Table of contents

- Main points

- Things you need to know about this release

- Narrowing of the UK current account deficit

- Narrowing trade deficit in Quarter 3 2017

- Earnings on investment abroad narrows deficit on primary income

- Financial account shows a net inflow to the UK

- International investment position

- Quality and methodology

1. Main points

The UK’s current account deficit was £22.8 billion (4.5% of gross domestic product) in Quarter 3 (July to Sept) 2017, a narrowing of £3.0 billion from a revised deficit of £25.8 billion (5.1% of gross domestic product) in Quarter 2 (Apr to June) 2017.

The narrowing in the current account deficit was driven by a narrowing of the deficits on primary income by £1.8 billion, secondary income by £1.0 billion and total trade by £0.3 billion in Quarter 3 2017.

The primary income deficit narrowed to £11.4 billion in Quarter 3 2017, mostly due to UK earnings on investment abroad, which increased by £3.6 billion, partially offset by payments increasing by £1.8 billion.

The international investment position shows UK net liabilities of £207.6 billion at the end of Quarter 3 2017.

2. Things you need to know about this release

In accordance with the National Accounts Revisions Policy, the revision period for this release is open from Quarter 1 (Jan to Mar) 2016. Revisions from Quarter 1 (Jan to Mar) 2016 reflect the introduction of annual benchmarks from the 2016 Foreign Direct Investment survey and the Financial Inquiries surveys, new and revised survey data, new estimates from the Bank for International Settlements, and a reassessment of seasonal factors.

During 2017 there have been numerous large acquisitions of foreign companies by UK investors, most notably in Quarter 3 (July to Sept) 2017. Some of the impacts on the accounts are outlined in section 6, the financial account. Currently, we have all the relevant details of the financial account transactions; however, we do not have final information on certain business structure changes and therefore have an incomplete stock position in the international investment position (IIP). As further information becomes available, we will reflect it in the IIP at the earliest opportunity. Further information can also be found in the Mergers and acquisitions involving UK companies statistical bulletin.

A brief introduction to the UK Balance of Payments provides an overview of the concepts and coverage of the UK Balance of Payments using the Balance of Payments Manual sixth edition.

The Balance of payments (BoP) Quality and Methodology Information (QMI) report is available.

Also available is an overview of how movements in foreign exchange rates can impact the balance of payments and international investment position.

Office for National Statistics (ONS), like all government departments, has to ensure all of its outputs meet accessibility guidelines. As a result, from the Quarter 4 (Oct to Dec) 2017 (29 March 2018) release onwards, we will no longer be publishing a PDF file of the UK Economic Accounts (UKEA). The data contained in the current PDF file will continue to be available within the UKEA dataset and reference tables that are currently published.

Back to table of contents3. Narrowing of the UK current account deficit

In Quarter 3 (July to Sept) 2017, the UK current account deficit was £22.8 billion and equates to 4.5% of gross domestic product (GDP) at current market prices. This was a narrowing from a revised deficit of £25.8 billion (5.1% of GDP) in Quarter 2 (Apr to June) 2017 (Figure 1).

Figure 1: UK balances as a percentage of gross domestic product

Quarter 4 (Oct to Dec) 2014 to Quarter 3 (July to Sept) 2017

Source: Office for National Statistics

Notes:

- Q1 refers to Quarter 1 (Jan to Mar), Q2 refers to Quarter 2 (Apr to June), Q3 refers to Quarter 3 (July to Sept) and Q4 refers to Quarter 4 (Oct to Dec).

Download this chart Figure 1: UK balances as a percentage of gross domestic product

Image .csv .xlsThe main driver of the reduction to the current account deficit was the primary income account, which narrowed to a deficit of £11.4 billion (or 2.2% of GDP) in Quarter 3 2017, compared with a revised deficit of £13.2 billion (or 2.6% of GDP) in Quarter 2 2017 (see section 5 for more information). In addition, the deficit on the secondary income account narrowed by £1.0 billion to £5.5 billion (or 1.1% of GDP), with payments decreasing by £0.7 billion and receipts increasing by £0.3 billion.

