Table of contents

- Main points

- Things you need to know about this release

- Oil and gas asset accounts

- Fuel use, energy consumption and greenhouse gas emissions

- Material flow accounts

- Environmental taxes

- Environmental goods and service sector

- Environmental protection expenditure

- Links to other related statistics

- What’s changed in this release?

- Quality and methodology

1. Main points

The continued switch from coal to natural gas by the energy supply and manufacturing sectors resulted in a fall in overall greenhouse gas (GHG) emissions in 2016, the continuation of a long-term trend.

In 2016, households were the biggest emitter of GHGs, accounting for one-quarter of total UK GHG emissions.

In 2016, the UK consumed 570 million tonnes of material, still below pre-2008 levels.

Almost three-quarters of environmental tax revenue in 2017 was related to energy taxes, the majority of which were taxes on transport fuels.

The environmental goods and services sector (EGSS) contributed an estimated £30.5 billion to the UK economy in terms of value added in 2015 (1.6% of gross domestic product (GDP)).

In 2016, UK government spent an estimated £14.4 billion on environmental protection (EPE), accounting for 1.8% of UK government expenditure, a similar proportion to in recent years.

2. Things you need to know about this release

The UK Environmental Accounts show how the environment contributes to the economy (for example, through the extraction of raw materials), the impact that the economy has on the environment (for example, energy consumption and air emissions) and how society responds to environmental issues (for example, through taxation and expenditure on environmental protection).

The UK Environmental Accounts are “satellite accounts” to the main UK National Accounts and they are compiled in accordance with the System of Environmental Economic Accounting (SEEA), which closely follows the UN System of National Accounts (SNA). This means they are comparable with economic indicators such as gross domestic product (GDP).

The UK Environmental Accounts are based on a UK residency basis (as opposed to a territory basis). This means that data relating to UK residents and UK-registered businesses are included, regardless of whether they are in the UK or overseas. Data relating to foreign visitors and foreign businesses in the UK are excluded.

Full definitions for terms can be found within Section 11: Quality and methodology section.

Back to table of contents3. Oil and gas asset accounts

Main points

At the end of 2016, the expected level of discovered oil reserves was estimated to be 515 million tonnes (mt), 9% lower than in 2015.

Expected reserves of discovered gas at the end of 2016 were estimated to be 297 billion cubic metres (bcm), 11% lower than in 2015.

Things you need to know about this section

This section presents non-monetary estimates of the oil and gas reserves and resources in the UK. In the context of oil and gas reserves and resources presented in this section, reserves refer to discovered oil and gas reserves, which are recoverable and commercially viable, whereas resources refers to oil and gas that are potentially valuable and for which reasonable prospects exist for eventual extraction.

From 2015, the Oil and Gas Authority have developed a new category of oil and gas reserves, known as contingent resources. Contingent resources are defined as “significant discoveries where development plans are under discussion”. In the past, these would have been included as “probable reserves”. The apparent loss in discovered reserves is due largely to this change in classification.

Other changes in oil and gas reserves are a result of:

changes in production during the year

new field developments including those from recent exploration success

revisions to established fields

Table 1: Definitions of oil and gas reserves

| Deposit Type | Definition |

|---|---|

| Discovered - Proven reserve | Virtually certain to be technically and commercially producible i.e. have a better than 90% chance of being produced |

| Discovered - Probable reserve | Not yet proven, but have a more than 50% chance of being produced |

| Contingent resources | Significant discoveries where development plans are under discussion |

| Possible | Cannot be regarded as probable, but which are estimated to have a significant – but less than 50% – chance of being technically and commercially producible |

| Potential additional resources (PAR’s) | Not currently technically or commercially producible |

| Undiscovered | Provide a broad indication of the level of oil resources which are expected to exist. However, they are subject to higher levels of uncertainty than reserves and PAR’s |

| Source: Office for National Statistics | |

Download this table Table 1: Definitions of oil and gas reserves

.xls (37.4 kB)Oil reserves and resources

Oil is defined as both oil and the liquids that can be obtained from gas fields. Shale oil is not included in these estimates.

Discovered oil reserves

The expected level of discovered oil reserves is the sum of proven and probable reserves. In 2016, this was estimated at 515 million tonnes, 9% lower than in 2015, which was 566 million tonnes.

Figure 1: Estimates of discovered and undiscovered oil reserves, 1995 to 2016

UK

Source: Department for Business, Energy and Industrial Strategy (BEIS) and Oil and Gas Authority

Notes:

- All data refer to end of year.

- Components may not sum to totals due to rounding.

- Discovered reserves are the sum of proven plus probable reserves.

- Maximum reserves for 2015 and 2016 include central estimates for contingent resources.

Download this chart Figure 1: Estimates of discovered and undiscovered oil reserves, 1995 to 2016

Image .csv .xlsGas reserves and resources

Gas estimates include gas expected to be available for sale from dry gas fields, gas condensate fields, oil fields with associated gas and a small amount from coal bed methane projects. Shale gas is not included in these estimates. These reserves include onshore and offshore discoveries but not flared gas or gas consumed in production operations.

Discovered gas reserves

The expected level of gas reserves (proven plus probable) in 2016 was estimated to be 297 billion cubic metres (bcm), 11% lower than in 2015. The fall in expected reserves was driven primarily by a fall in proven reserves. In 2016 the probable reserves were largely unchanged from 2015.

Figure 2: Estimates of discovered and undiscovered gas reserves, 1995 to 2016

UK

Source: Department for Business, Energy and Industrial Strategy (BEIS) and Oil and Gas Authority

Notes:

- All data refer to end of year.

- Components may not sum to totals due to rounding.

- Discovered reserves are the sum of proven plus probable reserves.

- Maximum reserves for 2015 and 2016 include central estimates for contingent resources.

Download this chart Figure 2: Estimates of discovered and undiscovered gas reserves, 1995 to 2016

Image .csv .xlsMore detail can be found in the Oil and gas dataset.

Back to table of contents4. Fuel use, energy consumption and greenhouse gas emissions

Main points

The continued switch from coal to natural gas by the energy supply and manufacturing sectors resulted in a fall in overall greenhouse gas (GHG) emissions in 2016, the continuation of a long-term trend.

Energy consumption and GHG emissions for the transport sector have increased each year between 2013 and 2016, after decreasing continuously between 2005 and 2013.

In 2016, households were the biggest emitter of GHGs, accounting for one-quarter of total UK GHG emissions.

Things you need to know about this section

The UK Environmental Accounts are based on a UK residency basis (as opposed to a territory basis):

fuel use and energy consumed by UK residents and UK-registered businesses is included, regardless of whether they are in the UK or overseas; the fuel used and energy consumed by foreign visitors and foreign businesses in the UK is excluded

emissions that UK residents and UK-registered businesses are directly responsible for, whether in the UK or overseas, are included; emissions from foreign visitors and businesses in the UK are excluded

This is in line with national accounting principles, allowing environmental impacts to be compared on a consistent basis with economic indicators such as gross domestic product (GDP).

UK figures for energy and air emissions on a territory basis are published by the Department for Business, Energy and Industrial Strategy (BEIS) and the Department for Environment, Food and Rural Affairs (Defra). The energy and emissions bridging tables illustrate the difference between these estimates. Further explanation of the differences can be found in the following articles on energy consumption and alternative approaches to reporting UK greenhouse gas emissions.

This section includes analysis by Standard Industry Classification 2007: SIC 2007. To simplify, within the text:

households include “consumer expenditure” and “activities of households as employers; undifferentiated goods and services – producing activities of households for own use” (for example, employing a cleaner and growing vegetables for your own consumption)

the electricity, gas, steam and air conditioning supply sector is referred to as the energy supply sector

the transport and storage sector is referred to as the transport sector

The switch away from coal has reduced fuel use, energy consumption and greenhouse gas emissions

Fuel use1, energy consumption and greenhouse gas emissions all fell between 2015 and 2016, the continuation of a long-term trend. Figure 3 shows these values as an index to allow comparison. Average temperature is also included, as short-term fluctuations tend to be explained by variations in temperature.

There was a 3% reduction in fuel use between 2015 and 2016, bringing fuel use to 170 million tonnes of oil equivalent, around one-fifth less than in 1990. Energy consumption also fell, by just over 1%, to 202 million tonnes of oil equivalent. These reductions in fuel use and energy consumption are reflected in GHG emissions, which were down just under 4% between 2015 and 2016, to 576.3 million tonnes of carbon dioxide equivalent. This was almost one-third below 1990 levels.

