1. Main points

- Membership of defined contribution (DC) occupational pension schemes was 22.4 million at the end of 2019, compared with 18.3 million for funded defined benefit and hybrid (DBH) pension schemes.

- Employees’ and employers’ contributions to DC pension schemes rose rapidly in 2018 and 2019 as a result of auto-enrolment, reaching £6.3 billion and £14.1 billion respectively in 2019.

- Over 60% of private sector DBH employers’ pension contributions in Quarter 4 (Oct to Dec) 2019 were deficit reduction contributions.

- Of total benefits paid of £16.3 billion in Quarter 4 2019, three-quarters were from private sector DBH pension schemes.

- Market value of pension funds reached £2.2 trillion at the end of 2019, while gross assets excluding derivatives was £2.4 trillion.

- Gross assets excluding derivatives of private sector DC schemes reached £146 billion at the end of 2019; DC schemes invested almost entirely via pooled investment vehicles.

- Gross assets excluding derivatives of private sector DBH schemes were £1,859 billion at the end of 2019; 55% were direct investments, 39% were via pooled investment vehicles and 6% were in the form of insurance policies.

- At the end of 2019, nearly 70% of direct investments of private sector employee schemes were in long-term debt securities, of which three-quarters was in UK Gilts.

- At the end of 2019, 60% of direct investments of public sector employee schemes were in equities and unquoted private equity and alternatives.

- Derivatives balances of occupational pension schemes were around £300 billion at the end of 2019, with most held by private sector employee schemes.

- Repos accounted for 89% of pension schemes’ £191 billion of non-pension liabilities at the end of 2019.

- At the end of 2019, 70% of schemes’ equities held as direct investments were issued overseas, but most bonds held as direct investments were issued in the UK.

- At the end of 2019, 29% of the value of investment via pooled vehicles related to overseas-registered vehicles, of which over half was held in vehicles registered in Ireland.

2. Introduction

The Office for National Statistics (ONS) replaced the MQ5 Pension Funds Survey (PFS) with the Financial Survey of Pension Schemes (FSPS) from Quarter 2 (Apr to June) 2019. The FSPS is a quarterly survey that collects data on income and expenditure, transactions, assets and liabilities of UK funded occupational pension schemes.

The ONS has now analysed the results from three quarters of FSPS data collection – Quarter 2, Quarter 3 (July to Sept) and Quarter 4 (Oct to Dec) 2019 – and is satisfied that they are of good quality. This is a result of the work to redevelop the survey and improve its design, as discussed in Section 4: Survey redevelopment and Section 5: Survey design. Therefore, we are publishing the first set of results (see Section 6: FSPS results).

Like its predecessor, the FSPS collects information for the UK National Accounts and UK Balance of Payments (BoP). The results of the new survey, including pension contributions and benefit payments, have already started to feed into the national accounts and economic statistics including gross domestic product (GDP) and the household saving ratio. They will soon be incorporated into the national accounts supplementary table on pensions, which brings together information on UK pension schemes’ liabilities, and the enhanced financial accounts (flow of funds) work to improve the coverage, quality and granularity of UK financial statistics. The FSPS results also form part of ONS submissions to international organisations such as the European statistics agency (Eurostat), the Organisation for Economic Co-operation and Development (OECD), and the International Monetary Fund (IMF). They are used by government and international bodies to inform decision-making and by the pensions industry and pensions researchers.

The FSPS is designed to be able to monitor changes in pension schemes’ financial flows and balances. For instance, in 2020, if the economic downturn produced by the coronavirus (COVID-19) pandemic has an impact on pension contributions, the survey should pick this up. The ONS will be monitoring any such changes and keeping a close watch on any consequences that they may have for important economic indicators.

The FSPS is also designed to track changes over longer periods, such as the shift in UK pension provision from defined benefit (DB) to defined contribution (DC) pensions (see Section 8: Glossary). This shift began with the closure of many private sector DB schemes from the early 2000s, a trend that accelerated following the 2008 to 2009 financial crisis. It sped up with the expansion of DC multi-employer schemes to meet employers’ obligations under the government’s automatic enrolment policy (see Section 8: Glossary), introduced from 2012.1 The FSPS results, as published in this article, showed that at the end of 2019, DB schemes accounted for 94% of total gross assets of funded occupational pension schemes (excluding derivatives), while DC schemes made up only 6%. However, as active membership of private sector DB schemes continues to fall and membership of DC schemes rises, these proportions will change. Already in Quarter 4 2019, 65% of total employee pension contributions were in DC schemes and DC pension assets were growing. A shift of this kind is likely to have consequences for the UK economy, so the new survey is designed to report on it.

Notes for: Introduction

- See the Occupational Pension Schemes Survey (OPSS) statistical bulletins and accompanying data sets; and Employee workplace pensions in the UK – analysis of the Annual Survey of Hours and Earnings (ASHE).

3. Coverage of the survey

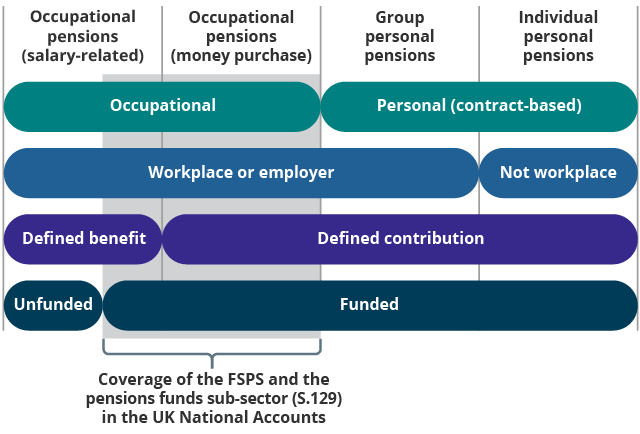

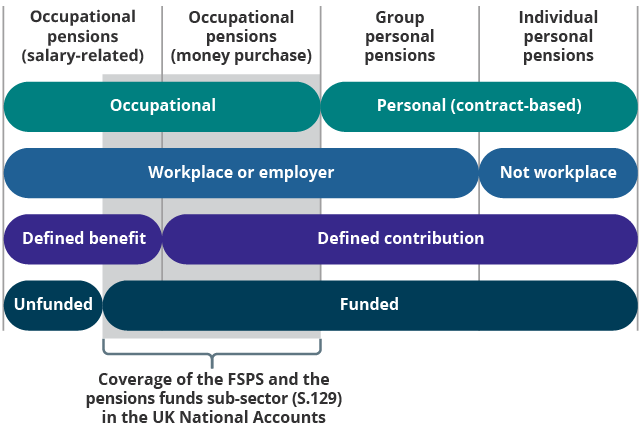

The Financial Survey of Pension Schemes (FSPS) reports on UK funded occupational pension schemes. Figure 1 shows the demarcation of the survey and of pension funds sub-sector S.129 in the UK National Accounts, where the survey data is used. All occupational schemes that are funded (see Section 8: Glossary) are in the survey, and these may be defined benefit (DB) or defined contribution (DC) (see Section 8: Glossary). In practice, this means that all occupational schemes for private sector employees are in the survey, but the survey does not include all occupational schemes for public sector employees: funded schemes for public sector employees such as the Local Government Pension Scheme (LGPS) are included, but unfunded schemes such as those for civil servants, teachers and NHS staff are not.

As the FSPS only covers occupational pension schemes, personal (contract-based) pensions provided by insurance companies are not covered by this survey. These are all DC and may be group (workplace-related) or individual (not workplace-related) pensions. In the national accounts, personal pensions are part of the insurance companies sub-sector S.128. The data for them come from other Office for National Statistics (ONS) financial surveys and regulatory sources.

Figure 1: Funded occupational pension schemes are part of the UK pension system

Source: Adapted from ‘Pensions: Challenges and Choices, the First Report of the Pensions Commission’, Pensions Commission 2004

Notes:

- The pension system shown here is for private pensions only (state pensions are not included).

Download this image Figure 1: Funded occupational pension schemes are part of the UK pension system

.png (41.3 kB){kind=link}

The FSPS, like its predecessor the MQ5 Pension Funds Survey (PFS), is principally designed to report on financial flows and balances of pension schemes. In addition to the kind of data collected previously by the PFS, the FSPS collects data on membership. The inclusion of membership in the FSPS data collection allowed the ONS to cease the Occupational Pension Schemes Survey (OPSS) after 35 years of data collection. Membership data remain indispensable for pensions policy analysis.