Notes for: Narrowing of the UK current account deficit

- Throughout this release Quarter 1 refers to January to March, Quarter 2 refers to April to June, Quarter 3 refers to July to September, and Quarter 4 refers to October to December.

4. Narrowing trade deficit in Quarter 3 2017

The total trade deficit narrowed slightly to £5.8 billion in Quarter 3 (July to Sept) 2017. This was mostly due to the surplus on trade in services increasing by £1.5 billion in Quarter 3 2017, which was partially offset by a widening of the deficit on trade in goods, which widened by £1.2 billion.

Figure 2: UK trade in goods and services balances (seasonally adjusted)

Quarter 4 (Oct to Dec) 2014 to Quarter 3 (July to Sept) 2017

Source: Office for National Statistics

Notes:

- Q1 refers to Quarter 1 (Jan to Mar), Q2 refers to Quarter 2 (Apr to June), Q3 refers to Quarter 3 (July to Sept) and Q4 refers to Quarter 4 (Oct to Dec).

Download this chart Figure 2: UK trade in goods and services balances (seasonally adjusted)

Image .csv .xlsThe trade in services surplus increased by £1.5 billion to a record £27.7 billion in Quarter 3 2017 (Figure 2). This was due to exports increasing by £1.2 billion and imports decreasing by £0.3 billion. Exports of services increased to £70.0 billion due to exports of other business services increasing by £0.5 billion, exports of financial services increasing by £0.3 billion and exports of travel services increasing by £0.2 billion. Imports of services decreased to £42.3 billion due to imports of other business services decreasing by £0.7 billion, which was partially offset by small increases elsewhere.

The widening in the trade in goods deficit was due to imports increasing more than exports. Imports of goods increased by £2.0 billion to £120.4 billion in Quarter 3 2017; of which, imports of finished manufactured goods increased by £0.8 billion, imports of oil increased by £0.5 billion and imports of other fuels increased by £0.6 billion.

Meanwhile, exports of goods increased by just £0.7 billion in Quarter 3 2017 to £86.8 billion. This was due mainly to finished manufactured goods, which increased by £1.0 billion, along with increases in exports of food, beverages and tobacco, which increased by £0.4 billion, and unspecified goods, which increased by £0.3 billion. These increases were partially offset by a decrease to exports of semi-manufactured goods, which decreased by £0.9 billion.

Notes for: Narrowing trade deficit in Quarter 3 2017

- Throughout this release Quarter 1 refers to January to March, Quarter 2 refers to April to June, Quarter 3 refers to July to September, and Quarter 4 refers to October to December.

5. Earnings on investment abroad narrows deficit on primary income

The primary income deficit narrowed by £1.8 billion in Quarter 3 (July to Sept) 2017 to £11.4 billion (Figure 3), with receipts increasing by £3.6 billion and payments rising by £1.8 billion. The narrowing of the deficit in Quarter 3 2017 was due primarily to UK net foreign direct investment (FDI) earnings increasing in Quarter 3 2017, due to the value of credits increasing and debits staying constant over the quarter.

Figure 3: UK primary income account balances (seasonally adjusted)

Quarter 4 (Oct to Dec) 2014 to Quarter 3 (July to Sept) 2017

Source: Office for National Statistics

Notes:

- Q1 refers to Quarter 1 (Jan to Mar), Q2 refers to Quarter 2 (Apr to June), Q3 refers to Quarter 3 (July to Sept) and Q4 refers to Quarter 4 (Oct to Dec).

Download this chart Figure 3: UK primary income account balances (seasonally adjusted)

Image .csv .xlsThe value of FDI earnings generated by UK investors abroad (credits) increased in Quarter 3 2017, continuing the broadly upwards trend from 2016. Credits in Quarter 3 2017 increased by £2.9 billion to £20.8 billion from the previous quarter. This is the highest quarterly value since Quarter 3 2013.

