Table of contents

- Authors

- Main points

- Introduction

- Assessing the post-referendum UK economy

- Preliminary estimate of gross domestic product for Quarter 3 2016

- Gross capital formation

- Labour productivity analysis for the period before and after the economic downturn

- An analysis of 2016 Annual Survey of Hours and Earnings (ASHE) data

- Annex A – Dates of our upcoming releases

- Demand and Supply Indicators

2. Main points

Assessing the post-referendum UK Economy

ONS is launching a newly developed dashboard of economic indicators which have particular relevance to monitoring the UK economy going forwards. This contains a range of economic statistics, commentary and trends to consider that are relevant to assessing the post-referendum UK economy.

GDP quarter 3

The economy as a whole has grown an estimated 0.5% in Quarter 3 (July to September) 2016. Although this is a slightly slower growth rate than the previous quarter, GDP has continued the trend of positive growth seen since 2015.

Continued growth in services this quarter means that Gross Domestic Product (GDP) is now 8.2% above its pre-downturn level. The recovery of output in the other main industrial groupings has been relatively slow, with all of these sharing negative growth in the quarter.

Labour productivity analysis before and after the economic downturn

Manufacturing, financial and insurance activities, and information and communication industries make the biggest contribution to the cumulative gap in productivity when compared to the UK’s pre-downturn trend.

Annual Survey of Hours and Earnings (ASHE) 2016

In 2016, there was a continuation of the trend for a growing concentration of pay at the bottom of the UK’s earnings distribution, clustered around the new National Living Wage (NLW) of £7.20 per hour, which is required to be paid for those employees who are 25 years and older.

Around 10% of full-time 16- to 24-year-olds and 15% of part-time 16- to 24-year-olds appear to be getting paid at around the £7.20 NLW in April 2016, although they are not legally required to be paid this rate.

There is less evidence of a concentration at earnings around the new National Living Wage in the public sector compared to the private sector as workers are generally paid above this level in the public sector.

Back to table of contents3. Introduction

This edition of the Economic Review launches the newly developed dashboard of economic indicators which have particular relevance to monitoring the UK economy going forwards.

An updated table of forthcoming ONS economic statistics releases and the data periods they cover is at Annex A.

This edition of the Economic Review also provides further commentary and analysis of:

- the preliminary estimate of gross domestic product for quarter 3 2016

- an explainer for Gross Capital Formation (GCF)

- labour productivity analysis for the period before and after the 2008 economic downturn

- an analysis of 2016 Annual Survey Hours and Earnings (ASHE) provisional data

4. Assessing the post-referendum UK economy

ONS produces a wide range of economic statistics, which now contain data which fall after the UK vote on EU membership that was held on 23 June.

The commentary and trends to consider information is not a forecast or prediction of whether the statistics will show any discernible effects of the EU referendum result but are to aid understanding of how these data are potentially impacted by the international and domestic economic environment as we move forward in time.

Economic overview: November 2016

The economy as a whole has grown by an estimated 0.5% in Quarter 3 (July to September) 2016. Although this is a slightly slower growth rate than the previous quarter, GDP has continued the trend of positive growth seen since 2015.

ONS Chief Economist Nick Vaughan said:

“The ONS data so far have shown an economy largely undisrupted by the UK's decision to leave the EU. Growth has continued at roughly the same rate seen for the past few years with our large and relatively robust services sector still significantly outperforming the rest of the economy.

“On the downside, the costs of raw materials have clearly started to rise due to the weakened pound but there is little sign yet of this feeding through to consumer prices.

“Of course this is only the first chapter of a long story. As well as continuing to survey many thousands of households and businesses, ONS is developing innovative data sources that will help to provide an even more timely and comprehensive picture of the post-referendum economy.”

Embed code

5. Preliminary estimate of gross domestic product for Quarter 3 2016

Figure 1 shows that the economy as a whole has grown an estimated 0.5% in Quarter 3 (July to September) 2016. Although this is a slightly slower growth rate than the previous quarter, GDP has continued the trend of positive growth seen since 2015.

Figure 1: Quarter-on-quarter GDP growth and quarter-on-same-quarter of previous year growth

Chained volume measure, Quarter 1 2012 to Quarter 3 2016, UK

Source: Office for National Statistics

Download this chart Figure 1: Quarter-on-quarter GDP growth and quarter-on-same-quarter of previous year growth

Image .csv .xlsThe main driver of quarter-on-quarter growth in Quarter 3 2016 came from the services industries, which collectively grew by 0.8% to contribute 0.64 percentage points to overall GDP growth. The contribution of services is larger than total GDP growth because it was offset by production and construction,the other main industries which contributed negatively to GDP growth (negative 0.05 and negative 0.09 percentage points respectively). Within the services sector growth of film and TV production activities (which includes cinema ticket sales) grew by 16.4% on the quarter, adding around 0.1 percentage points to GDP growth despite only accounting for 0.6% of the whole economy.

In addition, strong growth in retail trade (excluding motor vehicles) of 1.8% in Quarter 3 2016 also contributed 0.1% to GDP growth. Relatively strong outturns since 2010, averaging 0.6% on the quarter, mean that the output of the services industries is now 12.2% above its pre-downturn peak in Quarter 1 2008.

Figure 2: GDP and main components

chained volume measure, Quarter 1 2008 to Quarter 3 2016, UK

Source: Office for National Statistics

Download this chart Figure 2: GDP and main components

Image .csv .xlsFigure 2 shows that continued growth in services this quarter means that GDP is now 8.2% above its pre-downturn level. The recovery of output in the other main industrial groupings has been relatively slow and this trend continued in Quarter 3 2016. Of the components of production, although mining and quarrying grew relatively strongly at 5.2%, manufacturing, and production of electricity, gas and steam and air conditioning supply contracted by 1.0% and 3.6% respectively.

Construction output also decreased, with growth falling to negative 1.4%. However, this follows a period of strong growth since early 2013.

Back to table of contents6. Gross capital formation

Business investment is an important economic indicator which can act as a barometer of business confidence in the post-referendum UK economy. A significant fall in business investment may reflect a drop in the level of confidence businesses have in the future economic performance of the UK – though many other factors such as the availability of credit are also important.

This section provides a brief summary of the main components of gross capital formation (GCF), the highest level aggregation of investment activity in the expenditure measure of gross domestic product (GDP (E)). The expenditure measure is released with the second estimate of GDP each quarter. This section provides some context for GCF data and its component parts prior to the first publication of GDP (E) data for the post-referendum period, on 25 November 2016.

GCF is produced in accordance with the European System of Accounts (ESA 2010). GCF consists of 3 components: gross fixed capital formation (GFCF), changes in inventories and acquisitions less disposals of valuables.

GFCF consists of resident producers’ acquisitions, less disposals, of fixed assets during a given period. It also includes certain additions to the value of "non-produced assets1" realised by productive activity. Fixed assets are produced assets used in production for more than one year. This includes products such as machinery and transport, as well as buildings and non-tangible assets such as intellectual property among others. GFCF can be broken down by sector and by asset type. Business investment is the main component of GFCF by sector.

Changes in inventories are measured by the value of the entries into inventories less the value of withdrawals and the value of any recurrent losses of goods held in inventories. This mainly comprises of producers’ materials and supplies, work-in-progress goods such as growing crops, finished goods, goods awaiting sale and goods for resale. Within inventories is a separate "alignment adjustment" term which is described in more detail in this section. While the alignment adjustment can be substantial in a given quarter, the adjustment has to sum to zero over the year, so has no effect on calendar year figures.

Acquisitions less disposals of valuables are acquisitions of non-financial goods that are not used primarily for production or consumption, do not deteriorate (physically) over time under normal conditions and are acquired and held primarily as stores of value. This mainly comprises of valuable goods such as precious stones and metals, antiques, other art objects and collectors’ items. This includes "non-monetary gold2" but does not include monetary gold, foreign currency, bonds or other financial assets. Since quarter 4 (Oct to Dec) 2014 acquisitions less disposals of valuables have been consistently higher than in previous quarters.

