2. Main points

Post-referendum data

The Office for National Statistics (ONS) has recently produced an assessment of the post-referendum economy. This concluded that although the picture is still emerging, there has been no major collapse in confidence and within the data that is available there are indications of continued momentum in the economy.

This has been confirmed by the Index of Services for July 2016 which shows month-on-month growth of 0.4%. This can be interpreted as further evidence that the economy has not shown any immediate signs of major negative effects following the EU referendum decision.

GDP

The latest estimate of gross domestic product (GDP) for Quarter 2 (April to June) 2016 published in September 2016 indicated that the UK economy grew by 0.7%, revised up 0.1 percentage points from the second estimate published in August. This maintains the picture of positive growth in the economy in the run-up to the EU referendum vote in June.

Investment

Investment as measured by gross fixed capital formation (GFCF) was 1.6% higher in Quarter 2 (Apr to June) 2016 compared with Quarter 1 (January to March 2016). This is the first quarter of positive growth since Quarter 3 (July to Sept) 2015 and the highest growth rate since Quarter 1 (Jan to Mar) 2015.

Sterling effects on prices

Sterling appears to have had a greater impact on PPI input prices than on PPI output prices in July and August 2016. It is likely UK producers have not passed on all of the increase in input prices to their customers, and that latent pressures on output and consumer prices may later emerge.

Annual Survey of Hours and Earnings regional analysis

London has a noticeably smaller concentration of employees earning the minimum wage in 2015 and a greater proportion of people on higher hourly wages compared with the other regions. London also displays the most equal distribution of wages between the sexes in 2015.

Back to table of contents3. Introduction

This edition of the Economic Review provides a summary of ONS data covering the post-EU referendum period which have been published since the last Review. This supplements the assessment of the post-referendum economy published on 21 September and the previous edition of the Economic Review which provided a summary of data published in August.

This section of the Review will cover:

- Index of Services for July

- trade statistics for July

- construction output for July

- CPI, PPI and House Price Indices for August

- retail sales for August

- some labour market indicators for August (claimant count and vacancies), and

- public sector finances for August

This summary of recently published data will be an ongoing section for the Economic Review over the coming months as more economic data from Quarter 3 (July to September) 2016 and beyond becomes available. An updated table of forthcoming ONS economic statistics releases and the data periods they cover is at Annex A. Further context for these data is also available at Visual.ONS.

This edition of the Economic Review also provides further commentary and analysis of:

- the latest estimate of gross domestic product (Quarterly National Accounts) for Quarter 2 (Apr to June) 2016

- trends in investment (gross fixed capital formation (GFCF))

- a summary of the effects of changes in sterling on prices

- an analysis of 2015 Annual Survey Hours and Earnings (ASHE) data by region

4. Summary of ONS data covering the post-referendum period

In response to a clear user need to closely monitor official data covering the immediate post-referendum period and the economy, we have recently produced 2 summary documents:

- Assessment of the UK post-referendum economy, published on 21 September, and

- an updated table of forthcoming ONS releases which provides information on the current picture for each release, its economic context and trends to consider in the data going forward; this is published on Visual.ONS and was updated on 23 September

The assessment of the UK post-referendum economy concluded that although the picture is still emerging, there has been no major collapse in confidence and within the data that is available there are indications of continued momentum in the economy.

This has since been confirmed by the Index of Services for July which shows month-on-month growth of 0.4%. This can be interpreted as further evidence that the economy has not shown any immediate signs of major negative effects following the EU referendum decision.

This section summarises the main points from this month’s economic releases which cover data reference periods in July and August. Other important releases this month include current estimates for Quarter 2 (April to June) of GDP, and investment. These are covered elsewhere in the Economic Review. Annex A provides a timetable of forthcoming releases and their data periods.

GDP (Quarter 2 April to June)

The Quarterly National Accounts (QNA) indicated that the UK economy grew by 0.7% in the second quarter of 2016 and by 2.1% when compared with the same quarter of the previous year. This represents a 0.1 percentage point upward revision to the quarter-on-quarter growth rate but a 0.1 percentage point downward revision for growth compared with the previous year. The contrasting directions of the revisions to growth rates are due to the incorporation of further data and the results of an annual seasonal adjustment review. More information is included in the Quarterly National Accounts publication released on 30 September.

Index of Services (July)

The Index of Services (IoS) provides a short-term indicator on the services sector performance which accounts for nearly 79% of total economic activity and has been driving economic recovery since 2009.

In July 2016, the IoS grew 0.4% on the month and by 2.9% compared with July 2015.

All of the 4 main components of the services industries increased in the most recent month compared with the same month a year ago.

The monthly growth in services between June 2016 and July 2016 of 0.4% follows growth of 0.3% between May 2016 and June 2016, which is revised up 0.1 percentage points from the previous estimate.

In terms of annual growth, the Index of Services increased by 2.9% in July 2016 compared with July 2015 driven by the following components, in order of their contribution to growth:

- business services and finance increased by 2.6%

- distribution, hotels and restaurants increased by 4.5%

- transport, storage and communication increased by 4.1%

- government and other services increased by 1.9%

Looking at growth to Quarter 2 (April to June), total services grew by 2.7% between 2015 and Quarter 2 2016 and by 0.6% between Quarter 1 (Jan to Mar) 2016 and Quarter 2 2016. This compares with growth rates of 2.1% and 0.7% respectively for the economy as a whole.

Trade (July)

This month’s UK Trade release showed that the deficit on goods and services was £4.5 billion in July 2016, a narrowing of £1.1 billion from June 2016. While the UK’s goods deficit also narrowed by £1.2 billion in July, this is unlikely to reflect improved trading conditions from the depreciation of the pound. Given order and delivery lags, any such impact is likely to take longer to emerge.

Between the 3 months to April 2016 and the 3 months to July 2016, the total trade deficit for goods and services still widened by £5.1 billion to £14.0 billion, driven by an overall widening deficit in goods.

Construction (July)

In July 2016, construction output was estimated to have shown no growth compared with June 2016. Over the year (compared with July 2015), construction output decreased by 1.5%, with falls in all new work, and repair and maintenance of 0.6% and 3.2% respectively. The underlying pattern as suggested by the 3 month on 3 month movement in output in the construction industry decreased by 1.2%, driven mainly by falls in output for private new housing work and new infrastructure.

New orders in the construction industry – projects where tender has been agreed but work has not yet commenced – rose by 8.6% on the quarter in Quarter 2 (April to June) 2016 and by 7.5% compared with Quarter 2 2015. There were increases in the volume of new orders across all the work types in Quarter 2 2016 except infrastructure and private industrial work. New housing orders increased by 25.0% while there was a fall of 17.4% in infrastructure.

There is typically a time lag between orders and output, and conceptual differences between the 2 measures. Therefore, it should not be assumed that improved new orders data will necessarily result in an improved output estimate in the short-term.

Prices (August)

This month’s Consumer Prices Index and Producer Price Index releases cover the calendar month of August 2016.

The Consumer Price Index (CPI) rose by 0.6% in the year to August 2016, unchanged from July. The rate is still relatively low in the historic context although it is above the rates experienced in 2015 and early 2016. The main upward contributors were rising food prices and air fares, and a smaller fall in the price of motor fuels compared with a year ago. These upward pressures were offset by falls in hotel accommodation prices, in addition to smaller rises in the prices of alcohol, and clothing and footwear than a year ago.