The value of earnings generated by overseas investors on direct investment in the UK (debits) was virtually unchanged in Quarter 3 2017. This is the second quarter in a row in which the value of debits has been above £17 billion (Figure 4). Net FDI earnings had been increasing over the five quarters to Quarter 1 (Jan to Mar) 2017, taking it from negative to positive net earnings before falling slightly in Quarter 2 (Apr to June) 2017.

Figure 4: Quarterly foreign direct investment earnings (seasonally adjusted)

Quarter 2 (Apr to June) 2011 to Quarter 3 (July to Sept) 2017

Source: Office for National Statistics

Notes:

- Q1 refers to Quarter 1 (Jan to Mar), Q2 refers to Quarter 2 (Apr to June), Q3 refers to Quarter 3 (July to Sept) and Q4 refers to Quarter 4 (Oct to Dec).

Download this chart Figure 4: Quarterly foreign direct investment earnings (seasonally adjusted)

Image .csv .xlsNotes for: Earnings on investment abroad narrows deficit on primary income

- Throughout this release Quarter 1 refers to January to March, Quarter 2 refers to April to June, Quarter 3 refers to July to September, and Quarter 4 refers to October to December.

6. Financial account shows a net inflow to the UK

The total financial account showed a net inflow (that is, more money flowing into the UK) of £16.5 billion in Quarter 3 (July to Sept) 2017, compared with a revised net inflow of £26.7 billion in Quarter 2 (Apr to June) 2017 (Figure 5).

Figure 5: UK financial account balances (not seasonally adjusted)

Quarter 4 (Oct to Dec) 2014 to Quarter 3 (July to Sept) 2017

Source: Office for National Statistics

Notes:

- Q1 refers to Quarter 1 (Jan to Mar), Q2 refers to Quarter 2 (Apr to June), Q3 refers to Quarter 3 (July to Sept) and Q4 refers to Quarter 4 (Oct to Dec).

- Total includes reserve assets.

Download this chart Figure 5: UK financial account balances (not seasonally adjusted)

Image .csv .xlsIn Quarter 3 2017, direct investment recorded a net outflow (that is, more money flowing out of the UK) of £30.3 billion. Within direct investment, the UK was a net investor abroad in equity capital of £28.0 billion, the highest since Quarter 4 (Oct to Dec) 2007 when it was £30.8 billion. The increase to direct investment abroad reflects a small number of high-value mergers and acquisitions that completed in Quarter 3 2017, as outlined in the Mergers and acquisitions involving UK companies: July to September 2017 statistical bulletin.

Portfolio investment recorded a net inflow (that is, more money flowing into the UK) of £46.2 billion in Quarter 3 2017, compared with a net outflow (that is, more money flowing out of the UK) of £13.5 billion in Quarter 2 2017. The inflow in Quarter 3 2017 was mainly due to a net flow of investment into the UK of £37.2 billion, with foreign investors investing in UK equities (£20.0 billion) and UK debt securities (£17.2 billion).

Additionally, there was a net inflow of £9.0 billion as UK residents were net sellers of portfolio investment abroad. This was mostly due to disinvestment in foreign equities to the value of £23.7 billion by the following sectors:

- monetary financial institutions (£9.8 billion)

- insurance companies and pension funds (£11.2 billion)

- other financial intermediaries (£4.7 billion)

Partially offsetting the disposal of foreign equities, UK residents continued to invest in foreign debt securities (£14.7 billion) in Quarter 3 2017.

Despite net selling of foreign equities (£23.7 billion), Figure 6 shows that this has been more than offset by the continued strength of foreign stock markets (price changes) in Quarter 3 2017 and resulted in an increase of £21.2 billion to the international investment position (IIP) equity asset position.

Figure 6: Total quarterly change in IIP equity assets broken down into impacts

Quarter 4 (Oct to Dec) 2011 to Quarter 3 (July to Sept) 2017

Source: Office for National Statistics

Notes:

- Q1 refers to Quarter 1 (Jan to Mar), Q2 refers to Quarter 2 (Apr to June), Q3 refers to Quarter 3 (July to Sept) and Q4 refers to Quarter 4 (Oct to Dec).