This article is about the FSPS, which – like the PFS and OPSS – is a survey of pension schemes. Although not discussed in this article, the ONS also collects pensions information from employers using the Annual Survey of Hours and Earnings (ASHE) and from households using the Wealth and Assets Survey (WAS). The FSPS, ASHE and WAS complement each other because pension schemes, employers and households are each able to provide different information.

4. Survey redevelopment

The replacement of the paper-based MQ5 Pension Funds Survey (PFS) with the online Financial Survey of Pension Schemes (FSPS) took place over 15 months between February 2018 and May 2019. The general objectives of the redevelopment were to move the survey from paper to online, to bring it into line with the latest requirements and definitions of the UK National Accounts and recent changes in the pensions industry and policy environment, and to improve the quality and granularity of the results. The specific objectives included:

- to produce separate estimates for funded public sector employee pension schemes and private sector employee pension schemes

- to produce separate estimates for defined benefit (DB) pensions and defined contribution (DC) pensions

- to produce a “look-through” for pooled investment vehicles, without which we cannot see the asset allocation of schemes investing through such vehicles

- to improve the sampling frame by using data from The Pensions Regulator’s (TPR’s) register of all UK funded occupational pension schemes (see Section 5: Survey design) instead of the Pension Funds Online list used by the PFS

- to produce balances and transactions data quarterly, avoiding the annual balance sheet reconciliation process of the PFS, which was challenging for our national accounts teams

- to improve efficiency for survey respondents and the Office for National Statistics (ONS) data validation team by removing inconsistencies in the old questionnaire that led to repetitious queries

Redeveloping the questionnaires

Much of the 15-month period of the survey redevelopment was dedicated to developing the questionnaire for the new survey.

Understanding data requirements

First, a team of pensions experts and methodologists within the ONS looked at the main purposes of the survey: supplying data for the UK National Accounts, UK Balance of Payments (BoP) and related products; meeting our obligations towards international organisations; and providing information for pensions policy analysis. We analysed what data the survey needed to collect (including future requirements, where known) in relation to each of these purposes. A principle of the survey redevelopment was to keep respondent burden to a minimum by not collecting information that would not be used.

The team then looked at where the paper PFS questionnaires – which consisted of two quarterly forms (income and expenditure and transactions and balances) and an annual balance sheet form – met existing and future needs and where they did not. Our aim was to maintain continuity between the old and new surveys to preserve time series (see Section 6: FSPS results). However, following the principle of minimum respondent burden, we wanted to remove any questions for which there was no longer a need or use.

Consulting and testing

Having understood the data needs, we designed a first version of the data collection instrument in the form of an electronic questionnaire. In April and May 2018, the ONS pensions team met with experts from the Department for Work and Pensions (DWP), TPR, Financial Conduct Authority (FCA) and Debt Management Office (DMO) and with pensions industry specialists including the Pensions and Lifetime Savings Association (PLSA). After incorporating their comments and producing a second version of the electronic questionnaire, ONS methodologists, accompanied by a pensions specialist, undertook testing with potential survey respondents in July and August 2018. Those selected to take part in the test included schemes for public and private sector employees and for DB, DC and hybrid (see Section 8: Glossary) pensions.

The testing used cognitive testing techniques, which study the ways in which individuals mentally process and respond to survey questionnaires, including how they understand the questions and answer them. The interviewers also asked how the data would be obtained, who would be involved in completing the survey (including any external suppliers), and whether they would prefer the new survey to be an electronic questionnaire or a spreadsheet-based questionnaire.

The first round of testing in July and August 2018 shed light on many things that could be improved, including guidance and definitions. Interviewees also noted that aligning the questions as closely as possible to modern pension scheme accounting frameworks would help them to provide the data. They expressed a preference for a spreadsheet-based questionnaire because pension scheme administrators and accountants generally work with spreadsheets for financial reporting.

For the second round of testing between October and December 2018, we decided to test a spreadsheet-based questionnaire. We also realised that we needed to specifically invite investment professionals to be part of the testing, as they often provide the information for the “investment side” of the survey (balances, transactions and related investment information).

In October and December 2018, in addition to testing the questionnaire with potential survey respondents, we had meetings with third-party data suppliers (administrators and custodians) who provided helpful advice. Finally, we talked to the Chartered Institute of Public Finance and Accountancy (CIPFA) about public sector employee schemes.

The design of the questionnaire went through many versions from April to December 2018 as we modified it to incorporate the findings from the testing process. The final design preserved our essential requirements for the survey but dropped some breakdowns to avoid overburdening respondents. For example, we originally hoped to be able to identify pension payments to dependents separately from payments to original members, to meet one of our international reporting requirements. However, we dropped this breakdown when we found that this is not available as part of standard scheme reporting and respondents said it would be costly to produce.

At the beginning of 2019, we finalised our spreadsheet-based questionnaire and the ONS’s user testing team visited several pension schemes to observe how it was used in a real-life environment. The user testing results were positive, and the process of questionnaire design was complete.

Advance warning

At the request of several people who were interviewed during the testing process, the new questionnaire was made available on a new FSPS web page on the ONS website in February 2019, four months before the FSPS was due to go live. Letters were sent out to respondents at the same time, giving advance notice of the introduction of the FSPS from Quarter 2 (Apr to June) 2019 and providing a link to the questionnaire. This allowed time for respondents and data providers to redevelop their internal systems to meet the new requirements and to train their staff.

This “advance warning” smoothed the way for a successful introduction of the new survey. By the time requests to complete the FSPS were sent to respondents, at the end of June 2019, most were prepared for the change. As a result, in the first quarter of data collection (Quarter 2 2019), response rates were good and data quality surpassed our expectations (see Section 5: Survey design).

Moving the survey online

In addition to the spreadsheet-based questionnaire, moving the survey online required work in several areas:

- the FSPS was included in the ONS’s Secure Data Collection system, a platform for respondents to download and upload questionnaires and communicate with respondents

- an automated data processing system was built to extract data from the FSPS questionnaires, run data validation checks and produce results for the over 5,000 variables (see Section 5: Survey design)

- members of the ONS surveys team who specialise in checking financial surveys (including pensions) data learnt to work with the new questionnaire and data validation systems (see Section 5: Survey design).

5. Survey design

Sampling methods

For the Financial Survey of Pension Schemes (FSPS), we take a sample from an extract of The Pensions Regulator’s (TPR’s) register of UK funded occupational pension schemes. This is an improvement on the Pension Funds Online list used by the MQ5 Pension Funds Survey (PFS), which suffered from incomplete coverage of the population. For the FSPS, we select the sample having excluded small self-administered schemes (SSASs) and executive pension plans (EPPs) where they are identifiable.

The sample is designed as a stratified random sample with the strata defined by benefit type – defined benefit and hybrid (DBH) and defined contribution (DC) – and by membership size. To do this, we take an extract from TPR’s register and restructure it to create three lists of “sampling units” covering:

- list one: those classified for the purposes of national accounts as “government managed” (see Section 8: Glossary) – broadly speaking, schemes for public sector employees

- list two: those relating to schemes for private sector employees (strictly speaking, those classified as “non-government managed”) with DBH members

- list three: those with DC members

The TPR extract is either at the level of the scheme or of sections within the scheme. Once restructured based on benefit types of members (DBH and DC), the resulting sampling units are therefore a mixture of scheme, section and sub-section level. For example, a single section “mixed hybrid” arrangement that has defined benefit (DB) and DC members will become two sampling units, one in a DBH stratum and one in a DC stratum. Therefore, the DB part of it will be reported in our DBH results and the DC part in the DC results. A single section “pure” hybrid arrangement (where the member receives a benefit that is a mixture of DB and DC) will become one sampling unit in a DBH stratum and will be reported only in the DBH results; such “pure” hybrid arrangements are rare and cannot be reported separately for confidentiality reasons.

