Table of contents

- Main points

- Latest indicators at a glance

- Restaurant seated diners

- UK spending on debit and credit cards

- Social impact of the coronavirus

- Business impacts and insights

- Online job adverts

- Retail footfall

- Road traffic in Great Britain

- Ship visits

- Data

- Glossary

- Measuring the data

- Strengths and limitations

- Related links

1. Main points

In the week to Monday 17 May 2021, the seven-day average estimate of UK seated diners was at 73% of its level in the equivalent week of 2019, a 13 percentage point increase from the previous week; this was in part driven by a notable rise to UK seated diners on Monday 17 May 2021, the day on which indoor dining started to reopen across the UK (OpenTable). See Section 3.

In the week to 13 May 2021, the aggregate CHAPS-based indicator of credit and debit card purchases decreased by 9 percentage points from the previous week, to 97% of its February 2020 average level; this was driven by falls across all four consumption categories (Bank of England Clearing House Automated Payment System (CHAPS) data). See Section 4.

Of the 96% of adults who reported they had left home in the last seven days, the proportion who shopped for things other than food or medicine saw a slight decrease of 4 percentage points to 26% this week (period 12 to 16 May 2021) compared with the previous week (period 5 to 9 May 2021) (Opinions and Lifestyle Survey). See Section 5.

The proportion of businesses currently trading has remained stable, at 83% from mid-April to mid-May 2021, and a further 5% of businesses intend to restart trading in the next two weeks (Business Insights and Conditions Survey (BICS)). See Section 6.

The volume of online job adverts on 14 May 2021 had increased across all categories when compared with 7 May 2021 and was at 114% of its February 2020 average level (Adzuna). See Section 7.

In the week to 15 May 2021, UK retail footfall was at 72% of its level in the equivalent week of 2019; this remains much stronger than the levels seen earlier in the year (before restrictions eased), but is still considerably lower than that seen before the coronavirus (COVID-19) (Springboard). See Section 8.

The volume of motor vehicle traffic on Monday 17 May 2021 was at 96% of the level seen in the first week of February 2020, a 3 percentage point increase from the previous week (Department for Transport (DfT)). See Section 9.

There was an average of 350 daily ship visits in the week ending 16 May 2021, an increase of 8% from the previous week (323) but 6% lower than the equivalent week in 2019 (371) (exactEarth). See Section 10.

There were 17,316 company incorporations in the week to 14 May 2021, a 26% increase from the previous week (13,768), and 25% higher than the equivalent week in 2019 (13,847) (Companies House). See the accompanying dataset.

There were 5,790 voluntary dissolution applications in the week to 14 May 2021, a 4% decrease from the previous week (6,019) and 6% lower than the equivalent week of 2019 (6,128) (Companies House). See the accompanying dataset.

The overall price of items in the online food and drink basket decreased by 0.1% in the week ending 16 May 2021; six categories provided small downward contributions (online price collection). See the accompanying dataset.

Improving our analysis

Please complete our survey to help us improve this bulletin. The survey will be live for a minimum of one week.

Results presented throughout this bulletin are experimental and may be subject to revision.

2. Latest indicators at a glance

Embed code

This week, the following indicators are featured in this section of the bulletin only:

Companies House company incorporations and voluntary dissolution applications. See also the accompanying dataset.

Online price changes. See also the accompanying dataset.

Energy Performance Certificate (EPC) lodgements.

Traffic camera activity data are available in the accompanying dataset only.

Back to table of contents3. Restaurant seated diners

OpenTable is a leading provider of online restaurant reservations, with daily data being publicly available in its The state of the industry dashboard. These data show the impact of recent events and restrictions on the hospitality industry using a sample of restaurants on the OpenTable network across all channels, that is, online reservations, phone reservations, and walk-ins.

Figure 1: In the week to Monday 17 May 2021, the seven-day average estimate of UK seated diners was at 73% of the level in the same week of 2019, an increase of 13 percentage points from the previous week

Seated diners, seven-day average, percentage compared with the equivalent week of 2019, week ending 24 February 2020 to week ending 17 May 2021, UK, London and Manchester

Source: OpenTable

Download this chart Figure 1: In the week to Monday 17 May 2021, the seven-day average estimate of UK seated diners was at 73% of the level in the same week of 2019, an increase of 13 percentage points from the previous week

Image .csv .xlsIn the week to Monday 17 May 2021, the seven-day average estimate of UK seated diners was at 73% of the level seen in the equivalent week of 2019. This is a 13 percentage point increase when compared with the equivalent index in the previous week. It also continues the notable rise in seated diner estimates seen since pubs and restaurants first reopened in England on 12 April 2021, prior to which estimates were at 0% of their 2019 level. This latest week’s increase was in part driven by a notable rise in seated diners observed on Monday 17 May 2021, the day on which indoor dining reopened in England, Wales and Scotland.

