Table of contents

- Main points

- Management practices during the pandemic

- The determinants of good management in the pandemic

- Business changes in the pandemic: good management as facilitator of homeworking

- Labour productivity and management practices in the pandemic

- Glossary

- Data sources and quality

- Future developments

- Related links

1. Main points

The main determinants of good management in British businesses are firm size, firm age and employee human capital, and have not changed significantly during the coronavirus (COVID-19) pandemic.

Good management practices have made it easier for firms to adapt to novel practices like homeworking and online sales during the pandemic.

Overall, better-managed firms have retained their labour productivity advantage over comparable peers during 2020.

2. Management practices during the pandemic

The coronavirus (COVID-19) pandemic upended established business practices in many ways, and forced firms to adopt new ways of working. It seems natural to ask: has the role and importance of good management changed over the last 12 months?

We and others have documented many important changes in the way businesses operate and interact with customers since early 2020. Homeworking has become much more common. Online sales have risen to a record high. Many sectors reported more innovative activity since the start of the coronavirus (COVID-19) pandemic.

Amidst these changes, a growing literature recognises the importance of good management in explaining growth, innovation and productivity across businesses (PDF, 1.48MB). Good management, and in particular processes focused on managing change, would appear particularly important in dealing with the increased uncertainty and the challenges of the last year. This article sets out to see if this is true for British firms in 2020.

Back to table of contents3. The determinants of good management in the pandemic

The characteristics that reliably predict good management practices across a variety of settings, industries and countries have not changed during the pandemic. From an economic point of view, this is perhaps not surprising, as management practices are a form of capital, and therefore a stock variable that changes slowly over time (as opposed to a flow variable like investment).

