Table of contents

- Main points

- Things you need to know about this release

- E-commerce sales for businesses with 10 or more employees

- E-commerce sales including micro-enterprises

- Businesses’ use of websites, internet access and internet connection speeds

- Use of social media

- Cloud computing

- Big data

- Your views matter

- Main issues specific to this bulletin

- Quality and methodology

1. Main points

In 2015, e-commerce sales by businesses with 10 or more employees in the UK non-financial sector were £533 billion, representing 19.0% of business turnover. This decreased from £543 billion (19.4% of business turnover) in 2014. These estimates are at current prices.

Sales made by Electronic Data Interchange (EDI) of £318 billion contributed 59.6% of the value of total e-commerce sales in 2015 for businesses with 10 or more employees, a decrease from 63.8% in 2014.

Website sales of £215 billion contributed 40.4% to the total e-commerce sales in 2015 for businesses with 10 or more employees, an increase from 36.2% in 2014.

Micro-enterprises’ (businesses with less than 10 employees) e-commerce sales were £21.2 billion in 2015. This represented 4.6% of business turnover of micro-enterprises. Their e-commerce sales consisted of £18.8 billion of website sales and £2.4 billion of EDI sales.

In 2015, 83.0% of all businesses had internet access, 80.7% of all businesses used a fixed broadband connection and 55.6% used a mobile broadband internet connection.

Back to table of contents2. Things you need to know about this release

The Organisation for Economic Co-operation and Development (OECD) definition of e-commerce is used in this statistical bulletin. An e-commerce transaction is defined as “the sale or purchase of goods or services, conducted over computer networks by methods specifically designed for the purpose of receiving or placing of orders”. It is important to note, under this definition, that “the goods or services are ordered by those methods, but the payment and the ultimate delivery of the goods or services do not have to be conducted online”.

These estimates are sourced primarily from the E-commerce Survey of UK Businesses and supplemented with information from the Annual Business Survey (ABS). The 2015 E-commerce Survey of UK Businesses selected nearly 11,000 UK businesses in the manufacturing, production, construction, distribution and parts of the service sectors of the economy. These statistics are presented on a current price basis, which reports prices as they were at the time of measurement and not adjusted for inflation.

This release contains information on micro-enterprises (businesses with fewer than 10 employees) and also estimates broken down by the following employment sizebands: 10 to 49, 50 to 249, 250 to 999 and 1,000 or more.

Furthermore, approximately 40% of the survey questions change each year. This is to enable the survey to cover changes and developments in the use of information and communication technologies (ICT) and e-commerce. Therefore the availability of time series varies according to how long a particular question has been included in the survey.

E-commerce estimates prior to 2008 are not directly comparable to recent years due to changes to the measurement of e-commerce. Therefore, the time series for e-commerce estimates in this release start at 2008. The revisions policy for this release is that estimates in the previous two years are subject to revision.

Estimates from the E-commerce survey and the Retail Sales Inquiry (RSI) measure completely different concepts. The E-commerce survey measures sales over a website, regardless of who the sales are to. Therefore, the estimates for the retail sector from the E-commerce survey relate to total sales over a website made by businesses classified to the retail sector (ie division 47 of the Standard Industrial Classification). These sales will be all sales over a website, not just retail sales over a website, whereas the RSI just measures retail sales, defined as sales to the general public for household consumption. Therefore, estimates from the RSI and the E-commerce survey are not directly comparable.

Back to table of contents3. E-commerce sales for businesses with 10 or more employees

Total e-commerce sales are comprised of sales received over a website and sales received over Electronic Data Interchange (EDI). These 2 components are quite different types of activity, but both are considered as e-commerce due to their use of electronic communication for transactions:

- website sales are sales over a website or “app” irrespective of the payment method

- EDI is the computer-to-computer exchange of data and documents in a standard electronic format; EDI is a central part of e-commerce because it enables businesses to exchange information electronically much faster, more cheaply and more accurately than is possible using other methods

In 2015, the value of e-commerce sales by businesses was £533 billion (based on businesses with 10 or more employees). This was a decrease, at current prices, of £9.9 billion since the 2014 estimate of £543 billion. The total e-commerce sales of £533 billion represented 19.0% of business turnover, compared with 19.4% in 2014 and 13.7% in 2008.