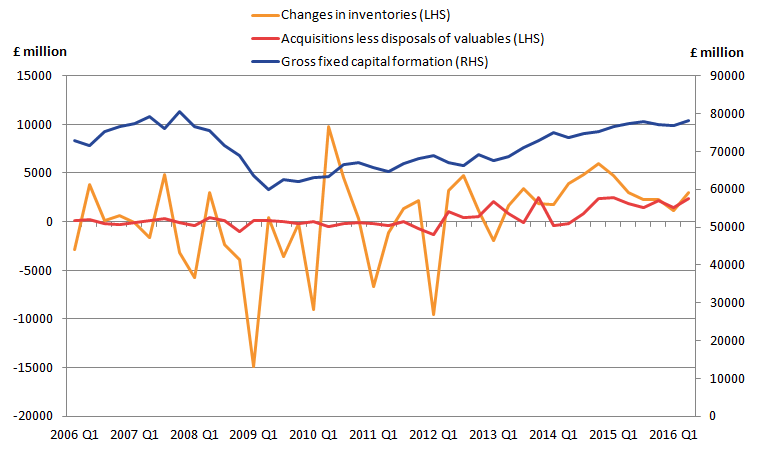

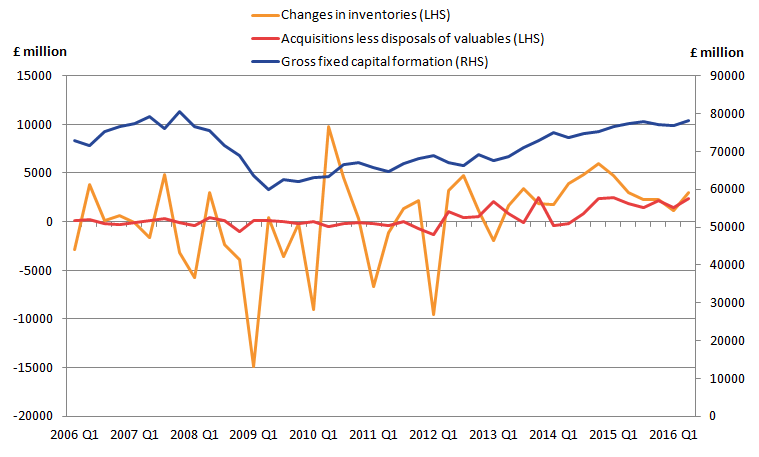

Figure 3 shows that GCF almost entirely comprises GFCF. Even when there are large changes in the other components such as in 2012 Quarter 1 (Jan to Mar), their effect on the level of GCF is small compared with changes in GFCF. Therefore more attention should be attached to GFCF changes over the other 2 components when looking at GCF levels as a whole.

Figure 3: Gross capital formation (GCF) by components, 2006 to 2016

UK

Source: Office for National Statistics

Download this chart Figure 3: Gross capital formation (GCF) by components, 2006 to 2016

Image .csv .xlsFigure 4 repeats the components data in Figure 3 but highlights that changes in inventories in particular tend to be more volatile than GFCF. This can be partly explained by the alignment adjustment applied to this component of GCF.

Figure 4: Components of Gross Capital Formation

Chained volume measure, seasonally adjusted, Quarter 1 2006 to Quarter 2 2016, UK

Source: Office for National Statistics

Download this image Figure 4: Components of Gross Capital Formation

.png (27.8 kB) .xls (71.7 kB){kind=link}

Figure 5 shows the contributions to quarter-on-quarter growth of GDP by component of GCF. The quarter-on-quarter contribution shows how particularly between 2007 Quarter 4 (Oct to Dec) and 2012 Quarter 3 (July to Sept) changes in inventories were both volatile and influential.

Figure 5: Contributions to Quarter-on-quarter growth of Gross Domestic Product by GCF component

Chained volume measure, seasonally adjusted, Quarter 1 2006 to Quarter 2 2016, UK

Source: Office for National Statistics

Download this chart Figure 5: Contributions to Quarter-on-quarter growth of Gross Domestic Product by GCF component

Image .csv .xlsAlignment adjustment

Within inventories, as mentioned earlier in this section, there is an alignment adjustment. The purpose of this is to help balance the 3 approaches to measuring GDP produced by ONS: income, expenditure and output. These are balanced to produce the final GDP estimate. The output measure of GDP has more data available and less erratic components at the time of producing the first balanced estimates for GDP, compared with the other 2 approaches of GDP.

To assist with bringing the growth rates of the income and expenditure measures of GDP into line with the output measure, from the second estimate onwards, there is an alignment adjustment. The alignment adjustment is applied to changes in inventories to balance the quarterly path of the expenditure approach with the output approach. All alignment adjustments in a given calendar year sum to zero so there is no impact on calendar year growth figures and there is no distortion to the real data. At present the sum of the alignment adjustment (equal to the first 2 quarters of the year) is around £100 million. In each quarter the adjustment can be much larger than this, for example, it was plus £1.8 billion in Quarter 2 2016.

Therefore future revisions to these periods plus the sum of the Quarter 3 and Quarter 4 adjustments must equal approximately negative £100 million which will place a small “statistically-driven” downwards pressure on GCF over the second half of the year. However, it is important to consider that as further estimates of GDP are released over the quarter the alignment adjustment can be revised. This reinforces the importance of paying attention to GFCF, the primary driver of GCF.

Notes:

Non-produced assets are non-financial assets that come into existence other than through processes of production; they include both tangible assets (such as land, subsoil assets, non-cultivated biological resources and water resources) and intangible assets (such as patented entities, transferable contracts, purchased goodwill), and also include costs of ownership transfer on and major improvements to these assets.

Non-monetary gold covers exports and imports of all gold not held as reserve assets (monetary gold) by the authorities.

7. Labour productivity analysis for the period before and after the economic downturn

A number of articles were released updating the productivity analysis for the UK economy up to Quarter 2 2016 in October. These data showed that output per hour worked grew by 0.6% on the quarter – slightly faster than the 0.5% observed in the previous quarter. Output per hour has now slightly exceeded its pre-downturn level for the first time since 2008. Estimates of productivity which are comparable across countries suggest that the productivity gap between the UK and the Group of 7 (G7) economies as a whole was little changed in 2015. On a GDP per hour worked basis, productivity in the UK was 18 percentage points lower than the average for the rest of the G7 advanced economies in 2015. (More information on UK productivity can be found in our UK productivity introduction).

Before and after the economic downturn

Measures of productivity over time in the UK show a clear "break" around the time of the economic downturn starting in early 2008, with productivity growth slowing down considerably compared with its pre-downturn rate, although when looking at other developed economies there is some evidence of the slow-down in other countries commencing before the 2008 recession. Explanations for why this break in trend has remained are incomplete and as such this is often referred to as the "productivity puzzle".

This section presents some data on the productivity performance of specific industries, to identify whether the slowdown in productivity growth is broad-based or whether particular industries have been disproportionately affected.

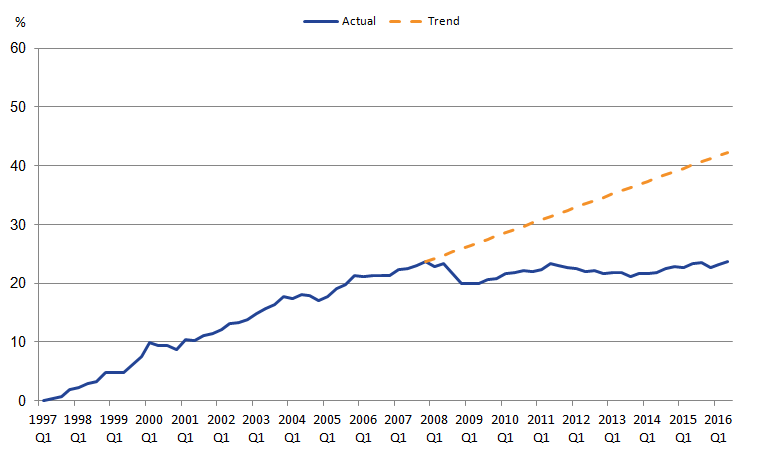

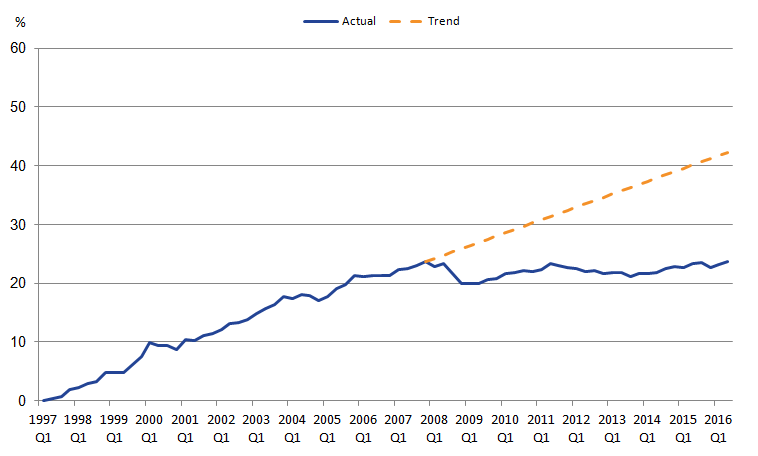

Figure 6 presents an output per hour measure of productivity, plotting the cumulative change in output per hour for the whole economy since Quarter 1 (Jan to Mar) 1997.

