Table of contents

1. UK productivity flash estimate: July to Sept 2016

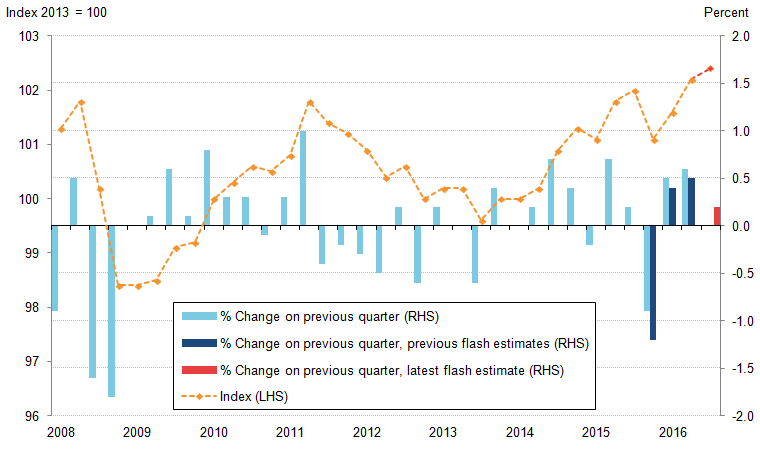

The latest Labour Force Survey data and preliminary gross domestic product (GDP) estimate indicate that output per hour – our main measure of labour productivity – grew by 0.2% in Quarter 3 (July to Sept) 2016 (Figure 1), somewhat slower than the 0.6% growth rate experienced in Quarter 2 (Apr to June) 2016. The weakening of productivity growth in Quarter 3 is the result of slower GDP growth combined with an increase in average weekly hours worked and stronger employment. This flash estimate of UK productivity uses the first available information on output and labour input for the quarter, and may be revised when we release the more detailed productivity bulletin after the third estimate of GDP for the quarter is published.

Despite this slower growth in Quarter 3, the level of output per hour in the UK remains higher than its pre-downturn peak, a largely symbolic threshold which was passed in Quarter 2 2016. UK productivity growth has been weak since the onset of the economic downturn in Quarter 1 (Jan to Mar) 2008 as a result of the relative strength of the labour market compared with GDP. Both employment – which captures the total number of people in work – and total hours – which captures both changes in employment and working patterns – fell in the course of the economic downturn, but the latter measure fell further, reflecting falls in the average hours of those in employment. However, as GDP fell by a larger proportion than either of these series – and has grown slowly by historical standards during the recovery – productivity growth has been subdued since the downturn and has recovered more slowly than following previous downturns.

Figure 1: Percentage change on previous quarter and index of output per hour

Quarter 1 (Jan to Mar) 2008 to Quarter 3 (July to Sept) 2016, UK

Source: Office for National Statistics

Download this image Figure 1: Percentage change on previous quarter and index of output per hour

.png (28.0 kB) .xls (20.0 kB){kind=link}

This growth in productivity in Quarter 3 2016 was largely a result of higher output; the most recent estimate of GDP indicated that the UK economy grew by 0.5% in Quarter 3. Figure 2 shows that in the second quarter, the economy was 8.2% larger than the pre-downturn peak level of output in Quarter 1 2008.

The services industry continued to be the main driver of growth in output in the latest quarter, as the only broad industry grouping to record positive growth. Services grew by 0.8% in Quarter 3 2016 and contributed 0.64 percentage points to the quarterly GDP growth rate. By contrast, output in the production industries fell by 0.4%, within which manufacturing fell by 1.0%. This compares with Quarter 2 2016, in which production output grew by 2.1%, with manufacturing growing by 1.6%. Production contributed negative 0.05 percentage points to GDP growth, and construction contributed a further negative 0.09 percentage points following a negative 1.4% decline in output.

Figure 2: Index of GDP (chained volume measure), employment level (16 and over) and total hours worked (weekly)

Quarter 1 (Jan to Mar) 2008 to Quarter 3 (July to Sept) 2016, UK

Source: Office for National Statistics

Download this chart Figure 2: Index of GDP (chained volume measure), employment level (16 and over) and total hours worked (weekly)

Image .csv .xlsNovember’s UK Labour Market release shows that employment of those aged 16 and over increased by 0.16% in Quarter 3 2016 to reach 31.8 million and was 1.5% higher than the same quarter in 2015. Growth in output per hour was dampened by total weekly hours worked increasing by 0.3% on the quarter, reflecting an increase of 0.15% in average weekly hours worked and the increase in employment.

Back to table of contents