EDI sales of £318 billion accounted for 59.6% of the value of e-commerce sales in 2015 (based on businesses with 10 or more employees), with the remaining £215 billion (40.4%) being website sales. The proportion of businesses making e-commerce sales was 21.5% in 2015, an increase from 17.1% in 2009 (the earliest year when comparable records are available). In 2015, more businesses made website sales (18.6%) compared with EDI sales (5.1%), although the value of EDI sales is much greater than website sales.

Figure 1: UK e-commerce sales, 2008 to 2015 (excluding micro-enterprises)

Source: Office for National Statistics

Download this chart Figure 1: UK e-commerce sales, 2008 to 2015 (excluding micro-enterprises)

Image .csv .xlsSales over a website have grown steadily in recent years, both in terms of the proportion of businesses using websites for sales and the value of website sales.

In 2015, the value of website sales as a proportion of turnover was 7.7%, up from 7.0% in 2014 and 4.9% in 2009.

The value of sales to private customers in 2015 was £119 billion. The largest businesses (1,000 or more employees) made the highest sales to private customers at £77.5 billion in 2015. The value of sales to businesses or public authorities was £96.5 billion. Businesses with 250 to 999 employees made the highest sales to businesses or public authorities of £35.9 billion.

Figure 2: Value of UK e-commerce sales over a website, by size of business, 2009 to 2015 (excluding micro-enterprises)

Source: Office for National Statistics

Download this chart Figure 2: Value of UK e-commerce sales over a website, by size of business, 2009 to 2015 (excluding micro-enterprises)

Image .csv .xlsSales over EDI are only made to businesses, whereas website sales are made to businesses or public authorities and households. The value of EDI sales was £318 billion in 2015. This is a decrease of £28.4 billion (8.2%) since 2014, but an increase of £53.2 billion (20.1%) since the 2009 estimate of £264 billion.

Figure 3: Value of UK e-commerce sales over EDI, by size of business, 2009 to 2015 (excluding micro-enterprises)

Source: Office for National Statistics

Download this chart Figure 3: Value of UK e-commerce sales over EDI, by size of business, 2009 to 2015 (excluding micro-enterprises)

Image .csv .xlsE-commerce sales by industry sector

The wholesale and manufacturing sectors reported the highest values of e-commerce sales in 2015 at £189 billion and £155 billion respectively. These values represented 35.5% and 29.1% of e-commerce sales respectively.

The construction sector reported the highest percentage increase in total e-commerce sales in 2015, an increase of 50.0% from £5.6 billion in 2014 to £8.4 billion in 2015.

Figure 4: Value of UK e-commerce sales, by industry sector, 2009 to 2015 (excluding micro-enterprises)

Source: Office for National Statistics

Download this chart Figure 4: Value of UK e-commerce sales, by industry sector, 2009 to 2015 (excluding micro-enterprises)

Image .csv .xls4. E-commerce sales including micro-enterprises

In 2015 micro-enterprises made total e-commerce sales of £21.2 billion. These consisted of £18.8 billion website sales and £2.4 billion Electronic Data Interchange (EDI) sales. Combining the e-commerce sales made by micro-enterprises with those made by businesses with 10 or more employees gave an overall value of e-commerce sales of £554 billion in 2015.

Including micro-enterprises’ sales with those made by businesses with 10 or more employees increased total website sales to £234 billion and EDI sales to £320 billion.

Website sales made by micro-enterprises represented 8.0% of the value of website sales for all businesses. EDI sales made by micro-enterprises represented just 0.7% of the value of all EDI sales in 2015.

Figure 5: Total UK e-commerce sales, by size of business, 2014 and 2015 (including micro-enterprises)

Source: Office for National Statistics

Download this chart Figure 5: Total UK e-commerce sales, by size of business, 2014 and 2015 (including micro-enterprises)

Image .csv .xlsIn 2015 website sales to private customers by all businesses were £131 billion.

Businesses with 10 or more employees accounted for £119 billion of these sales, while micro-enterprises accounted for £12.3 billion. This value was higher than sales to private customers made by businesses with 10 to 49 employees at £11.7 billion. Website sales to businesses or public authorities were £103 billion in 2015 and micro-enterprises made just £6.5 billion of these sales.

