Table of contents

- Main points

- Introduction

- Number of property sales up 71% in March 2016

- Buy-to-let market drives peak in property sales

- Effects of historic stamp duty changes

- Sales of existing properties nearly double the 5-year average

- Sales of flats more than double the 5-year average in March 2016

- Effect of stamp duty changes in major towns and cities

- Links to related ONS statistics

1. Main points

The number of residential property sales increased by 71% between February and March 2016, ahead of stamp duty changes in April.

The number of sales of flats and maisonettes in March 2016 was more than double the average for March in the previous 5 years.

The number of property sales in April 2016 was 19.6% below the 5 year average for April.

The increased number of property sales in March 2016 was driven by an increase in the number of buy-to-let mortgage completions.

Back to table of contents2. Introduction

The Autumn Statement 2015 set out an additional 3% stamp duty land tax charge for purchases of second homes (including buy-to-let homes). This change was introduced on 1 April 2016. Since then, evidence of a rush to purchase buy-to-let properties ahead of the rise has emerged and data from the Council of Mortgage Lenders (CML) show the extent of the March rush and a subsequent April lull in the buy-to-let market.

This article explores the House Price Statistics for Small Areas (HPSSA) data on a monthly basis to provide insight into the scale of the increase in number of property sales during the months leading up to and immediately after the stamp duty change. Based on Land Registry Price Paid Data, the HPSSA data are produced quarterly, and so in order to examine the effects of the stamp duty change, a monthly extract of the HPSSA data is used in this article to provide a clearer picture of the impact of stamp duty change.

Whilst the standard HPSSA data are available at the small area level, the smallest geographic area on which analysis in this article is based is for major towns and cities in England and Wales. This is because the number of property sales for individual months is insufficient to provide robust analyses for smaller geographies.

The Land Registry data used to produce the HPSSAs are subject to some degree of registration lag, whereby some records of residential property transactions are registered some time after the month in which the transaction took place. This lag effect is stronger for more recent months, and so future releases of the Land Registry Price Paid Data are likely to contain a higher number of records of sales that took place in April and, to a lesser extent, a higher number of records for sales which took place in March, and so on.

However, now is the first time a sufficiently large number of transactions have been registered to provide an accurate indication of the number of property sales in April 2016. Therefore, the trends seen in the Price Paid Data are unlikely to change despite more transactions being registered in the future, so analysing a monthly extract of the data now is a useful exercise in understanding the impact of the stamp duty changes.

Back to table of contents3. Number of property sales up 71% in March 2016

Figure 1 shows that the number of residential property sales each month between January 2010 and April 2016 fluctuated within each year, with regular peaks and dips in the number of sales.

Figure 1: Number of residential property sales

England and Wales, January 2010 to April 2016

Source: Office for National Statistics, Land Registry

Download this chart Figure 1: Number of residential property sales

Image .csv .xlsSales of residential properties are to some extent seasonal, and so it is important to be aware of this when analysing monthly changes in housing market activity. To adjust for these seasonal variations, we can examine fluctuations in the number of property sales over recent months compared with the same months in previous years.

Figure 2 shows that, between May 2015 and February 2016, the trend in the number of property sales each month was broadly in line with the trend for the 5-year average, although the number of sales was generally higher than the historical average. A peak in the number of property sales in March 2016 marked a significant departure from the 5-year average for March. This was a 71% increase on the number of sales in February compared with a 17% increase in the 5-year average in the same period.

In April 2016, there was a large fall in the number of property sales, to the lowest level in the last 12 months and, unusually, below the 5-year average. In April 2016 the number of property sales was 10,936 lower (almost 20% lower) than the 5-year average for April.

Figure 2: Number of residential property sales for individual months and the historic 5-year average by month

England and Wales, May 2015 to April 2016

Source: Office for National Statistics, Land Registry

Download this chart Figure 2: Number of residential property sales for individual months and the historic 5-year average by month

Image .csv .xls4. Buy-to-let market drives peak in property sales

The Council of Mortgage Lenders (CML) publishes data on mortgage completions in the UK, which show that, in March 2016, the number of mortgage completions had the same peak and subsequent fall in the number of completions as seen in the HPSSA property sales data. These data don’t include the number of buy-to-let properties bought without a mortgage, but nevertheless indicate the general trends of the buy-to-let market.

