2. Abstract

The 2008 economic slowdown highlighted the need for high quality statistics measuring the current state of the UK economy and the build-up of risk across different sectors.

Office for National Statistics (ONS), in partnership with the Bank of England, is undertaking the Enhanced Financial Accounts (EFA) Initiative, which seeks to improve the quality, coverage and granularity of the UK’s Financial Accounts. Part of this development involves the acquisition, interrogation and ultimately implementation of new data sources to meet the aims set out by users across government, industry and further afield.

This paper sets out the progress we have made in acquiring data from commercial sources that can provide new insights into the state of the economy.

Back to table of contents3. Introduction

We have ambitious plans to transform our economic statistics over the coming years, informed by our Economic Statistics and Analysis Strategy and with the aim of increasing the robustness and quality of UK economic statistics. Working in partnership with the Bank of England, one main element of our transformation work is the development of Enhanced Financial Accounts (EFA) – in particular more detailed “Flow of Funds” statistics – to meet evolving user needs.

Some of the main aims of the EFA programme of work are to improve the quality, coverage and granularity of financial statistics and a possible avenue for these improvements is through the use of commercial data. The benefits of commercial data over traditional surveys are numerous. Data can be obtained in a far more timely manner and has the potential for more granularity. Obtaining data from a single source, rather than multiple respondents to surveys also further ensures that the same definitions are being applied across a common subject, leading to higher quality.

This article provides an update on recent progress made in this area and the short term plans for the use of this data. A follow-up article will be published in approximately 6 months, presenting experimental statistics and providing an update on how this work is progressing.

Back to table of contents4. Context

The commercial data that we are in the process of acquiring includes information in relation to:

i) loans, credit and other forms of borrowing

ii) the issuance and ownership of debt securities and equity

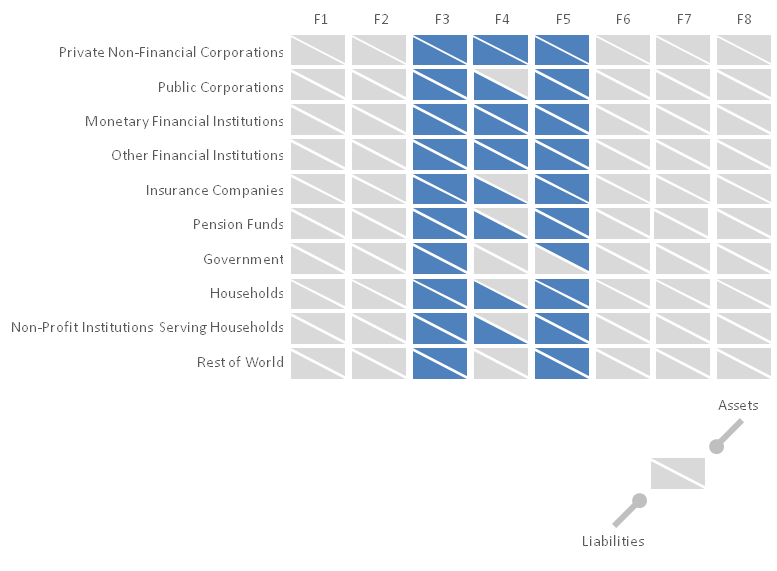

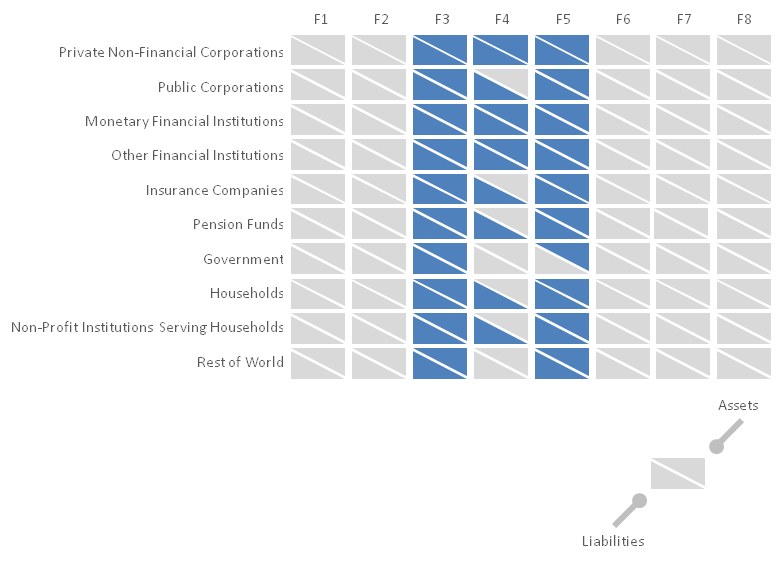

The matrix shown in Figure 1 highlights, by sector and transaction, the areas of the economy this commercial data exercise will provide information on.