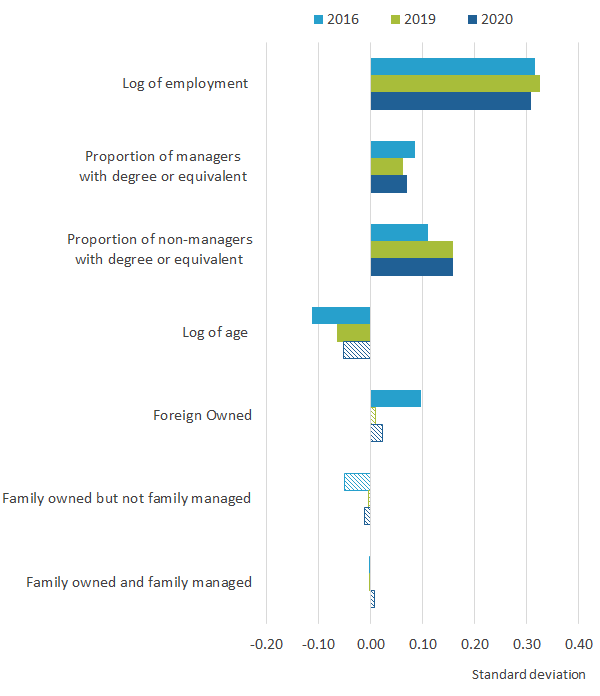

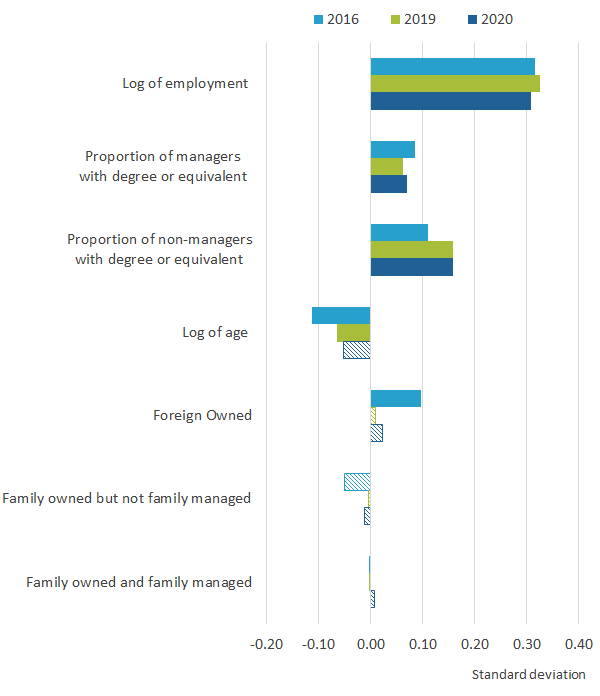

Figure 1 shows the standardised coefficients from an Ordinary Least Squares (OLS) regression of management score on observable firm characteristics and industry-region fixed effects.1 This allows us to compare like with like firms within the same industry and region. The coefficients have been standardised resulting in so-called “beta coefficients” to ensure effect sizes are comparable across variables.2

Larger firms are better managed than otherwise comparable smaller firms. Similarly, younger firms appear to be better managed. Human capital among both managers and non-managers, as approximated by the share of employees with degrees, also strongly predicts management score. This suggests that some management practices might be embodied in the skills and knowledge of the workforce, or that a certain level of human capital is needed for modern management practices to work. The type of firm structure, such as foreign ownership or family management and ownership are not strongly correlated once we control for other characteristics. Of course, a firm’s ownership could determine variables such as its size and human capital, and therefore still indirectly influence management practices.

When we compare results across years, we can see that the determinants of good management are quite stable over time, even into the coronavirus (COVID-19) pandemic of 2020. The sign of the coefficients never changes between years in the Management and Expectations Survey (MES) data, and size and statistical significance are comparable for all variables between the available years (2016, 2019 and 2020).

Figure 1: Employment, age and employee human capital predict management scores

Standardised coefficients from an OLS regression of management score on observables and industry-region fixed effects, Great Britain, 2016 to 2020

Source: Office for National Statistics – Management and Expectations Survey

Notes:

- Our population of interest covers businesses in production and services industries with employment of at least 10 in Great Britain.

- The MES sample excludes firms in Section A (Agriculture, forestry and fishing), and Sections K and L (Financial and insurance activities), and results are weighted to reflect the population of firms.

- Shaded bars indicate coefficient is not significant at the 5 percent level in the baseline regression. Variables that are not significant at the 5 percent level are: 2016 (Family owned not family managed, Family owned and family managed), 2019 (Family owned not family managed, Family owned and family managed, Foreign Owned), 2020 (Family owned not family managed, Family owned and family managed, Foreign owned, Log of age).

Download this image Figure 1: Employment, age and employee human capital predict management scores

.png (17.4 kB) .xlsx (16.1 kB){kind=link}

Notes for: The determinants of good management in the pandemic

- Controls include size, age, family management and foreign ownership; industry fixed effects are at 2 digit SIC level, region fixed effects are at NUTS1 level. Regressions are weighted using design weights and use heteroskedasticity-robust standard errors.

- Coefficients are standardised by substracting the variable mean and dividing by its standard error.

4. Business changes in the pandemic: good management as facilitator of homeworking

Can good management practices help businesses adapt to unexpected changes? Better-managed firms were more likely to adopt homeworking and shift to online sales than other comparable businesses, but only during the 2020 coronavirus (COVID-19) pandemic, when these changes were necessary.

We make use of the fact that the Management and Expectations Survey (MES) 2020 is the only British firm-level dataset that measures homeworking rates consistently before and during the pandemic.1 This allows us to establish a baseline pre-pandemic relationship between management practices, homeworking and productivity and investigate explicitly how these relationships have been affected by the changing homeworking patterns since January 2020.