Figure 6: Whole economy increase in output per hour since Q1 1997

Actual and pre-2008 trend, UK

Source: Office for National Statistics

Notes:

- These estimates may not equal the labour productivity National Statistics productivity estimate, due to the use of the 'Generalised Exactly Additive Decomposition' (GEAD) methodology as described in Tang and Wang (2004) on a quarterly basis.

Download this image Figure 6: Whole economy increase in output per hour since Q1 1997

.png (11.0 kB) .xls (26.6 kB){kind=link}

The trend line shows how output per hour would have performed had it continued to grow at the Quarter 1 1997 -Quarter (Oct to Dec) 4 2007 rate (taking a compound average growth rate). The darker blue line represents the change in productivity shown in the latest data - so for example, output per hour was 23.8% higher in 2016 Quarter 2 2016 compared with Quarter 1 1997, but remains roughly the same level as in Quarter 4 2007.

Since the projected increase in aggregate output per hour since Quarter 1 1997 is roughly twice that of the actual increase, any industries that are adrift of trend growth by more than 50% (or that have performed relatively close to trend growth) could be of interest.

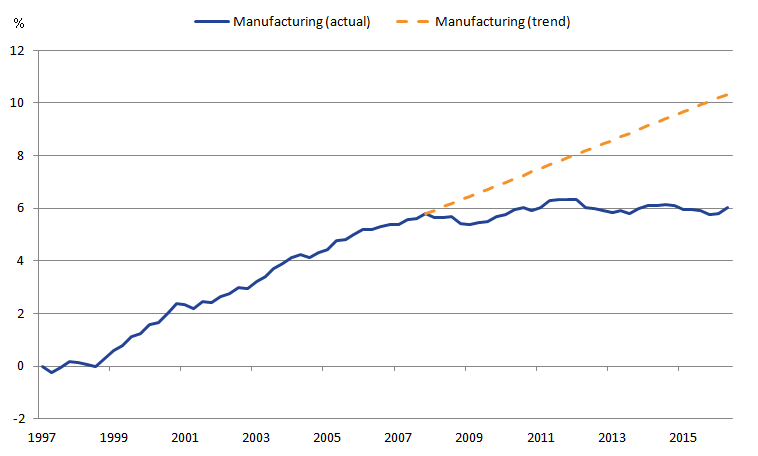

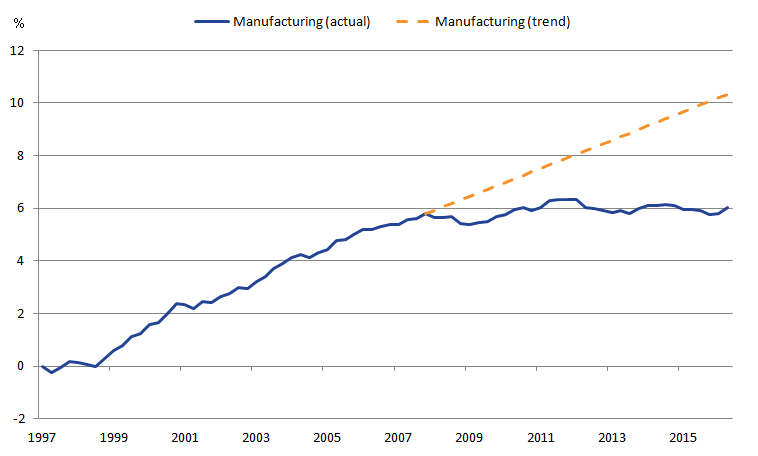

Manufacturing

Figure 7 shows that since the onset of the downturn, contributions to productivity growth in manufacturing as a whole has slowed down at roughly the same rate as that in the total economy. This reflects a decline in manufacturing GVA, while productivity hours in manufacturing has remained fairly stable.

Figure 7: Contributions to total productivity growth from manufacturing (C)

Quarter 1 1997 to Quarter 2 2016, UK

Source: Office for National Statistics

Notes:

- These estimates may not equal the labour productivity National Statistics productivity estimate, due to the use of the 'Generalised Exactly Additive Decomposition' (GEAD) methodology as described in Tang and Wang (2004) on a quarterly basis.

Download this image Figure 7: Contributions to total productivity growth from manufacturing (C)

.png (14.8 kB) .xls (29.7 kB){kind=link}

Manufacturing has a number of sub-components and the slowdown in productivity growth has had a broadly symmetric impact across all these sub-components. The only exception is productivity in the manufacture of transport equipment, which has tracked its pre-downturn trend growth.

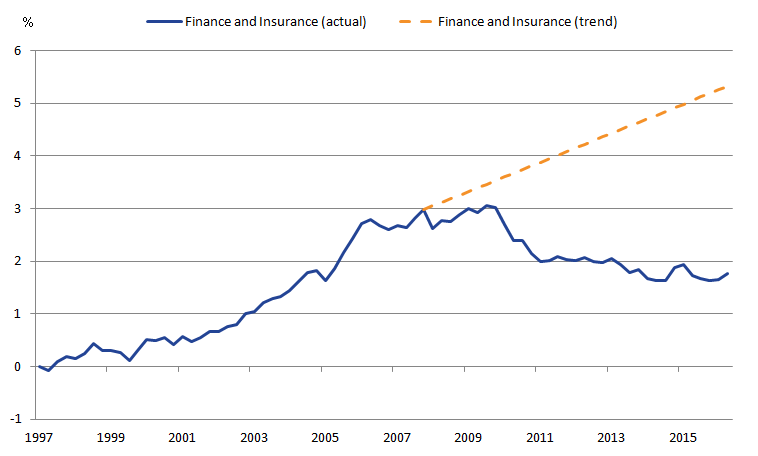

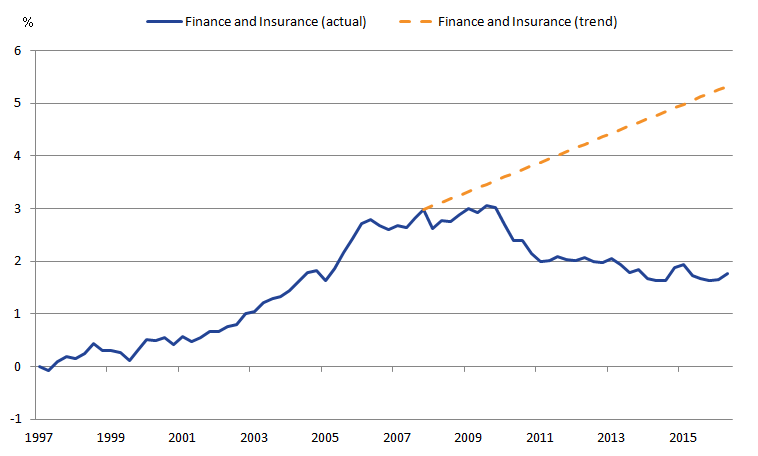

Finance and insurance activities

Figure 8 shows that contributions to productivity growth in finance and insurance activities has departed significantly from trend since the downturn. Instead of contributing a projected 5.3% to total productivity growth in Q2 2016 (compared to Q1 1997), only 1.8% has been contributed (remaining well below its pre-downturn peak). This largely reflects a decline in the industry’s GVA. Productivity hours in the industry dropped immediately after the downturn but have since returned to their pre-downturn peak.

