Table of contents

- Main points

- Statistician’s comment

- Summary

- 12-month growth in producer input prices continues to slow

- Growth in food prices is at its highest rate since October 2013

- UK experienced higher goods price inflation than the EU as a whole over the last 6 months

- Wholesale gas and electricity prices and energy producers’ input prices follow similar trends

- Flat sales dominate property transactions in London while average price growth for London flats falls

1. Main points

Growth in consumer prices including owner occupiers’ housing costs remained at the same rate of 2.8% for October 2017.

Growth in input prices for UK manufacturers is slowing rapidly, in line with an unwinding of the sterling depreciation effect on import prices seen during 2016.

Food prices are increasing across all main classes of product, including dairy products, which have seen recent wholesale shortages.

Goods price inflation has been increasing compared with other European countries, and is associated with higher import-intensive products bought in the UK such as food and clothing.

Retail energy prices for consumers do not always closely follow producer prices for the same products, but this is likely to be due to complex regulatory structures, pricing strategies and environmental and tax policies present in these markets.

Flat sales dominate property transactions in London but average price growth across all property types in London has been slowing from mid-2016, reversing previous trends.

2. Statistician’s comment

Commenting on today’s inflation figures, ONS Head of Inflation Mike Prestwood said:

“Inflation remains at a five year high with rising food prices offset by a fall in the cost of fuel.

“The rise in the cost of raw materials and goods leaving factories both slowed, with crude oil and petroleum prices both increasing less than at this time last year.

“House price growth increased in September, with property prices in the North West and South West of England increasing most strongly. However, growth slowed again in London with the housing market in the capital continuing to cool.”

Back to table of contents3. Summary

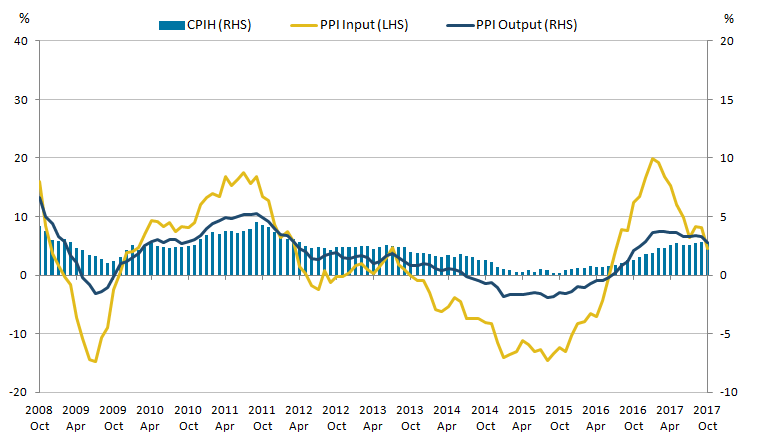

Figure 1 shows the 12-month growth in the Consumer Prices Index including owner occupiers’ housing costs (CPIH) remained unchanged at 2.8% in October 2017. The input Producer Prices Index (input PPI) grew by 4.6% in the 12 months to October 2017, down from 8.1% in the 12 months to September 2017. The output Producer Prices Index (output PPI) grew by 2.8% in the 12 months to October 2017, down from 3.3% in the 12 months to September 2017.

Figure 1: Annual growth rate for Producer Price Index (PPI) input (left-hand side), PPI output and Consumer Prices Index including owner occupiers' housing costs (CPIH) (right-hand side)

UK, October 2008 to October 2017

Source: Office for National Statistics

Notes:

- These data are also available within the Dashboard: Understanding the UK economy.

Download this image Figure 1: Annual growth rate for Producer Price Index (PPI) input (left-hand side), PPI output and Consumer Prices Index including owner occupiers' housing costs (CPIH) (right-hand side)

.png (22.9 kB) .xls (34.3 kB){kind=link}

4. 12-month growth in producer input prices continues to slow

Figure 2 shows the 12-month growth rate in the input Producer Price Index (input PPI) since January 2015, broken down into the percentage point contribution from movement in the current month and the remaining contribution from the comparison with the base index assuming no change in the current month (a form of base effect).