Download this chart Figure 6: Total quarterly change in IIP equity assets broken down into impacts

Image .csv .xlsFinancial derivatives and employee stock options showed net settlement receipts of £3.7 billion in Quarter 3 2017, following net settlement receipts of £4.8 billion in Quarter 2 2017.

Other investment in Quarter 3 2017 recorded a net inflow (that is, more money flowing into the UK) of £4.4 billion, compared with a net inflow of £59.6 billion in Quarter 2 2017.

Notes for: Financial account shows a net inflow to UK

- Throughout this release Quarter 1 refers to January to March, Quarter 2 refers to April to June, Quarter 3 refers to July to September, and Quarter 4 refers to October to December.

7. International investment position

The international investment position showed net external liabilities (that is, liabilities exceeds assets) of £207.6 billion at the end of Quarter 3 (July to Sept) 2017, compared with net external liabilities of £225.1 billion at the end of Quarter 2 (Apr to June) 2017 (Figure 7).

Figure 7: UK international investment position (not seasonally adjusted)

Quarter 4 (Oct to Dec) 2014 to Quarter 3 (July to Sept) 2017

Source: Office for National Statistics

Notes:

- Q1 refers to Quarter 1 (Jan to Mar), Q2 refers to Quarter 2 (Apr to June), Q3 refers to Quarter 3 (July to Sept) and Q4 refers to Quarter 4 (Oct to Dec).

Download this chart Figure 7: UK international investment position (not seasonally adjusted)

Image .csv .xlsUK assets fell by £10.7 billion to £10,560.8 billion in Quarter 3 2017. UK external liabilities dropped £28.2 billion in Quarter 3 2017 to £10,768.3 billion; the lowest level since Quarter 1 (Jan to Mar) 2016.

The total net direct investment position increased by £8.0 billion in Quarter 3 2017 to a net liability position of £16.7 billion. In fact, foreign direct investment (FDI) net positions were similar for the first three quarters of 2017, as the values of both FDI assets and liabilities stayed relatively constant over those quarters. This followed the values of both assets and liabilities increasing over the successive quarters of 2016. These 2016 trends were partly explained by the impact of exchange rate movements on the value of assets, in addition to very high-value inward mergers and acquisitions on liabilities. It can also be seen that the quarterly values of assets and liabilities so far in 2017 have all been below their respective values in Quarter 4 (Oct to Dec) 2016.

These trends in quarterly assets and liabilities have seen the UK net FDI international investment position decrease to be around zero by the end of 2016 (Figure 8). This implies that the UK has become less of a net direct investor overseas, to the point that the stock of FDI assets held abroad by UK residents is similar to the stock of FDI liabilities non-UK residents hold in the UK.

Figure 8: Quarterly foreign direct investment positions

Quarter 3 (July to Sept) 2011 to Quarter 3 (July to Sept) 2017

Source: Office for National Statistics

Notes:

- Q1 refers to Quarter 1 (Jan to Mar), Q2 refers to Quarter 2 (Apr to June), Q3 refers to Quarter 3 (July to Sept) and Q4 refers to Quarter 4 (Oct to Dec).