Figure 8: Contributions to total productivity growth from finance and insurance activities (K)

Quarter 1 1997 to Quarter 2 2016, UK

Source: Office for National Statistics

Notes:

- These estimates may not equal the labour productivity National Statistics productivity estimate, due to the use of the 'Generalised Exactly Additive Decomposition' (GEAD) methodology as described in Tang and Wang (2004) on a quarterly basis.

Download this image Figure 8: Contributions to total productivity growth from finance and insurance activities (K)

.png (17.2 kB) .xls (23.6 kB){kind=link}

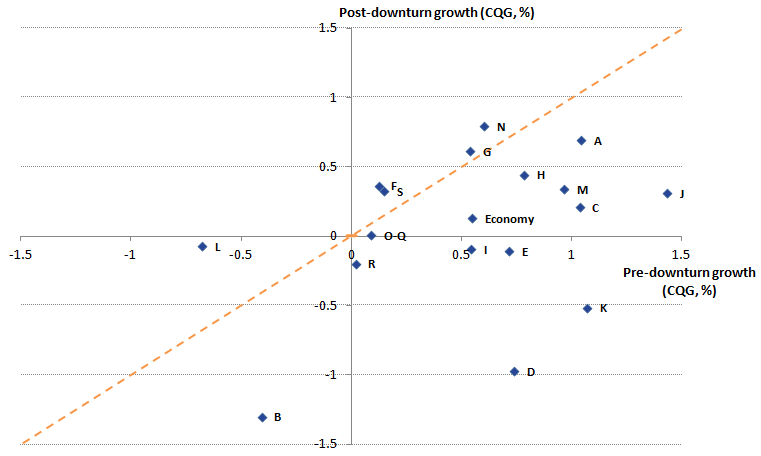

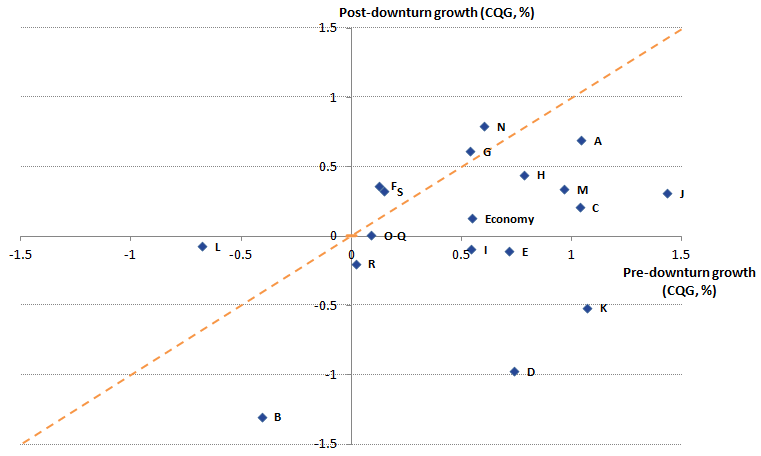

Comparing annual growth rates for labour productivity across industries before and after the economic downturn

Figure 9 compares productivity growth in each industry (using a quarterly compound average growth rate) before and after the economic downturn (the downturn period, when total productivity fell, is excluded).

Figure 9 shows that industries above the 45 degree line have seen higher productivity growth since the downturn while those below (the majority) have seen lower growth.

Figure 9: Compound average quarterly growth rates by industry

Pre-downturn (Quarter 1 1997 to Quarter 4 2007) and post-downturn (Quarter 2 2009 to Quarter 2 2016), UK

Source: Office for National Statistics

Notes:

- Sections come from the Standard Industrial Classification 2007

- A = agriculture, forestry, fishing B = mining and quarrying, C = manufacturing, D = electricity, gas, steam and air conditioning supply, E = water supply; sewerage, waste management and remediation activities, F = construction, G = wholesale and retail trade, repair of motor vehicles and motorcycles, H = transportation and storage, I = accommodation and food service activities, J = information and communication, K = financial and insurance activities, L = real estate activities, M = professional, scientific and technical activities, N = administrative and support service activities, O = public administration and defence; compulsory social security, P = education, Q = human health and social work activities, R = arts, entertainment and recreation, S = other services activities.

Download this image Figure 9: Compound average quarterly growth rates by industry

.png (13.6 kB) .xls (23.0 kB){kind=link}

Particular contrasts before and after the economic-downturn are in industry K (finance and insurance), D (electricity, gas, steam and air conditioning supply) and B (mining and quarrying). Only industry sector L (real estate activities) shows some substantive improvement over its pre-downturn productivity growth rate. However, some of the these industry sectors have a much lower weight which affects how they contribute to overall productivity growth in the economy.

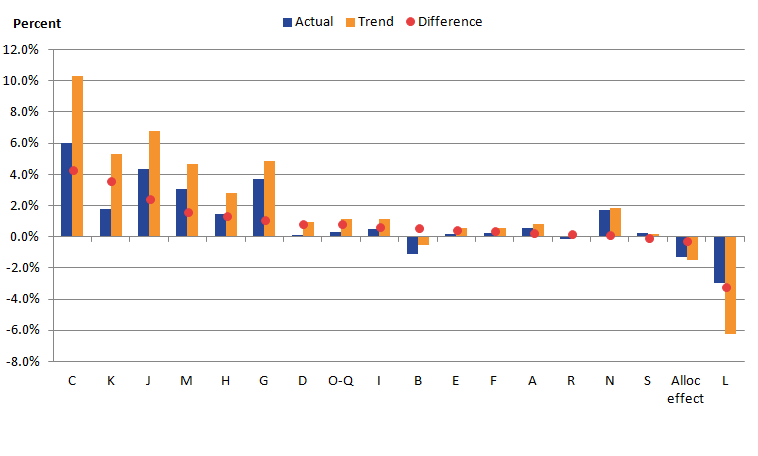

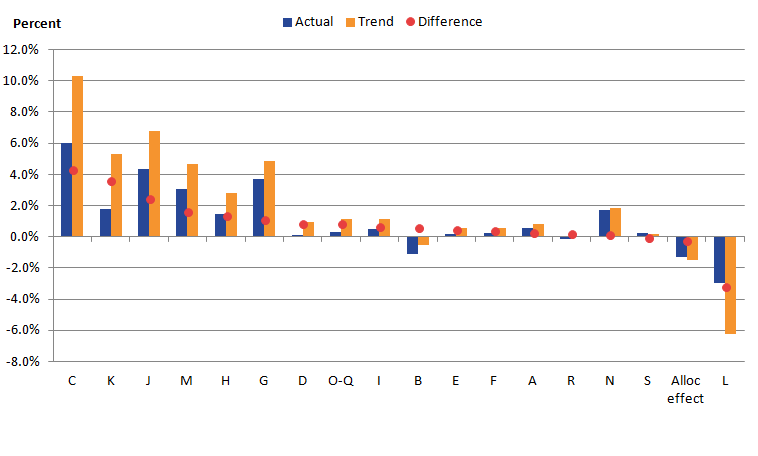

Projected and actual contributions to total productivity growth by industry

In Figure 10 the orange bars give the projected contribution to total productivity growth by industry, had that industry had contributions to productivity growth from that industry continued in line with its Quarter 1 1997 to Quarter 4 2007 trend.

Figure 10: Projected contributions to total productivity growth (output per hour), actual contributions to productivity, and differences, by industry

Quarter 1 1997 to Quarter 2 2016, UK

Notes:

- Sections come from the Standard Industrial Classification 2007

- A = agriculture, forestry, fishing B = mining and quarrying, C = manufacturing, D = electricity, gas, steam and air conditioning supply, E = water supply; sewerage, waste management and remediation activities, F = construction, G = wholesale and retail trade, repair of motor vehicles and motorcycles, H = transportation and storage, I = accommodation and food service activities, J = information and communication, K = financial and insurance activities, L = real estate activities, M = professional, scientific and technical activities, N = administrative and support service activities, O = public administration and defence; compulsory social security, P = education, Q = human health and social work activities, R = arts, entertainment and recreation, S = other services activities.

- ‘Allocation effects’ refer to changes in productivity due to labour and price movements between industries, rather than inherent changes in productivity within an industry.

- "Alloc effect" = Allocation effect.

