Table of contents

- Main points

- Things you need to know about this release

- Largest increase in aGVA comes from the Americas

- Growth in the production and agriculture industry

- Foreign-owned businesses were more likely to be large (with employment of 250 and over) compared with UK-owned businesses

- Links to related statistics

- Quality and methodology

1. Main points

In 2015, there were just over 2 million registered businesses in the UK non-financial business economy; of these, 1.1% (24,145) were owned by businesses outside of the UK, that is, were foreign-owned.

Despite this small proportion (1.1%) of businesses being foreign-owned, they contributed £333.7 billion in approximate gross value added (aGVA) to the UK non-financial business economy in 2015; this was a contribution of 28.6% to total aGVA in the UK.

Of these foreign-owned businesses, the majority were owned in Europe with over 13,000 businesses; the largest proportion were within the wholesale and retail trade industry, which accounted for nearly a third of all European-owned businesses.

Just over 7,500 businesses were owned within the Americas; these businesses provided the largest contribution to the increase in aGVA generated by foreign-owned businesses and again the largest proportion of these businesses were in the wholesale and retail trade industry.

In 2015, aGVA for foreign-owned businesses increased by 6.3% compared with 2014; in comparison, aGVA for UK-owned businesses increased by 6.8% over the year.

2. Things you need to know about this release

The estimates contained in this release are taken from the Annual Business Survey (ABS). The data show how many businesses are UK or foreign-owned by industry and employment size. Information is provided for business counts, turnover and approximate gross value added at basic prices (aGVA).

The ABS covers only the UK non-financial business economy, which accounts for approximately two-thirds of the UK economy in terms of gross value added. The industries covered are:

- Agriculture (support activities SIC 01.6 only), forestry and fishing – Section A

- Production industries – Sections B to E

- Construction industries – Section F

- Distribution industries – Section G

- Service industries – Sections H, I, J, L, M, N, P (private provision only), Q (private provision only in SIC 86.1 and 86.9), R and S

For presentation purposes, this article does contain rounded data. Unrounded data is provided in the accompanying datasets.

Back to table of contents3. Largest increase in aGVA comes from the Americas

Despite only 1.1% of businesses in the UK being foreign-owned they contributed an approximate gross value added (aGVA) of 28.6% (£333.7 billion) to the UK non-financial business economy in 2015. The highest continental contributors to aGVA were Europe with 49.7% and the Americas with 36.7% of foreign-owned aGVA.

More than half (55.4%) of foreign-owned businesses in the UK were European-owned in 2015; compared with 2014 the number of European-owned businesses increased by a total of 557. Although the number of businesses owned by the Americas increased by only 91 between 2014 and 2015, these businesses contributed the most (£7.8 billion) to the increase in aGVA generated by all foreign-owned businesses; accounting for 39.1% of the increase in foreign-owned aGVA over the period.

Looking at individual countries, the United States of America had the largest share (22.3%) of foreign-owned businesses in the UK non-financial business economy, with 5,378 businesses. The USA also provided the highest contribution to aGVA at £100 billion.

Of the distribution of foreign-owned businesses, USA contributions of aGVA were over 3 times that of the second largest contributing country, Germany, which contributed an aGVA of £31.2 billion. This is proportional to the ratio of business counts between the countries, as the USA owns nearly 3 times more businesses in the UK than Germany. As a whole, European-owned businesses contributed £165.8 billion towards aGVA, which is a 3.6% increase compared with 2014.