Figure 3: Fuel use, energy consumption, greenhouse gas emissions and average temperature, 1990 to 2016

UK

Source: Ricardo Energy and Environment, Met Office, Office of National Statistics

Notes:

- Fuel use does not include renewable or nuclear fuel use but does include fuel for non-energy purposes.

- Total figures are based on raw data and therefore may not sum due to rounding.

Download this chart Figure 3: Fuel use, energy consumption, greenhouse gas emissions and average temperature, 1990 to 2016

Image .csv .xlsThese reductions were driven largely by a switch from the use of coal and heavy polluting fuels by the manufacturing and energy supply sectors to other, more efficient, fuels. Between 2015 and 2016 coal use by the energy supply sector fell 59%, to almost 85% below 1990 levels. The move towards natural gas for electricity generation, shown in Figure 4, is likely to have contributed to an overall improvement in energy efficiency of electricity generation, thereby resulting in lower overall energy consumption.

Energy consumption has not fallen at the same rate as fuel use and GHG emissions in part because of the increasing consumption of energy from renewables and other non-fossil fuel sources. Data on energy from renewables and waste can be found in the Energy consumption from renewables and waste dataset.

A similar story emerges for the manufacturing sector, where there has been a 74% reduction in coal use and a 96% reduction in fuel oil combustion since 1990. This has helped reduce overall reallocated energy consumption (where losses incurred during transformation2 and distribution3 are allocated to the final consumer) of the manufacturing sector fall to 40 million tonnes of oil equivalent, 38% below 1990 levels.. More recent reductions in the manufacturing sector have been a result of reduced activity in iron and steel and associated industries.

Figure 4: Fuel use by energy supply sector, 1990, 2005, 2015 and 2016

UK

Source: Ricardo Energy and Environment, Office for National Statistics

Notes:

- The energy supply sector refers to the electricity, gas, steam and air conditioning supply sector

- Includes anthracite, blast furnace gas, burning oil, coke, coke oven gas, colliery methane, liquid petroleum gas, lubricants, naphtha, other petroleum gas, orimulsion, peat, petroleum coke, refinery miscellaneous, sour gas, secondary solid fuels, waste oils and waste solvent.

- Total figures are based on raw data and therefore may not sum due to rounding.

Download this chart Figure 4: Fuel use by energy supply sector, 1990, 2005, 2015 and 2016

Image .csv .xls

Figure 5: Fuel use by the manufacturing sector, 1990, 2005, 2015 and 2016

UK

Source: Ricardo Energy and Environment, Office for National Statistics

Notes:

- Includes marine diesel oil; excludes diesel oil for road vehicles (DERV).

- Includes anthracite, blast furnace gas, burning oil, coke, coke oven gas, colliery methane, liquid petroleum gas, lubricants, naphtha, other petroleum gas, orimulsion, peat, petroleum coke, refinery miscellaneous, sour gas, secondary solid fuels, waste oils and waste solvent.

- Total figures are based on raw data and therefore may not sum due to rounding.

Download this chart Figure 5: Fuel use by the manufacturing sector, 1990, 2005, 2015 and 2016

Image .csv .xlsA switch from these heavy polluting fuels has resulted in a reduction in GHG emissions for these sectors, and for total GHG emissions (Figure 6). GHG emissions are widely believed to contribute to global warming and climate change. When used for electricity generation, coal produces more CO2 than natural gas per unit of electricity produced, so the switch away from coal to natural gas use in power stations has led to a reduction in CO2 emissions. As CO2 is the most dominant greenhouse gas, changes in CO2 tend to be reflected in overall GHG emissions.

Emissions by the transport sector have been increasing since 2013

Unlike the energy supply and manufacturing sectors, the transport sector has not seen the same reduction in energy consumption or GHG emissions. The “transport sector” refers to the industry classification, not all transport by UK residents and businesses.

For the transport sector, there was a steady increase in energy consumption between 1990 to its peak in 2005. This was due to an increase in fuel oil used in shipping and aviation fuel. In the UK Environmental Accounts, emissions from international aviation and shipping relating to UK operators are included. However, these are excluded from the data compiled for United Nations Framework Convention on Climate Change (UNFCCC) purposes.

Between 2005 and 2013, energy consumption by the transport sector reduced by 20%, due largely to a reduction in the use of fuel oil and fuel used in diesel-engine road vehicles (DERV). However, this trend has reversed since 2013, with increases in the use of DERV and gas oil contributing to an overall increase in energy consumption by the transport sector to 29.6 million tonnes of oil equivalent in 2016, a 7% rise on 2013. Data relating to fuel use and energy consumption can be found in the reference tables Fuel use by industry and type and Energy: total consumption dataset.

These changes in energy consumption are reflected in GHG emissions by the transport sector (Figure 6). In 2005, GHG emissions by the transport sector peaked at 100 million tonnes of carbon dioxide equivalent (Mt CO2e), 52% above 1990 levels. Between 2005 and 2013, emissions for this sector declined, before starting to increase again. Between 2013 and 2016, GHG emissions by the transport sector have increased each year, and in 2016 were 86 million tonnes of carbon dioxide equivalent. While this is 14% below 2005 levels, it is still almost one-third higher than GHG emissions by the transport sector in 1990.

Households the biggest emitters of GHGs since 2015

The level of energy consumption and GHG emissions by households has remained relatively stable since 1990, with fluctuations tending to be explained by temperature, as households use more or less fuel depending on the weather. In 2015, households overtook the energy supply sector as the largest emitters of GHGs. Households were responsible for one-quarter of all GHG emissions in the UK in 2016.

Around 40% of fuel used by households in 2016 relates to travel, such as domestic car travel and flights. The increasing number of cars, the majority of which are registered to households, may help explain why energy consumption and GHG emissions by households have not been falling. While the number of alternative fuel vehicles has been increasing in the UK, there were still only 388,000 licensed by December 2016. Further information on fuel use by households can be found in last year’s Environmental Accounts bulletin and the Fuel use by industry and type dataset.

Greenhouse gas emissions from road transport by all sectors have been increasing since 2013 and in 2016 accounted for around one-fifth of total greenhouse gas emissions. Emissions from the majority of other pollutants from road transport have been falling, due largely to more stringent emissions standards. More detail can be found in the Atmospheric emissions: road transport emissions dataset.

Figure 6: Greenhouse gas emissions for the four most emitting sectors, 1990 to 2016

UK

Source: Ricardo Energy and Environment, Office for National Statistics

Notes:

- Industry aggregations are based on the UK Standard Industrial Classification (SIC) 2007.

- The household category includes consumer and activities of households as employers, undifferentiated goods and services-producing activities of households for own use.

Download this chart Figure 6: Greenhouse gas emissions for the four most emitting sectors, 1990 to 2016

Image .csv .xlsTransport sector remained the most energy intensive sector despite becoming more energy efficient

This switch towards more efficient methods or fuels can be seen in the energy intensity figures. Energy intensity, energy use (reallocated) per gross value added (GVA), fell 3% between 2015 and 2016, to 3.1 terajoules per £ million of value added. This was a continuation of a general downward trend since first figures were available in 1997.

The manufacturing and transport sectors, traditionally two of the most energy-intensive sectors, have seen declines in energy intensity between 1997 and 2016. For the transport sector, this reflects the improvement in the efficiency of vehicles. However, despite improvement, the transport sector still remained the most energy intensive industry. While the manufacturing industry has become more energy-efficient, it’s decreasing importance in the economy as a whole has contributed to the reduction in overall energy intensity. Manufacturing is traditionally an energy intensive industry and the UK has moved towards a more service-based economy.

For the last few years, the energy supply sector has seen an increase in energy intensity (Figure 7). Over the longer-term, energy intensity for the energy supply sector has been relatively stable. This would indicate that this sector has not seen the same improvements in energy efficiency as the manufacturing and transport industries since 1997. This is most likely because the energy supply sector was already relatively energy efficient in 1997, so had limited scope for improvement when compared with the manufacturing and transport sectors.

Figure 7: Energy intensity for main sectors, 1997 to 2016

UK

Source: Ricardo Energy and Environment, Office for National Statistics

Notes:

- Industry aggregations are based on the UK Standard Industrial Classification (SIC) 2007. Not all industries (SICs) have been included.

- Energy intensity is calculated by dividing reallocated energy consumption by gross value added (GVA) in constant prices. This is the difference between output and intermediate consumption for any given industry/sector. This means the difference between the value of goods and services produced (output) and the cost of raw materials and other inputs which are used up in production (intermediate consumption).

- Data are in constant prices with 2013 defined as the base year.