In the same week ending 17 May 2021, the seven-day average estimate of seated diners in London increased by 6 percentage points to 43% of its level in the equivalent week of 2019. Meanwhile, the equivalent figure in Manchester was 124%, a notable increase of 22 percentage points from the previous week. Similar to that for total UK, these increases were in part driven by notable rises to seated diners in both London and Manchester on Monday 17 May 2021, coinciding with the reopening of indoor dining.

Back to table of contents4. UK spending on debit and credit cards

These data series are experimental faster indicators for estimating UK spending on credit and debit cards. They track the daily Clearing House Automated Payment System (CHAPS) payments made by credit and debit card payment processors to around 100 major UK retail corporates. These payments are the proceeds of recent credit and debit card transactions made by customers at their stores, both via physical and online platforms. More information on the indicators is provided in the accompanying methodology article.

Companies are allocated to one of four categories based on their primary business:

- "staples" refers to companies that sell essential goods that households need to purchase, such as food and utilities

- "work-related" refers to companies providing public transport or selling petrol

- "delayable" refers to companies selling goods whose purchase could be delayed, such as clothing or furnishings

- "social" refers to spending on travel and eating out

Figure 2: In the week to 13 May 2021, the aggregate CHAPS-based indicator of credit and debit card purchases decreased by 9 percentage points from the previous week, to 97% of its February 2020 average

Index February 2020 = 100, a backward looking seven-day rolling average, 13 January 2020 to 13 May 2021, non-seasonally adjusted, nominal prices

Source: Office for National Statistics and Bank of England calculations

Notes:

- Users should note the daily payment data is the sum of card transactions processed up to the previous working day, so there is a slight time lag when compared with real-life events on the chart.

- The vertical lines indicate important events. In order, the events are: PM coronavirus (COVID-19) announcement; lockdown begins; some non-essential shops allowed to reopen; local coronavirus alert levels; national restrictions begin in England; Christmas Eve; lockdown begins in England and Scotland; “stay at home” rule ends in England; reopening of non-essential shops, and pubs and restaurants (outdoors) in England.

- Percentage point difference is derived from current week and previous week index before rounding.

Download this chart Figure 2: In the week to 13 May 2021, the aggregate CHAPS-based indicator of credit and debit card purchases decreased by 9 percentage points from the previous week, to 97% of its February 2020 average

Image .csv .xlsFigure 2 shows changes in the value of CHAPS payments received by large UK corporates from their credit and debit card processors, "merchant acquirers".

In the week to 13 May 2021, the CHAPS-based indicator of credit and debit card purchases in aggregate decreased by 9 percentage points from the previous week to 97% of its February 2020 average level. All consumption categories fell in this latest week:

- “delayable” spending fell by 15 percentage points

- “work-related” spending fell by 3 percentage points

- “social” spending fell by 5 percentage points

- “staples” spending fell by 8 percentage points

In the latest week, only “staples” spending was above its February 2020 average level at 112%. Meanwhile, “social” was at 81%, while “delayable” and “work-related” spending were both at 97% of their February 2020 average levels.

Since the substantial fall in spending at the beginning of the year, the aggregate CHAPS-based indicator of debit and credit card purchases has gradually increased; its level in this latest week was up by 32 percentage points from that seen on 14 January 2021, and “delayable” spending saw the largest increase over this period of 46 percentage points.

The full data time series available for data on UK spending on debit and credit cards can be found in the accompanying dataset.

Back to table of contents6. Business impacts and insights

The proportion of businesses currently trading has remained stable, at 83% from mid-April to mid-May 2021, and a further 5% of businesses intend to restart trading in the next two weeks.

Final data for Wave 30 of the Business Insights and Conditions Survey (BICS) can be found at Business insights and impacts on the UK economy: 20 May 2021.

Further information can also be found in the Business insights and impact on the UK economy dataset.

Back to table of contents7. Online job adverts

Online job adverts by category

These figures are experimental estimates of online job adverts provided by Adzuna, an online job search engine, by category and by UK countries and English regions. The number of job adverts over time is an indicator of the demand for labour. The Adzuna categories used do not correspond to Standard Industrial Classification (SIC) categories, so these values are not directly comparable with our Vacancy Survey.

Figure 3: On 14 May 2021, the proportion of total online job adverts was at 114% of its February 2020 average, and “wholesale and retail” exceeded its February 2020 average for the first time since 6 March 2020

Volume of online job adverts by category, index February 2020 = 100, 4 January 2019 to 14 May 2021, non-seasonally adjusted

Embed code

Notes:

- Further category breakdowns are included in the Online job advert estimates dataset and more details on the methodology can be found in Using Adzuna data to derive an indicator of weekly vacancies

The proportion of UK online job adverts on 14 May 2021 was at 114% of its February 2020 average level, an increase of 8 percentage points when compared with a week ago (7 May 2021).