Figure 2: 12-month growth rate in Producer Price Index input prices, by current month and base effects, and inverted 12-month sterling effective exchange rate growth rate

UK, January 2015 to October 2017

Source: Office for National Statistics and Bank of England

Download this chart Figure 2: 12-month growth rate in Producer Price Index input prices, by current month and base effects, and inverted 12-month sterling effective exchange rate growth rate

Image .csv .xlsMovements in the 12-month growth rate of input PPI in most periods are driven by comparisons to the base year index, rather than seeing strong movements in the current month itself. As oil and commodity prices (generally priced in dollars) have tended to increase since the start of 2016, the depreciation of sterling has also had an effect over this period, ending a period of deflation in input producer prices.

Figure 2 shows the inverted sterling effective exchange rate (ERI) showing the lagged association between the depreciation of sterling, which began in early 2016, and the 12-month growth rate of producer input prices. As the 12-month growth rate for the inverted ERI has fallen, the 12-month growth rate for input PPI has also reduced, with a lag. The effect of the base index comparison has also fallen on average over the period since February 2017.

Back to table of contents5. Growth in food prices is at its highest rate since October 2013

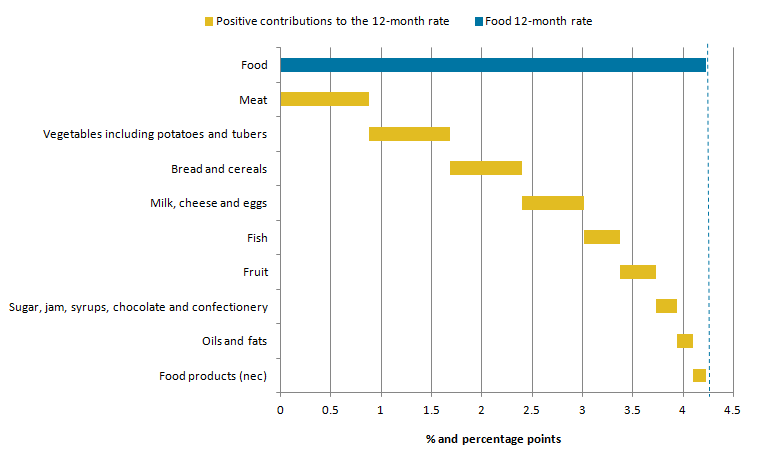

In October 2017, the food category, which grew by 4.2% since October 2016, contributed 0.3 percentage points to the overall 12-month growth rate of all-items in the Consumer Prices Index including owner occupiers’ housing costs (CPIH). Figure 3 shows, within the food category, the contributions to the 4.2% growth rate by class.

Figure 3: Contributions to the 12-month growth rate in the food category of the Consumer Prices Index including owner occupiers’ housing costs

UK, January 2015 to October 2017

Source: Office for National Statistics

Download this image Figure 3: Contributions to the 12-month growth rate in the food category of the Consumer Prices Index including owner occupiers’ housing costs

.png (14.4 kB) .xls (17.9 kB){kind=link}

The main contributors to the 12-month growth in food prices were staple products such as meat, vegetables, bread and cereals, and dairy products (milk, cheese and eggs). October 2017 is the second consecutive month where every class within the CPIH food category has made a positive contribution to the 12-month rate of food price growth. This includes dairy products, for example, where previous analysis has highlighted producer and wholesale shortages in recent months.

Back to table of contents6. UK experienced higher goods price inflation than the EU as a whole over the last 6 months

Figures 4 and 5 show the 12-month growth rates in the aggregate goods and services components of the Harmonised Index of Consumer Prices (HICP) for the UK, France, Germany and the EU as a whole from January 2010 to August 2017. August 2017 is the latest date for which comparable data for the UK and other countries’ goods and services sub-aggregates of HICP are available from Eurostat.