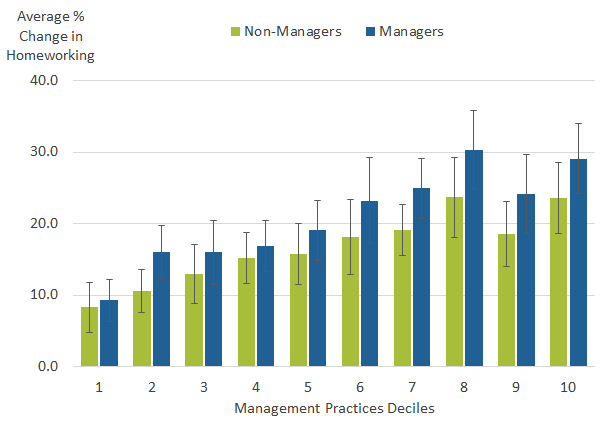

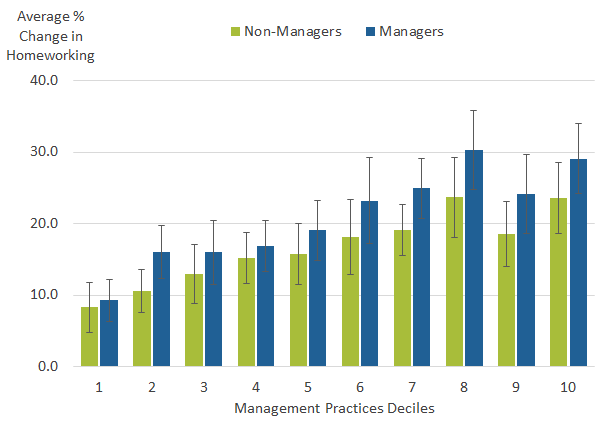

Figure 2 shows, for the purposes of a simple comparison, the change in homeworking rates from 2019 to 2020 for managers and non-managers across deciles of the management score distribution in Great Britain. For both managers and non-managers, the change in homeworking rates broadly increases across deciles, suggesting that better-managed firms are better able to switch to homeworking in 2020. Of course, better-managed firms could be different in many other ways: they could be bigger or more modern; they could be operating in different industries or regions; and they could have different ownership structures or different levels of human capital. Better-managed firms could have already had higher homeworking rates before the pandemic, suggesting that they simply operated in a different way, rather than being better able to adapt to unforeseen changes.

Figure 2: Better-managed firms increased their homeworking rates by more in 2020

Change in homeworking rates from 2019 to 2020 by decile of management score, Great Britain

Source: Office for National Statistics – Management and Expectations Survey

Notes:

- Our population of interest covers businesses in production and services industries with employment of at least 10 in Great Britain.

- The MES sample excludes firms in Section A (Agriculture, forestry and fishing), and Sections K and L (Financial and insurance activities), and results are weighted to reflect the population of firms.

- The black lines represent 95% confidence intervals, indicating the range that we expect the true parameter to lie in 95% of the time.

Download this image Figure 2: Better-managed firms increased their homeworking rates by more in 2020

.png (19.0 kB) .xlsx (17.9 kB){kind=link}

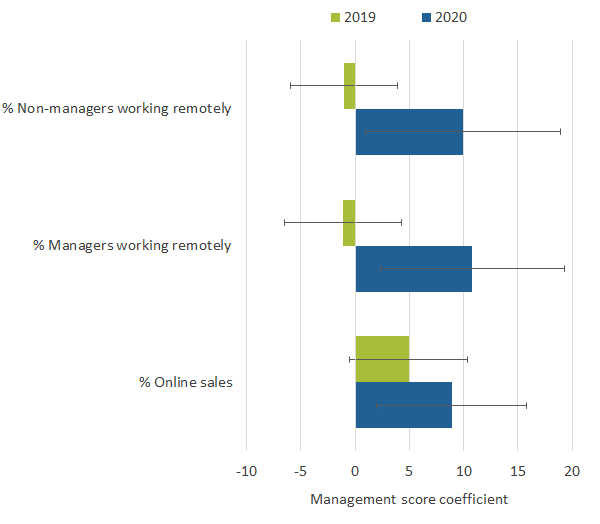

Figure 3 aims to take these other potential explanations out of the equation. Each bar shows the management score coefficients from an Ordinary Least Squares (OLS) regression2 of a different outcome controlling for the same explanatory variables. This allows us to examine the effect of good management practices on homeworking and online sales for the pre-pandemic and pandemic period without the confounding effect of other variables that could be affecting homeworking rates.