Units on list one, which we will refer to as “public sector employee schemes”, are fully enumerated; in other words, they are required to complete the survey every quarter. For those on lists two and three, which we will refer to as “private sector employee schemes”, stratum boundaries were created using the Dalenius–Hodges cumulative square root frequency method. These are shown in Table 1.

| Band | DBH | DC |

|---|---|---|

| A | 50,000 members + | 25,000 members + |

| B | 10,000 members to <50,000 members | 5,000 members to <25,000 members |

| C | 2,000 members to <10,000 members | 1,000 members to <5,000 members |

| D | >1 member to < 2,000 members | >1 member to < 1,000 members |

Download this table Table 1: The strata for the FSPS sample are defined by benefit type and membership size

.xls .csvDBH schemes, or sections with more than 10,000 members (bands A and B), and DC schemes, or sections with more than 25,000 members (band A), are fully enumerated: all schemes in these size bands are required to complete the survey every quarter. For the remaining strata (DBH bands C and D as well as DC bands B, C and D), a sample of schemes was selected at random to represent the population, using Neyman allocation to optimise the process.

We intend to keep the sample fixed for a period of 18 months (or six quarterly returns). The sample will be redrawn for Quarter 4 (Oct to Dec) 2020.

The questionnaire

The FSPS questionnaire that came out of the process of consultation and testing, described in Section 4: Survey redevelopment, uses a spreadsheet-based questionnaire to ask about all aspects of a pension scheme’s accounts, including balances, every quarter. It has over 5,000 cells (variables), which allows different pension schemes to report using the same questionnaire, filling in only those cells that are applicable to their scheme.

At first sight, the questionnaire may appear complex because there are 18 spreadsheets within a single workbook. However:

- the workbook is clearly divided into six sections: reporting information, membership, income, expenditure, balances (including transactions) and additional breakdowns

- most of the spreadsheets follow standard pension scheme accounting approaches that are familiar to pension scheme administrators, who tend to complete the sections on reporting information, membership, income and expenditure, and to investment professionals, who complete the “investment side” sections (balances and additional breakdowns)

- for those spreadsheets that go beyond the standard pension scheme accounts, the testing process ensured that respondents could understand what is required and provide the data

- some spreadsheets or parts of spreadsheets are “not applicable” for many schemes, and this is clearly indicated in the questionnaire

- where we expect to see multiple lines of data, the spreadsheets are designed to allow the respondent to copy and paste from their own sources to avoid inputting data cell by cell

The questionnaire includes – within the workbook – detailed guidance, definitions and technical instructions to help the respondent. The guidance and definitions are written in the language of pension scheme accounting and have been subject to cognitive testing to make sure they are clear. There is also additional guidance on the Office for National Statistics (ONS) website. Any internal inconsistencies between or within spreadsheets are highlighted by error messages as the respondent completes the questionnaire.

Robustness of the survey

The FSPS is conducted under the Statistics of Trade Act 1947, which means that its completion is mandatory. The survey is important for UK economic statistics (see Section 2: Introduction), but it also imposes costs on pension schemes and their members. Therefore, it is the ONS’s responsibility to ensure that the data collection process is as efficient as possible and that the results are robust, timely and meet their objectives.

Every survey redevelopment starts with the aim of doing this, but financial surveys are particularly complex and challenging. In this context, the FSPS redevelopment is a true success story.

In the first two quarters of the survey, we had response rates of 89% and 90% respectively. In the third quarter, Quarter 4 2019, the response rate was 84%, slightly lower than before because the survey return period coincided with the start of the coronavirus (COVID-19) pandemic in the UK.

The quality of the FSPS data has surpassed our expectations. ONS pensions analysts have completed the process of quality assuring the data collected in the first three quarters of the survey, checking that the results make sense and comparing them with the previous survey and with other data sources. We are confident that for Quarter 2 (Apr to June) 2019, the totals are reliable although some of the breakdowns are less robust, and for Quarter 3 (July to Sept) and Quarter 4 2019, the data quality is good at all levels. We present detailed results for Quarters 3 and 4 2019 in Section 6: FSPS results.

In addition to the improved survey design, questionnaire redevelopment and moving to an online, automated system, one more factor has contributed to the quality of the FSPS results: the work of the six members of the ONS surveys team who specialise in financial surveys and who have the task of checking the FSPS data. Using the new data validation system, this team runs the data through a series of validation tests to identify potential errors. The tests check whether all the data required has been provided and whether they are in the correct units. They also compare data returned by each respondent in the current quarter with data returned previously. Where failures are judged potentially significant to survey results, the team queries them with respondents. The work of this team using the new data validation system means that the data delivered to the analysts are almost all “clean” and results can be produced in an efficient and timely manner.

Weighting and estimation

To produce results, data are weighted up to represent the population of funded occupational pension schemes in the UK. Weights are created for each size band. For those sampling units within the fully enumerated strata (DBH bands A and B, DC band A in Table 1, and public sector employee schemes), the weight is initially set to one. For the sampled strata (DBH bands C and D as well as DC bands B, C and D in Table 1), the weight is calculated using the number of sampling units within each stratum divided by the number of sampling units selected within that stratum. The weights are then adjusted to take account of any non-response, that is, multiplied by the count of units sampled divided by the count of units that responded. Adjustments for non-response have been small in the first three quarters of the survey because response rates have been high.

We have made further modifications to the weights where respondents are reporting differently to how the lists of sampling units were originally set up. This mainly covers instances where schemes have approached the ONS to say that the data for the selected unit can only be reported at a more aggregated level, for example, where the respondent only has data available for the whole scheme but not for the specific part of the scheme selected in the sampling process.

We have also made adjustments to take account of cases where schemes, or sections of schemes, have ceased to exist for reporting purposes (referred to as “deaths”). This can be either because of the winding up of the scheme or because the scheme should not have been in scope for selection at the point the lists were set up, for instance, because it is a SSAS or EPP but was not identified as such on TPR’s register. The latter is particularly relevant for the small DC schemes (DC band D).

Back to table of contents6. FSPS results

This section presents the Financial Survey of Pension Schemes (FSPS) results so far. Results include membership, employer and employee contributions, benefits, transfers, assets and liabilities.

When presenting detailed breakdowns, we focus on the last two quarters of 2019 for which the breakdowns and the totals are judged to be robust (see Section 5: Survey design). We also present time series using the results from the MQ5 Pension Funds Survey (PFS) up to Quarter 1 (Jan to Mar) 2019 and from the FSPS thereafter.

Throughout this section, we present results with breakdowns by pension schemes for private sector employees (including those covered by the Pension Protection Fund) versus those for public sector employees1 and by defined benefit including hybrid (DBH) pensions versus defined contribution (DC) pensions. There are no DC occupational pension schemes for public sector employees, so in practice we have three categories: public sector employee schemes, which are DBH, and private sector employee schemes, which may be further divided into DBH and DC schemes.

Membership

The FSPS estimates that total membership of DC occupational pension schemes reached 22.4 million at the end of 2019 (Figure 2), more than the combined total for DBH occupational pension schemes for employees in the public and private sectors (18.3 million). Participation in occupational DC schemes has been growing rapidly since the introduction of automatic enrolment in 2012. Between the end of September and the end of December 2019, membership of DC schemes rose by 3.4%.

Figure 2: In Quarter 4 2019, membership of DC schemes rose by 3.4%, faster than increases for DBH schemes

Membership of UK funded occupational pension schemes, 30 September and 31 December 2019

Source: Office for National Statistics – Financial Survey of Pension Schemes

Notes:

- DBH = defined benefit and hybrid.

- DC = defined contribution.

Download this chart Figure 2: In Quarter 4 2019, membership of DC schemes rose by 3.4%, faster than increases for DBH schemes

Image .csv .xlsReaders should note that membership figures do not represent individuals with pensions. There are three types of membership – active, deferred and pensioner (see Section 8: Glossary) – and many people have more than one membership type. For example, someone might be working and contributing to one scheme (or section of a scheme) while being entitled to a deferred pension from another. This person would appear in the active and deferred membership categories. People taking drawdown income while still working and contributing might appear in the active and pensioner membership categories. Memberships can be thought of as “entitlements” or, in the case of DC schemes, “pension pots”. People usually build up several pots or entitlements over their working lives.

DC schemes have mainly active and deferred membership (very few pensioner members). However, it is not possible to report membership types separately for DC schemes from the FSPS. This is because while some schemes distinguish between types of membership, others only count total membership.