Figure 4: 12- month growth rates in the goods component of the Harmonised Index of Consumer Prices, various countries

January 2010 to August 2017

Source: Eurostat

Notes:

1 The latest comparable data available from Eurostat is for August 2017.

Download this chart Figure 4: 12- month growth rates in the goods component of the Harmonised Index of Consumer Prices, various countries

Image .csv .xlsAs Figure 4 shows, the growth rate for goods prices in the UK has followed similar trends to France, Germany and the EU as a whole over the period, with all having a period of relatively steep decline between October 2011 and February 2015. The decline in goods prices growth as measured by the HICP was felt most strongly by the UK; falling from a growth rate of 5.6% in October 2011 to a rate of negative 2.1% in February 2015, a decline of 7.7 percentage points across the period.

In recent months, UK goods price growth has diverged from the trends seen in France, Germany and the EU as a whole, with price growth continuing to increase. Evidence from the import intensity data table for Consumer Prices Index (CPI), available with this release, shows that the main contributors to goods price inflation are the higher import-intensive products (30% to 40% and 40% plus) such as food, clothing and household goods. These goods, alongside fuel prices, are the most likely to have seen upwards pressure on costs due to higher import costs and sterling exchange rate effects.

Recent analysis also describes how different households are affected by price rises in different types of goods, with food being particularly important for lower-income households and retired households compared with higher-income and non-retired households.

Figure 5 shows that in contrast to the growth in goods prices, the UK has consistently seen higher services price inflation than the equivalent in France, Germany and the EU as a whole since January 2010.

Figure 5: 12- month growth rates in the services component of the Harmonised Index of Consumer Prices, various countries

January 2010 to August 2017

Source: Eurostat

Notes:

- The latest comparable data available from Eurostat is for August 2017.

Download this chart Figure 5: 12- month growth rates in the services component of the Harmonised Index of Consumer Prices, various countries

Image .csv .xlsThe difference in growth rates between the UK and the EU as a whole peaked at 2 percentage points in April 2011 and has narrowed over time reaching its lowest level at 0.6 percentage points in October 2015. In August 2017, the gap was slightly higher at 0.9 percentage points. Particular services that have seen higher price growth in the UK compared with rates in other EU countries include communication and transport services. Although services price inflation in the UK as measured by the HICP has remained broadly stable since 2014 at around 2.5%, the recent uptick in July and August 2017 may be influenced by continued positive growth in unit labour costs for the sector, which has been over 2.0% since Quarter 2 (Apr to June) 2016.

Back to table of contents7. Wholesale gas and electricity prices and energy producers’ input prices follow similar trends

Figure 6 shows relative changes in input prices for firms producing and distributing electricity, consumer prices for electricity, and the wholesale electricity price, all indexed to the average price for 2011.

The market for electricity, including generation, transmission, distribution and supply, has recently been reviewed by Dieter Helm in an independent report for government (PDF 6.55MB) on the cost of energy in the UK. This report identified that electricity energy prices faced by consumers are higher than would be expected based on underlying costs and highlighted complex regulations, legacy costs and the structure of the market as likely explanations.

The same divergences of consumer and producer prices can be seen in Figure 6. Generally, prices paid by energy producers track changes in the wholesale price relatively closely, whereas the consumer price shows more of a difference.

Figure 6: Trends in Producer Price Index input electricity, Consumer Prices Index including owner occupiers’ housing costs electricity and wholesale electricity prices

June 2010 to September 2017

Source: Office for National Statistics, Office of Gas and Electricity Markets (Ofgem)

Download this chart Figure 6: Trends in Producer Price Index input electricity, Consumer Prices Index including owner occupiers’ housing costs electricity and wholesale electricity prices

Image .csv .xlsFor example, in Figure 6, between early 2014 and early 2016, wholesale and producer prices for electricity were falling while Consumer Prices Index including owner occupiers’ housing costs (CPIH) prices remained relatively flat. The sharp increase in wholesale electricity prices in late 2016 and the more gradual increases in the Producer Price Index (PPI) input prices were also not directly reflected in consumer price changes. In early 2017, wholesale and PPI prices both fell while the electricity component of CPIH rose relatively sharply, although in recent months wholesale and PPI prices have been rising again.