The upper bars in the first two panels show homeworking rates for non-managers and managers in 2019, respectively. After controlling for other factors, better-managed firms do not have higher homeworking rates than worse-managed firms (the confidence intervals fall across the zero line). However, as can be seen from the lower bars, in 2020 this changes considerably: now, a firm with a 1 percentage point higher management score on average has about a 10 percentage point higher homeworking rate than other comparable firms. The last panel shows that a similar pattern holds for online sales: the management score coefficient doubles in size during the pandemic and becomes more statistically significant. In other words, better management is not in and of itself related to homeworking or online sales, but when businesses had to switch to homeworking and online sales because of the pandemic, better-managed businesses were better able to do so.

Figure 3: Better-managed firms have higher homeworking rates, but only in 2020

OLS coefficients for homeworking rates and online sales in 2019 and 2020, Great Britain

Source: Office for National Statistics – Management and Expectations Survey

Notes:

- Our population of interest covers businesses in production and services industries with employment of at least 10 in Great Britain.

- The MES sample excludes firms in Section A (Agriculture, forestry and fishing), and Sections K and L (Financial and insurance activities), and results are weighted to reflect the population of firms.

- The black lines represent 95% confidence intervals, indicating the range that we expect the true parameter to lie in 95% of the time.

Download this image Figure 3: Better-managed firms have higher homeworking rates, but only in 2020

.png (11.8 kB) .xlsx (17.2 kB){kind=link}

These results are particularly interesting for homeworking because theoretically, the relationship could plausibly have been either positive or negative: good management practices might make any change, including homeworking, easier; but better-managed firms could in principle also be more reliant on face-to-face interactions than less well-managed firms.

Table 1 shows the same picture by looking at changes in homeworking and online sales rates during the pandemic, rather than levels. Better-managed firms are more likely to increase their homeworking rates and online sales rates during the pandemic, compared with otherwise similar firms in the same industry and region. The effect is very similar for managers and non-managers, perhaps suggesting coordination advantages in the homeworking decision between the two groups.

| Variables | Change in % of non-managers working from home 2019 to 2020 | Change in % of managers working from home 2019 to 2020 | Change in % of online sales 2019 to 2020 |

|---|---|---|---|

| Overall management score | 14.19*** | 15.18*** | 2.022*** |

| (4.212) | (3.72) | (0.741) | |

| Log of employment | -0.314 | 1.176** | 0.104 |

| (0.549) | (0.522) | (0.109) | |

| Family owned but not family managed | -2.169 | -2.247 | -0.0305 |

| (1.776) | (1.819) | (0.565) | |

| Family owned and family managed | -5.659*** | -6.691*** | -0.0561 |

| (1.439) | (1.646) | (0.404) | |

| Foreign owned | 8.080*** | 8.856*** | -0.414 |

| (2.678) | (2.81) | (0.425) | |

| Proportion of managers with degree or equivalent | 1.911*** | 2.527*** | 0.0592 |

| (0.534) | (0.502) | (0.112) | |

| Proportion of non-managers with degree or equivalent | 4.102*** | 3.711*** | 0.544* |

| (0.795) | (0.784) | (0.294) | |

| Log of age | 2.458*** | 0.623 | -0.184 |

| (0.757) | (0.865) | (0.2) | |

| Observations | 12,167 | 12,167 | 12,167 |

| R-squared | 0.367 | 0.312 | 0.073 |

| Industry fixed effects | Yes | Yes | Yes |

| Location fixed effects | Yes | Yes | Yes |

Download this table Table 1: Management score predicts changes in homeworking rates and online sales

.xls .csvNotes for: Business changes in the pandemic: good management as facilitator of homeworking

- On the employee-level, the Labour Force Survey (LFS) also provides a consistent comparison between the pre-pandemic and the pandemic period. This is explored in an earlier homeworking-focused article.