Download this chart Figure 7: Energy intensity for main sectors, 1997 to 2016

Image .csv .xlsGreenhouse gas (GHG) emissions intensity continued to fall

Greenhouse gas (GHG) emissions intensity, the level of emissions per unit of economic output (constant price level) fell 7% between 2015 and 2016, below half that of the 1997 levels. It has declined from 0.54 thousand tonnes of carbon dioxide equivalent (CO2e) per £ million value added in 1997 to 0.25 thousand tonnes of CO2e per £ million value added in 2015. This change was due largely to the reductions in GHG intensity by the energy and water supply4 sectors.

Greenhouse gas emissions intensity for the whole economy (total) is much lower than for the manufacturing and energy sectors. This reflects the fact that the sectors that contribute the most to the UK economy tend to have low levels of GHG emissions intensity.

Figure 8: Greenhouse gas intensity for main sectors, 1997 to 2016

UK

Source: Ricardo Energy and Environment, Office for National Statistics

Notes:

- Industry aggregations are based on the UK Standard Industrial Classification (SIC) 2007. Not all industries (SICs) have been included.

- Greenhouse gas emissions intensity is calculated by dividing the level of greenhouse gas emissions by gross value added (GVA) in constant prices. This is the difference between output and intermediate consumption for any given industry/sector. This means the difference between the value of goods and services produced (output) and the cost of raw materials and other inputs which are used up in production (intermediate consumption).

- Data are in constant prices with 2015 defined as the base year.

- All emissions intensity figures exclude consumer expenditure. Industry level greenhouse gas emissions intensity calculations cannot be summed to reach total greenhouse gas intensity because it is calculated as a ratio.

Download this chart Figure 8: Greenhouse gas intensity for main sectors, 1997 to 2016

Image .csv .xlsNotes for: Fuel use, energy consumption and greenhouse gas emissions

Fuels from renewable sources are not covered under fuel use as defined here.

Transformation losses are the differences between the energy content of the input and output product arising from the transformation of one energy product to another.

Distribution losses are losses of energy product during transmission (for example, losses of electricity in the grid) between the supplier and the user of the energy.

Water supply refers to the water supply; sewerage, waste management and remediation activities industry.

5. Material flow accounts

Main points

In 2016, the UK consumed 570 million tonnes of material.

Material consumption fell in 2008 and 2009 at the beginning of the economic downturn and has not returned to pre-2008 levels.

The UK has a positive physical trade balance, meaning that more materials and products are imported than are exported.

Things you need to know about this section

Data on levels of extraction of minerals were not available for 2015 and 2016, so estimates for these have been used in the calculations of the material flow accounts. In addition, estimates of some minor minerals were not available in 2016. This may result in an underestimate of the total domestic extraction, although the impact is likely to be minor (these were worth less than 0.5% of total domestic extraction in 2015).

It is important to note that there are a number of limitations to the domestic material consumption (DMC) indicator, most notably that it does not take the weight of raw materials (RME) used to produce imported and exported products into account.

What are material flow accounts?

Material flow accounts estimate the physical flow of materials through our economy. This includes the amount of raw materials extracted within the UK (domestic extraction) and the import and export of materials. This information is used to calculate indicators showing the quantity of materials that are available for use and that are consumed within the economy. It also helps to understand resource productivity. For example, they shed light on the depletion of natural resources and seek to promote a sustainable and more resource-efficient economy.

Domestic extraction fallen 35% since 1992

Domestic extraction in 2016 was 447 million tonnes, a slight fall on 2015 levels and 35% below domestic extraction in 1992. Domestic extraction is divided into four categories: biomass, non-metallic minerals, fossil energy materials and carriers, and metal ores1. In 2016, half of all domestic extraction was of non-metallic minerals. These are mainly construction and industrial minerals, including limestone and gypsum, sand and gravel, and clays. The remainder was split between biomass (29%) and fossil energy materials and carriers (20%) (this includes coal, peat2, crude oil and natural gas). The main decline in extraction has been driven by reductions in the amount of non-metallic minerals and fossil energy materials that have been extracted. Biomass extraction has remained relatively stable. While there has been a decline in the extraction in metal ores to practically zero, metal ores have only ever accounted for a small proportion of all domestic extraction.

The UK imports more material than it exports

The physical trade balance (PTB) shows the relationship between imports and exports and is calculated by subtracting the weight of exports from the weight of imports3. The UK has a positive PTB, meaning that more materials and products are imported than are exported.

Imports and exports data are available from 2000 when the PTB was relatively small at 21 million tonnes. PTB generally increased between 2000 and 2013, except between 2007 and 2010 when there was a fall following the economic downturn. However, the PTB decreased year-on-year between 2013 and 2016, with a 6% drop in 2016 from 2015 (to 123 million tonnes). This has been driven largely by a reduction in imports.

A partial explanation for the fall in overall imports of materials is the reduction in the amount of coal imported. Figure 9 shows the imports of coal and natural gas between 2000 and 2016. Between 2006, when coal imports reached their highest amount since 2000, and 2010 coal imports more than halved, from 50 million tonnes to 24 million tonnes. From 2010 until 2013, coal and natural gas imports both increased. Coal imports then fell sharply by 82% to 8 million tonnes in 2016. This is likely related to a simultaneous price rise for natural gas and lowering of price for coal4.

Figure 9: Coal and natural gas imports, 2000 to 2016

UK

Source: HM Revenue and Customs

Download this chart Figure 9: Coal and natural gas imports, 2000 to 2016

Image .csv .xlsDespite this fall in imports, the amount of materials and products that were imported (281 million tonnes) was almost twice the amount of materials and products that were exported (158 million tonnes) in 2016, suggesting that the UK is reliant on the production of materials in other countries.

Material consumption remains lower than pre-2008 levels

Direct material input (DMI) (domestic extraction plus imports) measures the total amount of materials that are available for use in the economy.

Domestic material consumption (DMC) (domestic extraction plus imports minus exports) measures the amount of materials used in the economy, and is calculated by subtracting exports from DMI.

In 2016, the UK consumed 570 million tonnes of material. Non-metallic minerals accounted for 42% of this, followed by biomass (30%), fossil fuels (26%) and 12 million tonnes of metal ores (2%). Material consumption (DMC) was relatively stable between 2000 and 2007, then fell sharply in 2008 and 2009 at the beginning of the economic downturn. This was largely driven by falls in the consumption of fossil fuels and non-metallic minerals, the latter of which are associated with construction. Material consumption has become relatively steady again since then, but has not returned to pre-2008 levels.

While there has been an increase in the consumption of non-metallic minerals since 2013, this has been offset by the continued decline in the consumption of fossil fuels (Figure 10).

Figure 10: Domestic material consumption, 2000 to 2016

UK

Source: Office for National Statistics

Notes:

Imports and exports have been allocated to categories within domestic material consumption using the same method that is used by Eurostat.

Total material input and consumption for 2016 may be slight underestimates due to small missing data sources on extraction for some minor materials.

Download this chart Figure 10: Domestic material consumption, 2000 to 2016

Image .csv .xlsThe same pattern can be seen when considering estimates of DMC and DMI on a per person basis. This indicates that changes in the figures above are not being driven by changes in the population. Figures on DMC and DMI can be found in the Material Flow Accounts dataset.

Notes for: Material flow accounts

Full definitions of these can be found in Section 11: Quality and methodology.

For fossil energy materials and carriers (which include coal, crude oil, natural gas and peat) peat estimates were not available for 2016.

The physical trade balance (imports minus exports) is defined in reverse to the monetary trade balance (exports minus imports). Physical estimates can differ quite significantly from monetary estimates.

6. Environmental taxes

Main points

Revenue from environmental taxes in the UK has remained relatively stable over the last 20 years when considered as a percentage of gross domestic product (GDP) and was 2.4% of GDP in 2017, raising £48.9 billion in tax revenue.

Almost three-quarters of environmental tax revenue in 2017 was related to energy taxes, the majority of which were taxes on transport fuels.

Households account for around half of revenue from environmental taxes and UK households paid an average £693 in environmental taxes in 2015.

Things you need to know about this section

Environmental taxes are designed to promote environmentally positive behaviour, reduce damaging effects on the environment and generate revenue that can potentially be used to promote further environmental protection.

Data on total UK environmental tax revenue are available for the years 1997 through to 2017. All data are reported at current prices so no adjustments have been made to account for the effects of inflation.

Environmental taxes revenue data broken down by economic activity are available to 2015 only. NACE1 is the European classification system for economic activity, categories are comparable with the Standard Industrial Classifications (SICs) reported elsewhere in this release.