For DBH schemes, membership types can be reported separately. In the second half of 2019, membership of public sector employee DBH schemes was evenly spread across active, deferred and pensioner membership (Figure 3). On the other hand, membership of private sector employee DBH schemes was mainly in the deferred and pensioner categories, with active membership making up only 8% of the total (Figure 4). This reflects the closure of many private sector DBH schemes to future accruals since the early 2000s. As members with existing entitlements grow older and are not replaced by new generations of active members, such schemes are “ageing”, with many now in cashflow negative positions (see Section 8: Glossary). This affects the contributions that such schemes receive and their benefit payments; it may also influence their investment strategies.

Figure 3: Public sector employee DBH schemes have similar proportions of active, deferred and pensioner members

Membership of public sector DBH schemes by membership type, UK, 30 September and 31 December 2019

Source: Office for National Statistics – Financial Survey of Pension Schemes

Notes:

- DBH = defined benefit and hybrid.

- For definitions of active, deferred and pensioner members, please see Section 8: Glossary.

Download this chart Figure 3: Public sector employee DBH schemes have similar proportions of active, deferred and pensioner members

Image .csv .xls

Figure 4: Private sector employee DBH schemes have only 8% active membership

Membership of private sector DBH schemes by membership type, UK, 30 September and 31 December 2019

Source: Office for National Statistics – Financial Survey of Pension Schemes

Notes:

- DBH = defined benefit and hybrid.

- For definitions of active, deferred and pensioner members, please see Section 8: Glossary.

Download this chart Figure 4: Private sector employee DBH schemes have only 8% active membership

Image .csv .xlsContributions

Figure 5 shows the value of contributions by employees and employers to UK funded occupational pensions paid each year since 1992. In nominal terms, employees’ contributions were flat in the 1990s, increased slowly in the decade before the 2008 to 2009 financial crisis and fell over the following five years as many DB schemes for private sector employees closed to future accruals. Employers’ contributions grew rapidly before the 2008 to 2009 financial crisis, reflecting the increasing need for deficit reduction contributions (DRCs) in DB schemes; since then, they have shown considerable volatility as sponsors try to address deficits in a challenging economic environment.

Figure 5: Pension contributions’ growth slowed after the 2008 to 2009 financial crisis

Employees’ and employers’ pension contributions, UK, 1992 to 2019

Source: Office for National Statistics – MQ5 pension fund survey to Quarter 1 2019, Financial Survey of Pension Schemes from Quarter 2 2019

Notes:

- Employee contributions to defined contribution (DC) schemes include tax relief at source, that is, amounts claimed by the scheme from HM Revenue and Customs (HMRC) in respect of tax relief on members’ pension contributions.

Download this chart Figure 5: Pension contributions’ growth slowed after the 2008 to 2009 financial crisis

Image .csv .xlsThe introduction of automatic enrolment, or auto-enrolment, changed this pattern. Auto-enrolment was rolled out between October 2012 and February 2018, starting with large employers and finishing with small employers and new businesses. Minimum contribution rates were established and were also introduced in stages, rising in April 2018 and in April 2019 (see Section 8: Glossary).

Most of the increase in active membership associated with auto-enrolment has been in DC schemes including the multi-employer “Master Trusts”. Figure 6 shows that contributions to DC schemes started to rise from 2015.2 Employees’ contributions to DC schemes rose from £1.7 billion in 2017 to £4.8 billion in 2018; employers’ contributions to DC schemes rose from £5.5 billion to £12.0 billion. Last year (2019), employees’ contributions to DC schemes were £6.3 billion, 13 times higher than in 2009, while employers’ contributions were £14.1 billion, 10 times higher than in 2009.

Figure 6: Contributions to DC schemes rose from 2015 as the auto-enrolment programme was rolled out

Employees’ and employers’ contributions to DC pension schemes, UK, 2009 to 2019

Source: Office for National Statistics – MQ5 pension fund survey to Quarter 1 2019, Financial Survey of Pension Schemes from Quarter 2 2019

Notes:

- DC = Defined contribution.

- Employee contributions to defined contribution (DC) schemes include tax relief at source, that is, amounts claimed by the scheme from HM Revenue and Customs (HMRC) in respect of tax relief on members’ pension contributions.

Download this chart Figure 6: Contributions to DC schemes rose from 2015 as the auto-enrolment programme was rolled out

Image .csv .xlsFigures 7 and 8 show employee and employer pension contributions in the second half of 2019 according to whether they were contributions to public or private sector employee DBH schemes or private sector employee DC schemes. Readers should note the different scales on the Y axes. The largest category by value for employees’ pension contributions was DC (64% of total employees’ contributions in Quarter 4 2019), reflecting the fact that most active membership was in DC schemes. For employers’ pension contributions, on the other hand, DC was only 28% of the total and half of the value of private sector DBH employers’ contributions in Quarter 4 2019 (Figure 8).

Figure 7: Nearly two-thirds of employees’ contributions in Quarter 4 2019 were to DC schemes

Employees’ pension contributions, UK, Quarter 3 (July to Sept) and Quarter 4 (Oct to Dec) 2019

Source: Office for National Statistics – Financial Survey of Pension Schemes

Notes:

- DBH = defined benefit and hybrid.

- Employee contributions to defined contribution (DC) schemes include tax relief at source, that is, amounts claimed by the scheme from HM Revenue and Customs (HMRC) in respect of tax relief on members’ pension contributions.

Download this chart Figure 7: Nearly two-thirds of employees’ contributions in Quarter 4 2019 were to DC schemes

Image .csv .xls

Figure 8: Over 70% of employers’ contributions in Quarter 4 2019 were to DBH schemes

Employers’ pension contributions, UK, Quarter 3 (July to Sept) and Quarter 4 (Oct to Dec) 2019

Source: Office for National Statistics – Financial Survey of Pension Schemes

Notes:

- DBH = defined benefit and hybrid.

- DC = defined contribution.

Download this chart Figure 8: Over 70% of employers’ contributions in Quarter 4 2019 were to DBH schemes

Image .csv .xlsAnother way of looking at the results shown in Figure 8 is to examine why employers’ contributions to DBH schemes were high. While employers contributing to DC schemes contributed around two-thirds of the total (employees’ plus employers’ contributions) in the second half of 2019, and employers contributing to public sector DBH schemes contributed around three-quarters of the total, employers contributing to private sector DBH schemes accounted for over 95% of the total.

This can be explained firstly by the relatively old “age profile” of the schemes (private sector DBH schemes have few active members making employee contributions) and secondly by the requirement for sponsors to make DRCs to address deficits built up over the lifetime of the schemes. Figure 9 shows that 46% of private sector employers’ contributions to DBH schemes in Quarter 3 (July to Sept) 2019 were DRCs, rising to 62% in Quarter 4 2019; this compares with 9% and 13% for public sector employers.

Figure 9: Over 60% of private sector DBH employers’ contributions in Quarter 4 2019 were DRCs

Private sector DBH employers’ contributions by type of contribution, UK, Quarter 3 (July to Sept) and Quarter 4 (Oct to Dec) 2019

Source: Office for National Statistics – Financial Survey of Pension Schemes

Notes:

- DRCs = deficit reduction contributions.

- DBH = defined benefit and hybrid.

- DC = defined contribution.

Download this chart Figure 9: Over 60% of private sector DBH employers’ contributions in Quarter 4 2019 were DRCs

Image .csv .xlsA final piece of information collected by the FSPS in relation to contributions concerns salary sacrifice (see Section 8: Glossary). The survey asks whether the scheme or section is subject to a salary sacrifice arrangement, and if so whether the scheme was “fully” or “partially” subject to salary sacrifice. Figure 10 shows the results in relation to total contributions: one-third of private sector DBH contributions were in schemes that used salary sacrifice fully in Quarter 4 2019 and two-thirds were in schemes that used it fully or partially. By contrast, in the public sector, three-quarters of contributions were in schemes that did not use salary sacrifice at all (“none”). For private sector DC schemes, the largest part of contributions (53%) related to schemes that were partial users of salary sacrifice arrangements, while another 16% were in schemes that were fully subject to salary sacrifice.

Figure 10: Most contributions to private sector employee schemes are in schemes that use salary sacrifice to some extent

Total contributions by degree of salary sacrifice, UK, Quarter 4 (Oct to Dec) 2019

Source: Office for National Statistics – Financial Survey of Pension Schemes

Notes:

- DBH = defined benefit and hybrid.