Download this image Figure 10: Projected contributions to total productivity growth (output per hour), actual contributions to productivity, and differences, by industry

.png (13.2 kB) .xls (29.7 kB){kind=link}

Comparing the two bars (or looking at the difference in percentage points, denoted by the dots) gives an indication of how each section has performed relative to its pre-downturn productivity growth path.

Manufacturing (C), financial and insurance activities (K) and information and communication industries (J) have a 2 percentage point or more difference over their projected contributions to productivity growth. Contributions to differences over their projected trends are relatively small in most other industry sectors.

Back to table of contents8. An analysis of 2016 Annual Survey of Hours and Earnings (ASHE) data

An analysis 1 of the distribution of earnings using ASHE 2016 data and previous ASHE datasets over time was published on 26 October 2016. The analysis looks at some interesting differences in earnings distribution of the UK workers by sex, region, skill level, age and working pattern. Earnings growth for those in employment between 2 consecutive years is also discussed. The analysis focuses on the low-end of the distribution and highlights some interesting elements of the National Living Wage (NLW) introduced in April 2016 for adults 25 years and over.

Trends over time

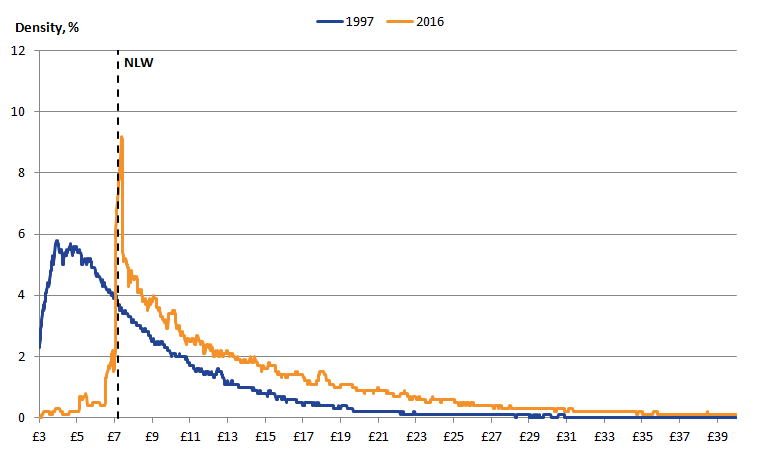

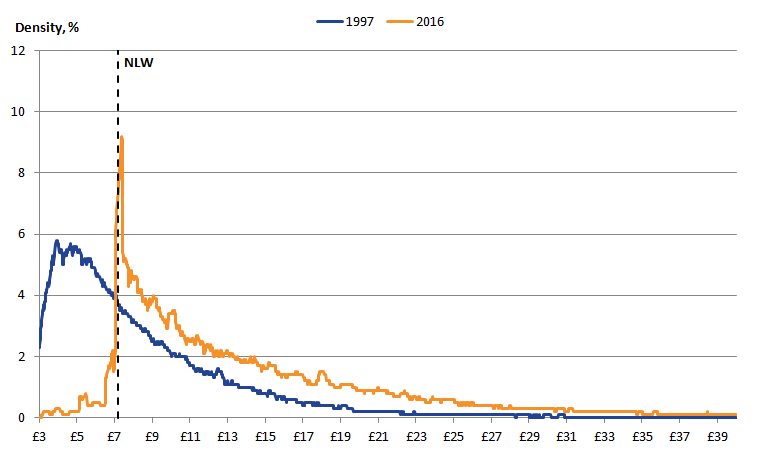

Figure 11 shows that in 1997, prior to the introduction of the National Minimum Wage (NMW), the UK’s distribution was relatively smooth, positively skewed and centered on hourly earnings of between £4 and £5 per hour. By 2016, however, the shape of this distribution changed markedly. The earlier, smooth profile was replaced by a sharply-edged distribution, with a mass around £7.20 per hour - the prevailing adult National Living Wage (NLW) in April 2016. Above this level of pay, the density of the distribution has slightly shifted to the right.

Figure 11: Distribution of gross hourly earnings and the Adult National Living Wage in April 2016

+/-20 pence, 1997 and 2016, UK

Source: Office for National Statistics, Annual Survey of Hours and Earnings

Notes:

- Each point on the x-axis represents a rolling sum of the density of jobs receiving greater than or equal to 20 pence below, and strictly less than 20 pence above, the stated hourly earnings.

- As the density records the rolling sum of jobs paid within 20 pence of the stated amount at each point on the x-axis, jobs paid the April 2016 Adult National Living Wage (£7.20) will appear between the x-axis values of £7.00 and £7.40.

Download this image Figure 11: Distribution of gross hourly earnings and the Adult National Living Wage in April 2016

.png (15.8 kB) .xls (174.1 kB){kind=link}

Growth of earnings over time

Analysis of variation in levels of pay provides useful insight into distributional outcomes in the UK, yielding information about one group's earnings relative to another. However, the Annual Survey of Hours and Earnings (ASHE) datasets can also be used to examine the typical experience of earnings growth through time.

The experience of earnings growth is remarkably varied from one period to the next. Figure 12 shows the distribution of nominal hourly earnings growth rates in the year to:

- April 2007 (corresponding to individuals in employment in both 2006 and 2007)

- April 2016 (corresponding to individuals in employment in both 2015 and 2016)

For each growth rate on the horizontal axis, the area under the curve indicates a portion of employees who experienced earnings growth within 0.5 percentage points of that rate.

In 2016, the most frequently occurring rate of growth was around zero %, suggesting that a larger number of people experienced a nominal pay freeze in 2016 compared with 2007, although around 7% of workers also had a zero % growth in pay in that year. There is also a noticeable bump between 10% and 11% pay growth. This increase in the share of employees receiving a pay rise around 10.8% is likely to reflect the switch from the National Minimum Wage (NMW) of £6.50 an hour in April 2015 to the National Living Wage (NLW) of £7.20 in April 2016.

Thus, 2 main observations are noticeable from the distribution of growth in earnings:

amongst workers who experienced changes in earnings, those receiving the NLW instead of NMW saw a large increase in pay

there is evidence of limited earnings growth, which may partially reflect the historically low levels of inflation during the period April 2015 to April 2016

Figure 12: Distribution of growth in gross nominal hourly earnings

+/- 0.5 percentage points, 2007 and 2016, UK

Source: Office for National Statistics, Annual Survey of Hours and Earnings

Notes:

- This chart uses individual level data from ASHE to calculate the growth of nominal weekly earnings for individuals observed in pairs of years in 2007 and 2016. Note that the ASHE methodology is not specifically designed to model earnings growth for individuals over time.

- Note that the proportion of people experiencing a pay growth between 10% and 11% may not reflect the proportion of people on the National Living Wage in the earnings distribution in April 2016. This is because the growth analysis is focussing on employed workers in two consecutive periods and not just in April 2016.

Download this chart Figure 12: Distribution of growth in gross nominal hourly earnings

Image .csv .xlsRegional analysis

Amongst the regions of the UK, each region shows a clear spike around £7.20 - representing the new National Living Wage (NLW) for ages 25 and over, introduced in April 2016. However, the main difference between regions is the height of the spike. The largest regional difference in the distribution of earnings and the share of employees earning around £7.20 per hour is between London where around 5.8% of employees earn this amount and Northern Ireland where around 13.7% earn this amount. London also has a higher proportion of people on the higher pay brackets than any other region. Detailed analysis can be found on our website.

Sex analysis

Figure 13 shows there are large differences in the earnings distribution for men and women with a greater share of women earning around the National Living Wage (NLW) in 2016 compared with men. This partly reflects the greater share of women working in part-time jobs which are more likely to be paying around the NLW in 2016 than full-time jobs. In 2016, the modal earnings for both men and women is around £7.00 (plus or minus 20 pence), covering 6.9% of all jobs for men and 11.5% of all jobs for women. This means that women’s earning profile has a bigger spike around the (NLW) in comparison with men. A greater share of men than women receive hourly earnings of more than £12, although previous analysis suggests that the gap between the earnings profile of men and women has declined substantially since 1997.

Figure 13: Distribution of gross nominal hourly earnings by gender

April 2016, +/-20 pence, UK

Source: Office for National Statistics, Annual Survey of Hours and Earnings

Notes:

- Each point on the x-axis represents a rolling sum of the density of jobs receiving greater than or equal to 20 pence below, and strictly less than 20 pence above, the stated hourly earnings.