The Producer Price Index for inputs – The prices of material and fuel purchased by producers rose 7.6% in the year to August 2016, compared with a rise of 4.1% in the year to July 2016. The large rise in the August 12-month rate was mainly as a result of a large fall in the index in August 2015 which was driven by falling prices for crude oil. Significant upward pressure on imported input prices was also reported coinciding with the sharp falls in sterling seen at the end of June, into July and August.

Factory gate prices (output prices) for goods produced by UK manufacturers rose 0.8% in the year to August 2016, compared with a rise of 0.3% in the year to July 2016. This suggests the higher input and import prices have not immediately been passed through to higher output. This should be put in the context of historic evidence that output prices have been more stable than import and input prices.

House Price Index (July) - Average house prices in the UK have increased by 8.3% in the year to July 2016 (down from 9.7% in the year to June 2016), continuing the strong growth seen since the end of 2013.

Retail sales (August)

The reporting period for this month’s retail sales release covers a 4 week period from 31 July to 27 August 2016. In August 2016, the volume of retail sales is estimated to have increased by 6.2% compared with August 2015. All store types except textiles, clothing and footwear, and household goods showed growth with the main contribution coming from food stores.

The volume of retail sales decreased by 0.2% compared with July 2016 but 3 month on 3 month growth was 1.6%, suggesting the underlying pattern in the retail sector is still one of growth.

Public sector finances (August)

The data presented in this month’s Public sector finances bulletin presents the latest fiscal position of the public sector at 31 August 2016 and so includes 2 months of post-EU referendum data. However, estimates for the latest period always contain a substantial forecast element and so any post-referendum impact may not become clear for some time.

Public sector net borrowing (excluding public sector banks) decreased by £2.1 billion to £8.6 billion over July and August 2016, compared with July and August 2015.

Public sector net debt, excluding public sector banks was 83.6% of GDP at the end of August 2016, down from 84.3% at the end of June 2016.

Central government tax revenues (including National Insurance contributions) were £106.0 billion over July and August 2016, £5.0 billion higher than in July and August 2015. Of this revenue, stamp duty on land and property was £2.1 billion over July and August 2016, an increase of £0.1 billion from July and August 2015.

Labour market (May, June, July and some data for August)

While the majority of the labour market release covered the 3 months to July, it also included August data for the claimant count and vacancies.

For the 3 months to July 2016, the employment rate (the proportion of people aged from 16 to 64 who were in work) was 74.5%, the joint highest since comparable records began in 1971. The unemployment rate was 4.9%, down from 5.5% for a year earlier. The last time it was lower was in the July to September 2005 period. There were 752,000 job vacancies for June to August 2016. This was little changed (up 3,000) compared with March to May 2016 and up slightly (9,000) compared with a year earlier.

For August 2016, there were 771,000 people claiming unemployment-related benefits. This was 2,400 more than July 2016 but 21,300 fewer than a year earlier.

Back to table of contents5. GDP Quarterly National Accounts

The Quarterly National Accounts (QNA) – which contains revisions covering the period back to Quarter 1 (Jan to Mar) 2015 - indicated that the UK economy grew by 0.7% in the second quarter of 2016, and by 2.1% when compared with the same quarter of the previous year.

Figure 1 shows that the revisions to GDP growth have been upward in Quarter 2 (Apr to June) 2015 and Quarter 2 2016 but downward in Quarter 3 (July to Sept) 2015, so that the broad picture of economic growth in recent quarters remains similar to the previously published GDP growth path. Taken together, these changes mean that UK GDP is estimated to have been 2.6% larger in Quarter 2 2016 than in Quarter 1 2015, the same amount as it was in the previously published data.

Figure 1: GDP growth: Quarterly National Accounts compared with previously published, quarter on same quarter a year earlier, 2014 to 2016, UK

UK, Chained volume measure, seasonally adjusted

Source: Office for National Statistics

Download this chart Figure 1: GDP growth: Quarterly National Accounts compared with previously published, quarter on same quarter a year earlier, 2014 to 2016, UK

Image .csv .xlsThe QNA provides much greater information on the expenditure and income measures of GDP compared with the second estimate published in August, as well as information regarding the sector and financial accounts. A breakdown of the expenditure components of GDP growth is shown in Figure 2, and illustrates that GDP growth in the second quarter was driven by household (and Non-Profit Institutions Serving Households (NPISH)) final consumption and gross fixed capital formation (GFCF) - the latter of which was driven by business investment growth - while government consumption made a small positive contribution to growth. This is broadly consistent with the contributions that expenditure components have made to GDP over the last few years.

Net exports pulled down GDP growth by 0.6 percentage points on a quarter on year basis, and by 1.0 percentage point for quarter-on-quarter growth. Net exports have exerted a modest drag on GDP growth since the economic downturn, albeit with some volatility during this time.

Figure 2: Contributions to GDP growth, expenditure components, quarter on same quarter of previous year

UK, chain volume measure

Source: Office for National Statistics

Notes:

- GDP Components may not sum due to rounding.

- HHFCE refers to Household Final Consumption Expenditure.

- NPISH refers to Non-Profit Institutions Serving Households.

- GFCF refers to Gross Fixed Capital Formation.

- Other includes changes in inventories including alignment adjstument, acquisitions less disposables of valuations, and net transfers.

- Q1 is Quarter 1 (Jan to Mar), Q2 is Quarter 2 (Apr to June), Q3 is Quarter 3 (July to Sept) and Q4 is Quarter 4 (Oct to Dec).

Download this chart Figure 2: Contributions to GDP growth, expenditure components, quarter on same quarter of previous year

Image .csv .xlsIncome measure of GDP

The QNA also provides detail on the income measure of GDP. Figure 3 shows that the main drivers of GDP growth in nominal terms were from growth in compensation of employees – total gross (pre-tax) wages paid by employers to employees for work - and "other income" (including mixed income, a measure of the income and profits generated from the self-employed). The consistent contribution from compensation of employees (COE) in recent quarters echoes the contribution from household consumption to the expenditure measure of GDP.

The contributions to the income measure of GDP also highlight the different performance of the financial and non-financial sectors, with the latter contributing more positively and on a more consistent basis. This is consistent with the relative performances of industry output: in Quarter 2 2016, output of total services industries was 11.3% above pre-downturn levels while the financial industry remained 10.4% below pre-downturn levels.

Figure 3: Contributions to GDP growth, income components, quarter on same quarter of previous year, current prices

UK

Source: Office for National Statistics

Notes:

- FC GOS refers to Financial Corporation Gross Operating Surplus.

- NFC GOS Ex refers to Non-Financial Corporation Gross Operating Surplus, and covers both private and public corporations.

- CoE refers to Compensation of Employees.

- Q1 is Quarter 1 (Jan to Mar), Q2 is Quarter 2 (Apr to June), Q3 is Quarter 3 (July to Sept) and Q4 is Quarter 4 (Oct to Dec).

Download this chart Figure 3: Contributions to GDP growth, income components, quarter on same quarter of previous year, current prices

Image .csv .xls6. Investment

Commentators have focused on business confidence and its implications for business investment as a primary channel that could be affected by the EU referendum result. At present we do not have the data to assess investment performance post-referendum, as the latest gross fixed capital formation (GFCF) data only covers the period up to June. However, assessing the latest data in Quarter 2 (Apr to June) can help us understand whether uncertainty had any effects in the run-up to the referendum.

GFCF grew by 1.6% in Quarter 2 2016 which was the first quarter of positive growth since Quarter 3 (July to Sept) 2015 and the highest growth rate since Quarter 1 (Jan to Mar) 2015.