E-commerce sales by industry sector

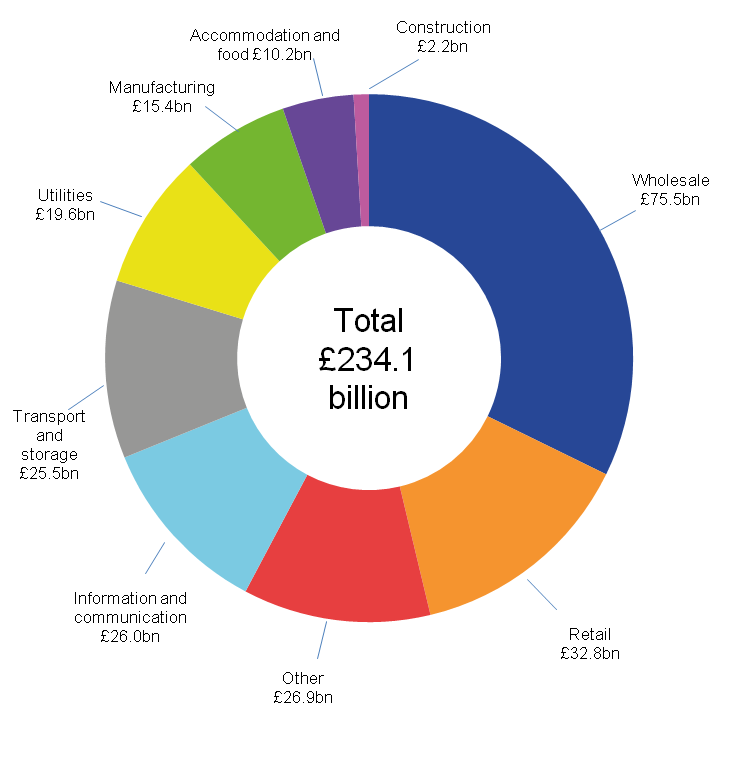

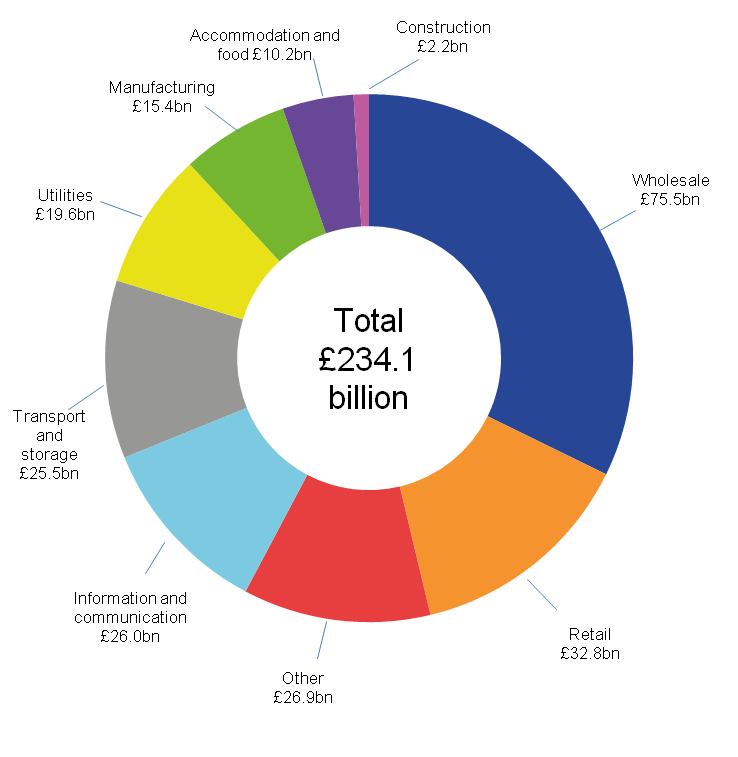

The wholesale sector reported the highest value of website sales at £75.5 billion; the construction industry reported the lowest value at £2.2 billion in 2015.

Figure 6: UK e-commerce sales via a website, by industry sector, 2015 (including micro-enterprises)

£ billion

Source: Office for National Statistics

Download this image Figure 6: UK e-commerce sales via a website, by industry sector, 2015 (including micro-enterprises)