UK environmental tax revenue increased from 1997 to 2017 but remains broadly stable as a percentage of GDP

In 2017, revenue from environmentally-related taxes stood at £48.9 billion, equivalent to 2.4% of the UK’s gross domestic product (GDP).

UK government revenue from environmentally-related taxes has increased by, on average, 3.6% per year since 19972. Total revenue in 2017 (£48.9 billion) was more than double the revenue collected in 1997 (£24.3 billion). This increase is due largely to increases in revenue from hydrocarbon oils, which include taxes on transport fuels. There was a jump in revenue between 1997 and 1998 when the fuel escalator increased from 5% to 6%. Air Passenger Duty also doubled at this time, to £10 for flights to Europe and £20 for flights to the rest of the world.

The drop in revenue in 2001 was likely due to changes to taxes relating to road transport. Following national protests, fuel tax for road vehicles was reduced, resulting in a £1.0 billion fall in revenue. During the same year there was also a change from taxing based on engine size to fuel type and carbon dioxide emissions, further reducing tax revenue. This change in policy is reflected in statistics on fuel use (see Section 4: Fuel use, energy consumption and greenhouse gas emissions), which show a switch from petrol to DERV (fuel used in diesel-engine road vehicles). Fuel tax for road vehicles has been frozen since 2010. The UK government is currently developing policy aimed at reducing emissions from road vehicles as part of the clean growth strategy.

The general increase in revenue from 1997 to 2017 reflects changes in the wider economy as well as being impacted by specific policy changes such as those outlined previously. Between 1997 and 2017, environmental taxes as a share of GDP have remained at a broadly consistent level of between 2.0% and 3.0% (Figure 11).

Another way of examining the nature of environmental taxes is to look at the contribution of environmental tax revenue to all tax revenue. This is useful as it provides some indication of the relative importance of environmental taxes to the overall taxation system.

In 2017, environmental tax revenue represented 7.1% of all taxes and social contributions (TSC) revenue in the UK. After peaking at 8.6% of TSC in 1998, following growing concern and political commitment (for example, the signing of the Kyoto protocol) regarding averting climate change in the early 1990s, environmental taxes as a percentage of TSC then generally fell to reach 6.6% in 2006. In 2009, as a possible result of a fall in other government tax revenue following the economic downturn, the share of TSC comprised of environmental taxes rose to 7.5% then remained relatively constant before declining slightly from 7.5% in 2014 to 7.1% in 2017 (Figure 11).

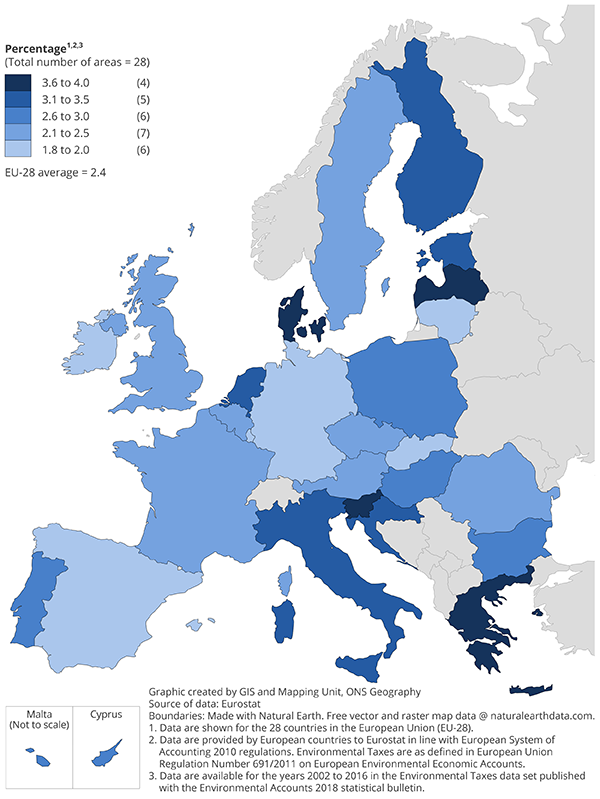

Data demonstrating how the UK compares with other European Union (EU28) countries are available up to 2016. Environmental tax revenue was equivalent to 2.4% of UK GDP in 2016, similar to the EU28 average of 2.4%. Across the EU28 in 2016, environmental tax revenue as a proportion of GDP was highest in Denmark (4.0%) and lowest in Luxembourg (1.8%) (Figure 12).

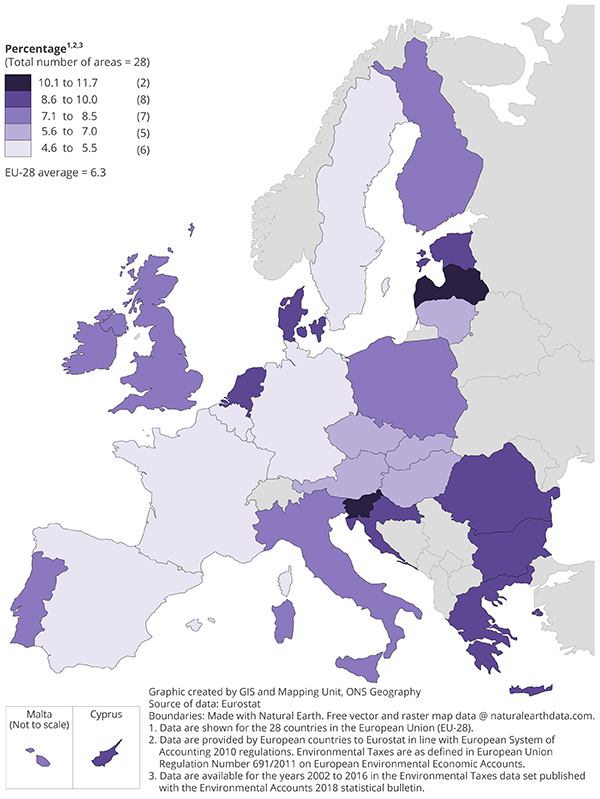

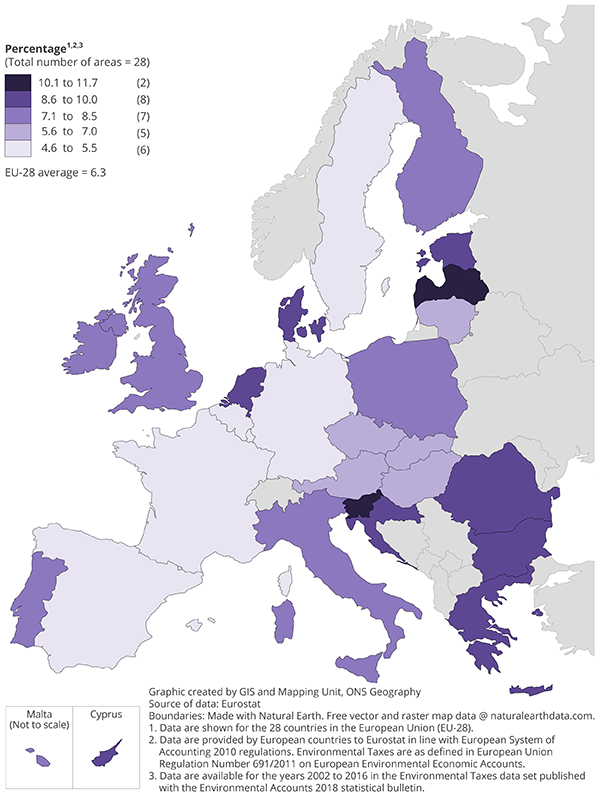

Environmental tax revenue represented 7.3% of all tax and social contribution revenue in the UK in 2016, slightly higher than the EU28 average of 6.3%. Across the EU28 in 2016, environmental tax revenue as a proportion of all tax and social contribution revenue was highest in Latvia (11.7%) and lowest in Luxembourg (4.6%) (Figure 13).

When comparing the level of environmental taxation across European countries, differences should be interpreted with caution. For instance, low government revenue from environmental taxes could signal relatively low environmental tax rates in a given country, or could result from high tax rates that have had the effect of changing patterns of consumption of the related products or activities (for example, landfill taxes in the UK). On the other hand, higher levels of environmental tax revenue could be due to low tax rates that incentivise non-residents to purchase taxed products across a border (for example, low fuel taxes in Luxembourg).

Figure 11: Environmental tax revenue, as a percentage of gross domestic product and total taxes and social contributions, 1997 to 2017

UK

Source: Office for National Statistics

Notes:

- All estimates are reported at current prices, no adjustments have been made to account for the effects of inflation.