By asset, Figure 4 shows that the main contributor to the growth in GFCF in Quarter 2 was from transport equipment investment – with the Quarterly Capital Acquisitions Survey (QCAS) showing strong acquisitions from the private sector.

Transport investment made a similar contribution to GFCF in Quarter 1 but then it was offset by falls in investment in information and communications technology (ICT) equipment and other machinery and equipment and falls in other buildings and structures and transfer costs. Growth in buildings in Quarter 2 was driven by government investment expenditure.

Overall investment growth in Quarter 2 2016 was therefore broadly in line with that recorded during most of 2014 and early 2015.

Figure 4: Contribution to GFCF growth, quarter on previous quarter, 2014 Q1 to 2016 Q2

UK

Source: Office of National Statistics

Download this chart Figure 4: Contribution to GFCF growth, quarter on previous quarter, 2014 Q1 to 2016 Q2

Image .csv .xlsLonger term context

Figure 5 presents average compound growth rates of the main GDP expenditure components at 3 different stages:

- the 7 years prior to the downturn

- the downturn period of Quarter 1 2008 to Quarter 2 2009

- growth since the start of the economic recovery in Quarter 3 2009

This shows that GFCF was the most pro-cyclical GDP component, contracting the fastest at a compound average growth rate of 4.8% per quarter during the economic downturn. Trade volumes, both on the imports and exports side, also fell during the downturn, but have since recovered quite strongly since Quarter 3 2009. GFCF has since recovered strongly, surpassing pre-downturn rates of growth, while household consumption has grown at lower rates.

Figure 5: Compound quarterly average growth rates of GDP and the main expenditure components prior to the downturn, during the downturn and following the downturn

UK

Source: Office of National Statistics

Notes:

- GDP Components may not sum due to rounding.

- Economic downturn (Q1 2008 to Q2 2009).

- Downturn (Q1 2008 to Q2 2009).

- Following the downturn (Q3 2009 to Q2 2016).

- Quarterly average growth rates are geometric means.

Download this chart Figure 5: Compound quarterly average growth rates of GDP and the main expenditure components prior to the downturn, during the downturn and following the downturn

Image .csv .xlsGFCF by sector

The stronger growth in GFCF following the downturn masks differences in investment growth by sector (Figure 6). Prior to the downturn (Quarter 1 2001 to Quarter 1 2008) general government investment was growing at a faster rate (2.4% per quarter) than growth of investment from the private business sector (0.3% per quarter).

During the economy’s downturn (Quarter 1 2008 to Quarter 2 2009) all the main sectors except general government contracted, with private sector dwellings having the largest contraction. This coincided with over 40% contraction in private new housing construction. Following the downturn (Quarter 3 2009 to Quarter 2 2016) it has been the private business sector which has been driving growth while growth in government sector investment has been subdued. This coincided with the more than doubling of construction of private new housing as well as improvements in lending conditions and business confidence.

Figure 6: Compound quarterly average growth rates of GFCF’s investment sectors prior to the downturn, during the downturn and following the downturn

UK

Source: Office of National Statistics

Notes:

- Economic downturn (Q1 2008 to Q2 2009).

- Downturn (Q1 2008 to Q2 2009).

- Following the downturn (Q3 2009 to Q2 2016).

- Quarterly average growth rates are geometric means.

Download this chart Figure 6: Compound quarterly average growth rates of GFCF’s investment sectors prior to the downturn, during the downturn and following the downturn

Image .csv .xlsGFCF by asset

GFCF growth by asset (or the products that institutions are investing in) has also changed comparing the pre- and post-downturn periods. For example, investment in transport equipment has grown strongly post-downturn despite seeing the slowest quarterly growth prior to the downturn (Figure 7).

Figure 7: Compound quarterly average growth rates of GFCF assets prior to the downturn, during the downturn and following the downturn

UK

Source: Office of National Statistics

Notes:

- Economic downturn (Q1 2008 to Q2 2009).

- Downturn (Q1 2008 to Q2 2009).

- Following the downturn (Q3 2009 to Q2 2016).

- Quarterly average growth rates are geometric means.

Download this chart Figure 7: Compound quarterly average growth rates of GFCF assets prior to the downturn, during the downturn and following the downturn

Image .csv .xlsDwellings investment and housing construction

Figure 8 shows that there is some correlation between investment in dwellings and total housing construction although both series are volatile. However, there is some lag before a construction project is logged as investment (only completed construction projects are listed as investment) which may explain the difference in growth rates.

Figure 8: Comparison between the growth rates of total housing construction and investment in dwellings

UK

Source: Office of National Statistics

Notes:

- Q1 = Quarter 1 (Jan to Mar), Q2 = Quarter 2 (Apr to June), Q3 = Quarter 3 (July to Sept) and Q4 = Quarter 4, (Oct to Dec).

Download this chart Figure 8: Comparison between the growth rates of total housing construction and investment in dwellings

Image .csv .xls7. Sterling effects on prices

Following the EU referendum, the value of sterling fell sharply against a basket of currencies at the end of June 2016 and into July. In July, the sterling Exchange Rate Index (ERI) was 6.6% lower compared with the average level in June and 15.0% lower compared with July 2015.

Economic theory suggests the recent depreciation should boost export and manufacturing competitiveness as changes in the value of a country’s currency can, all else equal, make export prices more competitive. For example, if the UK chooses to import everything in dollars and export everything in sterling, a depreciation in sterling would cause UK exports to become more competitive and UK imports to be more expensive. Therefore it would be expected that export prices would fall and import prices would rise when reported in sterling.

Export and import prices

Figures 9a and 9b show the relationship between export prices and import prices for UK and US trade in goods since 1998. From this, it is clear that export prices and import prices follow broadly similar trends in both countries. Further analysis was published in the UK trade: July 2016 publication, which also showed that other countries’ export and import prices were mostly positively correlated. In July 2016, UK export prices increased by 3.6% while import prices increased by 3.2%, compared with June 2016.

A similar rise in export and import prices also occurred during the 2008 to 2009 economic downturn, where there was a depreciation in sterling. Previous analysis by ONS looking at the depreciation of sterling during the 2008 economic downturn can be found on our website.

Figure 9a: UK export prices and import prices, index 2013=100, January 1998 to July 2016

UK Not Seasonally Adjusted

Source: Office of National Statistics

Download this chart Figure 9a: UK export prices and import prices, index 2013=100, January 1998 to July 2016

Image .csv .xls

Figure 9b: US export prices and import prices for trade in goods, January 1998 to July 2016

US, Not Seasonally Adjusted

Source: Bureau of Labor Statistics

Download this chart Figure 9b: US export prices and import prices for trade in goods, January 1998 to July 2016

Image .csv .xlsIt is important to note that both export and import prices are based in sterling for the UK. This means that while export prices on a sterling basis have risen, there may have been no change in the price in the importer’s currency. Consideration of the underlying survey data suggests that if price growth is calculated in the currency prices are reported in, then there has been no increase in export prices in July 2016. It is only when prices reported in foreign currency are converted to sterling that there is an increase in price, due to the depreciation of sterling following the EU referendum.

Producer and consumer prices

Additional analysis of the Producer Price Index (PPI) and Consumer Prices Index (CPI): Aug 2016 examined the effect of sterling on producer prices. Figure 10 shows the contribution of the main components of PPI input prices to the annual growth rate, including imports which may be affected by changes in the sterling exchange rate. PPI input prices increased 7.6% in the year to August 2016, up from 4.1% in the year to July 2016, although this has been following an upward trend since August 2015. This is suggestive of longer-term economic pressures, rather than this being caused only by the depreciation of sterling.