.png (41.7 kB) .xls (27.1 kB){kind=link}

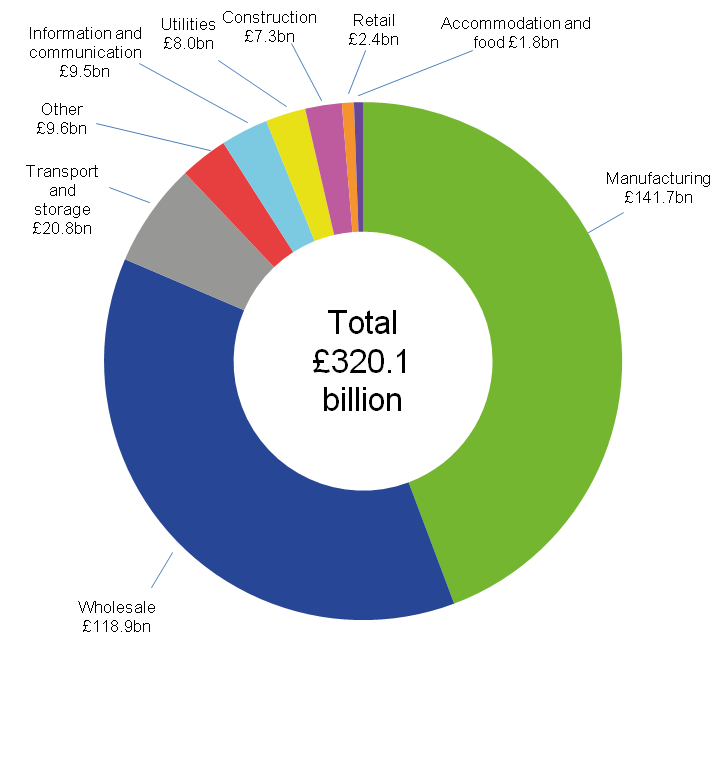

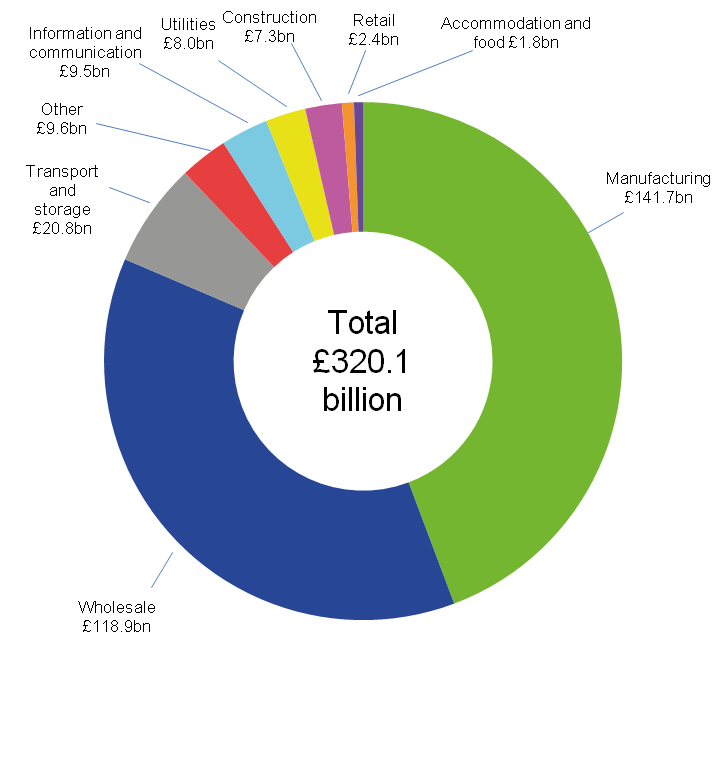

The manufacturing sector reported the highest value of EDI sales at £142 billion; the accommodation and food services industry reported the lowest value at £1.8 billion in 2015.

Figure 7: UK e-commerce sales via EDI, by industry sector, 2015 (including micro-enterprises)

£ billion

Source: Office for National Statistics

Download this image Figure 7: UK e-commerce sales via EDI, by industry sector, 2015 (including micro-enterprises)

.png (41.2 kB) .xls (27.6 kB){kind=link}

5. Businesses’ use of websites, internet access and internet connection speeds

Use of websites

In 2015, 50.1% of all businesses had a website. There appears to be a clear difference in the use of websites by micro-enterprises, compared with larger businesses. In 2015, nearly all of the largest businesses (250 to 999 and 1,000 or more employees) had a website (97.0% and 97.6% respectively), while 80.6% of businesses with 10 to 49 employees had a website, but less than half (46.4%) of the micro-enterprises did so. Since 2014 there has been a slight increase of 2.6 percentage points in the proportion of all businesses with a website.