Over the same period, excluding the “unknown” category, the volume of online job adverts had increased in all 28 categories. The largest weekly increase was for "transport and logistics", which rose by 20 percentage points to 254% of its February 2020 average level. This is a continuation of a strong upward trend for this category, having increased every week since 12 February 2021 and by 127 percentage points over this period. This is also the highest volume of online job adverts seen for this category since the beginning of the series in February 2018.

The proportion of online job adverts for “wholesale and retail” also saw a substantial increase of 17 percentage points from last week to 105% of its February 2020 average level on 14 May 2021. The volume of online job adverts for this category has risen every week since 26 February 2021, increasing by 49 percentage points over this period. This is also the first time that the volume of online job adverts in this category has exceeded its February 2020 average level since 6 March 2020.

For “catering and hospitality”, the proportion of online job adverts increased by 12 percentage points from a week ago to 115% of its February 2020 average level. This continues its recent upward trend and is an increase of 57 percentage points since 9 April 2021, just before the first easing of hospitality restrictions when pubs and restaurants reopened in England.

Online job adverts by region

Figure 4: On 14 May 2021, the volume of online job adverts had increased in all UK countries and English regions when compared with a week ago

Volume of online job adverts by region, index February 2020 = 100, 4 January 2019 to 14 May 2021, non-seasonally adjusted

Embed code

On 14 May 2021, the volume of UK online job adverts had increased across all UK countries and English regions when compared with a week ago. Northern Ireland saw the largest weekly increase, where the proportion of online job adverts rose by 61 percentage points to 149% of its February 2020 average level. Note that this increase for Northern Ireland follows a substantial decrease last week, which was a result of a drop in adverts from a single source.

North East England also saw a notable increase in its proportion of online job adverts over the latest week, by 11 percentage points, to 151% of its February 2020 average level on 14 May 2021. This is the highest volume of online job adverts seen on 14 May 2021 out of all of the UK countries and regions as a proportion of their February 2020 average.

The smallest weekly increases were recorded in London, South East England and the East of England, each by 6 percentage points, with their proportion of online job adverts at 98%, 106% and 119% of their February 2020 average levels respectively. London was the only region where online job adverts were below their February 2020 average level on 14 May 2021.