- As the density records the rolling sum of jobs paid within 20 pence of the stated amount at each point on the x-axis, jobs paid the April 2016 Adult National Living Wage (£7.20) will appear between the x-axis values of £7.00 and £7.40.

Download this chart Figure 13: Distribution of gross nominal hourly earnings by gender

Image .csv .xlsSkills analysis

Comparing earnings by skill level shows that those working in lower-skill occupations such as cleaning and basic administrative roles are strongly clustered around the £7.20 National Living Wage (NLW) rate in April 2016. The Standard Occupational Classification 2010 (SOC2010) separates the labour market into 9 major groups, based on criteria such as the qualifications, skills and experience associated with each job. These 9 major groups can be combined further into 4 skill groups; levels 1 through 4. Level 1 indicates relatively low skill requirements and level 4 indicates relatively high skill requirements. Table 1 describes some of important features of each skill group.

Table 1: SOC 2010 classification of skill groups and share of employees by skill group

| Skill group | Proportion of men, ASHE 2016 | Proportion of women, ASHE 2016 | Typical occupations |

| 1 (low) | 12% | 11% | Labourers (e.g. agriculture, construction), cleaners & basic admin workers |

| 2 (lower-mid) | 26% | 46% | Secretaries, carers, hairdressers, cashiers, machine operatives, transport drivers |

| 3 (upper-mid) | 31% | 16% | Skilled trade workers, associate professionals and technical occupations |

| 4 (upper) | 31% | 27% | Professionals (e.g. teachers, doctors, scientists, engineers, managers, directors) |

| Source: Office for National Statistics | |||

Download this table Table 1: SOC 2010 classification of skill groups and share of employees by skill group

.xls (26.6 kB)Figures 14a and 14b show the distribution of nominal hourly earnings by skill-group for full-time and part-time workers. It shows that the distribution of earnings differs considerably by skill group. Those in the “low” category are clustered at or just above the NLW in 2016. This applies to both full- and part-time jobs, although more so for part-time workers. The “lower-mid” category workers are also grouped at the NLW (more so for part-time workers), but with a greater proportion of workers earning above the NLW than in the lowest skill group. The “upper-mid” category shows less clustering at the NLW, although part-time workers in particular still show a clear NLW spike. However, part-time workers account for only around 12% of this skill group. The highest skill category shows a relatively even distribution across the wage brackets shown, extending well into £30 plus per hour territory. Additional analysis of ASHE data for 2016, with a particular focus on public and private sector earnings, is available in an article “Analysis of factors affecting earnings using ASHE 2016”.

Figure 14a: Distribution of gross nominal hourly earnings by skill group for full-time workers

April 2016, +/-20 pence, UK

Source: Office for National Statistics, Annual Survey of Hours and Earnings

Notes:

- Full-time defined as employees working more than 30 paid hours per week (or 25 or more for the teaching professions).

- Each point on the x-axis represents a rolling sum of the density of jobs receiving greater than or equal to 20 pence below, and strictly less than 20 pence above, the stated hourly earnings.

- As the density records the rolling sum of jobs paid within 20 pence of the stated amount at each point on the x-axis, jobs paid the April 2016 Adult National Living Wage (£7.20) will appear between the x-axis values of £7.00 and £7.40.

Download this chart Figure 14a: Distribution of gross nominal hourly earnings by skill group for full-time workers

Image .csv .xls

Figure 14b: Distribution of gross nominal hourly earnings by skill group for part-time workers

April 2016, +/-20 pence, UK

Source: Office for National Statistics, Annual Survey of Hours and Earnings

Notes:

- Each point on the x-axis represents a rolling sum of the density of jobs receiving greater than or equal to 20 pence below, and strictly less than 20 pence above, the stated hourly earnings.

- As the density records the rolling sum of jobs paid within 20 pence of the stated amount at each point on the x-axis, jobs paid the April 2016 Adult National Living Wage (£7.20) will appear between the x-axis values of £7.00 and £7.40.

Download this chart Figure 14b: Distribution of gross nominal hourly earnings by skill group for part-time workers

Image .csv .xlsAge analysis

Looking at a breakdown of the Annual Survey of Hours and Earnings (ASHE) data by age is particularly interesting with the 2016 data, given that the National Living Wage (NLW) wage only legally applies to those aged 25 or over. Looking at the wage distribution for 16- to 24-year-olds in particular can give an indication as to whether employers have chosen to keep younger workers on lower rates, or whether they moved them up to the NLW along with workers aged 25 and over. The 16- to 24-year-olds category is further broken down into 16- to 20-year-olds and 21- to 24-year-olds to give a finer breakdown.

Figures 15a and 15b show the distribution of gross nominal hourly earnings for specific age bands for full-time and part-time workers in April 2016.

16 to 20 year olds

The distribution for full-time workers shows that those aged 16 to 20 years old have 3 peaks:

- one at £3.50 (corresponding to the £3.30 an hour Minimum Wage rate for apprentices)

- one at £5.40 (corresponding to the £5.30 National Minimum Wage for 18- to 20-year-olds)

- the highest peak at £7.36 (corresponding to the £7.20 National Living Wage)

Figure 15a: Distribution of gross nominal hourly earnings by age band for full-time workers

April 2016, +/-20 pence, UK

Source: Office for National Statistics, Annual Survey of Hours and Earnings

Notes:

- Full-time defined as employees working more than 30 paid hours per week (or 25 or more for the teaching professions).

- Each point on the x-axis represents a rolling sum of the density of jobs receiving greater than or equal to 20 pence below, and strictly less than 20 pence above, the stated hourly earnings.

- As the density records the rolling sum of jobs paid within 20 pence of the stated amount at each point on the x-axis, jobs paid the April 2016 Adult National Living Wage (£7.20) will appear between the x-axis values of £7.00 and £7.40.

Download this chart Figure 15a: Distribution of gross nominal hourly earnings by age band for full-time workers

Image .csv .xls

Figure 15b: Distribution of gross nominal hourly earnings by age band for part-time workers

April 2016, +/-20 pence

Source: Office for National Statistics, Annual Survey of Hours and Earnings

Notes:

- Each point on the x-axis represents a rolling sum of the density of jobs receiving greater than or equal to 20 pence below, and strictly less than 20 pence above, the stated hourly earnings.

- As the density records the rolling sum of jobs paid within 20 pence of the stated amount at each point on the x-axis, jobs paid the April 2016 Adult National Living Wage (£7.20) will appear between the x-axis values of £7.00 and £7.40.

Download this chart Figure 15b: Distribution of gross nominal hourly earnings by age band for part-time workers

Image .csv .xlsThis may indicate that some employers might be paying younger full-time workers the NLW even if they are not legally required to do so. The earnings distribution for 16- to 20-year-olds is more spread out than the earnings distributions for other age brackets, which show sharper albeit smaller spikes at the NLW.

20 to 24 year olds

The distribution by age for full-time workers shows that for 20- to 24-year-olds there are 2 peaks – one clustered around £6.54 (corresponding to the £6.70 National Minimum Wage (NMW) for 21- to 24-year-olds), and one with a mass of jobs at £7.34 (corresponding to the £7.20 National Living Wage (NLW) for people aged 25 and over). Again, this gives tentative evidence that some employers might be paying younger full-time workers the NLW even if they are not legally required to do so.

The other age bands also see a peak at the NLW, but they are relatively small for the older age brackets. Above the NLW the 3 older groups tend to converge, with the distribution for the 25 to 34 age group slightly to the left of the other 2.

For part-time workers (Figure 15b) the distribution around the NLW is somewhat different. Each age band has a much sharper spike at the NLW, with 25- to 34-year-olds seeing the largest concentration at this rate. The age band with the highest peak are 21- to 24- year olds at £6.90 - which corresponds to the £6.70 per hour NMW.

There are several peaks for 16- to 20-year-olds - one at £4.02 (corresponding to the £3.87 per hour NMW for under 18 year olds), the highest at £5.46 (corresponding to the £5.30 per hour NMW for under 18- to 20-year-olds), one at £6.86 (corresponding to the £6.70 per hour NMW for under 21- to 24-year-olds), and one at £7.34 (corresponding to the £7.20 per hour NLW for people aged 25 and over).

Hence, there is some evidence that suggests that some employers might be paying younger part-time workers the NLW or the NMW for a higher age group, even if they are not legally required to do so.