Figure 10: Contributions to the 12-month rate of input producer price inflation by component and overall input PPI rate, August 2014 to August 2016

UK

Source: Office of National Statistics

Download this chart Figure 10: Contributions to the 12-month rate of input producer price inflation by component and overall input PPI rate, August 2014 to August 2016

Image .csv .xlsThe recent recovery of oil prices has been a major factor in the upward trend in input producer price inflation, as seen in Figure 10, particularly when the long-running negative impact began to ease off from August 2015 onwards, contributing to the gradual rise of the input PPI inflation rate. This contribution turned positive in August 2016, which may have been a consequence of the depreciation of sterling increasing the price of imported oil.

Figure 10 also provides evidence of the positive contribution to input PPI by imports since May 2016. In particular the positive contribution from imports to the input PPI in July and August 2016 may be related to the depreciation of sterling.

Sterling appears to have had a greater impact on PPI input prices than on PPI output prices in July and August 2016, as PPI output prices increased 0.8% in the year to August 2016 compared with 0.3% in the year to July 2016. This suggests that, for example, the increase in crude oil prices (affecting input prices) has yet to feed into refined petroleum products (including duty) which affect output prices. It is likely UK producers have not passed on all of the increase in input prices to their customers, and that latent pressures on output prices may later emerge.

The difference between output price and export price growth may be explained by the depreciation of sterling. As previously mentioned, export prices recorded in foreign currencies are converted into sterling, so even if the actual price shows no change, on a sterling basis there will be an increase in price.

Transactions by currency unit

Another factor that affects export and import prices is the currency that the price is reported in. For example, if a UK firm provides information that it imports goods in sterling, it will not be affected by currency movements, so the price would only change if the exporting firm changes their price.

Figure 11 shows the unweighted shares of transactions of UK exports and imports in the main traded currencies. A greater proportion of UK exports to non-EU countries are denominated in sterling compared with exports to EU countries. In contrast, a greater proportion of imports to the UK from EU countries are in sterling compared with imports from non-EU countries.

Figure 11: Proportion of export and import transactions completed by currency EU and non-EU, August 2016

UK, Unweighted

Source: Office of National Statistics

Notes:

- Currency shares are unweighted.

Download this chart Figure 11: Proportion of export and import transactions completed by currency EU and non-EU, August 2016

Image .csv .xlsGiven the recent depreciation of sterling and the proportion of transactions conducted in trade with EU and non-EU countries, import and export prices would have been affected to different extents.

As sterling depreciated more against the US dollar than the euro and a larger proportion of import transactions with non-EU countries are conducted in dollars compared with EU countries, this would indicate that prices of imports from non-EU countries would grow faster than prices of imports from EU countries. This was the case in July 2016, as prices of imports rose by 3.9% from non-EU countries and 2.6% from EU countries, compared with June 2016.

However in July 2016, export prices rose at a similar rate from EU (3.7%) and non-EU countries (3.6%). This is likely to be because a larger proportion of export transactions to non-EU countries that were recorded in sterling compared with EU countries. As fewer non-EU exports are affected by the previously mentioned effect of converting the price into sterling than EU exports, this offsets the greater depreciation of sterling against the dollar than the euro. This may explain the similar growth in export prices to the EU and non-EU countries.

Another possible explanation could be that many domestic firms may agree to export goods at a fixed price in the importer’s currency, to maintain client relationships and consistency of orders. If a UK firm agrees to do this, the price of the export on a sterling basis would rise as the currency depreciates.

It is also important to note that the proportions of transactions in Figure 11 are unweighted. This means it does not take into account the monetary value of different transactions. Therefore a large transaction would have a much larger effect on prices than several small transactions. For example, if there was a large transaction recorded in US dollars for exports to non-EU countries, this may have a greater effect than several small transactions recorded in sterling.

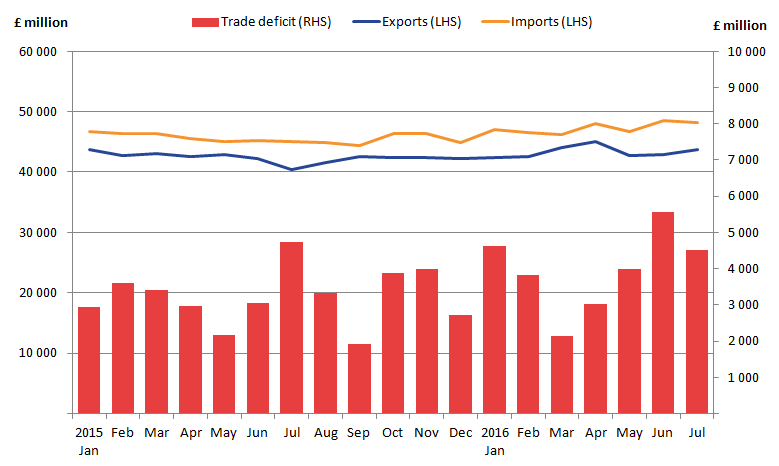

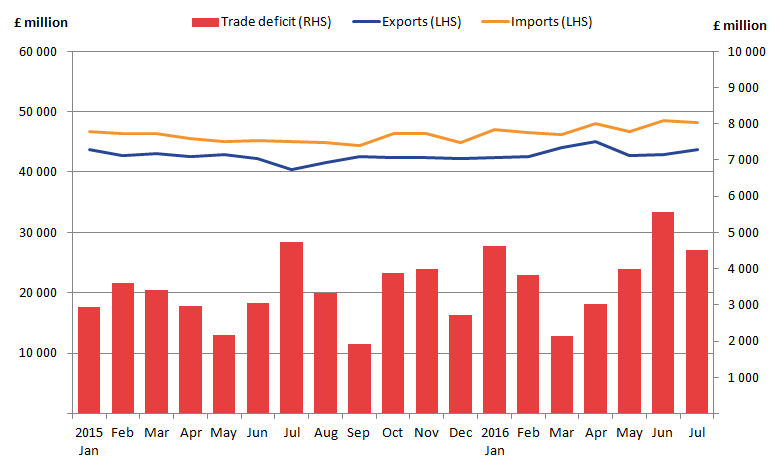

Balance of payments

Figure 12 shows that in July 2016, the UK’s trade deficit fell £1.1 billion from £4.5 billion in June 2016. The value of exports increased by £0.8 billion while imports fell by £0.3 billion, most of which came from trade in goods. However, this narrowing of the trade deficit is unlikely to reflect improved trading conditions from the depreciation of sterling. Theoretically, given order and delivery lags, any such impact would take longer to emerge.

Figure 12: Value of UK exports, imports and trade deficit Current prices, seasonally adjusted, January 2015 to July 2016

UK

Source: Office of National Statistics

Download this image Figure 12: Value of UK exports, imports and trade deficit Current prices, seasonally adjusted, January 2015 to July 2016

.png (24.7 kB) .xls (28.2 kB){kind=link}

As well as the potential impact on the UK’s balance of trade, the depreciation in sterling is likely to affect other areas of the balance of payments. An article was published by ONS on the impact of recent currency fluctuations on foreign direct investment statistics: Apr to June 2016.