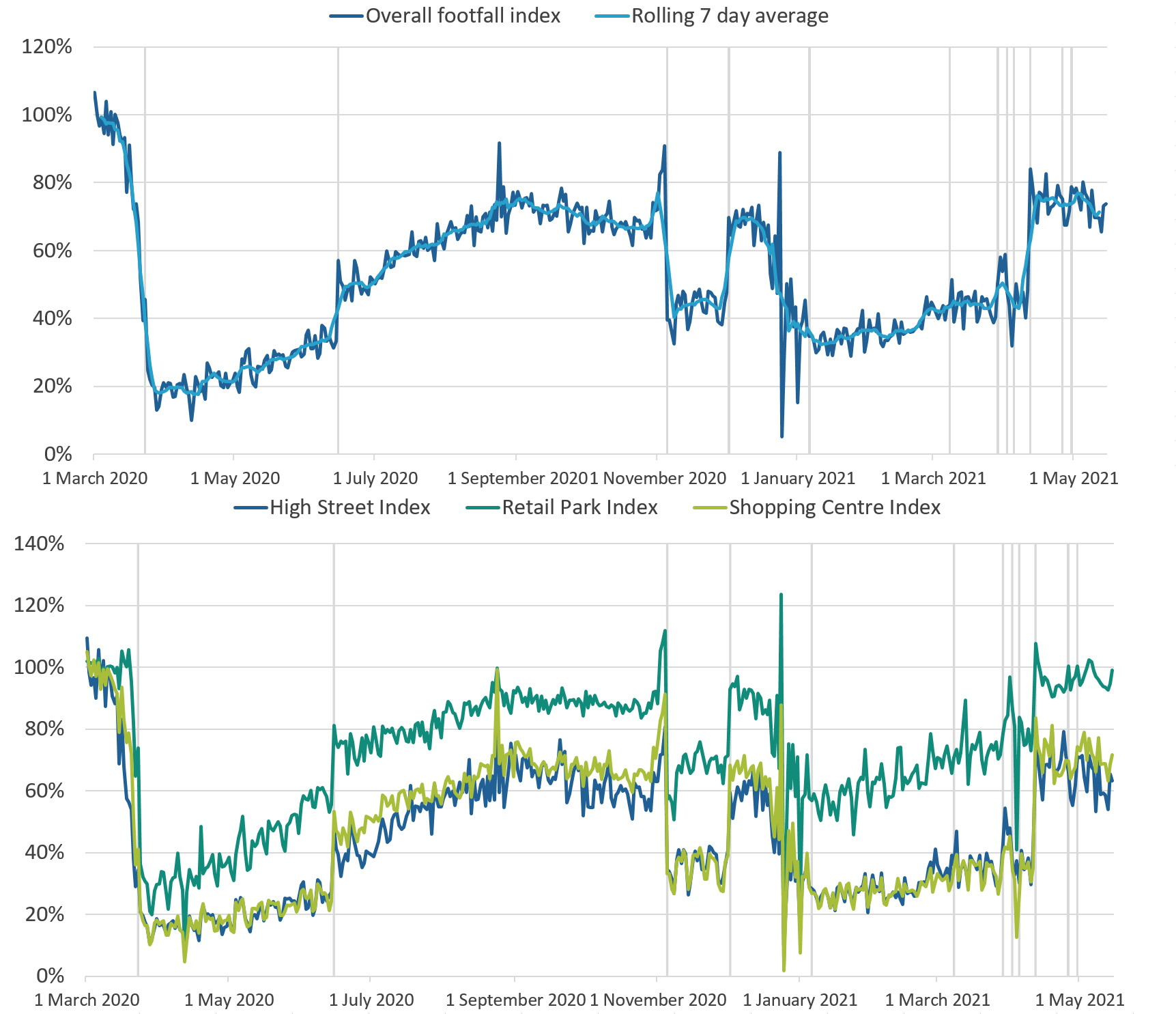

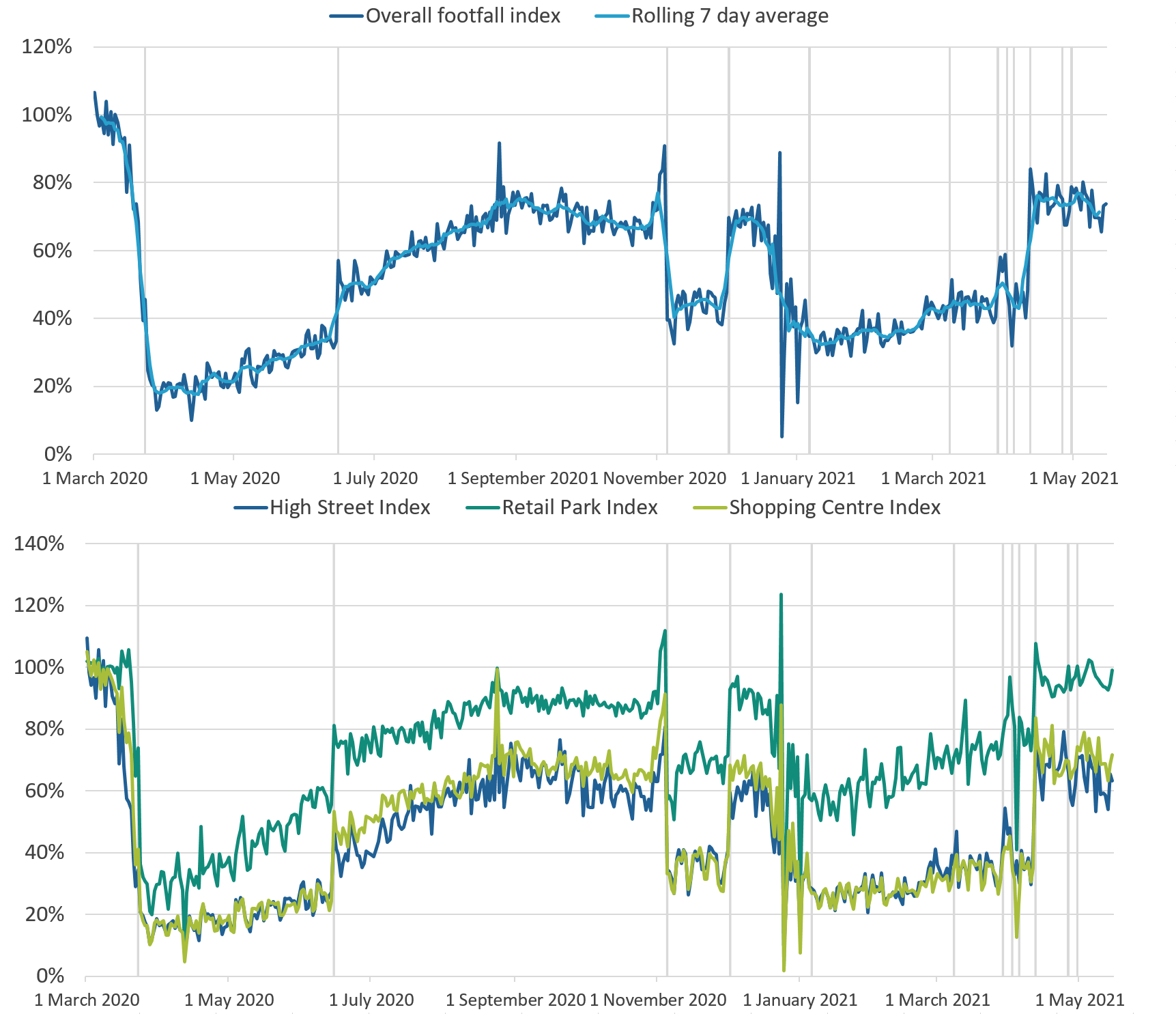

Back to table of contents8. Retail footfall

National retail footfall

National footfall figures are supplied by Springboard, a provider of data on customer activity. It measures the following for overall UK retail footfall, as well as by high street, retail park, and shopping centre categories:

daily retail footfall as a percentage of its level on the same day of the equivalent week of 2019; for example, Saturday 15 May 2021 is compared with Saturday 11 May 2019

total weekly retail footfall as a percentage of its level in the equivalent week of 2019

the percentage change in weekly footfall compared with the previous week; for example, Week 19 of 2021 is compared with Week 18 of 2021

Springboard's weekly data are defined over a seven-day period running from Sunday to Saturday; Week 19 of 2021 therefore refers to the period Sunday 9 May 2021 to Saturday 15 May 2021

Figure 5: In the week to 15 May 2021, overall retail footfall was at 72% of its level in the same week of 2019

Volume of overall daily retail footfall, percentage compared with the equivalent day of the equivalent week of 2019, 1 March 2020 to 15 May 2021

Source: Springboard and the Department for Business, Energy and Industrial Strategy

Notes:

- The vertical lines indicate important events. In order, the events are; first national lockdowns imposed; lockdown restrictions begin to ease across the UK; circuit-breaker lockdown in England; regional restrictions begin in England; national lockdown begins in England; reopening of schools in England; "stay at home" rule ends in England; Good Friday 2021; Easter Monday 2021; reopening of non-essential retail in England and Wales; reopening of non-essential retail in Scotland; reopening of non-essential retail in Northern Ireland.

Download this image Figure 5: In the week to 15 May 2021, overall retail footfall was at 72% of its level in the same week of 2019

.png (288.4 kB){kind=link}

According to Springboard, in the week to 15 May 2021, UK retail footfall remained much stronger than the levels seen earlier in the year (before restrictions eased), but still considerably lower than that seen before the coronavirus (COVID-19) pandemic started, at 72% of its level in the equivalent week of 2019.

In the latest week, retail footfall as a proportion of its level in the equivalent week of 2019 remained strongest at retail parks at 95%; the equivalent figures for shopping centres and high streets were 71% and 61%, respectively.

High streets saw a week-on-week increase in footfall of 4%, its first week-on-week increase since the easing of lockdown restrictions in England on 12 April 2021 when retail footfall volumes grew substantially higher. This weekly increase was in part driven by a 19% increase in footfall at high streets on Saturday 15 May 2021 when compared with the Saturday in the previous week. Footfall at retail parks and shopping centres both fell by 3%, when compared with the previous week.