Back to table of contents4. Growth in the production and agriculture industry

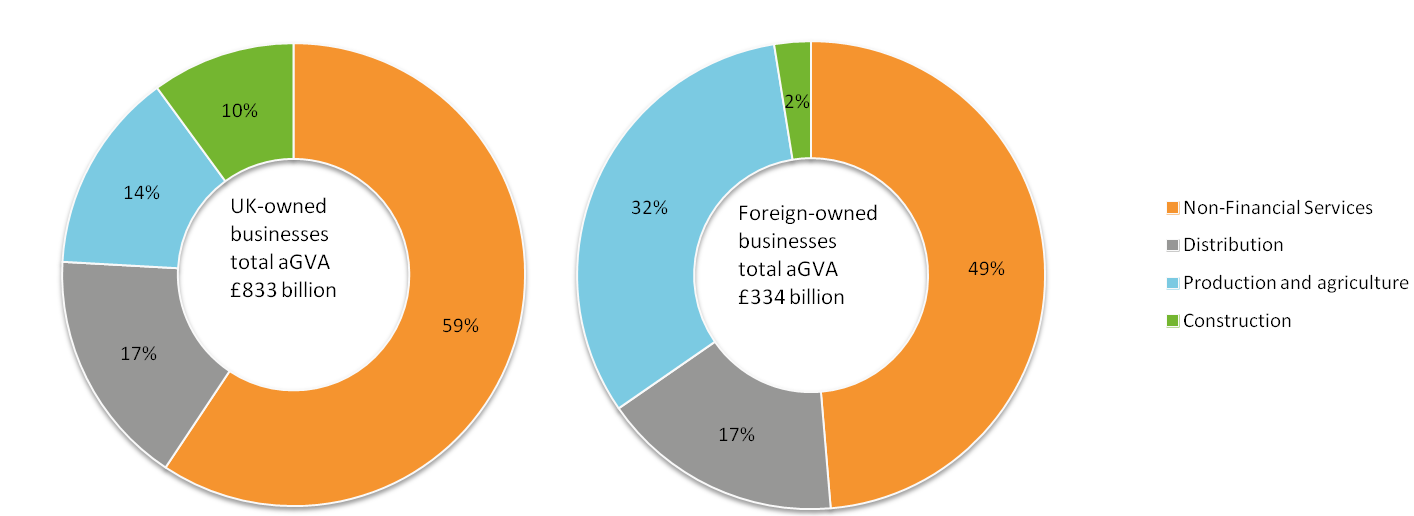

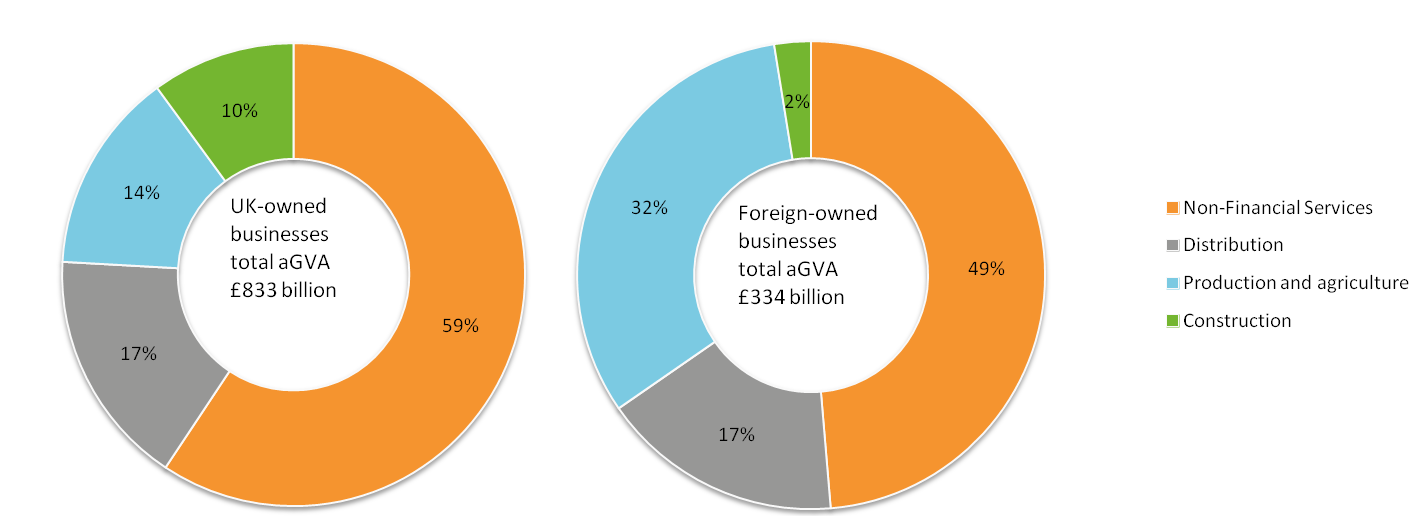

In 2015, foreign-owned businesses across the UK production and agriculture industry contributed near similar levels of approximate gross value added (aGVA) as their UK-owned competitors, despite representing only 2.8% of all registered businesses in this industry (4,384 businesses compared with over 152,000 UK-owned). In particular, this was largely due to the vast difference in value added by foreign-owned businesses in the mining and quarrying industries.

Figure 1 shows the proportions of aGVA generated by the industry groupings for both UK-owned and foreign-owned businesses.

Figure 1: Proportion of aGVA by industry grouping

2015

Source: Office for National Statistics

Download this image Figure 1: Proportion of aGVA by industry grouping

.png (87.9 kB) .xlsx (8.9 kB){kind=link}

Figure 2 shows that aGVA contributions from foreign-owned businesses in the mining and quarrying, and manufacturing industries, were responsible for narrowing the overall gap between UK and foreign-owned businesses across the production and agricultural industries.

Figure 2: Proportion of aGVA by industries of production and agriculture

2015

Source: Office for National Statistics

Download this chart Figure 2: Proportion of aGVA by industries of production and agriculture

Image .csv .xls5. Foreign-owned businesses were more likely to be large (with employment of 250 and over) compared with UK-owned businesses

Foreign-owned businesses were less likely to be attributed to micro-sized ones (employment of 10 or less) than UK-owned businesses. Looking at the distribution of UK-owned businesses, nearly 2 million (1,941,000 or 88.0% of the non-financial business economy) were classed as micro-sized businesses, however, they accounted for a quarter of UK-owned businesses approximate gross value added (aGVA); contributing nearly £206 billion in 2015. In contrast, 10,700 (or 44.2%) foreign-owned businesses were micro-sized businesses, yet, they accounted for only 3.5% of foreign-owned businesses aGVA.