- DC = defined contribution.

- Percentages are calculated based on totals excluding non-response to the salary sacrifice questions.

Download this chart Figure 10: Most contributions to private sector employee schemes are in schemes that use salary sacrifice to some extent

Image .csv .xlsBenefits

Benefit payments have increased by 43% in nominal terms since 2009 (Figure 11). By contrast, with contributions, the 2008 to 2009 financial crisis does not appear to have affected benefit payments, presumably because benefits must be paid in accordance with the scheme rules, and sponsors and administrators made every effort to meet these commitments.

The time series for benefit payments does show decreases in 2007 and 2014. The first of these and part of the second are probably because of sampling variability, where a new sample was introduced for the PFS. Such effects are a risk for any survey, but we hope that the move to using The Pensions Regulator (TPR)’s register as a sampling frame for FSPS (see Section 5: Survey design) should reduce them. Also, part of the change in 2014 may be owing to the announcement of the 2015 “pension freedoms”, which reportedly led to some pension scheme members postponing decisions to take benefits in 2014.

Figure 11: The 2008 to 2009 financial crisis did not slow the growth of benefit payments

Benefits paid, UK, 1992 to 2019

Source: Office for National Statistics – MQ5 pension fund survey to Quarter 1 2019, Financial Survey of Pension Schemes from Quarter 2 2019

Download this chart Figure 11: The 2008 to 2009 financial crisis did not slow the growth of benefit payments

Image .csv .xlsBefore the FSPS, we were not able to provide breakdowns of benefits paid by whether they were from public or private sector employee DBH schemes or from private sector employee DC schemes. Figure 12 presents this breakdown, further split by type of benefit: on the one hand, pension payments and income withdrawals, and on the other, lump sums including lump sum death benefits. Of the £16.3 billion total benefits paid in Quarter 4 2019, over three-quarters were paid by private sector DBH schemes and only 2% by private sector DC schemes. However, private sector DC schemes accounted for 11% of lump sum benefit payments.

Figure 12: Over three-quarters of total benefits in Quarter 4 2019 were paid by private sector DBH schemes

Benefits paid by type of benefit, UK, Quarter 4 (Oct to Dec) 2019

Source: Office for National Statistics – Financial Survey of Pension Schemes

Notes:

- DBH = defined benefit and hybrid.

- DC = defined contribution.

Download this chart Figure 12: Over three-quarters of total benefits in Quarter 4 2019 were paid by private sector DBH schemes

Image .csv .xlsTransfers

Transfers out of UK funded occupational pension schemes rose sharply from £12.8 billion in 2016 to £36.9 billion in 2017 (Figure 13). The PFS did not provide estimates of transfers out by whether they were from public or private sector employee DBH schemes or from private sector employee DC schemes, nor was it clear in the PFS questionnaire whether buy-ins and buyouts (see Section 8: Glossary) were to be included in transfers out. The pensions industry media reported the 2017 increase as being mainly from DB schemes, as low interest rates made cash equivalent transfer values (CETVs) attractive. Some transfers were also reported to have been made abroad as transfers to recognised overseas pension schemes (ROPS). However, the PFS did not provide evidence to support or refute such explanations.

Figure 13: Transfers out of occupational pension schemes rose sharply in 2017, followed by transfers in in 2018

Transfers in and transfers out, UK, 1992 to 2019

Source: Office for National Statistics – MQ5 pension fund survey to Quarter 1 2019, Financial Survey of Pension Schemes from Quarter 2 2019

Download this chart Figure 13: Transfers out of occupational pension schemes rose sharply in 2017, followed by transfers in in 2018

Image .csv .xlsFigure 13 also shows transfers in rising from £2.2 billion in 2017 to £9.6 billion in 2018. The PFS provided estimates of transfers in by whether they were to DB and hybrid or DC schemes. Until 2017, most transfers in were to DB and hybrid schemes. Transfers into DC schemes then rose sharply, reaching £3.8 billion (40% of the total) in 2018. In 2019, they were £5.1 billion (57% of the total). Although we cannot be sure of the reason for this, it may be associated with the expansion of multi-employer “Master Trusts” in response to the auto-enrolment programme.

Using the FSPS data, we can now present a DBH versus DC breakdown for transfers out3 as well as for transfers in, although we cannot show public sector DBH separately from private sector DBH for confidentiality reasons. The FSPS questionnaire clarifies that buyouts (but not buy-ins) are to be included in transfers out. It also asks for information on “payments to and on account of leavers” separately from transfers out; payments to and on account of leavers includes purchase of annuities and other retirement products such as drawdown.

Figure 14 shows the FSPS results for all three types of movements in and out of DBH schemes in Quarters 3 and 4 2019; Figure 15 shows the same for DC schemes (note the different scales on the Y axes).

Figure 14: There were £10 billion of transfers out of DBH schemes in Quarter 4 2019

Transfers and leavers, DBH schemes, UK, Quarter 3 (July to Sept) and Quarter 4 (Oct to Dec) 2019

Source: Office for National Statistics – Financial Survey of Pension Schemes

Notes:

- DBH = defined benefit and hybrid.

Download this chart Figure 14: There were £10 billion of transfers out of DBH schemes in Quarter 4 2019

Image .csv .xls

Figure 15: Transfers in and out of DC schemes fell in Quarter 4 2019

Transfers and leavers, DC schemes, UK, Quarter 3 (July to Sept) and Quarter 4 (Oct to Dec) 2019

Source: Office for National Statistics – Financial Survey of Pension Schemes

Notes:

- DC = defined contribution.

Download this chart Figure 15: Transfers in and out of DC schemes fell in Quarter 4 2019

Image .csv .xlsThe transfers out of DBH schemes value in Quarter 4 2019 (£10 billion) was much higher than the Quarter 3 2019 value. On the other hand, for transfers out of DC schemes, the Quarter 4 2019 value (£1.4 billion) was much lower than the previous quarter. Although these are relatively new series, it seems likely that there will be continuing quarter-to-quarter volatility for both DBH and DC transfers out because of group transfers out, including buyouts in the case of DBH schemes.

Balances

This part of the article discusses what the FSPS can tell us about UK funded occupational pension schemes’ assets and liabilities and about the nature of their investments. Some of the results presented here build on the previous survey (the PFS). Others present data collected for the first time for such schemes or results collected for the first time by official pension surveys.

The pension funds sub-sector (S.129) in the UK National Accounts is one of the largest institutional investor sectors. At the end of 2019, according to the FSPS, it had assets of between £2.2 trillion and £2.7 trillion – depending on the measure used (Table 2). The FSPS is designed to produce estimates of assets separately for public sector employee pension schemes and private sector employee pension schemes as well as for DBH and DC schemes.

The main liability of S.129 is in the form of funded occupational pension schemes’ obligations to pay pensions: the schemes’ pension liabilities, which are also the pension entitlements of the household sector in the national accounts. For DBH pensions, pension liabilities are measured on an actuarial basis in the national accounts and compiled using regulatory and administrative sources.4 For DC occupational pensions, we will be able to use the FSPS to estimate pension liabilities because liabilities are equal to assets for DC schemes. The other (non-pension) liabilities of S.129 are also reported in the FSPS.

Total assets and liabilities

The FSPS collects information on assets and liabilities of UK funded occupational pension schemes by asking for information on a gross basis, as required for the national accounts. This is used to produce the measures shown in Table 2, some of which are on a gross basis while others – in particular, “market value of pension funds” – is a net measure, created by subtracting gross liabilities (other than pension liabilities) from gross assets.

| Gross assets excluding derivatives | 2,409 |

| Gross liabilities other than pension liabilities, excluding derivatives | 191 |

| Derivatives contracts with a positive (asset) value | 303 |

| Derivatives contracts with a negative (liability) value | 291 |

| Derivatives net positions | 12 |

| Net assets excluding derivatives or 'market value of pension funds' | 2,218 |

| Gross assets including derivatives contracts with a positive (asset) value | 2,712 |

Download this table Table 2: Market value of pension funds reached £2.2 trillion at the end of 2019

.xls .csvThe PFS collected similar information to produce measures of net and gross assets until 2017. This allows us to present the time series in Figure 16. Owing to the redevelopment of the pensions surveys, there was no PFS estimate for 2018; Figure 16 includes the 2018 estimate produced for the UK National Accounts pension funds sub-sector (S.129).