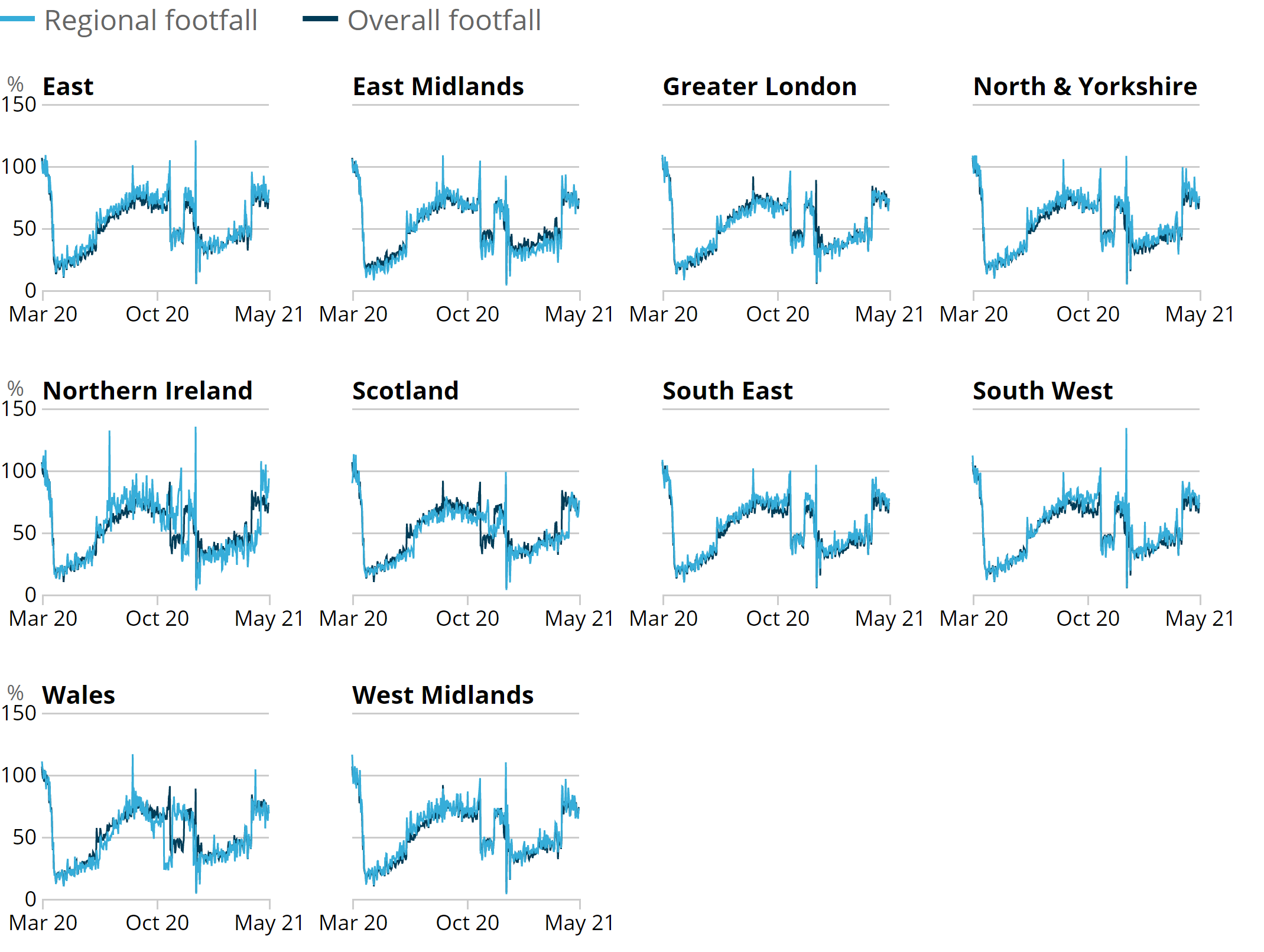

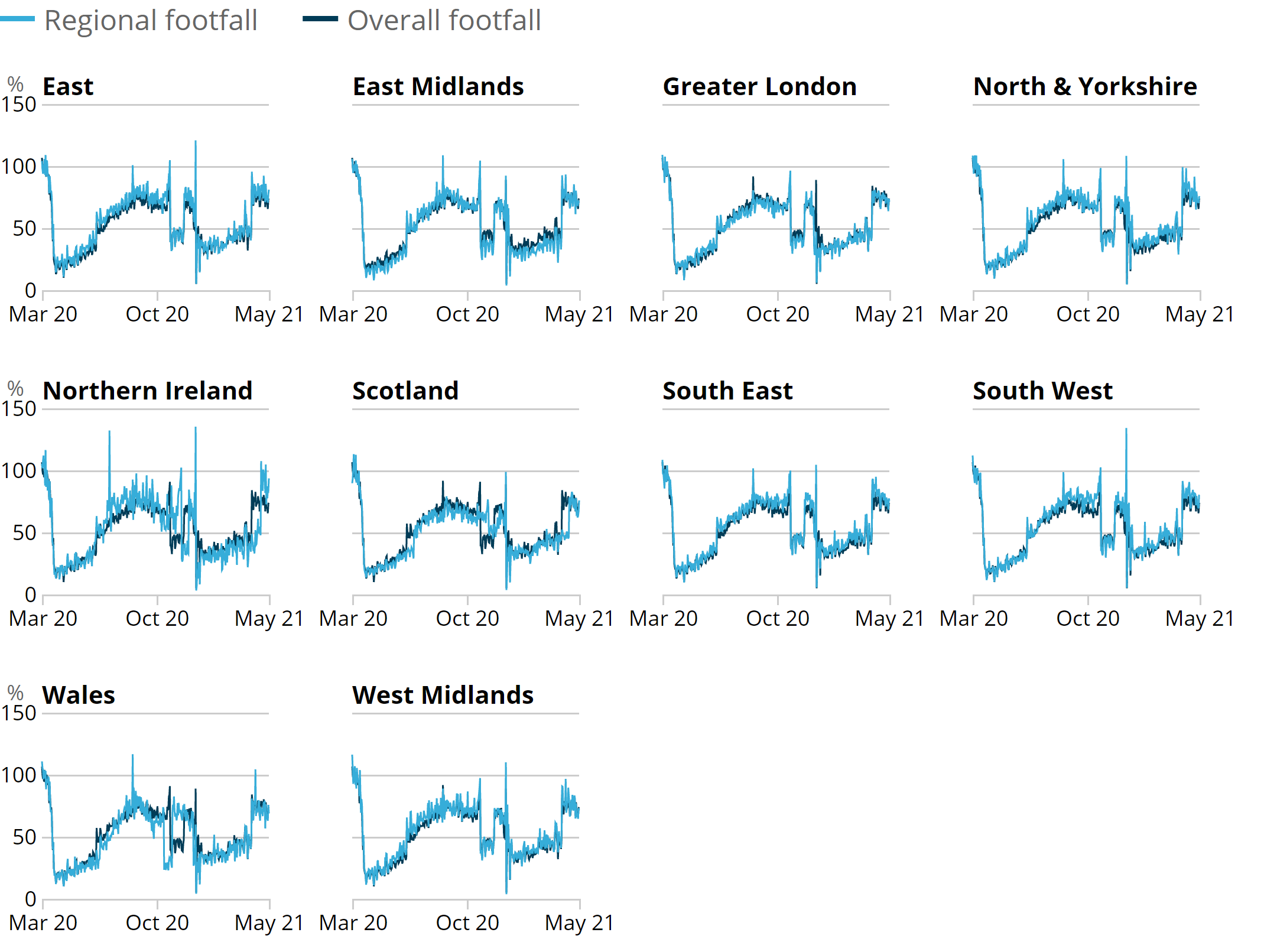

Regional retail footfall

Figure 6: Retail footfall in the week to 15 May 2021 was strongest in Northern Ireland at 85% of its level in the equivalent week of 2019

Volume of daily retail footfall, percentage of the level recorded on the same day of the equivalent week of 2019, UK regions, 1 March 2020 to 15 May 2021

Source: Springboard and the Department for Business, Energy and Industrial Strategy

Notes:

- Prior to 3 January 2021 daily indices were generated by comparing footfall against its level on the same day of the equivalent week the year before. From this date onwards they were generated by comparing footfall against its level on the same day of the equivalent week in 2019. For a two-day period, from 1 January 2021 to 2 January 2021 daily indices were therefore generated using a 2021 versus 2020 comparison.

Download this image Figure 6: Retail footfall in the week to 15 May 2021 was strongest in Northern Ireland at 85% of its level in the equivalent week of 2019

.png (218.0 kB){kind=link}

According to Springboard, when compared with other UK regions, retail footfall as a proportion of its level in the equivalent week in 2019 was strongest in Northern Ireland at 85%. In the same period, retail footfall was relatively the weakest in Wales, at 68% of its level in the equivalent week of 2019. Across all UK regions, retail footfall remains below its level in the equivalent week of 2019.

The North and Yorkshire saw the largest week-on-week increase in retail footfall by 5% in the week ending 15 May 2021. This was in part driven by a large increase in high street footfall (10%) for that region when compared with the previous week. Meanwhile, Scotland saw the largest week-on-week decrease in retail footfall by 4%.

Back to table of contents9. Road traffic in Great Britain

According to Department for Transport (DfT) non-seasonally adjusted road traffic data, the volume of all motor vehicle traffic on Monday 17 May 2021 was at 96% of the level seen on Monday of the first week of February 2020. This is a 3 percentage point increase from last week (Monday 10 May 2021) and a 19 percentage point increase since 8 March 2021, just before the first easing of restrictions was seen in the UK.