Internet access

In 2015, 83.0% of all businesses had internet access, remaining at the same level as the 2014 estimate. All sizebands of businesses with 50 or more employees had levels of internet access above 99.0%, compared with micro-enterprises at 81.6% and businesses with 10 to 49 employees at 94.7%.

As with household internet access, as reported in the Internet Access Households and Individuals 2016 statistical bulletin, the majority of businesses have a fixed internet connection, with 80.7% continuing to use fixed broadband (DSL or other fixed connection) in 2015. This was down from 81.7% in 2014. Mobile broadband using 3G or 4G increased in 2015 to 55.6% up from 46.9% in 2014.

Internet connection speeds

The E-commerce and ICT Survey measures the maximum contracted download speed of businesses in the following bands: less than 2Mbps (Megabits per second), 2Mbps or more but less than 10Mbps, 10Mbps or more but less than 30Mbps, 30Mbps or more but less than 100Mbps and 100Mbps or more.

As high-speed fibre optic broadband is rolled out across the UK by providers offering improved speeds for businesses and households, it is unsurprising that more businesses indicated in 2015 that they had faster contracted internet speeds than in 2014.

Only 6.9% of businesses reported speeds less than 2 Mbps. The number of businesses subscribing to broadband with a connection speed between 30Mbps and 100Mbps, increased from 12.8% in 2014 to 16.9% in 2015. Superfast broadband, above 100Mbps, was used by 5.9% of businesses in 2015.

The size of a business has a large effect on the likely internet connection speed it will subscribe to. The most common connection speed for the smallest businesses was between 2Mbps and 10Mbps at 22.8%. In contrast, the largest (1,000 or more employees) businesses were most likely to subscribe to superfast broadband, with 56.3% connecting at speeds above 100Mbps.

Figure 8: Proportion of UK businesses by maximum contracted internet connection speed, 2014 and 2015

Source: Office for National Statistics

Download this chart Figure 8: Proportion of UK businesses by maximum contracted internet connection speed, 2014 and 2015

Image .csv .xls7. Cloud computing

Cloud computing, or internet storage space, is the use of remote servers hosted on the internet to store, manage and process data. The use of cloud computing has become more common in recent years as an alternative to storing data on local servers or personal computers.

In 2015, 20.6% of all businesses purchased a cloud computing service, including email, database hosting and file storage. Larger businesses were more likely to purchase cloud computing services than smaller ones. Cloud computing services were purchased by 71.0% of businesses with 1,000 or more employees, while only 19.0% of businesses with 0 to 9 employees did so. The most purchased service was storage of files, with 15.0% of businesses reporting this. The lowest purchase of a cloud computing service was for computing capacity to run own software, with only 3.7% of businesses reporting this purchase.

The information and communication sector purchased the largest amount of cloud computing services across all types of services surveyed, while the accommodation and food services sector purchased the least.

Back to table of contents8. Big data

Big data are extremely large data sets that may be analysed to reveal patterns, trends, and associations. Analysing big data allows users to make better and faster decisions using data that were previously inaccessible or unusable.

Big data analysis was mostly used by the larger companies (1,000 or more employees). The larger the business employment sizeband the greater the use of big data.

Data generated from social media was the most popular type of big data analysis used by all business sizebands with 30.8% of larger companies (1,000 or more employees) and 3.8% of the micro-enterprises using this type of analysis.

Business’s own data from smart devices or sensors was used in big data analysis by 24.8% of larger companies (1,000 or more employees), 13.1% of businesses with 250 to 999 employees and 6.6% of businesses with 50 to 249 employees. The smaller businesses did not use this type of analysis as much as the other sources of big data collection with only 0.7% of micro-enterprises and 2.3% of businesses with 10 to 49 employees having used these methods.

Geolocation data from the use of portable devices using mobile telephone networks, wireless connections or GPS was used by 23.0% of larger companies.

Back to table of contents9. Your views matter

We are constantly aiming to improve this release and its associated commentary. We would welcome any feedback you might have and would be particularly interested in knowing how you make use of the data to inform your work. Please contact us via email: esociety@ons.gov.uk or telephone Cecil Prescott on +44 (0)1633 456767.

Back to table of contents10. Main issues specific to this bulletin

This is our latest annual release about e-commerce and the adoption and use of information and communication technologies (ICTs) by UK businesses. The results in this release are for 2015. The source of the information is the E-commerce and ICT Survey of UK businesses.