The depreciation in sterling has had an impact on the UK’s net international investment position. Assets and liabilities are valued at the end of each quarter, therefore as the end of Quarter 2 (April to June) 2016 and therefore after the EU referendum – and after the sharp depreciation in sterling – some stocks valued in foreign currency have increased in value. As well as this, changes in the price of financial instruments can also affect their value. An explanation of the transactions affected are summarised in the Balance of Payments for the UK: Apr to June 2016.

Figure 13 shows the net international investment position of the UK. The net international investment position has improved since the end of 2015. This may partially be attributable to the gradual depreciation of sterling since mid-2015.

Figure 13: Contributions to the net international investment position, non-seasonally adjusted, current prices, 2011 to 2016 Quarter 2

UK

Source: Office of National Statistics

Download this chart Figure 13: Contributions to the net international investment position, non-seasonally adjusted, current prices, 2011 to 2016 Quarter 2

Image .csv .xlsNet direct investment was on a downward trend from 2011 onwards, largely driven by an increase in foreign holdings of UK liabilities. Analysis of foreign direct investment was published in the Economic review: September 2016. In the first half of 2016, net direct investment holdings have increased, which has mainly been due to a fall in the value of UK liabilities, as well as a small increase in the value of UK assets.

Net other investment, which in previous years had provided a relatively large negative contribution to the net international investment position, also increased from the end of 2015. This includes transactions such as deposits and loans, some of which may be recorded in a foreign currency. The increase of other investment assets into Quarter 2 2016 may be partly attributable to the depreciation in sterling. For example, deposits held in a foreign currency, will now have increased in value on a sterling basis.

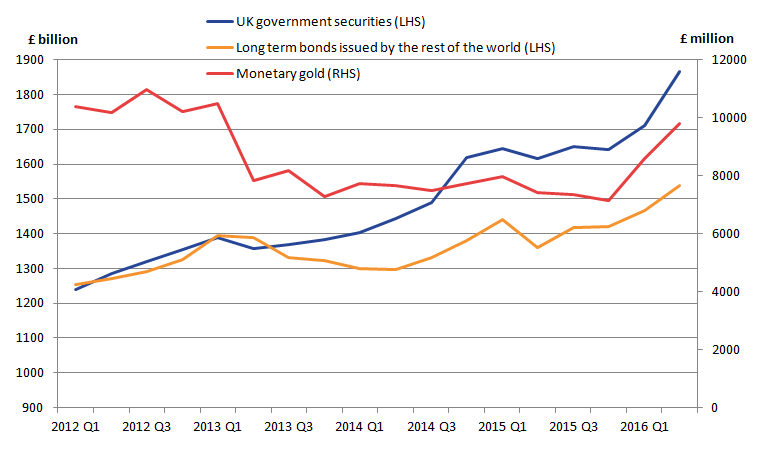

Offsetting these positive contributions, net portfolio investment made an increased downward contribution to the net international investment position in Quarter 2 2016. The majority of the fall in the net portfolio investment position came from debt securities. Debt securities (especially government bonds) and certain commodities such as gold are often seen as safer investments, so in times of uncertainty, demand for these rises which increases their value.

Figure 14 shows UK government securities (UK liabilities) and the UK holdings of monetary gold and long-term bonds issued by the rest of the world (UK assets). All series show an increase in value in 2016, with both debt securities series increasing at a faster rate in Quarter 2 2016. The increasing values of UK debt security assets and liabilities, as well as monetary gold may be a result of greater demand for relatively safe investments in the lead-up to and the period immediately after the EU referendum.

Figure 14: UK government securities, UK holdings of monetary gold and long term bonds issued by the rest of the world non-seasonally adjusted, current prices

UK

Source: Office of National Statistics

Download this image Figure 14: UK government securities, UK holdings of monetary gold and long term bonds issued by the rest of the world non-seasonally adjusted, current prices

.png (19.5 kB) .xls (28.7 kB){kind=link}

The UK has been a net seller of foreign bonds in recent quarters, however, the currency movements and change in valuation of these bonds in the latest quarter mean that the value of UK stocks of foreign bonds increased in value. Part of this increase in the value of foreign bonds may be a result of demand from central banks through expansionary monetary policy in areas such as Japan and the eurozone.

While it is too soon to see an impact of the EU referendum on many ONS statistics, the analysis above provides some evidence that the depreciation in sterling has had an effect in certain areas:

- producer input prices are rising and this may lead producer output prices to increase in the future in the absence of factors which may offset this cost pressure such as improved productivity or the ability to squeeze margins

- there is some evidence of investors moving into safer assets, possibly out of currency holdings as a result of the sterling depreciation

8. Analysis of earnings by region

The rate of recovery in the labour market has been stark compared with both historical and international experience. Some commentators have attributed the rapid improvement in employment immediately following the economic downturn to a relative weakness in real earnings growth that accompanied this. However, earnings growth has now been running consistently at around 2.0% per year since the end of 2014, coinciding with lower inflation to result in rising real incomes.

As with a wide range of our releases, the average figure can mask a vastly different distribution of earnings in both levels and growth terms. One way to examine this is to use the Annual Survey of Hours and Earnings (ASHE). Currently data is available for 2015. Provisional estimates for 2016 will be available on 26 October 2016.

Previous analysis has highlighted changes in the UK earnings distribution since 1997. At a UK level, in 1997, before the National Minimum Wage (NMW) was introduced, the UK’s earnings distribution was relatively smooth; it was positively skewed and centred on hourly earnings between £4 and £5 per hour. Relatively few jobs paid below £3 per hour, with the number of jobs steadily falling as hourly earnings rose. Mean hourly pay was around 24.2% above the median in 1997. However, by 2015 the earlier smooth profile had been replaced by a striking, sharply-edged distribution, with a mass at around £6.50 per hour – the prevailing adult NMW in April 2015.

Regional differences in earnings distribution

When looking across all regions, the NMW has had a similar, major impact on the earnings distribution.

Looking at the regional breakdown of the levels data for 2015 (Figures 15a and b) each region shows the clear spike between £6 and £7 representing the minimum wage. However, London has a smaller minimum wage spike and a greater proportion of people on higher hourly wages compared with the other regions. Those earning the highest salaries (£30 and over per hour) tend to be concentrated in London and the South East, while Wales, Northern Ireland and North East England have fewer people on these salaries.

Figure 15a: Comparing London with selected regions of England (South East, North East and South West)

Source: Office for National Statistics

Download this chart Figure 15a: Comparing London with selected regions of England (South East, North East and South West)

Image .csv .xls

Figure 15b: Comparing Northern Ireland, Scotland, and Wales

Source: Office for National Statistics

Download this chart Figure 15b: Comparing Northern Ireland, Scotland, and Wales

Image .csv .xlsSex

Looking at men and women, women have a larger minimum wage spike in each region, reflecting the greater proportion of women working in lower-paid jobs than men (Figures 16a and b). This is especially true within the North East region of England and in Northern Ireland. London and the South East were the top 2 highest paying regions for both men and women in 2015. Northern Ireland has the largest concentration of both male and female workers at the minimum wage in 2015. By contrast, London displays the most equal distribution of wages between the sexes.

Figure 16a: Earnings distribution by gender, London, 2015

Source: Office for National Statistics

Download this chart Figure 16a: Earnings distribution by gender, London, 2015

Image .csv .xls

Figure 16b: Earnings distribution by gender, Northern Ireland, 2015

Source: Office for National Statistics

Download this chart Figure 16b: Earnings distribution by gender, Northern Ireland, 2015

Image .csv .xlsGrowth of earnings

While a large gap exists between the earnings distribution of people in London compared with other regions, there were also differences in the growth in earnings across the regions in 2015. If these differences in earnings growth persist and the effects of entry and exit and composition of the labour market remain relatively unchanged across the regions, this may give an indication of whether overall pay differences are likely to increase or decrease in the future.