Download this chart Figure 11: Environmental tax revenue, as a percentage of gross domestic product and total taxes and social contributions, 1997 to 2017

Image .csv .xls

Figure 12: Environmental taxes as a percentage of gross domestic product, UK and other EU28 countries, 2016

Source: Eurostat and Office for National Statistics

Download this image Figure 12: Environmental taxes as a percentage of gross domestic product, UK and other EU28 countries, 2016

.png (211.1 kB) .xls (34.8 kB){kind=link}

Figure 13: Environmental taxes as a percentage of total taxes and social contributions, UK and other EU28 countries, 2016

Source: Eurostat and Office for National Statistics

Download this image Figure 13: Environmental taxes as a percentage of total taxes and social contributions, UK and other EU28 countries, 2016

.png (211.3 kB) .xls (34.8 kB){kind=link}

Households account for almost half of all revenue from environmental taxes

Almost half of environmental taxes revenue was attributed to households in 2015 (Figure 14). In total, households paid just under £19 billion in environmental taxes, equating to £693 per household. The average environmental tax paid per household has been gradually decreasing since 20102 when households paid a total of around £20 billion in environmental taxes which equated to £763 per household (see Environmental taxes dataset).

Almost three-quarters of environmental tax revenue in 2015 was related to energy taxes, which includes taxes on transport fuels. This is reflected in the finding that after households, the largest proportion of environmental tax revenue was produced by services (16.4%) and manufacturing (10.4%) industries (Figure 14), industries which likely have high energy and transport needs.

Figure 14: Environmental tax revenue by sector; including households, 1997 and 2015

UK

Source: Office for National Statistics

Notes:

- For a full list of NACE industries and further information, see the Environmental taxes dataset accompanying this statistical bulletin.

Download this chart Figure 14: Environmental tax revenue by sector; including households, 1997 and 2015

Image .csv .xlsNotes for: Environmental taxes

NACE categories include: Agriculture, forestry and fishing; Mining and quarrying; Manufacturing; Electricity, gas, steam and air conditioning supply; Construction; Wholesale and retail trade, repair of motor vehicles and motorcycles; Transportation and storage; Water supply, sewerage, waste management and remediation activities and Services (except wholesale and retail trade, transportation and storage). Although not classified as “industries” households are also included in Eurostat environmental taxes reporting.

All data are reported at current prices so no adjustments have been made to account for the effects of inflation.

7. Environmental goods and service sector

Main points

The environmental goods and services sector (EGSS) contributed an estimated £30.5 billion to the UK economy in terms of value added in 2015 (1.6% of gross domestic product (GDP).

Waste management was the largest single contributor to EGSS output in 2015, contributing £14.2 billion, around 20% of total EGSS output.

Things you need to know about this section

A detailed publication on the Environmental Goods and Services Sector was published in May 2018; only headline figures are presented here.

The methodologies used to develop the EGSS estimates remain under development; the estimates reported in this publication are experimental and should be interpreted in this context.

Environmental goods and services sector accounted for 1.6% of GDP in 2015

The environmental goods and services sector (EGSS) statistics indicate how much of the economy is engaged in producing goods and services for environmental protection purposes and resources management activities, relative to the wider economy and provide information on the number of jobs created. They also consider how the EGSS is changing through time.

In 2015, the EGSS contributed an estimated £30.5 billion to the UK economy (Table 2) in terms of gross value added (GVA) (1.6% of GDP), an output of £62.5 billion and around 335,000 full-time equivalent (FTE) jobs.

Table 2: Estimated total output, gross value added (GVA) and employment of the UK environmental goods and services sector, UK, 2010 to 2015

| Year | Output (£ billion) | GVA (£ billion) | Employment (Full time equivalents) |

|---|---|---|---|

| 2010 | 49.4 | 24.7 | 304,500 |

| 2011 | 51.8 | 26.2 | 313,100 |

| 2012 | 54.9 | 27.1 | 316,500 |

| 2013 | 57.1 | 27.6 | 324,300 |

| 2014 | 57.9 | 27.9 | 315,300 |

| 2015 | 62.5 | 30.5 | 335,100 |

| Source: Office for National Statistics | |||

Download this table Table 2: Estimated total output, gross value added (GVA) and employment of the UK environmental goods and services sector, UK, 2010 to 2015

.xls (27.6 kB)Waste management contributed the largest amount of output to the EGSS with £14.2 billion in 2015, accounting for around 20% of total EGSS output (Figure 15). This type of activity includes the collection, treatment and disposal of various forms of waste but does not include recycling. Output from the production of renewable energy nearly trebled, from £4.6 billion in 2010 to £12.8 billion in 2015 and was the second-largest contributor to total environmental goods and services sector output in 2015.

Recycling accounted for the second-largest proportion of environmental goods and services sector (EGSS) output between 2010 and 2012, but recycling output decreased steadily from £9.9 billion in 2011 (around 20% of total EGSS output) to £6 billion in 2015 (around 10% of total EGSS output). However, it is likely that the contribution from the public sector to recycling is underestimated under our current methodology and this may explain why the estimated output and GVA for recycling decrease over time. See the detailed publication on the Environmental Goods and Services Sector for more information.

Figure 15: Environmental goods and services sector output by activity, 2010 to 2015

UK

Source: Office for National Statistics

Notes:

- The Other category comprises 12 EGSS activities: Environmental charities, Managerial activities of government bodies, Management of forest ecosystems, , Insulation activities, In-house environmental activities, Organic agriculture, Environmental related education, Energy saving and sustainable energy systems, Environmental consultancy and engineering services, Environmental related construction activities, Environmental inspection and control and Production of industrial environmental equipment.

Download this chart Figure 15: Environmental goods and services sector output by activity, 2010 to 2015

Image .csv .xls8. Environmental protection expenditure

Main points

In 2016, the UK government spent an estimated £14.4 billion on environmental protection, accounting for 1.8% of UK government expenditure.

Environmental protection expenditure as a percentage of total government spending has been relatively consistent since 2006, ranging from 1.8% to 2.2%.

The majority (77.8%) of UK government environmental protection expenditure was related to waste management.

In 2016, UK businesses spent an estimated £2.9 billion on environmental protection operating expenditure and an estimated £0.3 billion on environmental protection capital expenditure.

Payments to other businesses for environmental protection services accounted for almost three-quarters of UK businesses total environmental protection operating expenditure.

Things you need to know about this section

Environmental protection expenditure (EPE) includes all activities and actions that have as their main purpose the prevention, reduction, and elimination of pollution or any other degradation of the environment. Examples of EPE include sewerage, waste management, treatment of exhaust gases and protection of natural landscapes.

It is important to note that a low level of environmental protection expenditure (EPE) does not necessarily mean that a country or industry is not effectively protecting the environment. If a country has already invested in equipment to reduce or clean waste products then the cost maintenance of these will be small compared with the cost of introducing new equipment. In addition, if a business invests in equipment that is integrated in the production process then only the additional cost over and above an equivalent less-environmentally friendly product is included.

In contrast, the total cost is included for equipment that is not integrated into the production process, that is, is the last step. This means if a country has more focus on reducing and cleaning pollution as part of their production process then their expenditure is likely to be less than other countries that do not change their production processes and just focus on cleaning the pollution produced by them.

This chapter presents two sections of the EPE accounts: how much the general government and certain industries spent on environmental protection in 2016. The latest available estimates of total UK EPE, which includes expenditure by general government, industry, non-profit institutions serving households (for example, charities, trade unions and religious societies) and households are available to 2015 only and are included in the Environmental protection expenditure: total dataset accompanying this bulletin.

Information on environmental protection expenditure (EPE) by industry comes from an annual survey. From 2016, information is collected via this survey on capital expenditure (Capex) – subdivided into “integrated” and “end of pipe”, and operating expenditure (Opex) – subdivided into internal (the operating costs of a company’s own environmental protection equipment and services) and external (payments to others for environmental protection services including waste disposal and sewage treatment).

Previous years statistics on EPE by industry are not comparable with 2016 as a result of changes in methodology and questionnaire. For more information see Section 11: Quality and methodology.

Environmental protection expenditure accounts for 1.8% of UK government spending in 2016

UK government data for environmental protection expenditure (EPE) comes from the annual expenditure of general government, which is broken down by the Classification of Functions of Government (COFOG).