The Inter-Departmental Business Register (IDBR) was used as the sampling frame for the survey. The survey was sent to 10,995 of all UK businesses in the Manufacturing, Production, Construction, Distribution and Service sectors.

This statistical bulletin reports e-commerce activity by UK businesses, regardless of where the respondent’s customer or supplier is located, or whether the trading activity is with households or businesses.

The Annual Business Survey (ABS), produced by us, is an important input for estimating the level of e-commerce in the UK. All sectors covered by the E-commerce survey are also covered by the ABS.

On 10 November 2016, we published provisional results from the 2015 ABS. The release covered:

- non-financial services

- distribution

- production

- construction

- parts of agriculture

Together these industries represent the UK Non-Financial Business Economy and account for around two-thirds of the whole economy of the UK in terms of gross value added.

In recent years there has been user interest in resuming coverage of businesses with less than 10 employees in the E-commerce and ICT Survey of UK businesses. Therefore the coverage of this survey was extended in 2014 to include these businesses.

Estimates in the data tables have been prepared using 2 bases:

- businesses with 10 or more employees to enable comparison with previous years

- all businesses including results for businesses with 0 to 9 employees, that are only available for 2014 and 2015

Common pitfalls in interpreting the series

This report should not be confused with the Internet Access Household and Individuals statistical bulletin. This is a separate release that contains estimates on internet access and use of the internet by households and individuals, not by businesses.

International comparisons

A comparable survey is run in all countries of the European Union (EU) and also in some non-EU countries. Eurostat plays an important role in this and each year leads a process whereby the data requirements for the survey are reviewed and updated. Comparative data for EU countries can be found on the Eurostat website.

Back to table of contents11. Quality and methodology

The E-commerce and ICT Activity of UK Businesses Quality and Methodology Information document contains important information on:

- the strengths and limitations of the data and how it compares with related data

- users and uses of the data

- how the output was created

- the quality of the output including the accuracy of the data

Classification changes

The 2015 survey was based on the Standard Industrial Classification (SIC) 2007. The estimates published for 2009 were the first to be published based on SIC 2007, which replaced the SIC 2003 classification system. Results for the 2008 survey were originally compiled and published based on SIC 2003, and have been re-estimated based on the new SIC 2007, to enable comparisons to be made with future years.

There were changes to the e-commerce questions asked in the 2008 survey, which impacted on the published results. The internet/non-internet split of e-commerce transactions that had been included since the survey began were discontinued after the 2008 survey. This split was replaced with a breakdown of website and non-website transactions. The historical e-commerce estimates, broken down by internet and non-internet sales, are still available on our website in the 2008 E-commerce and ICT Statistical Bulletin. As a result of the changes to the measurement of e-commerce, this release provides estimates of the values of e-commerce from 2008 onwards.

Until the 2007 survey, the definition of e-commerce sales and purchases included transactions over manually typed email. From the 2008 survey onwards this changed and email transactions have been excluded. This means that e-commerce sales published in this release are not directly comparable with estimates published for 2007 and previous years.

Quality improvement to the estimation of e-commerce sales values

A quality improvement to the estimates of the values of e-commerce sales was made for the 2011 release that was published in November 2012. Prior to the 2011 survey, estimates of the values of e-commerce sales had been calculated using ABS total business turnover data from the previous year. This method had been used since the e-commerce survey commenced in 2000. Since the 2011 survey it has been possible to use ABS data from the relevant survey year to derive estimates of e-commerce sales, which resulted in more accurate estimates. The information note on quality improvements to the e-commerce survey, published on our website has further details.

Users of the data

This bulletin provides information on the estimates of e-commerce sales, and the use by businesses of various types of information and communication technologies (ICT). In some cases, growth over time can be seen where ICT use has been measured on a comparable basis in previous years. Examples of this include the measurement of ICT activities such as internet access, broadband and websites. Results are presented by business employee sizeband. This allows comparisons of the levels of e-commerce trading and ICT activity to be made between different sized businesses.

Eurostat is the principal user of the statistics. The UK provides statistics to Eurostat which measure business use of ICT and e-commerce activity, in accordance with Regulation of the European Parliament and Council 808/2004. These estimates are used to provide information that is consistent with other European Union (EU) member states, as part of progress towards measuring EU benchmarking indicators. These EU indicators compare the development and use of ICT in the EU member states, and help to provide a better understanding of the adoption of ICT and the internet by businesses at an EU level.