Figure 17 shows the distribution of nominal weekly earnings growth within selected regions of the UK for 2015. For each growth rate on the horizontal axis, the figure indicates the frequency of employees who experienced earnings growth within 0.5 percentage points of that rate. Looking at the growth rates of earnings for 2015, there are 2 peaks clustered around zero growth and around 2 to 3% growth.

Northern Ireland has the highest proportion of people receiving between negative 1% and zero % growth in earnings. More people in Scotland received no pay rise compared with London. Also more people received a pay rise between 2 to 3% in London compared with Scotland and Northern Ireland. If these trends persist, this means that the pay gap between London, and Scotland and Northern Ireland is likely to exacerbate in the future.

Figure 17: Growth of earnings for the continuously employed, selected regions, 2015

UK

Source: Office for National Statistics

Notes:

- This chart uses individual level data from ASHE to calculate the growth of nominal weekly earnings for individuals observed in 2014 to 2015. Note that the ASHE methodology is not specifically designed to model earnings growth for individuals over time.

Download this chart Figure 17: Growth of earnings for the continuously employed, selected regions, 2015

Image .csv .xlsWider measures of financial well-being

While the distribution of earnings and growth in earnings using ASHE data shows a range of outcomes across regions, we can also use data on the costs of living and wider measures of financial well-being to provide some insight into how people feel about their finances.

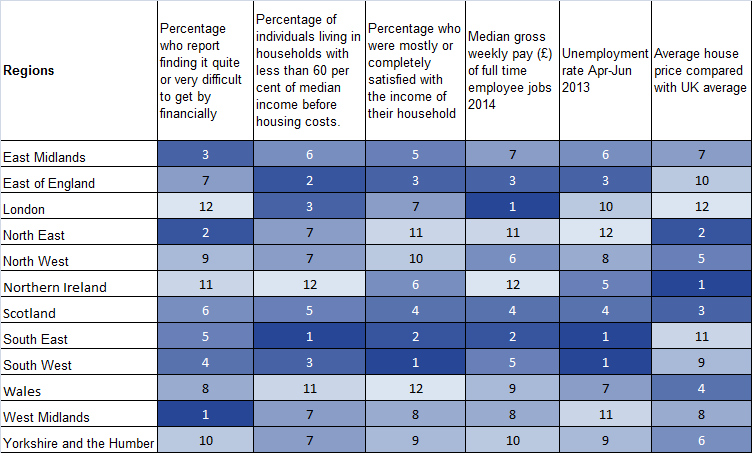

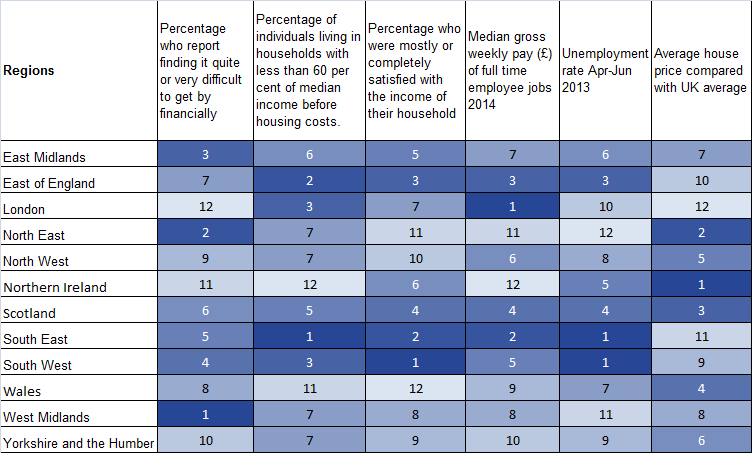

Table 1 shows regional rankings of earnings, unemployment and personal financial well-being measures in order to compare UK regions in the financial year from April 2013 to March 2014. This period is the latest on which comparable data is available1. A score of 1 represents the best outcome for that dataset and a score of 12 the worst outcome. Also using a graded colour scheme - a darker shade means a better score on that question (higher employment, higher income and so on) while moving to a lighter shade is a worse score. The lower the rank a region has, broadly the better it compares with other regions.

Table 1: Ranking comparison of earnings, house prices, employment and personal finance wellbeing measures, 2013-14

UK region

Source: ONS, DWP, and Understanding Society the UK Household Longitudinal Study

Notes:

- Column 1: UK regions according to the UK NUTS 1 classification.

- Column 2: source: Understanding Society the UK Household Longitudinal Study.

- Column 3: Family Resources Survey, Department for Work and Pensions. The figures here are three-year averages for 2012-13 to 2014-15.

- Column 4: source: Understanding Society the UK Household Longitudinal Study.

- Column 5: source: ASHE 2014 revised dataset, ONS. These estimates are all estimated with a coefficient of variation less than or equal to 5% so are considered precise. The estimates do not cover the self employed, people not paid in the period and are all from full-time employees.

- Column 6: source: ONS, UK Labour market.

- Column 7: source: ONS, House Price Index.

- For full details on personal finance well-being measures (columns 2, 3 and 4) see Measuring national well-being in the UK, domains and measures: Sept 2016.

- A rank of 1 represents the best outcome and 12 the lowest outcome.

Download this image Table 1: Ranking comparison of earnings, house prices, employment and personal finance wellbeing measures, 2013-14

.png (32.6 kB){kind=link}

Using data from Understanding Society: the UK Household Longitudinal Study we find that the proportion of families mostly or completely satisfied with their finances (column 4) broadly follows the pattern of earnings across the regions, with the South East and South scoring well and Wales and the North East scoring near the bottom. However, London is only mid-table on this measure, despite having the highest average earnings.

Living costs

Particularly important for London is the average house price which is a main element of living costs in the region. London had the highest average house price2 rank of all UK regions in the 2013 to 2014 financial year at approximately £340,000. This was close to double the UK average house price in April 2013 to March 2014 at £175,000. The next most expensive region was the South East where the average price was £235,000 in the same period, a large gap from London prices.

Similar information on living costs from the Index of Private Housing Rental Prices3 shows that over the same period London also saw the largest increase in private rental prices at 2.2%. Between March 2013 and March 2014, private rental prices in Great Britain grew by 1.0%. Rental prices for Great Britain excluding London grew by 0.7% in the same period4.

As well as these high costs of living, London reported the third highest unemployment rate of the regions in April to June 2013 and ranked tenth on that measure.

Finding it difficult to get by financially

Taking these factors together, London ranked the worst of the UK regions for the percentage of people “finding it quite or very difficult to get by financially” (column 2).

In contrast, the West Midlands and North East ranked among the lowest for the percentage of people “finding it quite or very difficult to get by financially” in the financial year to March 2014 despite performing poorly in other measures in the table such as average gross weekly earnings and unemployment rates.

This illustrates that a wide combination of factors affect how people feel about their financial situation and regional differences can be marked.

Conclusion

This section has illustrated that there are regional differences in the earnings distribution across the UK, although all regions have seen an effect of introduction of the National Minimum Wage through a greater concentration of workers receiving this level of hourly wage in 2015 compared with 1997.

London shows a more equal distribution of hourly earnings between sexes than some other regions, but there are still more men than women receiving higher hourly wages in London.

Growth in earnings of the continuously employed also differ across regions, with more workers in London receiving 2 to 3% pay increases in 2015 compared with other regions.