Public and private analysis

An interesting breakdown to look at is how the distribution of earnings differs between the public sector and private sector, as shown in Figure 16. This shows that, compared with the public sector, there is a higher concentration of jobs close to the National Living Wage (NLW) in the private sector. Around 12% of jobs in the private sector pay a wage within 20 pence of the NLW – compared with around 2% in the public sector.

The distribution of nominal hourly earnings for public sector workers is smooth and positively skewed. While the hourly earnings in the public sector tend to be higher in the lower and middle of the income distribution, hourly earnings for the private sector tend to be higher towards the top end of the income distribution. Additional analysis of ASHE data for 2016, with a particular focus on public and private sector earnings, is available in an article “Analysis of factors affecting earnings using ASHE 2016”.

Figure 16: Distribution of gross nominal hourly earnings by sector

April 2016, +/-20 pence, UK

Source: Office for National Statistics, Annual Survey of Hours and Earnings

Notes:

- Each point on the x-axis represents a rolling sum of the density of jobs receiving greater than or equal to 20 pence below, and strictly less than 20 pence above, the stated hourly earnings.

- As the density records the rolling sum of jobs paid within 20 pence of the stated amount at each point on the x-axis, jobs paid the April 2016 Adult National Living Wage (£7.20) will appear between the x-axis values of £7.00 and £7.40.

Download this chart Figure 16: Distribution of gross nominal hourly earnings by sector

Image .csv .xlsGrowth of earnings distribution by public and private

Figure 17 shows the distribution of growth in gross nominal hourly earnings by the public and private sector. Since more jobs in the private sector pay the National Living Wage (NLW), the growth distribution for the private sector shows a noticeable bump between a 10% and 11% pay rise - corresponding to the switch from the National Minimum Wage (NMW) in April 2015 to the NLW for adults over 25 years of age in April 2016. However, the public sector did not see the same increase, indicating a limited impact on public sector workers of the introduction of the NLW.

Close to 11% of jobs in both the public and private sectors received around zero % pay increase. However, the most common pay rise for the public sector was between 1% and 2%. Nearly 8% of jobs in the private sector also saw a pay rise between 2% and 3%.

Figure 17: Distribution of gross nominal hourly earnings growth by public and private sector

April 2016, +/- 0.5 percentage points, UK

Source: Office for National Statistics, Annual Survey of Hours and Earnings

Notes:

- This chart uses individual level data from ASHE to calculate the growth of nominal weekly earnings for individuals observed in pairs of years in 2015 and 2016. Note that the ASHE methodology is not specifically designed to model earnings growth for individuals over time.

- Note that the proportion of people experiencing a pay growth between 10% and 11% may not reflect the proportion of people on the National Living Wage in the earnings distribution in April 2016. This is because the growth analysis is focusing on employed workers in two consecutive periods and not just in April 2016.

Download this chart Figure 17: Distribution of gross nominal hourly earnings growth by public and private sector

Image .csv .xls9. Annex A – Dates of our upcoming releases

Users have been in contact with us to ask when any impact from the recent EU referendum could feed through to our economic statistics. Below we set out the release dates from our main economic indicators and the data periods they cover. Some economic context and trends to consider for these forthcoming releases has been provided at Visual.ONS.

Table 2: Dates of upcoming ONS releases

| Date | Indicator | Details | Date of following release |

| 08/11/2016 | Index of Production, September 2016 | Provides data for September | 7/12/2016: provides data for October |

| 09/11/2016 | UK Trade, September | Provides data for September | 9/12/2016: provides data for October |

| 11/11/2016 | Construction output, September and July to September, Quarter 3 | Provides data on construction output for first full quarter following the referendum | 9/12/2016: provides data for output for October and new orders quarter 3 2016 |

| 15/11/2016 | Consumer Price Index 2016, October | Provides data for October | 13/12/2016: provides data for November |

| 15/11/2016 | Producer Prices, October 2016 | Provides data for October | 13/12/2016: provides data for November |

| 15/11/2016 | UK House Price index, September | Provides data for September | 13/12/2016: provides data for October |

| 16/11/2016 | Labour Market Statistics, November | Includes Labour Force Survey data for July, August and September. The first unemployment release including an entirely post-referendum period. This release also includes Quarter 3 data of country of birth and nationality. | 14/12/2016: Provides data for August, September and October. |

| 17/11/2016 | Retail Sales, October | Provides data for October | 15/12/2016: provides data for November |

| 18/11/2016 | Overseas travel and tourism provisional, monthly September 2016 | Provides data for September | 19/1/2017 (provisional) : provides data for Quarter 3 2016 |

| 22/11/2016 | Public Sector Finances, October 2016 | Provides data for October | 21/12/2016: provides data for November |

| 25/11/2016 | GDP 2nd estimate, Quarter 3 | The first GDP release, including output, income and expenditure data including an entirely post-referendum period | 23/02/2017: Provides data for 2nd estimate of GDP Quarter 4 2016 |

| 25/11/2016 | Business Investment preliminary estimate, Quarter 3 | The first investment release including an entirely post-referendum period | 23/02/2017: provide data for Quarter 4 2016 |

| 25/11/2016 | Index of Services, September | Provides data for September | 23/12/2016: provides data for October |

| 25/11/2016 | Business investment in the UK, provisional: July to Sept 2016 | Investment trends by businesses, contains capital expenditure estimates at current prices, constant prices and seasonally adjusted. | 23/12/2016: revised Q3 estimates |

| 01/12/2016 | Migration in the UK, December | While this includes IPS estimates up to 30 June, the vast majority of the period was before the referendum. | 23/02/2017: provides data up to 30 September 2016 |

| 02/12/2016 | Foreign Direct Investment, 2015. | The annual FDI publication includes data up to 31 December 2015, the entire period was before the referendum – | December 2017 - provides results for 2016, where half of the period would be before the referendum. |

| 07/12/2016 | UK index of production: Oct 2016 | Provides data for October | 11/01/2017: provides data for November 2016 |

| 09/12/2016 | UK trade: Oct 2016 | Provides data for October | 10/01/2017 : provides data for November 2016 |

| 09/12/2016 | Construction output in Great Britain: Oct 2016 and new orders July to Sept 2016 | Provides data for October | 11/01/2017: provides data for November 2016 |

| 13/12/2016 | Consumer Price Index 2016, November 2016 | Provides data for November | 15.01.2017 (provisional): provides data for December 2016 |

| 13/12/2016 | Producer Prices, November 2016 | Provides data for November | 15.01.2017 (provisional): provides data for December 2016 |

| 13/12/2016 | UK House Price index, October 2016 | Provides data for October | 17/01/2017: provides data for November 2016 |

| 14/12/2106 | UK labour market statistics: Dec 2016 | Provides data for August to October | 18/01/2017: provides data for September to November 2016 |

| 15/12/2016 | Retail Sales, November | Provides data for November | 19/01/2017: provides data for December 2016 |

| 21/12/2016 | UK public sector finances: Nov 2016 | Provides data for November | 24/01/2017: provides data for December 2016 |

| 22/12/2016 | Index of private housing rental prices (IPHRP) in Great Britain, results: Nov 2016 | Provides data for November | 27/01/2017: provides data for December 2016 |

| 23/12/2016 | Index of Services, November | Provides data for October | 26/1/2017: provides data for November |

| 23/12/2016 | Balance of Payments, Quarter 3 | The first Balance of Payments figures folowing the referendum | 31/3/2017: provides data for Quarter 4 2016 |

| 23/12/2016 | Quarterly National Accounts, Quarter 3 | Provides data for quarter 3 | 31/3/2017: provides data for Quarter 4 2016 |

| 23/12/2016 | Consumer Trends, Quarter 3 | Provides data for quarter 3 | 31/3/2017: provides data for Quarter 4 2016 |

| 23/12/2016 | Business Investment revised, quarter 3 | Provides data for quarter 3 | 23/2/2017: provides provisional data for Quarter 4 2016 |

| 23/12/2016 | Economic Well-being, Quarter 2 | Provides data for quarter 3 | 31/3/2017: provides data for Quarter 4 2016 |

| December (exact data to be confirmed) | Investment by insurance companies, pension funds and trusts in the UK (MQ5): Quarter 3 (July to September) 2016 | The first MQ5 release including an entirely post-referendum period | March 2017 (provisional) : provides data for Quarter 4 2016 |