While foreign-owned businesses were half as likely (than UK-owned businesses) to be micro-sized, a significantly larger proportion of foreign-owned businesses were categorised as large businesses (with employment of 250 and over). In 2015, of all foreign-owned businesses 9.5% were considered to be large businesses (with a contribution of 74.4% to foreign-owned businesses’ aGVA). This compared with only 0.3% of UK-owned businesses being categorised as large; these large UK-owned businesses contributed 38.6% to UK-owned businesses’ aGVA.

Figure 3 shows aGVA distribution rates across different employment bands. For UK-owned businesses it resembles roughly a uniform distribution, whereas for foreign-owned there is a distinct positive linear relationship between the two.

Figure 3: aGVA distribution rates across employment bands for UK and foreign-owned businesses

2015

Source: Office for National Statistics

Download this chart Figure 3: aGVA distribution rates across employment bands for UK and foreign-owned businesses

Image .csv .xls7. Quality and methodology

What has changed in this publication?

The last article about foreign-owned business, Business Ownership in the UK, 2013, was published in July 2015. This article, and the accompanying tables, represents a new, enhanced foreign-owned businesses article.

This release covers the ABS 2014 revised and 2015 provisional datasets. It is our intention to publish a complete backseries (2008 to 2015) in July 2017, with further updates in July each year.

For the July edition, which coincides with the Annual Business Survey (ABS): UK non-financial business economy regional results, we will also be publishing regional tables.

Please do not hesitate to contact us (via melanie.richards@ons.gov.uk) if you would like to make any suggestion of further enhancements to this article.

Links to our quality information

The Annual Business Survey QMI Quality and Methodology Information document contains important information on:

- the strengths and limitations of the data

- the quality of the output: including the accuracy of the data and how it compares with related data

- uses and users

- how the output was created