Compared with the previous week, car traffic increased by 3 percentage points to 91% of the level seen on the same day of the first week in February 2020. Light commercial vehicle traffic also increased, by 2 percentage points, to 110% whereas heavy goods vehicle traffic remained broadly unchanged at 109%.

Figure 7: The volume of motor vehicle traffic on Monday 17 May 2021 was at 96% of the level seen in the first week of February 2020, a 3 percentage point increase from the previous week

Daily road traffic index: 100 = same traffic as the equivalent day of the week in the first week of February 2020, 1 March 2020 to 17 May 2021, non-seasonally adjusted

Source: Department for Transport road traffic statistics: management information

Notes:

- The vertical lines indicate important events. In order, these events are: first national lockdown begins; Easter; May day bank holiday; Spring bank holiday; August bank holiday; restrictions re-introduced in England; Christmas Day; lockdowns announced in England and Scotland; “stay at home” rule ends in England; Easter; Early May Bank Holiday.

Download this chart Figure 7: The volume of motor vehicle traffic on Monday 17 May 2021 was at 96% of the level seen in the first week of February 2020, a 3 percentage point increase from the previous week

Image .csv .xlsThe daily DfT estimates are indexed to the first week of February 2020 and the comparison is with the same day of the week. The data provided are useful as an indication of traffic change rather than actual traffic volumes. More information on the methods, quality and economic analysis for these indicators can be found in the DfT methodology article.

Back to table of contents10. Ship visits

These shipping indicators are based on counts of all vessels, and cargo and tanker vessels. As discussed in Faster indicators of UK economic activity: shipping, we expect the shipping indicators to be related to the import and export of goods.

The coronavirus (COVID-19) pandemic first began to affect the level of shipping visits from the week ending 29 March 2020. For this reason, average ship visits in the latest week are compared with the equivalent week in 2019 rather than 2020.