Figure 1: Coverage of the commercial data

Source: Office for National Statistics

Notes:

- F1- Monetary gold and special drawing rights

F2 - Currency and deposits

F3 - Debt securities

F4 - Loans

F5 - Shares and other equity

F6 - Insurance, pension and standardised guarantee schemes

F7 - Financial derivatives and employee stock option

F8 - Other accounts receivable/payable

Download this image Figure 1: Coverage of the commercial data

.png (39.4 kB){kind=link}

Work is currently being undertaken to develop a more granular breakdown of the institutional sectors listed above. An article has been published providing proposals in this area.

Back to table of contents5. Current data sources

Current data on lending is compiled from a variety of sources. The main source for lending by banks, building societies and a small number of other financial institutions is the Bank of England, while data on lending by other institutions is varied, with surveys often used alongside other administrative data sources. In line with European requirements, statistics are produced on short-term loans (debt with an original maturity of one year or less) and long term loans (lasting over one year), with the long-term element split further, identifying loans secured on dwellings, direct investment and financial leasing.

Data relating to the issuance and ownership of securities is currently sourced from a number of different areas. These include sources such as the London Stock Exchange, company registrars and the Bank of England, as well as via ONS surveys. Statistics are produced covering long term debt securities (lasting over one year) and short term debt securities (debt with an original maturity of one year or less). These include, for example, bonds, gilts and commercial paper. We also produce statistics on listed and unlisted shares as well as other equity. Listed shares are a financial instrument that is traded through an exchange, such as the London Stock Exchange whereas unlisted shares are not traded through an exchange.

Back to table of contents6. Acquiring and analysing commercial data

For many years, we have produced a wide range of economic, social and population statistics. Data are collected in a variety of formats, including surveys sent to individuals, businesses and other organisations. However, surveys are costly both to us and businesses and are slow at responding to evolving user needs. To address this, we are looking at using alternative data sources on a far greater scale. Administrative data sources from other government departments are being obtained, investigated and implemented into the production of all statistics, but commercial data are a relatively as yet untapped source.

A market engagement event was held in August 2016 in which we presented the vision of the Enhanced Financial Accounts (EFA) initiative and announced its intention to work increasingly with commercial companies. This was followed by detailed discussions with companies on a one to one basis, which allowed us to build up relationships with data providers whilst gaining a greater understanding of the breadth of data and services available.

From there, the data requirements were refined and underpinned the tender exercise which we hope, will ultimately lead to the delivery of a new rich and granular dataset.

The next step will be to work with the data providers to analyse the data acquired and start the process of investigating the usability and suitability of the data to enhance the UK’s financial account. The intention is to initially map data against previously published statistics or other data sources, investigating emerging trends or variances with the aim of starting to produce experimental flow of funds matrices with these new data.

With this in mind we have attempted to cover the important questions we wish to answer below. These questions will underpin our analysis and evaluation of the commercial data, which we intend to publish in the latter part of 2017.

1. Are the data gained from commercial sources any better than those sourced from surveys?

Applies to:

Loans, Debt Securities and Equity

Approach:

The first question we need to address is what does “better” look like. Each data source will have its own strengths and weaknesses. Some of the sources will be more granular in nature and allow a lot more flexibility in the types of analyses we can carry out. Other commercial sources may offer a far greater coverage than surveys, which will be constrained by sampling. Alternatively, the commercial data may offer better quality or timeliness than ONS survey data can. An initial assessment of the strengths and weaknesses of each data source has taken place as part of the procurement exercise but further analysis of the successful bidders’ submissions will take place when acquire the data. These further analyses will be at the heart of the initial work we will carry out while assessing the quality of the data.

Desired outcome:

Data sources that deliver a product which is a marked improvement in terms of granularity, coverage and quality, when compared to the traditional survey option.

The potential for cost savings will also be considered a benefit.

2. Are there gaps in the commercial data and if so, how would you propose to get an alternative data source?

Applies to:

Loans, Debt Securities and Equity

Approach:

The European System of Accounts (ESA 2010) framework sets out the structure with which financial statistics must be compiled to ensure international comparability. However the EFA proposals will look to provide further granularity to meet the needs of our varied stakeholders. It is already known that the commercial data available will not be a “silver bullet”, but rather it will be used alongside current and other new sources.

Gaps will be identified through understanding the data being used and its coverage and from knowledge picked up through previous reviews of financial statistics. Administrative and regulatory data, as well as ONS surveys, will all be used alongside commercial data to complete the picture.

Desired outcome:

A comprehensive matrix which will highlight areas of concern in terms of coverage which ONS can then investigate further with alternative data sources.

3. Will you be looking to make comparisons against current data sources?

Applies to:

Loans, Debt Securities and Equity

Approach:

Commercial data will be ‘mapped’ to the ESA2010 framework and experimental statistics produced based on it. This will be compared with any current statistics being produced.

Where feasible, this will be used to determine the quality of the commercial data. In some instances however, it is acknowledged that current data sources have some deficiencies in quality. In these scenarios, accompanying information and metadata linked to the commercial data will indicate the quality of the new (experimental) estimates. This will be done using ONS’s quality assurance toolkit.

Desired outcome:

A good outcome from these investigations will show that either:

- the quality of existing data sources is proven, with commercial data adding further depth and insight or

- commercial data can replace existing data sources due to its better quality.

It is fully acknowledged that it is likely to be a combination of the above for different uses of the data.