| 23/02/2017 | Migration in the UK, February | While this includes IPS estimates up to 30 September, most of the period was before the referendum | 25/05/2017: provides data up to 31 December 2016. Half of this period was before the referendum |

| Source: Office for National Statistics | |||

Download this table Table 2: Dates of upcoming ONS releases

.xls (34.3 kB)10. Demand and Supply Indicators

Table 3: UK demand side indicators

| 2014 | 2015 | 2016 | 2016 | 2016 | 2016 | 2016 | 2016 | 2016 | 2016 | |

| Q1 | Q2 | Q3 | May | Jun | Jul | Aug | Sep | |||

| GDP | 3.1 | 2.2 | 0.4 | 0.7 | 0.5 | |||||

| Index of Services | ||||||||||

| All Services1 | 3.3 | 2.5 | 0.7 | 0.6 | 0.8 | 0.0 | 0.3 | 0.4 | 0.2 | .. |

| Business Services & Finance1 | 3.9 | 2.6 | 0.7 | 0.6 | 0.5 | -0.1 | 0.3 | 0.2 | 0.1 | .. |

| Government & Other1 | 1.7 | 0.5 | 0.5 | 0.1 | 0.3 | 0.2 | 0.2 | 0.2 | -0.1 | .. |

| Distribution, Hotels & Rest1 | 4.8 | 4.6 | 1.4 | 1.1 | 1.1 | 0.4 | 0.1 | 0.0 | 1.0 | .. |

| Transport,Stor. & Comms1 | 3.0 | 3.8 | 0.0 | 0.6 | 2.2 | -0.5 | 0.9 | 1.6 | 0.4 | .. |

| Index of Production | ||||||||||

| All Production1 | 1.5 | 1.3 | -0.1 | 2.1 | -0.4 | -0.7 | 0.0 | 0.1 | -0.4 | .. |

| Manufacturing1 | 2.9 | -0.1 | -0.3 | 1.6 | -1.0 | -0.7 | -0.2 | -0.9 | 0.2 | .. |

| Mining & Quarrying1 | 0.6 | 8.5 | -1.2 | 2.8 | 5.2 | -0.5 | 1.6 | 6.8 | -3.7 | .. |

| Construction1 | 8.0 | 4.9 | 0.8 | -0.1 | -1.4 | |||||

| Retail Sales Index | ||||||||||

| All Retailing1 | 4.0 | 4.4 | 1.4 | 1.1 | 1.8 | 1.1 | -0.8 | 2.0 | 0.0 | 0.0 |

| All Retailing excl Fuel1 | 4.3 | 4.0 | 1.4 | 1.3 | 1.8 | 1.1 | -0.7 | 2.0 | -0.1 | 0.0 |

| Predom. Food Stores1 | 1.0 | 2.2 | 1.5 | 0.3 | 1.3 | 1.1 | -0.2 | 0.7 | 0.7 | -0.2 |

| Predom. Non-Food Stores1 | 6.4 | 4.4 | 1.1 | 1.4 | 1.5 | 0.7 | -1.5 | 3.6 | -1.8 | -0.2 |

| Non-Store Retailing1 | 12.0 | 13.1 | 2.1 | 5.6 | 5.8 | 3.6 | 1.1 | 0.3 | 4.5 | 1.5 |

| Trade | ||||||||||

| Balance2 3 | -36.2 | -38.7 | -10.0 | -12.7 | .. | -4.1 | -5.7 | -2.2 | -4.7 | .. |

| Exports4 | -1.2 | -0.6 | 2.1 | 1.6 | .. | -4.9 | 0.5 | 4.0 | 0.1 | .. |

| Imports4 | -1.6 | -0.1 | 1.5 | 3.4 | .. | -2.4 | 3.9 | -3.5 | 5.5 | .. |

| Public Sector Finances | ||||||||||

| PSNB-ex3 5 | -0.6 | -23.1 | -4.5 | -2.0 | -0.3 | -0.2 | -1.7 | -1.0 | -0.6 | 1.3 |

| PSND-ex as a % GDP | 83.9 | 84.8 | 84.0 | 84.1 | 83.3 | 83.9 | 84.1 | 83.3 | 83.4 | 83.3 |

| Source: Office for National Statistics | ||||||||||

| Notes: | ||||||||||

| 1. Percentage change on previous period, seasonally adjusted, CVM | ||||||||||

| 2. Levels, seasonally adjusted, CP | ||||||||||

| 3. Expressed in £ billion | ||||||||||

| 4. Percentage change on previous period, seasonally adjusted, CP | ||||||||||

| 5. Public Sector net borrowing, excluding the impact of financial interventions. Level change on previous period a year ago, not seasonally adjusted | ||||||||||

Download this table Table 3: UK demand side indicators

.xls (30.7 kB)

Table 4: UK supply side indicators

| 2014 | 2015 | 2016 | 2016 | 2016 | 2016 | 2016 | 2016 | 2016 | 2016 | |

| Q1 | Q2 | Q3 | May | Jun | Jul | Aug | Sep | |||

| Labour Market | ||||||||||

| Employment Rate1 2 | 72.9 | 73.7 | 74.2 | 74.5 | .. | 74.5 | 74.5 | 74.5 | .. | .. |

| Unemployment Rate1 3 | 6.2 | 5.4 | 5.1 | 4.9 | .. | 4.9 | 4.9 | 4.9 | .. | .. |

| Inactivity Rate1 4 | 22.2 | 22.0 | 21.7 | 21.6 | .. | 21.6 | 21.5 | 21.5 | .. | .. |

| Claimant Count Rate 7 | 3.0 | 2.3 | 2.2 | 2.2 | 2.3 | 2.2 | 2.2 | 2.2 | 2.3 | 2.3 |

| Total Weekly Earnings6 | £480 | £491 | £497 | £502 | .. | £502 | £502 | £505 | £504 | .. |

| CPI | ||||||||||

| All-item CPI5 | 1.5 | 0.0 | 0.3 | 0.4 | 0.7 | 0.3 | 0.5 | 0.6 | 0.6 | 1.0 |

| Transport5 | 0.3 | -2.1 | -0.6 | -0.9 | 0.8 | -1.0 | -0.2 | 0.2 | 1.0 | 1.2 |

| Recreation &Culture5 | 0.9 | -0.6 | -0.1 | 0.5 | 0.7 | 0.1 | 0.8 | 0.6 | 0.7 | 0.8 |

| Utilities5 | 3.0 | 0.5 | 0.4 | 0.0 | 0.0 | 0.0 | 0.1 | -0.1 | -0.1 | 0.2 |

| Food & Non-alcoh Bev5 | -0.2 | -2.6 | -2.5 | -2.7 | -2.3 | -2.8 | -2.9 | -2.6 | -2.2 | -2.3 |

| PPI | ||||||||||

| Input8 | -6.6 | -12.8 | -7.6 | -4.1 | 6.4 | -4.3 | -0.5 | 4.3 | 7.8 | 7.2 |

| Output8 | 0.0 | -1.7 | -1.0 | -0.4 | 0.8 | -0.5 | -0.2 | 0.4 | 0.9 | 1.2 |

| HPI8 | 8.0 | 5.9 | 7.9 | 8.7 | .. | 8.7 | 9.4 | 8.0 | 8.4 | .. |

| Source: Office for National Statistics | ||||||||||

| Notes: | ||||||||||

| 1. Monthly data shows a three month rolling average(e.g. The figure for November is for the three months ending in November) | ||||||||||

| 2. Headline employment figure is the number of people aged 16-64 in employment divided by the total population 16-64 | ||||||||||

| 3. Headline unemployment figure is the number of unemployed people (aged 16+) divided by the economically active population (aged 16+) | ||||||||||

| 4. Headline inactivity figure is the number of economically active people aged 16-64 divided by the 16-64 population | ||||||||||

| 5. Percentage change on previous period a year ago, seasonally adjusted | ||||||||||

| 6. Estimates of total pay include bonuses but exclude arrears of pay (£) | ||||||||||

| 7. Calculated by JSA claimants divided by claimant count plus workforce jobs | ||||||||||

| 8. Percentage change on previous period a year ago, non-seasonally adjusted | ||||||||||