- Controls include size, age, family and foreign ownership; industry fixed effects are at 2 digit SIC level, region fixed effects are at NUTS1 level. Regressions are weighted using design weights and use heteroskedasticity-robust standard errors.

5. Labour productivity and management practices in the pandemic

The overall relationship between management practices and labour productivity is strong, significant and positive, even during the pandemic. Among the four component categories, employment practices (and to some extent key performance indicators, KPIs) seem particularly important to labour productivity in 2020.

Table 2 presents our Ordinary Least Squares (OLS) regressions of the effect of management score on labour productivity for 2016, 2019 and 2020. Before the pandemic, we find a positive and significant relationship between management score and labour productivity, even when controlling for many other firm characteristics. This effect is of a very similar size and significance for the pandemic period, suggesting that the underlying advantage good management bestows on firms has not been altered by the changes in the economic environment since the start of 2020.

| Variables | Log of labour productivity 2016 | Log of labour productivity 2019 | Log of labour productivity 2020 |

|---|---|---|---|

| Management score | 1.376*** | 0.616*** | 0.543** |

| (0.317) | (0.209) | (0.222) | |

| Log of employment | -0.467*** | -0.122*** | -0.131*** |

| (0.153) | (0.0231) | (0.0252) | |

| Family owned but not family managed | -0.103 | 0.0527 | 0.0516 |

| (0.0899) | (0.0756) | (0.0805) | |

| Family owned and family managed | -0.236*** | -0.00015 | -0.0742 |

| (0.091) | (0.0686) | (0.0777) | |

| Foreign Owned | 0.685*** | 0.511*** | 0.459*** |

| (0.102) | (0.0846) | (0.0857) | |

| Proportion of managers with degree or equivalent | 0.0324* | 0.015 | 0.0251 |

| (0.0179) | (0.0221) | (0.027) | |

| Proportion of non-managers with degree or equivalent | 0.0755*** | 0.0439 | 0.0162 |

| (0.0254) | (0.0325) | (0.0356) | |

| Log of age | 0.170*** | 0.139*** | 0.130*** |

| (0.0448) | (0.0453) | (0.0449) | |

| Observations | 6,691 | 11,152 | 10,707 |

| R-squared | 0.412 | 0.205 | 0.219 |

| Industry fixed effects | Yes | Yes | Yes |

| Location fixed effects | Yes | Yes | Yes |

Download this table Table 2: Management score is strongly and positively related to labour productivity