Figure 7 shows the equivalent series for gas producers and distributors, consumers and wholesale prices. This shows a similar picture, with PPI gas input prices following similar trends to wholesale gas prices, while the movement in the gas component of CPIH shows less direct correlation, particularly after 2014.

For example, from January 2010 to late 2013, prices were broadly rising across all three measures. From late 2013, price falls were considerably more gradual in consumer prices than producer and wholesale prices, although increases in wholesale and producer prices since early 2016 have also not been reflected in consumer prices.

As seen with electricity, falls in wholesale and producer prices in early 2017 were not mirrored in consumer prices although, unlike for electricity, consumer gas prices have been gradually decreasing since late 2013.

The differences in relative price growth for retail, wholesale and producer gas prices are also likely to reflect additional costs in the supply chain, regulation, different approaches to hedging among energy retailers and other market factors (for more information, see Ofgem’s Understanding trends in energy prices page).

Figure 7: Trends in Producer Price Index input gas, Consumer Prices Index including owner occupiers’ housing costs gas and wholesale gas prices

January 2010 to September 2017

Source: Office for National Statistics, Office of Gas and Electricity Markets (Ofgem)

Download this chart Figure 7: Trends in Producer Price Index input gas, Consumer Prices Index including owner occupiers’ housing costs gas and wholesale gas prices

Image .csv .xls8. Flat sales dominate property transactions in London while average price growth for London flats falls

Figure 8 shows flat sales as a proportion of all property transactions in England, Wales, London, East of England and the East Midlands between 2006 and 2016. The share of flat sales in London is much higher than England as a whole at nearly three times the proportion, given the structure of the property market in the capital. Wales and the East Midlands have the lowest share of flat sales each year, and the East of England is close to the England average.

Figure 8: Selected English regions, England and Wales proportion of flat sales out of total sales

2006 to 2016

Source: HM Land Registry Price Paid data, Office for National Statistics calculations

Notes:

- Data for Scotland transactions by house type are not available.

- These data are presented as annual averages for complete calendar years.

Download this chart Figure 8: Selected English regions, England and Wales proportion of flat sales out of total sales

Image .csv .xlsFigure 9 shows that in some periods since 2006, the annual price growth of flats in London has been greater than detached properties, but on the whole price growth for the two types of property move in a similar way, despite the very different share of property transactions (Figure 8).

Price growth movements in London are also similar for terraced and semi-detached properties not shown in the chart. However, Figure 9 also shows that London price growth has usually been stronger than England as a whole for both detached houses and flats, but this trend has reversed over the last year.

Figure 9: Annual price growth for flats and detached properties, London and England

January 2006 to September 2017

Source: UK House Price Index, Office for National Statistics, HM Land Registry

Download this chart Figure 9: Annual price growth for flats and detached properties, London and England

Image .csv .xlsFrom July 2016 for flats, and from December 2016 for detached properties, average price growth in London has consistently been slower than England as a whole. Average 12-month price growth for flats in London was 2.3% in September 2017, compared with 4.6% for England as a whole, and average 12-month price growth for detached properties in London was 3.9% compared with 6.3% in England as a whole.

The overall slow-down in London and some other regions of the UK can be attributed to a range of factors. For example, the Royal Institute of Chartered Surveyors (RICS) highlight a combination of the increased cost of moving, a lack of fresh stock coming onto the market, and uncertainty over the political climate as being likely to impact on property sales and price performance in the UK.

Back to table of contentsContact details for this Article

Related publications

- Consumer price inflation, UK: October 2017

- Index of Private Housing Rental Prices, Great Britain: October 2017

- Index of Private Housing Rental Prices, Great Britain: October 2017

- Construction output price indices (OPIs), UK: July to September 2017

- Services producer price inflation, UK: July to September 2017

- Producer price inflation, UK: October 2017