EPE by the UK general government more than tripled between 1997 and 2016 from £4.2 billion to £14.4 billion (Figure 16). This expenditure is in current prices and no adjustments have been made to account for the effects of inflation. EPE as a percentage of total government spending has been relatively consistent since 2006, ranging from 1.8% to 2.2%. It stood at 1.8% in 2016. EPE includes expenditure on solid waste management, waste water management, protecting the air and climate, protecting biodiversity and any research and development relating to these.

The rise and subsequent fall of EPE by the UK general government between 2004 and 2006 was a result of British Nuclear Fuels, which was classified as a public corporation and so not included within government, being decommissioned and transferring some nuclear reactors to the Nuclear Decommissioning Authority, which is classified as within government.

Since 1997, waste management activities such as waste collection and treatment have accounted for the highest proportion of all general government EPE. In 2016, the government spent 77.8% of total EPE on waste management.

Figure 16: Environmental protection expenditure by general government, 1997 to 2016

UK

Source: Office for National Statistics

Notes:

- All estimates are reported at current prices, no adjustments have been made to account for the effects of inflation.

- Estimates of environmental expenditure by general government shown for 2005 are higher than those published in previous editions of this bulletin, due to the impact of a methodological change in how the transfer of nuclear assets between public corporations and the UK government are treated. See Section 10 for more information.

Download this chart Figure 16: Environmental protection expenditure by general government, 1997 to 2016

Image .csv .xlsEPE as a percentage of GDP showed a generally positive trend between 1997 and 2010 (Figure 17). The decrease and subsequent increase between 2004 and 2006 is attributed to the decommissioning of BNFL as explained previously. Between 2008 and 2009, EPE increased while GDP fell as a result of the economic downturn. EPE as a percentage of GDP fell slightly between 2010 and 2012, driven by a fall in EPE (mainly waste) and an increase in GDP. Since 2012, EPE as a percentage of GDP has remained relatively stable at 0.8%, before a small decrease to 0.7% in 2016.

Figure 17: Environmental protection expenditure by general government as a percentage of gross domestic product, 1997 to 2016

UK

Source: Office for National Statistics

Notes:

- All estimates are reported at current prices, no adjustments have been made to account for the effects of inflation.

- Estimates of environmental expenditure by general government shown for 2005 are higher than those published in previous editions of this bulletin, due to the impact of a methodological change in how the transfer of nuclear assets between public corporations and the UK government are treated. See Section 10 for more information.

Download this chart Figure 17: Environmental protection expenditure by general government as a percentage of gross domestic product, 1997 to 2016

Image .csv .xlsUK businesses spent £3.2 billion on environmental protection in 2016

UK businesses spent a total of £3.2 billion on environmental protection in 2016. Operating expenditure (opex) accounted for the majority (£2.9 billion) of this total. Opex includes internal operating costs of a company’s own environmental protection activities, as well as payments to others for environmental protection services (for example, waste disposal or sewage treatment). Almost three-quarters of operational expenditure on environmental protection by businesses was to external contractors.

Capital expenditure (capex) by businesses on environmental protection was £0.3 billion in 2016. Capex consists of end of pipe expenditure and expenditure on integrated processes. Almost two-thirds of capex on environmental protection by businesses related to end of pipe expenditure, this is expenditure on equipment used to treat, handle, measure or dispose of emissions and wastes from production. Examples include effluent treatment plants, exhaust air scrubbing systems or solid waste compactors.

Capex on integrated processes relates to new or modified production facilities designed to integrate environmental protection into the production process. This might include adaptation of an existing installation or process whereby the integrated expenditure is then the total purchase cost of the adaptation. It also includes installing a new process in which the design takes environmental protection into account. In this case, the expenditure included is only the extra cost compared with installing a less environmentally friendly alternative.

Figure 18: Industry environmental protection expenditure by activity and type, 2016

UK

Source: Office for National Statistics

Notes:

- Where expenditure for a particular activity and type is less than £0.1 billion, it is not shown.

Download this chart Figure 18: Industry environmental protection expenditure by activity and type, 2016

Image .csv .xlsIn 2016, the largest amount of environmental protection expenditure was spent on waste management activities (£1.3 billion), with the majority of this on external operating expenditure (£1.0 billion). This is the same area on which the government spent most on environmental protection.

The ratio of external to in-house opex varies by environmental protection activity type, which reflects the choices of businesses to potentially outsource to specialised firms or manage the process internally. There is greater expenditure on external providers, particularly for waste management where around 80% of opex expenditure is to external providers. This suggests that businesses often do not have their own disposal systems for solid waste. By contrast, just over half of opex expenditure is to external providers for the protection of air and climate.

The ratio of end of pipe to integrated capex also varies across the environmental protection activity types, which reflects the different measures that are taken to tackle each type of pollution. For protecting air and climate, businesses spend a similar amount on the additional cost of integrated environmentally friendly equipment as they do on end of pipe equipment. By contrast, the majority of expenditure on waste and wastewater management is on end of pipe equipment, suggesting that industries focus on cleaning the by-product produced rather than reducing the amount of by-product generated during the production process.

Back to table of contents10. What’s changed in this release?

Every year, there are revisions and updates to some of the accounts. This means that when comparing this bulletin with previous years’ editions there may be differences in some of the datasets. These are due largely to revisions in data sources and improvements to methodology. Updates, particularly those involving revised methodologies, may affect the whole time series so, for example, estimates of emissions for a given year may differ from estimates of emissions for the same year reported previously.

The following changes discussed in this section apply for this year.

10.1 Greenhouse gas emissions and energy consumption

Revisions to atmospheric emissions and energy data are primarily due to:

revisions to the core energy statistics presented in the Digest of UK Energy Statistics (DUKES)

revisions to the inventory methodologies and emission factors based on new evidence

the adoption of methodologies to reflect inclusion of newly compiled sources

Specific changes that impact on the 2018 UK Environmental Accounts are discussed further in this section.

There have been significant revisions to natural gas usage as reported by DUKES, affecting all years from 2008 onwards, as a result of a research project.

A major research project has been completed to improve the estimates of emissions from shipping and the results have been incorporated into the national inventory for the first time. This has caused large recalculations to the cross-boundary emissions for the UK Environmental Accounts, which led to an increase in both fuel oil and gas oil use in 2002 and 2015 (18% and 4% respectively), but a decrease from 2003 to 2007 (a maximum reduction of 34% in 2003).

In previous years, some of the Standard Industrial Classifications have been combined. From this year onwards, data have been provided for individual Standard Industrial Classifications. These changes are presented in Table 3.

Table 3: Revisions to atmospheric emissions and energy consumption sector classifications UK, 2016

| 2015 classifications (reported in 2017) | 2016 classifications (reported in 2018) | |||

|---|---|---|---|---|

| D,E | Electricity, gas, steam and air conditioning supply; water supply, sewerage, waste management activities and remediation services | D | Electricity, gas, steam and air conditioning supply | |

| E | Water supply; sewerage, waste management and remediation activities | |||

| H,J | Transport and storage; information and communication | H | Transport and storage | |

| J | Information and communication | |||

| L,M,N | Real estate activities; professional, scientific and technical activities; administrative and support service activities | L | Real estate activities | |

| M | Professional, scientific and technical activities | |||

| N | Administrative and support service activities | |||

| R,S | Arts, entertainment and recreation; other service activities | R | Arts, entertainment and recreation; other service activities | |

| S | Other service activities | |||

| Source: Office for National Statistics | ||||

Download this table Table 3: Revisions to atmospheric emissions and energy consumption sector classifications UK, 2016

.xls (37.9 kB)The methodology for calculating emissions from agriculture has improved to include further details and more accurate estimates of the source emissions. Similarly, emissions from the source categories of the construction sector have been recalculated and this has led to significantly higher estimates from this sector than previously reported.

The cumulative impact of these, and other smaller, changes on the headline figures can be seen in Table 4, which shows the differences between estimates published in UK Environmental Accounts in 2017 and 2018.