Figure 16 shows that both net and gross assets have more than doubled in nominal terms since the 2008 to 2009 financial crisis. The gap between net and gross assets has also widened over the past decade. This is mainly because of rapid growth in UK pension schemes’ use of derivatives since 2003 (see Table 4.2 in the MQ5 Quarter 4 2018 dataset). At the end of 2019, derivatives accounted for 11% of gross assets including derivatives contracts with a positive (asset) value.

Figure 16: Net and gross assets have more than doubled since the 2008 to 2009 financial crisis

Net and gross assets of UK pension schemes, 1992 to 2019 (£ billion)

Source: Office for National Statistics – MQ5 pension fund survey to Quarter 1 2019, Financial Survey of Pension Schemes from Quarter 2 2019

Notes:

- Net assets excluding derivatives or “market value of pension funds” to 2017 can be found on the Office for National Statistics (ONS) website.

- Gross assets including derivatives contracts with a positive (asset) value can be found on the ONS website.

- The 2018 figure is from the UK National Accounts, published as an ad hoc request on 29 May 2020.

- Although respondents are asked to report the value of derivatives contracts gross, a small proportion reported net; this probably produces slight overestimates of positive balances and slight underestimates of negative balances.

Download this chart Figure 16: Net and gross assets have more than doubled since the 2008 to 2009 financial crisis

Image .csv .xlsAsset allocation

Table 19 shows results for the main categories of assets collected in the FSPS – pooled investment vehicles, direct investments and insurance policies – with breakdowns by whether the scheme was for public or private sector employees and DBH or DC. This information comes from spreadsheet 11: Assets in the FSPS questionnaire. A time series cannot be provided for these asset categories (even without the public versus private sector employee and DBH versus DC scheme breakdowns) because they are different from those in the previous survey. The FSPS definitions5 of these categories are:

- pooled investment vehicles are defined as funds in which there is more than one investor in the fund or underlying fund(s); they exclude any funds that are created for a single investor

- direct investments are all investment assets that the scheme holds directly rather than through a pooled investment vehicle; this includes assets that are held in a fund structure created for a single investor such as a Qualifying Investor Fund (QIF)

- insurance policies are annuity and deferred annuity contracts relating to buy-ins and longevity swaps; they are assets held with insurance companies enabling the Trustees of an occupational pension scheme to meet all or part of their pension liabilities

Between the end of September and the end of December 2019, the value of gross assets of private sector DC schemes rose by 6% to £146 billion6 (Table 3). In the same period, the value of gross assets of private sector DBH schemes fell by 3%. For public sector DBH schemes, there was almost no change.

At the end of 2019, over half (55%) of private sector employee DBH schemes’ investments were direct investments, while 39% were made via pooled investment vehicles and 6% were in the form of insurance policies. By contrast, 56% of public sector employee DBH schemes’ investments were made via pooled investment vehicles, 43% were direct investments and less than 1% were in the form of insurance policies. DC schemes invested almost entirely via pooled investment vehicles.

| 30 Sept 2019 | 31 Dec 2019 | |||||

|---|---|---|---|---|---|---|

| Private sector DBH | Private sector DC | Public sector DBH | Private sector DBH | Private sector DC | Public sector DBH | |

| Gross assets excluding derivatives | 1,927 | 138 | 404 | 1,859 | 146 | 404 |

| Of which: | ||||||

| Pooled investment vehicles | 743 | 134 | 224 | 730 | 142 | 228 |

| Direct investments | 1,088 | 4 | 178 | 1,022 | 4 | 174 |

| Insurance policies | 96 | 1 | 2 | 108 | - | 2 |

Download this table Table 3: DC schemes invest mainly via pooled vehicles, while over half of private sector DBH schemes’ investments at end-2019 were direct investments

.xls .csvDirect investments

It is possible to show direct investments of private and public sector employee schemes by asset class7. Table 4 shows these breakdowns at the end of September and the end of December 2019, while Figure 17 shows the asset classes as proportions of total direct investment at end-2019. Of total direct investment of private sector employee schemes (almost all of which was by DBH schemes), nearly 70% was in long-term debt securities (including structured products) at end-2019, while only 10% was in equities and 6% in unquoted private equity and alternatives. This probably reflects the “ageing” of private sector DBH schemes (see the Membership subsection), with bonds seen as a way of providing income for cashflow negative schemes and managing the interest rate risk associated with pension liabilities. Within long-term debt securities, the main types of investment were central government bonds including UK government Gilts (75%) and corporate bonds (21%).

The picture is completely different for public sector employee schemes. At the end of 2019, less than one-quarter of their direct investments were in long-term debt securities (including structured products). Equities accounted for 41% of the total and unquoted private equity and alternatives for 19%, suggesting more “growth-oriented” investment strategies. This difference in asset allocation reflects the differences in age profiles of public and private sector employee schemes (see the Membership subsection) as well as differences in the risk and regulatory environments of schemes where the government is the “pension manager”, compared with those that have private sector sponsors.

| 30 Sept 2019 | 31 Dec 2019 | |||

|---|---|---|---|---|

| Private sector | Public sector | Private sector | Public sector | |

| Direct investments | 1,092 | 178 | 1,026 | 174 |

| Of which: | ||||

| Cash and cash equivalents | 80 | 13 | 75 | 11 |

| Short-term debt securities | 11 | 1 | 12 | 3 |

| Long-term debt securities | 760 | 44 | 705 | 41 |

| Of which: | ||||

| Central Government bonds (including UK Government Gilts) | 568 | 29 | 529 | 26 |

| Corporate bonds | 164 | 13 | 150 | 12 |

| Equities | 109 | 70 | 107 | 71 |

| Property | 30 | 15 | 31 | 14 |

| Unquoted private equity and alternatives | 64 | 30 | 63 | 32 |

| Other investment balances (receivables) | 12 | 3 | 7 | 1 |

| Any other assets | 25 | 2 | 25 | 1 |

Download this table Table 4: Long-term debt securities dominate private sector employee schemes’ direct investments

.xls .csv

Figure 17: Public sector employee schemes’ direct investments focus on growth assets

Composition of direct investments of private and public sector employee schemes, UK, end-2019

Source: Office for National Statistics – Financial Survey of Pension Schemes

Notes:

- Direct investments are defined in Section 8: Glossary.

- Long-term debt securities includes structured products.

Download this chart Figure 17: Public sector employee schemes’ direct investments focus on growth assets

Image .csv .xlsPooled investment vehicles

The FSPS also collects a quarterly “look-through” of investments by UK pension schemes in pooled vehicles using spreadsheet 15: Pooled investment vehicles of the FSPS questionnaire. This has never been done before. Figures 18 to 20 present the results for public sector DBH, private sector DBH schemes and DC schemes:

- Of the pooled investments of public sector DBH schemes at end-2019, 58% was in equity, suggesting a similar growth orientation to that of their direct investments; fixed interest (debt securities) made up 19% the total, with property, hedge funds, private equity and money markets accounting for 10% between them.

- Nearly one-quarter of the pooled investments of private sector DBH schemes at end-2019 was invested in each of equity, fixed interest and mixed assets; property, hedge funds, private equity and money markets accounted for 14% between them.

- On the other hand, 36% of the investments held by DC schemes in pooled vehicles at end-2019 was in equity and 13% in fixed interest; mixed assets accounted for 28%, while property and money market funds each made up 3% of the total.

Figure 18: Over half of public sector DBH investments in pooled vehicles are in equity

Asset classes held in pooled vehicles by public sector DBH schemes, UK, end-2019

Source: Office for National Statistics – Financial Survey of Pension Schemes

Notes:

- Percentages are calculated excluding non-response.

- DBH = defined benefit and hybrid.

- “Other” includes commodity, energy and with profits funds.

Download this chart Figure 18: Over half of public sector DBH investments in pooled vehicles are in equity

Image .csv .xls

Figure 19: Private sector DBH investments via pooled vehicles take a balanced approach

Asset classes held in pooled vehicles by private sector DBH schemes, UK, end-2019

Source: Office for National Statistics – Financial Survey of Pension Schemes

Notes:

- Percentages are calculated excluding non-response.

