

Figure 8: Net lending (positive) or borrowing (negative) positions of UK sectors and the rest of the world in the non-financial account as a percentage of UK GDP

Quarter 1 (Jan to Mar) 1987 to Quarter 2 (Apr to June) 2018

Source: Office for National Statistics

Download this chart Figure 8: Net lending (positive) or borrowing (negative) positions of UK sectors and the rest of the world in the non-financial account as a percentage of UK GDP

Image .csv .xlsNon-financial corporations

Non-financial corporations are made up of two sub-sectors: private non-financial corporations (PNFCs) and public corporations.

PNFCs’ net borrowing increased in the latest quarter, Quarter 2 (Apr to June) 2018, to £5.7 billion compared with £0.4 billion in the previous quarter. As a percentage of GDP, their net borrowing position increased to 1.1% compared with 0.1% in the previous quarter, and is the joint second-largest net borrowing sector in the UK.

This increase was due mainly to changes in inventories returning to positive levels in the latest quarter (£0.9 billion) following two quarters of relative large drops (inventories fell by £3.4 billion in Quarter 1 (Jan to Mar) 2018 and £0.9 billion in the previous quarter). This is PNFCs’ largest net borrowing position since Quarter 3 (July to Sept) 2016 when it was £13.2 billion, or 2.7% as a percentage of GDP.

In November 2017, following changes to the regulation of social housing in England, English housing associations were reclassified back into the private non-financial corporations sector. This reclassification has been implemented in Blue Book 2018 from November 2017, the date the regulations came into force.

As a result, public corporations’ net borrowing halved to £0.7 billion between Quarter 3 2017 and Quarter 4 (Oct to Dec) 2017.

In the first quarter of 2018, public corporations’ net borrowing then fell again (to £0.3 billion) as a result of English housing associations being completely excluded from the public corporations sector, and was unchanged in the latest quarter. As a percentage of GDP, public corporations were net borrowers of 0.1% of GDP.

From Quarter 1 2018 onwards, public corporations include devolved housing associations only.

Financial corporations

In the latest quarter, Quarter 2 2018, financial corporations returned to being net borrowers (of £5.7 billion) following a net lending position in the previous quarter (of £0.3 billion). As a percentage of GDP, their net borrowing position in the latest quarter is now 1.1% compared with a net lending position of 0.1% of GDP in the previous quarter, and is the joint second-largest net borrowing sector in the UK.

This switch in positions was due mainly to a net drop of £2.8 billion in distributed income of corporations.

General government

Government net borrowing decreased in the latest quarter, Quarter 2 2018, to £6.6 billion from £12.3 billion in the previous quarter. As a percentage of GDP, the general government’s net borrowing position narrowed to 1.3% compared with 2.4% in the previous quarter. This is the narrowest quarterly net borrowing position since Quarter 1 2002 and the movement in the latest quarter was driven by a drop in net borrowing from central government.

The drop in central government’s net borrowing was due to an increase in the income received from distributed income of corporations (£2.8 billion) and a decrease in investment grants paid out (£1.7 billion), partly offset by a £1.2 billion increase in social benefits other than transfers in kind paid out.

Further details on this sector can be found in Public sector finances, UK: August 2018. Note that although public sector finances and national accounts are compiled in accordance with the European System of Accounts: ESA 2010, some differences remain.

Households

It is now the seventh consecutive quarter in which households have been net borrowers, meaning that they had to borrow (or draw on their reserves) to fund their spending and investment activities. Up until Quarter 3 2016, households were net lenders.

In Quarter 2 2018, households experienced a marginal narrowing of their net borrowing position to £7.2 billion (or 1.4% of GDP) from £7.8 billion (or 1.5% of GDP).

Much of this slight narrowing in net borrowing in the latest quarter was due to an increased accumulation of pension entitlements (£1.3 billion) and an increase in wages and salaries (£0.7 billion), partially offset by an increase in households’ expenditure (up £2.0 billion).

Non-profit institutions serving households (NPISH)

In Quarter 2 2018, the NPISH sector was a net lender for the fourteenth consecutive quarter at £0.7 billion (or 0.1% of GDP) compared with £0.4 billion in the previous quarter. Driving this was an increase of £0.8 billion in current transfers from central government to NPISH, partially offset by a £0.3 billion drop in investment grants received.

The NPISH sector is a relatively small sector compared with other UK sectors. However, the sector (which includes, for example, charities and universities) remains an important one because of its social benefits to society.

Our Quarterly sector accounts, UK: October to December 2017 bulletin provided an overview on the net lending or borrowing position of the NPISH sector over time.

Rest of the world

The amount the rest of the world lends to UK sectors increased by £5.2 billion in the latest quarter, Quarter 2 2018, to £20.9 billion.

In Quarter 2 2018, the increase in lending was due mainly to an increase in the external balance of goods and services (£2.8 billion), and an increase in the amount received in distributed income of corporations (£2.0 billion) and interest received (£1.5 billion).

Further details of the UK Balance of Payments position can be found in the Balance of payments bulletin

Back to table of contents6. Summary of revisions to net lending or borrowing positions

A summary of revisions in the quarters open to revisions can be seen in Table 1. Most of these revisions are as a result of updated data sources.