Table 4: Air emissions and energy consumption estimates published in UK Environmental Accounts, UK, 2017 and 2018

| Measure | 1990 | 1995 | 2000 | 2005 | 2010 | 2015 | |||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Published in 2018 | |||||||||||||||||||||||||||||||||||||||

| Greenhouse gas emissions1 | 834,935 | 795,060 | 772,523 | 771,787 | 687,185 | 599,451 | |||||||||||||||||||||||||||||||||

| Acid rain precursor emissions2 | 7,103 | 5,318 | 3,748 | 3,365 | 2,207 | 1,840 | |||||||||||||||||||||||||||||||||

| Energy consumption3 | 225 | 231 | 245 | 251 | 229 | 205 | |||||||||||||||||||||||||||||||||

| Published in 2017 | |||||||||||||||||||||||||||||||||||||||

| Greenhouse gas emissions1 | 832,113 | 791,251 | 768,803 | 769,171 | 687,421 | 595,197 | |||||||||||||||||||||||||||||||||

| Acid rain precursor emissions2 | 6,869 | 5,115 | 3,568 | 3,198 | 2,159 | 1,794 | |||||||||||||||||||||||||||||||||

| Energy consumption3 | 222 | 228 | 242 | 249 | 227 | 202 | |||||||||||||||||||||||||||||||||

| Greenhouse gas emissions % change | 0.3 | 0.5 | 0.5 | 0.3 | -0.0 | 0.7 | |||||||||||||||||||||||||||||||||

| Acid rain precursor emissions % change | 3.4 | 4.0 | 5.1 | 5.2 | 2.3 | 2.6 | |||||||||||||||||||||||||||||||||

| Energy consumption % change | 1.1 | 1.3 | 1.1 | 0.7 | 0.7 | 1.1 | |||||||||||||||||||||||||||||||||

| Source: Ricardo Energy and Environment, Office for National Statistics | |||||||||||||||||||||||||||||||||||||||

| Notes: | |||||||||||||||||||||||||||||||||||||||

| 1.Thousand tonnes of carbon dioxide equivalent (CO2e) | |||||||||||||||||||||||||||||||||||||||

| 2.Thousand tonnes of sulphur dioxide equivalent (CO2e), excluding natural world | |||||||||||||||||||||||||||||||||||||||

| 3. Million tonnes of oil equivalent (Mtoe) | |||||||||||||||||||||||||||||||||||||||

Download this table Table 4: Air emissions and energy consumption estimates published in UK Environmental Accounts, UK, 2017 and 2018

.xls (36.4 kB)10.2 Material flows

The UK Environmental Accounts are based on a UK residency basis (as opposed to a territory basis). This means that data relating to UK residents and UK-registered businesses are included, regardless of whether they are in the UK or overseas. Data relating to foreign visitors and foreign businesses in the UK are excluded. From 2016, an adjustment for residence principle: fuel bunkered by resident units abroad, has been included in the import and export figures and the calculation of domestic material input. There has been no impact from this on domestic material consumption as these figures have previously included the residency adjustment for imports and exports in their calculations.

Provisional figures for 2015 have been revised and data gaps addressed, resulting in an increase in domestic extraction in the previously reported 2015 figures.

Table 5: Material flow estimates published in UK Environmental Accounts, 2017 and 2018

| Million metric tonnes | |||||

| Measure | 2000 | 2005 | 2010 | 2015 | |

|---|---|---|---|---|---|

| Published in 2018 | |||||

| Domestic extraction | 718 | 622 | 473 | 453 | |

| Imports | 221 | 293 | 274 | 289 | |

| Exports | 200 | 183 | 172 | 158 | |

| Direct Material Input (DMI) | 939 | 915 | 747 | 742 | |

| Domestic Material Consumption (DMC) | 739 | 733 | 575 | 584 | |

| Published in 2017 | |||||

| Domestic extraction | 718 | 622 | 474 | 450 | |

| Imports | 210 | 279 | 264 | 278 | |

| Exports | 194 | 177 | 166 | 152 | |

| Direct Material Input (DMI) | 928 | 902 | 739 | 728 | |

| Domestic Material Consumption (DMC) | 739 | 733 | 577 | 576 | |

| Domestic extraction % change | 0.0 | -0.0 | -0.3 | 0.6 | |

| Imports % change | 5.1 | 4.9 | 3.9 | 4.0 | |

| Exports % change | 2.9 | 3.2 | 3.5 | 4.3 | |

| Direct Material Input (DMI) % change | 1.2 | 1.5 | 1.2 | 1.9 | |

| Domestic Material Consumption (DMC) % change | 0.0 | 0.0 | -0.3 | 1.3 | |

| Source: Office for National Statistics | |||||

Download this table Table 5: Material flow estimates published in UK Environmental Accounts, 2017 and 2018

.xls (34.3 kB)10.3 Environmental taxes

In 2018, two additional taxes – Vehicle Registration Tax and Air Travel Operators Tax – have been classified as environmental taxes, therefore increasing total revenue from environmental taxes across the time series. Table 6 shows this year’s revisions, reflecting differences between estimates published in UK Environmental Accounts, 2017 and 2018.

Table 6: Revenue from environmental taxes published in UK Environmental Accounts, 2017 and 2018

| £ million | |||||

| Environmental taxes | 1997 | 2000 | 2005 | 2010 | 2016 |

|---|---|---|---|---|---|

| Total published 2018 | 24,265 | 29,322 | 31,645 | 39,399 | 47,748 |

| Total published 2017 | 24,151 | 29,204 | 31,502 | 39,231 | 47,643 |

| % increase | 0.5 | 0.4 | 0.5 | 0.4 | 0.2 |

| Source: Office for National Statistics | |||||

| Note: | |||||

| 1. All data are presented in current prices i.e. not adjusted for inflation. | |||||

Download this table Table 6: Revenue from environmental taxes published in UK Environmental Accounts, 2017 and 2018

.xls (36.9 kB)10.4 Environmental protection expenditure

Measuring environmental protection expenditure by industry

Information on environmental protection expenditure (EPE) by industry comes from an annual EPE survey. Prior to 2015, the EPE survey was commissioned by the Department for Environment, Food and Rural Affairs (Defra). Under Defra, data were collected in 1994 (pilot), 1997 and then annually between 1999 and 2013. Defra have published the results for these years.

In 2016, the survey was migrated to Office for National Statistics (ONS) and was dispatched in September 2016 to collect data for 2015. As a result of the migration, no data were collected for 2014. Results between the two surveys are not comparable owing to differences in the methodology between Defra and ONS1.

ONS sample around 3,000 businesses from four Standard Industrial Classification (SIC) sections: mining and quarrying (section B), manufacturing (Section C), energy production2 (section D), and water supply (section E36) for the survey. The survey collects information on operating and capital expenditure.

In 2016, a question was added to obtain estimates of external operating expenditure (opex); prior to this, information was only collected on in-house opex. External opex is defined as payments to others for environmental protection services (including waste disposal and sewage treatment). In-house opex is defined as the operating costs of a company’s own environmental protection equipment and services. The addition of this question highlighted that many businesses had previously been including external operating costs in the values they provided for in-house opex. Consequently, there were revisions to 2015 data, details of which can be found in the Revisions section.

As in 2015, the 2016 survey captures two types of capex: “end of pipe” and “integrated”. End of pipe capex is defined as expenditure on equipment used to treat, handle, measure or dispose of emissions and wastes outside of the production line or as the final step in the production process. Actions and activities that are beneficial to the environment and would have been taken irrespective of the environmental protection considerations are not included; for example, health and safety measures.

Integrated capex relates to new or adaptation of existing methods, technologies, processes and equipment, to prevent or reduce the amount of pollution created within the production process. For something to be considered as integrated capex for environmental protection, the company must have made a conscious decision to buy a more expensive product that would protect that environment more than a cheaper alternative. If the equipment is standard technology and there is not a cheaper, less environmentally beneficial alternative available to the company, then the cost of this would not be included. Only the additional cost of the more expensive product compared with a cheaper, less environmentally friendly alternative is captured.

For the first time in 2016, the survey collected information on the disposals of any capital assets that had been used for environmental protection purposes; estimates of such disposals are available in the Environmental protection expenditure: industry dataset accompanying this bulletin.

UK government expenditure on environmental protection

In its 2016 version of the Manual on Government Deficit and Debt, Eurostat introduced new European statistical rules on the treatment of the transfer of an asset to government to be decommissioned. As a result, the method for valuation and the timing of recording the capital transfer associated with the April 2005 transfer of nuclear assets between British Nuclear Fuels (a public corporation at that time) and the Nuclear Decommissioning authority (a central government body) has now changed.

Previously, this process was accounted for as a negative capital transfer to general government in 2005, which reduced environmental protection expenditure on waste management in that year as captured in the previous editions of this table. Under the new statistical rules, decommissioning is accounted for as a positive capital transfer in 2005 followed by smaller negative transfers from 2006 to 2010, to better reflect the periods when decommissioning took place.

Total government environmental protection expenditure estimates for 2005 are therefore around £10 billion higher than in previously published estimates, as a result of the impact of this methodological change. Total environmental expenditure estimates for 2006 to 2010 are also impacted by this change but to a much smaller extent (Figure 19).