- DBH = defined benefit and hybrid.

- “Other” includes commodity, energy and with profits funds.

Download this chart Figure 19: Private sector DBH investments via pooled vehicles take a balanced approach

Image .csv .xls

Figure 20: DC schemes focus on equity and mixed assets

Asset classes held in pooled vehicles by private sector DC schemes, UK, end-2019

Source: Office for National Statistics – Financial Survey of Pension Schemes

Notes:

- Percentages are calculated excluding non-response.

- DC = defined contribution.

- “Other” includes commodity, energy and with profits funds.

Download this chart Figure 20: DC schemes focus on equity and mixed assets

Image .csv .xlsThere are still some gaps in this analysis. For instance, the use of mixed asset class investments (a mixture of equity, fixed interest and other asset classes) delegates the investment decision to the fund manager and makes it hard to know what schemes are investing in. There is also significant reporting of other (or unknown) investments. However, we are now able to form a much clearer picture than before of the investments of UK funded occupational pension schemes, differentiating between private sector DBH, private sector DC and public sector DBH schemes. As UK pension provision changes and assets of DC schemes grow, the FSPS will track their investments and users of this information will be able to consider the implications for the UK economy.

Derivatives

Table 5 shows the derivatives balances presented in Table 2 with a breakdown for private sector employee schemes and public sector employee schemes. Public sector employee schemes accounted for 17% of gross assets excluding derivatives (Table 3), but they had a lower proportion of total derivatives balances (11%). This is because while many private sector employee DBH schemes use derivatives, particularly swaps, as part of Liability Driven Investment (LDI) strategies, use of LDI strategies (and swaps) is rare for public sector employee schemes.

| Private sector | Public sector | Total | |

|---|---|---|---|

| Derivatives contracts with a positive (asset) value | 271 | 32 | 303 |

| Derivatives contracts with a negative (liability) value | 260 | 31 | 291 |

Download this table Table 5: Private sector employee schemes held 89% of derivatives balances at end-2019

.xls .csvIt is not possible to present a breakdown for the private sector by whether the derivatives are used by DBH or DC schemes for confidentiality reasons, as few DC schemes use derivatives. Similarly, we cannot present a breakdown by type of derivative used and whether the schemes are for private or public sector employees because few public sector employee schemes use swaps. However, Figure 21 shows the breakdown by type of derivatives for all schemes. The main types are swaps and forward foreign currency contracts (56% and 43% of the value of derivatives contracts respectively); options and futures are hardly used by pension schemes.

Figure 21: Of the value of pension schemes’ derivatives contracts at end-2019, 56% was in swaps

Derivatives contracts by type of derivative, UK, end-2019

Source: Office for National Statistics – Financial Survey of Pension Schemes

Notes:

- Although respondents are asked to report the value of derivatives contracts gross, a small proportion reported net; this probably produces slight overestimates of positive balances and slight underestimates of negative balances.

Download this chart Figure 21: Of the value of pension schemes’ derivatives contracts at end-2019, 56% was in swaps

Image .csv .xlsLiabilities

The FSPS collects information on pension liabilities of DBH schemes and gross liabilities other than pension liabilities. Analysis of results for DBH pension liabilities showed significant data gaps and time lags. The ONS therefore expects to continue to estimate DBH pension liabilities using regulatory and administrative sources (publications by TPR and the Pension Protection Fund as well as scheme accounts for public sector employee schemes). However, for DC occupational pension schemes, pension liabilities are equal to the schemes’ assets and can be estimated using the FSPS.

Other (non-pension) gross liabilities of UK funded occupational pension schemes were estimated at £191 billion at end-2019 (Table 2). The breakdown of non-pension liabilities is shown in Figure 22. They consist mainly of repurchase agreements or “repos” (89% at end-2019). Schemes also had small amounts of cash and borrowing liabilities such as overdrafts (6%) and payables (3%).

Figure 22: Repos accounted for most of pension schemes’ non-pension liabilities at end-2019

Gross liabilities other than pension liabilities, excluding derivatives, UK, end-2019

Source: Office for National Statistics – Financial Survey of Pension Schemes

Download this chart Figure 22: Repos accounted for most of pension schemes’ non-pension liabilities at end-2019

Image .csv .xlsOverseas investments

Overseas investments are defined in the FSPS as those where there is a direct investment outside the UK, a financial instrument issued outside the UK or a fund registered outside the UK.

At the end of 2019, 27% of gross assets excluding derivatives of UK funded occupational pension schemes were reported as overseas. The proportion varied by type of investment: 29% of the value of investments in pooled investment vehicles related to overseas-registered vehicles, while for direct investments (shown in Figure 23) the proportions of overseas assets varied from equities (70%) to property and other assets (1%). There were also variations within these categories; for instance, although 16% of long-term debt securities including structured products are overseas, this ranged from 46% for corporate bonds to 6% for bonds issued by central governments (including UK Gilts).

Figure 23: 70% of schemes’ equity investments were issued overseas, while most bonds were issued in the UK

UK versus overseas breakdown of pension schemes’ direct investments, end-2019

Source: Office for National Statistics – Financial Survey of Pension Schemes

Notes:

- Long-term debt securities includes structured products.

- “Other” assets includes insurance policies.

Download this chart Figure 23: 70% of schemes’ equity investments were issued overseas, while most bonds were issued in the UK

Image .csv .xlsThe FSPS also collects data on overseas investments by country for selected investment categories. At the end of 2019, UK pension schemes held:

- short-term debt securities issued by 47 countries including securities issued in Ireland (62% of the total) and the United States (16%)

- long-term debt securities (including structured products) issued by 120 countries, with 51% issued in the United States, 5% in France and Ireland, and holdings of over £1 billion in the Netherlands, Germany, Panama, Luxembourg, Australia, Italy, Canada, Mexico, Spain, Jersey, Switzerland, Japan and the Cayman Islands

- equities issued by 86 countries, with 49% issued in the United States, 8% in Japan and investments of over £1 billion in France, Switzerland, Germany, Hong Kong, China, Canada, the Netherlands, South Korea, Taiwan, Spain, India, Australia, Sweden, Italy, Brazil and Ireland.

Further details are can be found in the accompanying datasets.

In addition, the survey asked for information on investments in pooled investment vehicles registered overseas by country of registration. Figure 24 shows the top 10 countries of registration by value of investment, which accounted for 88% of the total asset value at the end of 2019. Over half of UK pension funds’ investments in pooled investment vehicles that are registered overseas was in vehicles registered in Ireland, followed by Luxembourg (13%), the United States (11%) and the Cayman Islands (5%).

Figure 24: Ireland hosts 51% of pension schemes’ overseas investments via pooled vehicles

Proportion of total invested overseas via pooled vehicles by country where vehicle was registered, end-2019

Source: Office for National Statistics – Financial Survey of Pension Schemes

Notes:

- "Other" includes countries not specified and where data is disclosive.

Download this chart Figure 24: Ireland hosts 51% of pension schemes’ overseas investments via pooled vehicles

Image .csv .xlsAs the FSPS is a quarterly survey, it will be possible to monitor any changes in the patterns of overseas asset holdings by country as well as any changes in the balance between UK and overseas asset holdings. This information is required for the UK Balance of Payments (BoP). It should also be of interest to policymakers over the next few years, if the UK’s relationship with the EU and the rest of the world changes.

Notes for : FSPS results

We use the term “schemes for public sector employees” throughout the article. Strictly speaking, these are government-managed pension schemes (see Section 8: Glossary).

Contributions to DBH schemes did not rise over this period; see MQ5 Table 4.2 in the MQ5 2018 Q4 dataset.

The FSPS also asks for transfers out to be split according to whether they are individual or group transfers and whether the latter include buyouts. Unfortunately, these results can only be used for national accounts models, not for publication, because they do not pass our disclosure control (confidentiality) tests.

For further details, see Pensions in the national accounts, a fuller picture of the UK’s funded and unfunded pension obligations: 2010 to 2015.

Further details can be found in the survey questionnaire on the FSPS web page of the ONS website.

It should be noted that the FSPS results for DC schemes are not comparable with TPR’s DC Trust assets figure (£71 billion at end-2019), as the DC Trust asset figures exclude hybrid schemes with DC members and DC schemes with fewer than 12 members.