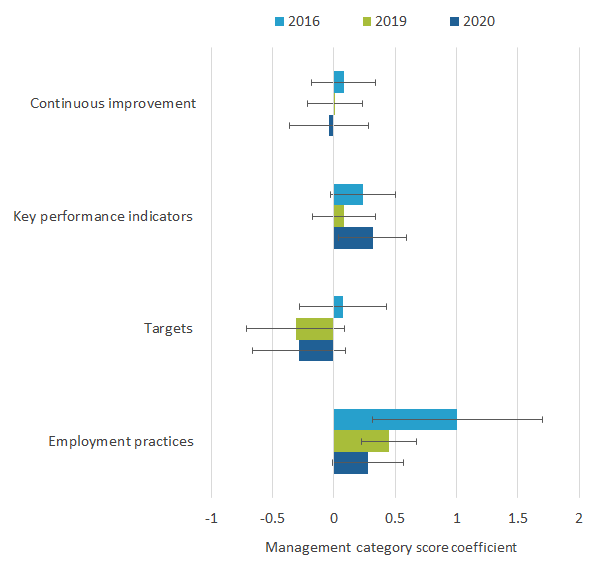

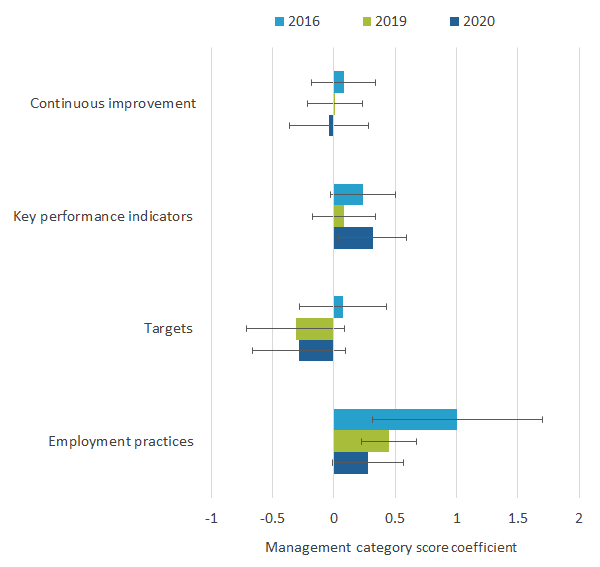

.xls .csvFinally, Figure 4 shows the coefficients from an OLS regression of labour productivity on the same firm characteristics as in Table 2, but with the overall management score split up into the four component categories – continuous improvement, KPIs, targets and employment practices. We can see that in 2020, employment practices seem to be most strongly correlated with labour productivity, with only KPIs also significant individually at least at the 10 percent level.1

Figure 4: Employment practices are most strongly related to labour productivity in 2020

Management category coefficients from a regression on labour productivity, 2016 to 2020, Great Britain

Source: Office for National Statistics – Management and Expectations Survey

Notes:

- Our population of interest covers businesses in production and services industries with employment of at least 10 in Great Britain.

- The MES sample excludes firms in Section A (Agriculture, forestry and fishing), and Sections K and L (Financial and insurance activities), and results are weighted to reflect the population of firms.

- The black lines represent 95% confidence intervals, indicating the range that we expect the true parameter to lie in 95% of the time.

Download this image Figure 4: Employment practices are most strongly related to labour productivity in 2020

.png (13.2 kB) .xlsx (17.5 kB){kind=link}

Notes for: Labour productivity and management practices in the pandemic

- When testing their significance jointly, the other categories are significant at conventional significance levels. This suggests that firms who have a high score in one category also do in the others. While we can therefore say that together they matter for labour productivity, we cannot with certainty say how much each category contributes.

6. Glossary

Confounder

A variable which is associated with both the dependent and an independent variable, and which may explain some of their apparent relationship or may cause two not directly related variables to appear related. For example, the size of businesses affects both management practices and labour productivity.

Heteroskedasticity-robust standard errors

Often in real-world data, the variation in the data that cannot be explained by observable characteristics varies itself between observations. This phenomenon is called heteroskedasticity and can cause problems when estimating parameters. Heteroskedasticity-robust standard errors allow the variance of the regression error term to be different for different observations, and therefore addresses this concern.

Human capital

Human capital refers to the skills, abilities and knowledge of individuals – a form of intangible asset embodied in the firm’s workers. Employees with higher human capital are generally thought to be more productive.

Industry and region fixed effects

We use regression analysis to compare like-for-like individuals or firms as much as possible. By including fixed effects, we are able to control for the average differences across industries or regions in both observable and unobservable explanatory variables. We can therefore compare observations that are much more alike.

Management practices score

The overall management practices score (management score for short) is an average of the scores along the four dimensions of management practices measured: continuous improvement, key performance indicators (KPIs), targets and employment practices.

Standardised (beta) coefficients

Standardised coefficients are obtained by demeaning a variable and scaling it by its standard error. They make coefficients comparable across variables. For example, a beta coefficient of 0.2 for log employment (independent variable) means that with every increase of one standard deviation in log employment, the management score (dependent variable) rises by 0.2 standard deviations, holding other factors constant.