Download this chart Figure 8: Quarterly foreign direct investment positions

Image .csv .xls

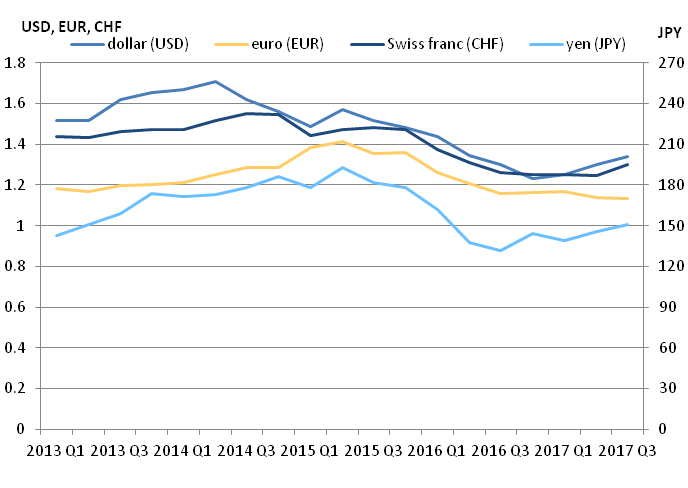

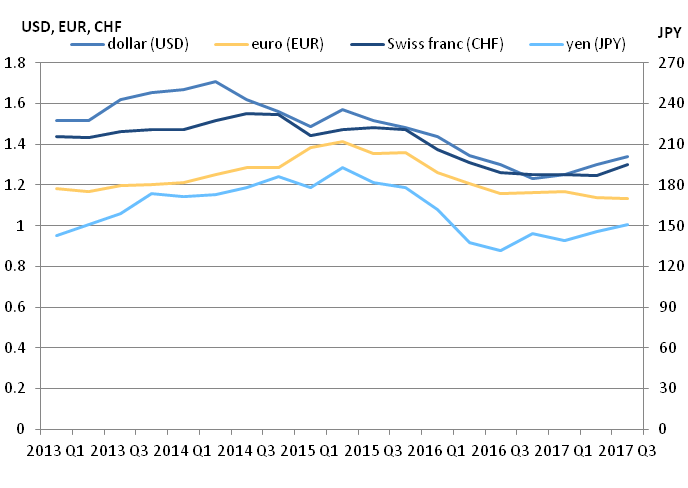

Figure 9: Sterling exchange rates with major trading partners

Quarter 1 (Jan to Mar) 2013 to Quarter 3 (July to Sept) 2017

Source: Office for National Statistics

Notes:

- Q1 refers to Quarter 1 (Jan to Mar), Q2 refers to Quarter 2 (Apr to June), Q3 refers to Quarter 3 (July to Sept) and Q4 refers to Quarter 4 (Oct to Dec).

Download this image Figure 9: Sterling exchange rates with major trading partners

.png (27.6 kB) .xls (28.7 kB){kind=link}

Figure 9 presents sterling exchange rates against the currencies of major trading partner countries at the close of markets at each quarter end. At the end of Quarter 3 2017, the sterling exchange rate against a basket of foreign currencies remained virtually unchanged when compared with the end of Quarter 2 2017.

However, when looking at the detail, it appreciated against several major currencies including the US dollar, the Swiss franc and the Japanese yen. Sterling showed a slight depreciation against the Euro in Quarter 3 2017 and stands at the lowest rate since Quarter 2 2011.

The stock of UK assets and liabilities with the rest of the world can be influenced by movements in exchange rates and price revaluations. On balance, exchange rate movements in Quarter 3 2017 have had less of an impact than the previous year. Table 1 summarises which type of investment is impacted by these changes.

Table 1: Revaluation impacts on investments

| Assets | Liabilities | |||

|---|---|---|---|---|

| Exchange rate movements | Price revaluations | Exchange rate movements | Price revaluations | |

| Direct Investment | Impact | Impact | No impact | Impact |

| Portfolio Investment | ||||

| Equities | Impact | Impact | No impact | Impact |

| Debt Securities | Impact | Impact | No impact | Impact |

| Other Investment | ||||

| Deposits | Impact | No impact | Impact | No impact |

| Loans | Impact | No impact | Impact | No impact |

| Source: Office for National Statistics | ||||

| Notes: | ||||

| 1. Q1 refers to Quarter 1 (Jan to Mar), Q2 refers to Quarter 2 (Apr to June), Q3 refers to Quarter 3 (July to Sept) and Q4 refers to Quarter 4 (Oct to Dec). | ||||

Download this table Table 1: Revaluation impacts on investments

.xls (33.3 kB)Notes for: International investment position

- Throughout this release Quarter 1 refers to January to March, Quarter 2 refers to April to June, Quarter 3 refers to July to September, and Quarter 4 refers to October to December.

8. Quality and methodology

The Balance of payments (BoP) Quality and Methodology Information report contains important information on:

- the strengths and limitations of the data and how it compares with related data

- uses and users of the data

- how the output was created

- the quality of the output including the accuracy of the data