We cannot show private sector DC separately because a further breakdown of the £4 billion in direct investments of DC schemes (Quarters 3 and 4 2019) does not pass our disclosure control (confidentiality) tests.

7. Future work

The results presented in this article mark the end of two years’ work to redevelop the surveys of UK funded occupational pension schemes. The Financial Survey of Pension Schemes (FSPS) is now running smoothly. It is providing data to the UK National Accounts (with Quarter 2 (Apr to June), Quarter 3 (July to Sept) and Quarter 4 (Oct to Dec) 2019 already in the accounts), UK Balance of Payments (BoP) and international organisations.

However, the Office for National Statistics (ONS) pensions teams have not finished analysing all parts of the survey. We are still working on the following sections of the questionnaire:

- investment income and transactions (spreadsheets 5 and 14 of the questionnaire)

- UK Gilt holdings (spreadsheet 16)

- the investments of pooled investment vehicles (spreadsheet 15), including detailed analysis of the underlying funds in which pension schemes invest

The ONS suspended publication of the MQ5 Pension Funds Survey (PFS) results in 2019. We are considering whether to publish some of the information from the FSPS on a regular basis, resources permitting (option one), or whether to publish more articles like this one as more results are produced and to respond to specific data requests (option two). Please email us at pensions@ons.gov.uk if you prefer one of these options. We would also like to hear which of the data series presented in Section 6: FSPS results are most useful to you.

Back to table of contents8. Glossary

Accrual

Accrual is the build-up of a scheme members’ pension benefits or entitlements.

Active members

Members of pension schemes who are current employees and are either contributing to the scheme themselves or having contributions made on their behalf (for instance, by their employer) are referred to as active members.

Auto-enrolment or automatic enrolment

Under reforms brought in by the Pensions Acts 2008 and 2011, employers must enrol all eligible employees into a qualifying private pension. Workers can opt out but will be re-enrolled every three years. Auto-enrolment was rolled out to employers in stages between 2012 and 2018. Minimum contribution rates were established and were also introduced in stages:

- before 6 April 2018: total contributions (employer plus employee, including tax relief) were 2% of qualifying earnings (the minimum band of earnings on which pension contributions must be made), of which employer contributions 1%

- from 6 April 2018 to 5 April 2019: total contributions were 5% of qualifying earnings, of which employer contributions 2%

- from 6 April 2019 to date: total contributions were 8% of qualifying earnings, of which employer contributions 3%

Bond

A bond is a negotiable loan instrument sold by firms (known as corporate bonds) and the government (known as UK Gilts in the case of UK government bonds), generally with a fixed term to maturity, that pays the holder the face value (or “principal”) upon redemption, together with coupon payments paid semi-annually (sometimes annually) during the term to maturity. A bond that makes no coupon payments is known as a zero-coupon bond.

Buy-in

A buy-in is an arrangement whereby the pension scheme Trustees “buy in” an insurance policy to cover all or part of their pension liabilities. By contrast with a buyout, the members covered by a buy-in remain in the scheme and the scheme continues to be responsible for paying their pensions. The insurance policy is held as an asset by the scheme to cover its liabilities in respect of these pensions.

Buyout

A buyout is an agreement between an occupational pension scheme and an insurance company where all or part of the scheme’s membership, together with the scheme’s liability to pay the members’ pension entitlements and related assets, are transferred to an insurance company. The Financial Survey of Pension Schemes (FSPS) asks that buyouts (but not buy-ins) be recorded as part of group or bulk transfers out of the scheme.

Cash equivalent transfer values (CETVs)

Cash equivalent transfer values (CETVs) are the cash values of members’ pension benefits, which in the case of DB schemes are the result of an actuarial calculation of the members’ accrued-to-date entitlements in the pension schemes.

Cashflow negative schemes

Cashflow negative schemes are schemes where benefits paid out exceed contributions and other income received.

Deferred members

Deferred members are members of pension schemes who have accrued rights to pensions that will come into payment in the future but who are no longer actively contributing (or having contributions paid on his or her behalf) into the scheme. Also known as members with preserved pension entitlements.

Defined benefit (DB)

A defined benefit (DB) pension is one in which the rules of the scheme specify the rate of benefits to be paid. The most common DB scheme is a final salary scheme in which the benefits are based on the number of years of pensionable service, the accrual rate and the final salary. An alternative to the final salary scheme is the Career Average Revalued Earnings (CARE) scheme, which is also a DB scheme.

Defined contribution (DC)

A defined contribution (DC) pension is one in which the benefits are determined by the contributions paid, the investment return on those contributions (less charges) and the type of annuity purchased upon retirement, if any. It is also known as a money purchase pension.

Direct investments

Direct investments are investment assets that the scheme holds directly rather than though a pooled investment vehicle. These include assets that are held in a fund structure created for a single investor such as a Qualifying Investor Fund (QIF).

Drawdown

Drawdown is where an individual does not buy an annuity with their pension pot at retirement but instead draws an income.

Equity

Equity is a share or any other security representing an ownership interest, typically in a company.

Funded scheme

A funded scheme is one in which benefits are met from a fund built up in advance from contributions and investment income. Such schemes have assets, even if these are not sufficient to meet all their liabilities, by contrast with unfunded schemes, in which liabilities are not underpinned by assets.

Government-managed pension schemes

Government-managed pension schemes are schemes classified as having the “pension manager” in the government sector (S.13) of the national accounts. In such cases, the government sector (central and local government) is judged to be ultimately responsible for the schemes’ pension obligations (the “pension manager”) even if the government sector is not responsible for scheme administration (the “pension administrator”).

Household saving ratio

The household saving ratio is the proportion of total household resources – the sum of all households’ gross disposable income plus the change in their pension entitlements during the period – that is left once the household’s consumption expenditure has been deducted.

Hybrid scheme

A hybrid scheme is an occupational pension scheme where members have either a choice, or mixture, of DB and DC pension entitlements. In a “pure” hybrid arrangement, members receive benefits that are a mixture of DB and DC. In a “mixed hybrid” scheme, there are separate DB and DC groups of members (often organised in separate sections of the scheme).

Insurance policies

In the FSPS, insurance policies mean annuity and deferred annuity contracts relating to buy-ins and longevity swaps. They are policies held with insurance companies and are recorded as assets of the scheme, enabling its Trustees to cover all or part of the scheme’s pension liabilities.

Liability Driven Investment (LDI)

A Liability Driven Investment (LDI) is an approach to investing pension scheme assets that is designed to match the scheme’s pension liabilities, including managing uncertainty relating to interest rate and inflation risk.

Master Trusts

A Master Trust is where a product provider manages a pension scheme for a number of employers under a single trust arrangement.

Non-government-managed pension schemes

Non-government-managed pension schemes are schemes where the “pension manager” (the body ultimately responsible for the schemes’ pension obligations) is judged to be in a national accounts sector other than the government sector. These are referred to in this article as schemes for private sector employees.

Occupational pension schemes

An occupational pension scheme is an arrangement (other than accident or permanent health insurance) organised by an employer (or on behalf of a group of employers) to provide benefits for employees on their retirement and for their dependants on their death. They are a form of workplace pension. Occupational pension schemes for private sector employees are also referred to as trust-based schemes.

Pensioner members

Pensioner members are members of pension schemes who are receiving pensions or income withdrawals, sometimes known as beneficiaries.

Pooled investment vehicles

Pooled investment vehicles are funds in which there is more than one investor in the fund or underlying fund(s).

Recognised overseas pension schemes (ROPS)

A recognised overseas pension scheme (ROPS) is one of the schemes on the list of overseas pension schemes recognised by HM Revenue and Customs (HMRC). A qualifying ROPS, or “QROPS”, is a ROPS that HMRC recognises as eligible to receive transfers from registered pension schemes in the UK.

Salary sacrifice

Salary sacrifice occurs when an employee gives up part of the cash pay due under their contract of employment in return for some other form of benefit. For example, an employee may forgo an increase in salary in return for an equal increase in employer contributions towards their pension. Sacrifices of this type have tax and National Insurance incentives for employees and National Insurance incentives for employers.

Sampling frame

A sampling frame is a list of units comprising the population from which a sample is drawn.