Figure 19: Total environmental protection expenditure by general government, 1997 to 2016

UK

Source: Office for National Statistics

Notes:

- All estimates are reported at current prices, no adjustments have been made to account for the effects of inflation.

Download this chart Figure 19: Total environmental protection expenditure by general government, 1997 to 2016

Image .csv .xlsIndustry expenditure on environmental protection

This release contains revisions to 2015 figures from the Environmental Protection Expenditure Survey since they were published in July 2017. Revisions are not unusual in the first few years of a new survey and result from a variety of factors, including:

the incorporation of additional data received from businesses who have been sampled in multiple years of the survey

changes to data as a result of businesses revising their previous submissions

developments in methodology and changes to the questionnaire

Table 6 allows comparison of the latest 2016 estimates of UK total environmental protection to revised and original 2015 estimates.

In 2016, a new question was added to the survey asking businesses to report external operating expenditure as well as internal operating expenditure. It became evident during 2016 data collection that in 2015 businesses had frequently included all operating expenditure as internal operating expenditure. Where businesses had been sampled in both years and provided updates to previous years data this was revised accordingly. This is reflected in the drop in internal operating expenditure from £2.4 billion in the original 2015 estimates to £0.9 billion in the revised 2015 estimates. The revised internal opex figure is in line with 2016 data, while the original 2015 data is in line with 2016 total operating expenditure. Revisions may continue to be made in future rounds of the survey as the survey matures.

Table 7: Revisions to Environmental Protection Expenditure Survey estimates, 2015 and 2016, UK

| £ billions | |||||

| 2016 | 2015 revised | 2015 original | |||

|---|---|---|---|---|---|

| External operating expenditure | 2.1 | - | - | ||

| Internal operating expenditure | 0.8 | 0.9 | 2.4 | ||

| End of pipe capital expenditure | 0.2 | 0.6 | 1.2 | ||

| Integrated capital expenditure | 0.1 | 0.4 | 0.4 | ||

| Total environmental protection expenditure | 3.2 | 1.8 | 4.0 | ||

| Source: Environmental Protection Survey, Office for National Statistics | |||||

| Note: | |||||

| 1. Information on businesses external operating expenditure was not collected on the Environmental Protection Survey prior to 2016. | |||||

Download this table Table 7: Revisions to Environmental Protection Expenditure Survey estimates, 2015 and 2016, UK

.xls (33.3 kB)Notes for: What’s changed in this release?

The 2013 EPE survey commissioned by Defra sampled 1,166 companies and had a response rate of 21% (247 returns). The latest 2016 EPE survey dispatched by ONS sampled around 3,000 businesses and had a response rate of 68% (2051 returns). In 2013, only a sub-section of manufacturing divisions were sampled and the remainder were modelled, whilst in 2016 all were sampled. A number of questions were removed when the survey migrated to ONS in 2015, in addition the layout and wording of the form was changed.

Electricity, gas, steam and air conditioning supply.

11. Quality and methodology

This section contains important notes and definitions used in the calculation and production of the UK Environmental Accounts. These can be quite technical, so they are presented as a separate section here, but follow the same order as the rest of the sections in this bulletin.

11.1 Fuel use, energy consumption and greenhouse gas emissions

Fuel use refers to the consumption of combustible fuels. It includes fuels used for non-energy purposes, such as to produce chemicals or other fuels, but excludes combustible renewable and waste fuels1.

Energy consumption is defined as the use of energy for power generation, industrial processes and heating and transport. Unlike fuel use, energy consumption in the UK Environmental Accounts includes other sources of energy that are not from combustible fuels (such as nuclear and primary renewable electricity).

In this release, “direct use of energy” refers to the energy content of fuel for energy at the point of use, allocated to the original purchasers and consumers of fuels. Whereas, for “reallocated use of energy” the losses incurred during transformation2 and distribution3 are allocated to the final consumer of the energy rather than incorporating it all in the electricity generation industry.

Greenhouse gas emissions include carbon dioxide (CO2), methane (CH4), nitrous oxide (N2O), hydro-fluorocarbons (HFCs), perfluorocarbons (PFCs), sulphur hexafluoride (SF6) and nitrogen trifluoride (NF3). These gases are widely believed to contribute to global warming and climate change. The potential of each greenhouse gas to cause global warming is assessed in relation to a given weight of CO2 so all greenhouse gas emissions are measured as carbon dioxide equivalents (CO2e).

11.2 Material flows

In Eurostat’s Economy-Wide Material Flow Accounts Compilation Guide 2013 (PDF, 1.7MB) a distinction is made between “used” and “unused” domestic extraction. “Used” refers to an input for use in any economy (for example, where a material acquires the status of a product) and “unused” flows refer to materials that are extracted from the environment without the intention of using them. Only domestically extracted items that are “used” are included within the UK’s material flow accounts.

Biomass includes material of biological origin such as crops, wood and wild fish but not material from fossil origin. The residual biomass from primary crop harvest, such as straw and leaves, is often subject to further economic use. A large fraction of crop residues is used as bedding material in livestock husbandry, but may also be used as animal feed, for energy production, or as industrial raw material.

Fodder crops consist of beets, cabbage, maize and turnips for fodder, as well as hay and silage from grass.

The quantity of grazed biomass used is estimated according to demand for animal feed that cannot be met by fodder crops and the area of grazing land available.

The physical trade balance (imports minus exports) is defined in reverse to the monetary trade balance (exports minus imports). Physical estimates can differ quite significantly to monetary estimates.

Non-metallic minerals are mainly construction and industrial minerals, including limestone and gypsum, sand and gravel, and clays.

Fossil energy materials and carriers include coal, peat, crude oil and natural gas.

11.3 Environmental protection expenditure

What is environmental protection expenditure?

Environmental protection expenditure (EPE) includes all activities and actions that have as their main purpose the prevention, reduction and elimination of pollution or any other degradation of the environment. Examples of EPE include sewerage, waste management, treatment of exhaust gases and protection of natural landscapes. The EPE accounts aim to assess the actual expenditure on environmental protection incurred by the total economy. Environmental protection activities are defined by the Classification of Environmental Protection Activity. Information is captured on the producers and users of environmental protection services from general government1, non-profit institutions serving households (for example, charities, trade unions and religious societies), corporations and households.

Measuring environmental protection expenditure by industry

Information on environmental protection expenditure (EPE) by industry comes from an annual EPE survey. Prior to 2015, the EPE survey was commissioned by the Department for Environment, Food and Rural Affairs (Defra). Under Defra, data were collected in 1994 (pilot), 1997 and then annually between 1999 and 2013. Defra have published the results for these years. In 2016, the survey was migrated to Office for National Statistics (ONS) and was dispatched in September 2016 to collect data for 2015. As a result of the migration, no data were collected for 2014. Results between the two surveys are not comparable owing to differences in the methodology between Defra and ONS2.

ONS sample around 3,000 businesses from four Standard Industrial Classification (SIC) sections: mining and quarrying (section B), manufacturing (section C), energy production3 (section D), and water supply (section E36) for the survey. The survey collects information on operating and capital expenditure.

In 2016, a question was added to obtain estimates of external operating expenditure (opex); prior to this, information was only collected on in-house opex. External opex is defined as payments to others for environmental protection services (including waste disposal and sewage treatment). In-house opex is defined as the operating costs of a company’s own environmental protection equipment and services. The addition of this question highlighted that many businesses had previously been including external operating costs in the values they provided for in-house opex. Consequently, there were revisions to 2015 data, details of which can be found in the Revisions section.

As in 2015, the 2016 survey captures two types of capex: “end of pipe” and “integrated”. End of pipe capex is defined as expenditure on equipment used to treat, handle, measure or dispose of emissions and wastes outside of the production line or as the final step in the production process. Actions and activities that are beneficial to the environment and would have been taken irrespective of the environmental protection considerations are not included; for example, health and safety measures.

Integrated capex relates to new or adaptation of existing methods, technologies, processes and equipment, to prevent or reduce the amount of pollution created within the production process. For something to be considered as integrated capex for environmental protection, the company must have made a conscious decision to buy a more expensive product that would protect that environment more than a cheaper alternative. If the equipment is standard technology and there is not a cheaper, less environmentally beneficial alternative available to the company then the cost of this would not be included. Only the additional cost of the more expensive product compared with a cheaper, less environmentally friendly alternative is captured.

For the first time in 2016, the survey collected information on the disposals of any capital assets that had been used for environmental protection purposes; estimates of such disposals are available in the datasets accompanying this bulletin.

Notes for: Quality and methodology

Fuels from renewable sources are not covered under fuel use as defined here.