However, more households in London report finding it difficult to get by financially than other regions, which may be partly due to higher costs of living and higher unemployment rates than other parts of the UK.

Notes for Analysis of earnings by region

Unemployment changes from April to June 2013 to January to March 2014 in the regions do not significantly affect the overall ranking of the regions in unemployment rate so April to June 2013 is used as a representative period.

Calculation method: the average house price column uses the regional average house price to calculate a mean over the financial year to March 2014. This regional mean is then compared with UK mean of average UK house price over the same period to create a regional rank.

See ONS guidance on experimental releases and the index of private housing rental prices release notes.

4.This difference is due to the higher inflation in rental prices experiences in London when compared with the rest of Great Britain and its large weight in the Great Britain index. The large weight that London has in the overall index reflects its high average rental prices and its large volume of private rented property.

Back to table of contents9. Annex A – Dates of our upcoming releases

Users have been in contact with us to ask when any impact from the recent EU referendum could feed through to our economic statistics. Below we set out the release dates from our main economic indicators and the data periods they cover. Some economic context and trends to consider for these forthcoming releases has been provided at Visual.ONS.

Table 2: Dates of upcoming ONS releases

| Date | Indicator | Details | Date of following release |

| 06/10/2016 | UK Productivity, Quarter 2 | While this release covers up to 30 June, the vast majority of the period was before the referendum | 6/1/2017 (provisional) : provides data for Quarter 3 2016 |

| 07/10/2016 | UK Trade, August | The second trade release including an entirely post-referendum period | 9/11/2016: provides data for September |

| 07/10/2016 | Index of Production, August 2016 | Provides data for August | 8/11/2016: provides data for September |

| 13/10/2016 | Overseas travel and tourism provisional, Quarter 2 | While these quarterly data cover up to 30 June, the vast majority of the period was before the referendum | 19/1/2017 (provisional) : provides data for Quarter 3 2016 |

| 14/10/2016 | Output in the Construction Industry, August | Provides data for August | 11/11/2016 : provides data for September |

| 18/10/2016 | Consumer Price Index 2016, September | Provides data for September | 15/11/2016: provides data for October |

| 18/10/2016 | Producer Prices, September 2016 | Provides data for September | 11/11/2016 : provides data for September |

| 18/10/2016 | UK House Price index, August | Provides data for August | 11/11/2016 : provides data for September |

| 19/10/2016 | Labour Market Statistics, October | Includes Labour Force Survey data for June, July and August. | 16/11/2016: provides data for Q3 July, August and September |

| 20/10/2016 | Retail Sales, September | Provides data for September | 17/11/2016: provides data for September |

| 21/10/2016 | Public Sector Finances, September 2016 | Provides data for September | 22/11/2016: provides data for October |

| 21/10/2016 | Overseas Travel and Tourism, provisional monthly results August | Provides data for August | 18/11/2016: provides data for September |

| 27/10/2016 | Index of Services, August | The second services release including an entirely post-referendum period | 25/11/2016: provides data for September |

| 27/10/2016 | GDP preliminary estimate, Quarter 3 | The first GDP release including an entirely post-referendum period July to September | 26/01/2017: provides preliminaty estimate for Quarter 4 2016 |

| 08/11/2016 | Index of Production, September 2016 | Provides data for September | 7/12/2016: provides data for October |

| 09/11/2016 | UK Trade, September | Provides data for September | 9/12/2016: provides data for October |

| 11/11/2016 | Construction output, September and July to September, Quarter 3 | Provides data on construction output for first full quarter following the referendum | 9/12/2016: provides data for output for October and new orders quarter 3 2016 |

| 15/11/2016 | Consumer Price Index 2016, October | Provides data for October | 13/12/2016: provides data for November |

| 15/11/2016 | Producer Prices, October 2016 | Provides data for October | 13/12/2016: provides data for November |

| 15/11/2016 | UK House Price index, September | Provides data for September | 13/12/2016: provides data for October |

| 16/11/2016 | Labour Market Statistics, November | Includes Labour Force Survey data for July, August and September. The first unemployment release including an entirely post-referendum period. This release also includes Quarter 3 data of country of birth and nationality. | 14/12/2016: Provides data for August, September and October. |

| 17/11/2016 | Retail Sales, October | Provides data for October | 15/12/2016: provides data for November |

| 18/11/2016 | Overseas travel and tourism provisional, monthly September 2016 | Provides data for September | 19/1/2017 (provisional) : provides data for Quarter 3 2016 |

| 22/11/2016 | Public Sector Finances, October 2016 | Provides data for October | 21/12/2016: provides data for November |

| 25/11/2016 | GDP 2nd estimate, Quarter 3 | The first GDP release, including output, income and expenditure data including an entirely post-referendum period | 23/02/2017: Provides data for 2nd estimate of GDP Quarter 4 2016 |

| 25/11/2016 | Business Investment preliminary estimate, Quarter 3 | The first investment release including an entirely post-referendum period | 23/02/2017: provide data for Quarter 4 2016 |

| 25/11/2016 | Index of Services, September | Provides data for September | 23/12/2016: provides data for October |

| 01/12/2016 | Migration in the UK, December | While this includes IPS estimates up to 30 June, the vast majority of the period was before the referendum. | 23/02/2017: provides data up to 30 September 2016 |

| 02/12/2016 | Foreign Direct Investment, 2015. | The annual FDI publication includes data up to 31 December 2015, the entire period was before the referendum – | December 2017 - provides results for 2016, where half of the period would be before the referendum. |

| 23/12/2016 | Index of Services, October | Provides data for October | 26/1/2017: provides data for November |

| 23/12/2016 | Balance of Payments, Quarter 3 | The first Balance of Payments figures folowing the referendum | 31/3/2017: provides data for Quarter 4 2016 |

| 23/12/2016 | Quarterly National Accounts, Quarter 3 | Provides data for quarter 3 | 31/3/2017: provides data for Quarter 4 2016 |

| 23/12/2016 | Consumer Trends, Quarter 3 | Provides data for quarter 3 | 31/3/2017: provides data for Quarter 4 2016 |

| 23/12/2016 | Business Investment revised, quarter 3 | Provides data for quarter 3 | 23/2/2017: provides provisional data for Quarter 4 2016 |

| 23/12/2016 | Economic Well-being, Quarter 2 | Provides data for quarter 3 | 31/3/2017: provides data for Quarter 4 2016 |

| December (exact data to be confirmed) | Investment by insurance companies, pension funds and trusts in the UK (MQ5): Quarter 3 (July to September) 2016 | The first MQ5 release including an entirely post-referendum period | March 2017 (provisional) : provides data for Quarter 4 2016 |

| 23/02/2017 | Migration in the UK, February | While this includes IPS estimates up to 30 September, most of the period was before the referendum | 25/05/2017: provides data up to 31 December 2016. Half of this period was before the referendum |

| Source: Office for National Statistics | |||

Download this table Table 2: Dates of upcoming ONS releases

.xls (33.8 kB)10. Demand and supply indicators

Table 3: UK demand side indicators

| 2014 | 2015 | 2015 | 2016 | 2016 | 2016 | 2016 | 2016 | 2016 | 2016 | |

| Q4 | Q1 | Q2 | Apr | May | Jun | Jul | Aug | |||

| GDP | 3.1 | 2.2 | 0.7 | 0.4 | 0.7 | |||||

| Index of Services | ||||||||||

| All Services1 | 3.3 | 2.5 | 0.9 | 0.7 | 0.6 | 0.6 | 0.0 | 0.3 | 0.4 | .. |

| Business Services & Finance1 | 3.9 | 2.6 | 0.7 | 0.7 | 0.6 | 0.5 | -0.1 | 0.3 | 0.3 | .. |