Stock vs. flow variable

A stock variable is a quantity measured at a particular point in time whereas a flow variable measures quantities over a specific time period. Investment is a flow variable, capital is a stock variable.

Design weights

Design weights are primarily used to compensate for factors that may make the sample unrepresentative of the population it was drawn from. Two important reasons to weigh the sample are non-random sampling (for instance, to ensure adequate coverage of specific segments of the British business population) and differential survey response rates.

Back to table of contents7. Data sources and quality

In this article, we use new data from the Management and Expectations Survey (MES) 2020 to shed light on the role management practices play in allowing businesses to adapt to the challenges of the coronavirus (COVID-19) pandemic. MES 2020 gathered information on the management practices, homeworking rates and other firm characteristics for about 12,000 firms in Great Britain during 2019 and 2020 and follows on from MES 2017, which collected similar information during 2016. For more information about MES 2020 and the broader context of measuring UK management practices, please see Management practices in Great Britain: 2016 to 2020.

In MES 2020, management practices are measured along four dimensions. These are continuous improvement (the degree to which emerging problems are used to improve processes), the use of key performance indicators (KPIs) to measure progress, the use of (and employee knowledge about) appropriate business targets and an index of employment, training and hiring practices. The overall score runs from a 0 for firms that fail to adopt modern management practices on all four dimensions to a 1 for firms that follow best practices in all areas. The average score across Great Britan in 2020 was 0.6.

Labour productivity for the purposes of this article is defined as turnover less intermediate costs divided by employment. This allows us to be consistent with the Annual Business Survey (ABS). All variables used to compute this figure are taken from the responses to MES 2020 and MES 2017 as necessary.

Given the nature of the survey, a few important caveats apply. First, the survey underlying this analysis was conducted across two national lockdowns and collected information retrospectively for two calendar years. These factors could have caused selective responses or recall bias, issues explored in more detail in Management practices in Great Britain: 2016 to 2020. Second, because of delays in the release of the ABS 2020, the analysis in this paper relies on MES data only and does not include total factor productivity analysis. Future work can hopefully fill this gap. Finally, given the nature of MES 2020, we can only examine firm responses to the disruptions of the coronavirus (COVID-19) pandemic in the short term. Long-term changes to the role of management practices are outside the scope of this article.

Back to table of contents8. Future developments

This article uses novel data from the Management and Expectations Survey (MES) 2020 to investigate the changing role of management practices during the ongoing coronavirus (COVID-19) pandemic. Overall, we find that while the relationships between firm characteristics and management practices, and between management practices and labour productivity are remarkably stable during the pandemic, good management has played a role in facilitating the transition to successful homeworking and online sales.

These results raise a series of follow-on questions.

First, to what extent are better-managed firms better positioned to take advantage of rebound growth as the economy recovers? Many of the components of the management practices score relate to longer-term planning and could therefore be more relevant to the recovery than the pandemic itself. Second, can better-managed firms learn from their homeworking experience and successfully integrate elements of homeworking and office-based work to transform their business model in a sustainable way? This matters because successfully integrating remote working could give firms access to much wider talent pools. Third, are the dimensions of management measured in MES (and methodologically similar surveys, such as the Management and Organisational Practices Survey (PDF, 715KB)) still the primary dimensions relevant to distinguish between well- and and less well-managed firms? As technologies change, so do management techniques. Perhaps future waves of MES will have to deal explicitly with changes in working arrangements that the pandemic may have accelerated.

Authors

Jakob Schneebacher, Kyle Jones, Mohammad Shafat.

In collaboration with the Economic Statistics Centre of Excellence (ESCoE), with funding from Economic and Social Research Council (ESRC) grant ES/S012729/1 and UK Research and Innovation (UKRI) grant ES/V004387/1.

Back to table of contents