Table 1: Summary of revisions to main economic indicators in the UK Quarterly sector accounts, Quarter 1 (Jan to Mar) 2017 to Quarter 1 (Jan to Mar) 2018

| Revisions to Net lending (+) borrowing (-) positions of UK sectors, £ billions | ||||||

|---|---|---|---|---|---|---|

| Non-financial account (B.9n) | ||||||

| Non- financial corporations | Financial corporations | General government | Households | NPISH1 | Rest of the world | |

| 2017 Q1 | -1.2 | 0.2 | -0.2 | 0.8 | 0.1 | 0.5 |

| 2017 Q2 | -2.5 | 2.0 | -0.3 | 0.7 | 0.2 | -0.1 |

| 2017 Q3 | 1.0 | 0.1 | -0.1 | 0.7 | 0.2 | -1.9 |

| 2017 Q4 | 1.4 | 0.4 | -0.3 | -1.1 | 0.3 | -1.0 |

| 2018 Q1 | 3.5 | -0.3 | 0.8 | -2.0 | -0.2 | -2.2 |

| Revisions to Net lending (+) borrowing (-) positions of UK sectors, £ billions | ||||||

| Financial account (B.9f) | ||||||

| Non- financial corporations | Financial corporations | General government | Households | NPISH1 | Rest of the world | |

| 2017 Q1 | 9.5 | -3.8 | 0.4 | -1.3 | 0.1 | -5.0 |

| 2017 Q2 | 0.6 | -7.1 | -0.2 | 6.8 | 0.1 | -0.1 |

| 2017 Q3 | -4.6 | 1.8 | -0.2 | -4.0 | 0.1 | 7.0 |

| 2017 Q4 | 1.4 | -2.5 | -0.3 | -2.1 | -0.5 | 4.1 |

| 2018 Q1 | -2.6 | 9.3 | 0.5 | -9.7 | 2.4 | 0.2 |

| Revisions to other key economic indicators | ||||||

| Households sector | ||||||

| RHDI2 growth rate (quarter on previous quarter, %) | Saving ratio (%) | HHFCE3 Deflator (index points) | ||||

| 2017 Q1 | 0.6 | 0.2 | -0.1 | |||

| 2017 Q2 | 0 | 0.2 | 0.1 | |||

| 2017 Q3 | -0.1 | 0.1 | 0.0 | |||

| 2017 Q4 | -0.3 | -0.3 | 0.1 | |||

| 2018 Q1 | 0.4 | -0.5 | -0.1 | |||

| Source: Office for National Statistics | ||||||

| Notes | ||||||

| 1. Non-profit institutions serving households | ||||||

| 2. Real households' disposable income | ||||||

| 3. Households' final consumption expenditure deflator | ||||||

Download this table Table 1: Summary of revisions to main economic indicators in the UK Quarterly sector accounts, Quarter 1 (Jan to Mar) 2017 to Quarter 1 (Jan to Mar) 2018

.xls (39.4 kB)7. National accounts articles

We recently published an article stating the impacts on the sector and financial accounts following changes made in Blue Book 2018. A detailed assessment on the indicative impacts can be found in National Accounts articles: Detailed assessment of changes to sector and financial accounts, 1997 to 2016.

Our national accounts publication Blue Book 2018 was published on 31 July 2018.

Back to table of contents10. Changes to this bulletin

Changes to Quarterly sector accounts datasets

To improve the user’s experience we have added an additional important economic indicator, "household sector debt to income ratio", to the bulletin alongside the per head data. As we plan on adding further indicators that are not part of the European System of Accounts 2010: ESA 2010 when they pass our quality assurance tests, we have renamed the "PH – Per head" table "KEI – Key economic indicators" so that users will be able to find these and future indicators under a clear heading.

If you have any suggestions please contact us by email at sector.accounts@ons.gov.uk.

Back to table of contents11. Quality and methodology

The Quarterly sector accounts Quality and Methodology Information report contains important information on:

- the strengths and limitations of the data and how it compares with related data

- uses and users of the data

- how the output was created

- the quality of the output including the accuracy of the data

The Quarterly sector accounts and the UK Economic Accounts are published at quarterly, pre-announced intervals alongside the Quarterly national accounts and Quarterly balance of payments statistical bulletins.

Back to table of contents12. Appendix A: key economic indicators

Figure 9: UK Households' debt to income ratio, percentage

UK, Quarter 1 (Jan to Mar) 1997 to Quarter 2 (Apr to June) 2018

Source: Office for National Statistics

Notes:

1.Gross disposable income calculated as the four-quarter rolling sum. 2.Households debt calculated as total loans held by households. 3. Households debt to income ratio calculated as gross disposable income divided by household debt, and refers to the right-hand side (RHS) axis.

Download this image Figure 9: UK Households' debt to income ratio, percentage

.png (19.9 kB) .xls (55.3 kB){kind=link}

13. Acknowledgements

The author, Michael Rizzo, would like to express his thanks to Freddy Farias Arias at Office for National Statistics for his contributions to this work.

Back to table of contentsContact details for this Statistical bulletin

Related publications

- Quarterly economic commentary: January to March 2026

- GDP quarterly national accounts, UK: January to March 2026

- Balance of payments, UK: January to March 2026

- Consumer trends, UK: January to March 2026

- Business investment in the UK: January to March 2026 revised results

- Economic statistics sector classification – classification update and forward work plan: June 2024