Figure 8: There was an average of 350 daily ship visits in the week ending 16 May 2021, an increase of 8% from the previous week (323) but 6% lower than the equivalent week in 2019 (371)

Daily movements in shipping visits, UK, seasonally adjusted, 1 December 2019 to 16 May 2021

Source: exactEarth

Download this chart Figure 8: There was an average of 350 daily ship visits in the week ending 16 May 2021, an increase of 8% from the previous week (323) but 6% lower than the equivalent week in 2019 (371)

Image .csv .xlsThe 8% weekly increase in average daily ship visits in the week ending 16 May 2021 is a return to similar levels seen two weeks ago, following the drop in visits seen last week (week ending 9 May 2021). This weekly increase can be attributed to higher activity in numerous UK ports including Southampton, Tyne, Holyhead and Belfast.

Figure 9: There was an average of 105 cargo and tanker ship visits in the week ending 16 May 2021, broadly unchanged from the previous week (103) and the equivalent week in 2019 (102)

Daily movements in shipping visits, UK, seasonally adjusted, 1 December 2019 to 16 May 2021

Source: exactEarth

Notes:

- See the accompanying dataset for notable dates and weather events.

Download this chart Figure 9: There was an average of 105 cargo and tanker ship visits in the week ending 16 May 2021, broadly unchanged from the previous week (103) and the equivalent week in 2019 (102)

Image .csv .xls11. Data

UK spending on credit and debit cards

Dataset | Released 20 May 2021

Experimental indicator for monitoring UK retail purchases derived from the Bank of England's Clearing House Automated Payment System (CHAPS) data.

Shipping indicators

Dataset | Released 20 May 2021

Experimental weekly and daily ship visits dataset covering UK ports.

Traffic camera activity

Dataset | Released 20 May 2021

Experimental daily traffic camera counts data for busyness indices covering the UK.

Online job advert estimates

Dataset | Released 20 May 2021

Experimental job advert indices covering the UK online job market.

Company Incorporations and Voluntary Dissolutions

Dataset | Released 20 May 2021

The number of weekly Companies House Incorporations and Voluntary Dissolution applications accepted.

Online weekly price changes

Dataset | Released 20 May 2021

Experimental estimates of online price changes for a selection of food and drink products from several large UK retailers.

Business insights and impact on the UK economy

Dataset | Released 20 May 2021

Responses from the Business Insights and Conditions Survey (BICS).

12. Glossary

Faster indicator

A faster indicator provides insights into economic activity using close-to-real-time big data, administrative data sources, rapid response surveys or Experimental Statistics, which represent useful economic and social concepts.

Company incorporations

Incorporations are when a company is added to the Companies House register of limited companies. This can also include where an existing business applies to become a limited company, where it was not one before.

Voluntary dissolution applications

A voluntary dissolution application is when a company applies to begin dissolution proceedings. As such, they effectively chose to be removed from the Companies House register. For a company to be eligible to voluntarily dissolve, it should not have completed any trading activity for a period of three months.

Back to table of contents13. Measuring the data

UK coronavirus restrictions

A full overview of coronavirus (COVID-19) restrictions for each of the four UK constituent countries can be found here:

These restrictions should be considered when interpreting the data featured throughout this bulletin.

Back to table of contents14. Strengths and limitations

Information on the strengths and limitations of the indicators in this bulletin is available in the Coronavirus and the latest indicators of the UK economy and society methodology.

As of 20 May 2021, we revised the online weekly price changes dataset to correct an issue that affected the results for week ending 9 May. The issue was caused by a change in processing that resulted in some incorrectly matched products. Changes at the aggregate level were small but the headline growth did change from 0.0% to 0.1%. No other time periods in the prices data were affected by this.

Back to table of contents

5. Social impact of the coronavirus

This section includes some provisional results from the Opinions and Lifestyle Survey (OPN) covering the period 12 to 16 May 2021. The survey went out to 5,984 adults in Great Britain and had a response rate of 69%.

Further information to help understand the impact of the coronavirus (COVID-19) pandemic on people, households, and communities in Great Britain, will be available in Coronavirus and the social impacts on Great Britain due to be published 21 May 2021.

Travelling to work

In the period 12 to 16 May 2021, the proportion of working adults in Great Britain who in the last seven days:

travelled to work (either exclusively or in combination with working from home) increased slightly by 2 percentage points from the previous week (5 to 9 May 2021) to 62%; this proportion has gradually increased since mid-February 2021 (44% in the period 10 to 14 February)

worked exclusively from home remained broadly similar to the previous week at 25%

neither travelled to work nor worked from home remained broadly similar to the previous week at 13%

Shopping

Of the 96% of adults that reported they had left home in the last seven days, the proportion that did so to shop for food and medicine remained broadly similar to the previous week at 73%.

The proportion of these adults who shopped for things other than food and medicine in the last seven days saw a slight decrease of 4 percentage points to 26% this week (period to 16 May 2021) compared with the previous week (period to 9 May 2021).

Back to table of contents