| Government & Other1 | 1.7 | 0.5 | 0.8 | 0.5 | 0.1 | 0.0 | 0.2 | 0.2 | 0.2 | .. |

| Distribution, Hotels & Rest1 | 4.8 | 4.6 | 1.5 | 1.4 | 1.1 | 0.7 | 0.4 | 0.1 | 0.0 | .. |

| Transport,Stor. & Comms1 | 3.0 | 3.8 | 1.2 | 0.0 | 0.6 | 1.8 | -0.5 | 0.9 | 1.6 | .. |

| Index of Production | ||||||||||

| All Production1 | 1.5 | 1.3 | -0.4 | -0.1 | 2.1 | 2.3 | -0.7 | 0.0 | 0.1 | .. |

| Manufacturing1 | 2.9 | -0.1 | 0.1 | -0.3 | 1.6 | 2.3 | -0.7 | -0.2 | -0.9 | .. |

| Mining & Quarrying1 | 0.6 | 8.5 | -2.2 | -1.2 | 2.8 | 1.3 | -0.5 | 1.6 | 4.7 | .. |

| Construction1 | 8.0 | 4.9 | 0.6 | 0.8 | -0.1 | 2.8 | -1.6 | -1.0 | 0.0 | .. |

| Retail Sales Index | ||||||||||

| All Retailing1 | 3.9 | 4.4 | 1.1 | 1.2 | 1.6 | 1.7 | 0.9 | -0.8 | 1.9 | -0.2 |

| All Retailing excl Fuel1 | 4.2 | 4.0 | 0.6 | 1.2 | 1.7 | 1.8 | 1.0 | -0.8 | 2.1 | -0.3 |

| Predom. Food Stores1 | 0.8 | 2.2 | 1.1 | 1.3 | 0.7 | 0.2 | 1.4 | -0.8 | 0.7 | 0.7 |

| Predom. Non-Food Stores1 | 6.4 | 4.3 | -0.2 | 1.1 | 1.8 | 2.9 | 0.3 | -1.3 | 3.7 | -1.9 |

| Non-Store Retailing1 | 11.7 | 13.2 | 2.0 | 1.0 | 6.2 | 3.8 | 2.5 | 1.3 | 0.3 | 2.7 |

| Trade | ||||||||||

| Balance2,3 | -36.2 | -38.7 | -10.6 | -10.0 | -12.7 | -3.0 | -4.0 | -5.6 | -4.5 | .. |

| Exports4 | -1.2 | -0.6 | 2.1 | 2.1 | 1.6 | 2.2 | -5.0 | 0.5 | 1.9 | .. |

| Imports4 | -3.4 | -0.1 | 2.4 | 1.5 | 3.4 | 4.0 | -2.6 | 3.8 | -0.5 | .. |

| Public Sector Finances | ||||||||||

| PSNB-ex3, 5 | -1.3 | -22.3 | -6.6 | -4.1 | -2.8 | -0.3 | -0.3 | -2.2 | -1.2 | -0.9 |

| PSND-ex as a % GD | 83.9 | 85.0 | 85.0 | 84.2 | 84.3 | 83.9 | 84.1 | 84.3 | 83.4 | 83.6 |

| Source: Office for National Statistics | ||||||||||

| Notes: | ||||||||||

| 1. Percentage change on previous period, seasonally adjusted, CVM | ||||||||||

| 2. Levels, seasonally adjusted, CP | ||||||||||

| 3. Expressed in £ billion | ||||||||||

| 4. Percentage change on previous period, seasonally adjusted, CP | ||||||||||

| 5. Public Sector net borrowing, excluding public sector banks. Level change on previous period a year ago, not seasonally adjusted | ||||||||||

Download this table Table 3: UK demand side indicators

.xls (30.2 kB)

Table 4: UK supply side indicators

| 2014 | 2015 | 2015 | 2016 | 2016 | 2016 | 2016 | 2016 | 2016 | 2016 | |

| Q4 | Q1 | Q2 | Apr | May | Jun | Jul | Aug | |||

| Labour Market | ||||||||||

| Employment Rate1, 2 | 72.9 | 73.7 | 74.1 | 74.2 | 74.5 | 74.4 | 74.5 | 74.5 | .. | .. |

| Unemployment Rate1, 3 | 6.2 | 5.4 | 5.1 | 5.1 | 4.9 | 4.9 | 4.9 | 4.9 | .. | .. |

| Inactivity Rate1, 4 | 22.2 | 22.0 | 21.8 | 21.7 | 21.6 | 21.6 | 21.6 | 21.5 | .. | .. |

| Claimant Count Rate7 | 3.0 | 2.3 | 2.3 | 2.2 | 2.2 | 2.2 | 2.2 | 2.2 | 2.2 | 2.2 |

| Total Weekly Earnings6 | £480 | £491 | £495 | £497 | £502 | £503 | £502 | £502 | £505 | .. |

| CPI | ||||||||||

| All-item CPI5 | 1.5 | 0.0 | 0.1 | 0.3 | 0.4 | 0.3 | 0.3 | 0.5 | 0.6 | 0.6 |

| Transport5 | 0.3 | -2.1 | -1.6 | -0.6 | -0.9 | -1.3 | -1 | -0.2 | 0.2 | 1 |

| Recreation &Culture5 | 0.9 | -0.6 | -0.3 | -0.1 | 0.5 | 0.4 | 0.1 | 0.8 | 0.6 | 0.7 |

| Utilities5 | 3.0 | 0.5 | 0.3 | 0.4 | 0.0 | -0.1 | 0.0 | 0.1 | -0.1 | -0.1 |

| Food & Non-alcoh Bev5 | -0.2 | -2.6 | -2.7 | -2.5 | -2.7 | -2.5 | -2.8 | -2.9 | -2.6 | -2.2 |

| PPI | ||||||||||

| Input8 | -6.6 | -12.8 | -12 | -7.6 | -4.1 | -7.1 | -4.3 | -0.5 | 4.1 | 7.6 |

| Output8 | 0.0 | -1.7 | -1.5 | -1 | -0.4 | -0.5 | -0.5 | -0.2 | 0.3 | 0.8 |

| HPI8 | 8.0 | 5.9 | 6.5 | 7.9 | 8.8 | 8.1 | 8.7 | 9.7 | 8.3 | .. |

| Source: Office for National Statistics | ||||||||||

| Notes: | ||||||||||

| 1. Monthly data shows a three month rolling average (e.g. The figure for April is for the three months March to May) | ||||||||||

| 2. Headline employment figure is the number of people aged 16-64 in employment divided by the total population 16-64 | ||||||||||

| 3. Headline employment figure is the number of unemployed people (aged 16+) divided by the economically active population (aged 16+) | ||||||||||

| 4. Headline inactivity figure is the number of economically active people aged 16-64 divided by the 16-64 population | ||||||||||

| 5. Percentage change on previous period a year ago, seasonally adjusted | ||||||||||

| 6. Estimates of total pay include bonuses but exclude arrears of pay (£) | ||||||||||

| 7. Calculated by JSA claimants divided by claimant count plus workforce jobs | ||||||||||

| 8. Percentage change on previous period a year ago, non-seasonally adjusted | ||||||||||