ICT is considered as critical for improving the competitiveness of European industry and more generally, to meet the demands of society and the economy. Broadband is considered to be important when measuring access to, and use of, the internet. Broadband offers users the possibility to rapidly transfer large volumes of data and keep access lines open. The take-up of broadband is a key ICT policy-making indicator. Widespread access to the internet, via broadband, is regarded as essential for the development of advanced services on the internet, such as e-business, e-government or e-learning.

Do you make use of our estimates of e-commerce and ICT activity? If yes, we would like to hear from you (ecommerce@ons.gov.uk) and understand how you make use of these statistics. This may enable us, in the future, to better meet your needs as a user.

International context

A comparable survey is run in all EU countries and also in some non-EU countries. The measurement of e-commerce and ICT activity by businesses is under continuing review and development. Eurostat plays a leading role in this and each year leads a process whereby the data requirements for the survey are reviewed and updated. Comparative data for EU countries can be found on the Eurostat website. Approximately 40% of the survey questions change each year to enable the survey to cover new and developing aspects of ICT use. This means that the available time series for ICT adoption and use varies and not all time series are updated each year.

Estimation

The estimates of the proportions of businesses use number raised estimation. Results weighted by number of businesses give an equal weight to businesses irrespective of size. This method reflects the greater number of small businesses than large ones. Therefore, estimates of proportions of businesses in “all sizebands” are likely to be closer to the estimates for the 0 to 9 employment sizeband, than for the 1,000 or more employment sizeband. Estimates of the monetary values of e-commerce use the employment of the business with the estimated percentage of total turnover derived from e-commerce. This means that businesses with larger employment have a greater weight in the estimation of the monetary values of e-commerce. Full details of the estimation methods used are available in the E-commerce and ICT Quality and Methodology Information report.

Coverage

The provision of the results to Eurostat is a requirement set out in EU Regulation 808/2004. The survey collects the data necessary to meet this requirement. The estimates in this release relate to those sectors of the economy where coverage is required by Eurostat under the terms of the Regulation. It should therefore be noted that the survey is not intended to provide full coverage of all UK ICT and e-commerce business activity.

The survey covers businesses within the following economic sectors, according to the Standard Industrial Classification (SIC) 2007.

Manufacturing: Divisions 10-33

Utilities: Divisions 35-39

Construction: Divisions 41-43

Wholesale: Divisions 45-46

Retail: Division 47

Transport and storage: Divisions 49-53

Accommodation and food services: Divisions 55-56

Information and communication: Divisions 58-63

Other services: Divisions 68-74, 77-82, 95.1

The sectors of the SIC 2007 not covered by the survey are as follows:

Section A - Agriculture, forestry and fishing

Section B - Mining and quarrying

Section K - Finance and insurance activities

Division 75 - Veterinary activities

Section O - Public administration and defence, social security

Section P - Education

Section Q - Health and social work

Section R - Arts, entertainment and recreation

Section S - Other service activities except SIC 95.1, repair of computers

Until the 2004 survey, businesses with less than 10 employees were included in the survey, due to a specific user interest from the then Department of Trade and Industry (DTI). When this user interest ended the coverage of these businesses was discontinued, leaving the coverage from 2005 onwards as being just what was required by Eurostat under EU Regulation 808/2004. In recent years there has been user interest in resuming coverage of the businesses with less than 10 employees therefore coverage resumed for the 2014 survey.

Revisions to earlier years

As in previous years, estimates are subject to revision. The usual revisions policy for this release is that estimates in the previous 2 years are subject to revision.

Sampling variability and confidence intervals

The estimates in this release are subject to sampling variability, as are those from all sample surveys. The confidence interval tables contained 95% confidence intervals for selected estimates relating to e-commerce and ICT activity.

All of the published estimates come from survey data and so have a degree of statistical error associated with them. Confidence intervals are an indication of the reliability of the estimate: the smaller the interval, the more reliable the estimate is likely to be. With regards to “95% confidence intervals”, we mean that if we repeated our survey 100 times, 95% of the time (95 times out of 100), the true population value would fall within the range of these confidence intervals.

Imputation

No imputations were made for contributor or item non-response, as all data items on a business’ completed questionnaire have to pass validation checks before being included in the survey results. The only exceptions to this are where, under certain conditions, a missing value data item was estimated based on other contributors in the same employment size band and SIC. For this to take place, the business had to have returned all non-value data items and all these items had to have passed the validation checks.

Back to table of contents