4. Could you tell me if you are going to be looking at investigating the make-up of different ownership types within equities floated on different markets such as AIM, FTSE etc?

Applies to:

Debt Securities and Equity

Approach:

Due to the granular level of the data, covering the entire equity market should enable us to gain a far greater understanding of the ownership make up of companies. This would include previously under examined entities such as the AIM market companies for example. We will look to utilise the market of issue information for individual equities to assign the relevant ownership breakdown to different markets. These data are not currently available to us.

Desired outcome:

There is an opportunity for commercial data to provide benefits beyond the core EFA aims.

A benefit of the EFA initiative is that access to more granular data will enable us to provide more informed economic statistics.

In terms of ownership of UK shares within different markets specifically, we are aware of the external interest in this area and we are very hopeful that these breakdowns would be available through the commercial data sources.

5. How will you find out about securities on overseas markets?

Applies to:

Debt Securities and Equity

Approach:

When securities data was first collected for the national accounts the vast majority of the UK’s interest was centered on the London Stock Exchange (LSE) itself and it was these data that we were primarily interested in. By not limiting ourselves to data providers who are associated with the LSE only and looking at working with providers with a more global outlook we hope to improve our coverage of this element of the securities market.

Desired outcome:

The desired outcome would be to have comprehensive coverage of the UK’s activities in the securities market, regardless of market of issue.

6. How are you looking to improve data on lending by using commercial data?

Applies to:

Loans

Approach:

Lending data by banks is currently of good quality due to our ongoing working relationship with the Bank of England.

Lending by other financial institutions is where we see more scope for improvement due to the current reliance on surveys.

On both sides, we intend to look at adding a further level of detail that couldn’t be obtained via current means.

We have a number of areas of interest including breaking down the types of lending undertaken in greater detail, identifying the levels of unsecured lending and possibly introducing a geographical element to the analysis by looking at borrowing by region.

Desired outcome:

The desired outcome is that more detailed statistics on lending can be produced by using a combination of commercial data and other sources.

7. Are there any other benefits of using commercial data you hope to be able to prove? Conversely, what risks are associated with the use of commercial data?

Applies to:

Loans, Debt Securities and Equity

Approach:

The expectation is that commercial data can be provided in a timelier manner than other ONS data sources, however working with commercial companies to design the service provided will prove this.

Commercial data represents a potential improvement over surveys as a more complete set of statistics can be produced in a quicker fashion, leading to fewer revisions. The quality of data should also prove to be greater than that of surveys due to its potentially wider coverage. This will be investigated.

Surveys can rely on the interpretation of those completing them, which can lead to potential bias. In the long run, there is also an expectation that the costs (both to ONS and business) will be reduced, though this will not be fully researchable at this time.

The risk to using commercially sourced data lies in terms of control. This will be a time of change for ONS and although we embrace it, there will undoubtedly be some moments of uncertainty as we step firmly out of our comfort zone. ONS has always prided itself on the quality of its data outputs, and the outsourcing of the initial collection and validation process is something that we will need to monitor. Another risk lies in the fact that the data has not been collected for statistical purposes which will mean we may need to adapt our method to make best use of it.

Desired outcome:

We will know the risks and benefits, have a clear view on where the commercial data can be best utilised and inform our final decisions on using commercial data.

Back to table of contents7. Next steps

We will spend the next few months working with commercial data providers to bring in the data and complete an assessment of how it can be used. By answering the questions raised in this paper and considering other factors regarding implementation, a decision will be made as to how this data could be integrated, alongside surveys, regulatory data and administrative data, into the financial accounts. We will report back with these findings later in the year.

It is important to us that we consider user needs when evaluating the data. We therefore seek user input on our research plans via flowoffundsdevelopment@ons.gov.uk.

Back to table of contents8. Further information

Flow of Funds archived background information

27 April 2017 article – Economic Statistics Transformation Programme: Enhanced financial accounts (UK flow of funds) employee stock options

29 March 2017 article – Economic Statistics Transformation Programme: Enhanced financial accounts (UK flow of funds) Government tables for the special data dissemination standards plus (SDDS plus)

30 January 2017 article – The UK Enhanced Financial Accounts: changes to defined contribution pension fund estimates in the national accounts; part 2 – the data

16 January 2017 article – The UK Enhanced Financial Accounts: changes to defined contribution pension fund estimates in the national accounts; part 1 – the methodology

8 August 2016 article – Economic Statistics Transformation Programme: UK flow of funds experimental balance sheet statistics, 1997 to 2015

14 July 2016 article – Economic Statistics Transformation Programme: Flow of funds - the international context

14 July 2016 article – Economic Statistics Transformation Programme: Developing the enhanced financial accounts (UK Flow of Funds)

10 March 2016 article – Identifying sectoral interconnectedness in the UK economy

24 February 2016 article – Improvements to the Sector & Financial Accounts

12 January 2016 article – Historical Estimates of Financial Accounts & Balance Sheets

6 November 2015 article – Comprehensive Review of the UK Financial Accounts including explanatory notes for each financial instrument covered in the article

13 July 2015 article – Introduction Progress & Future Work

Back to table of contents