Figure 3 shows that the March 2016 peak in mortgage completions was mainly driven by a large increase (181%) in the number of buy-to-let mortgages, from 10,400 in February to 29,200 in March. This increase meant that the number of buy-to-let mortgage completions exceeded the number of first time buyer mortgages for the first time since the CML started publishing data for buy-to-let mortgages in January 2013. Home-mover mortgages (mortgages to those who already have a mortgage) follow a similar but less volatile pattern, increasing by 60% from the February level of 25,900 to 41,500 in March. This is likely to be a secondary effect of the increases in buy-to-let mortgages.

Figure 3: Number of new mortgage completions for house purchases by mortgage type

UK, January 2013 to June 2016

Source: Council of Mortgage Lenders

Download this chart Figure 3: Number of new mortgage completions for house purchases by mortgage type

Image .csv .xlsWhilst the number of first time buyer mortgage completions increased in March, this was not by much more than the March increases in previous years and is arguably representative of the normal seasonal pattern for this type of mortgage. In April 2016, the number of mortgages for both buy-to-let and home-movers decreased sharply before beginning to recover in May. However, the recovery of the number of buy-to-let mortgage completions was somewhat subdued relative to other mortgage types. This may indicate a longer-term suppression in the buy-to-let property market.

Figure 4 shows that the proportion of different mortgage types out of all mortgage completions was relatively stable prior to 2016. In January and February 2016, the proportion of buy-to-let mortgages was slightly higher than in previous months, but an unprecedented increase occurred in March, where it rose to 30% of all mortgages, up from 18% in February.

Figure 4: Proportion of mortgage completions by mortgage type

UK, March 2015 to June 2016

Source: Council of Mortgage Lenders

Download this chart Figure 4: Proportion of mortgage completions by mortgage type

Image .csv .xlsIn the 3 months since March 2016, the proportion of mortgages that were buy-to-let was well below historic levels. This could be a reaction to the preceding spike in sales, or could be a new normal, following the stamp duty rises. Since March, while the proportion of home movers appears to be returning to normal, the proportion of buy-to-let mortgage completions remained low.

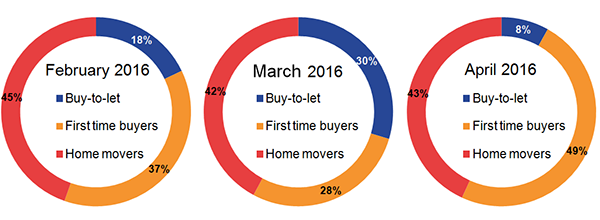

Figure 5 focuses on the 3-month period centred on March 2016. Whilst the proportion of buy-to-let mortgages increased between February and March, the proportion of mortgages to first-time buyers fell from 37% to 28%. In April however, the proportion of first-time buyer mortgages accounted for almost half of all mortgages, while buy-to-let mortgages accounted for around 8% of all mortgages, which is much lower than the historic level.

Figure 5: Proportion of mortgage completions by mortgage type

UK, February 2016 to April 2016

Source: Council of Mortgage Lenders

Download this image Figure 5: Proportion of mortgage completions by mortgage type

.png (61.9 kB) .xlsx (24.5 kB){kind=link}

5. Effects of historic stamp duty changes

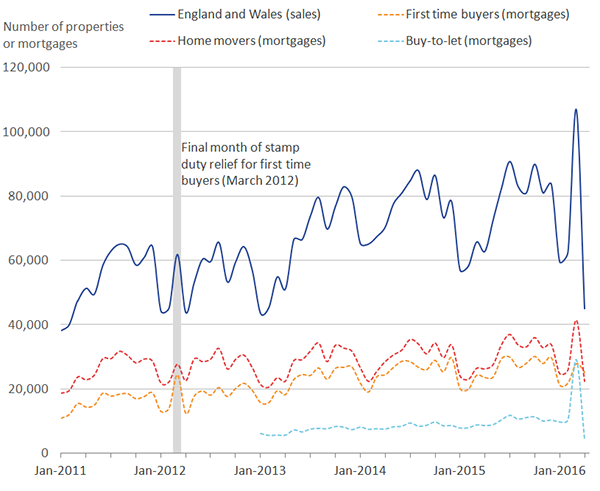

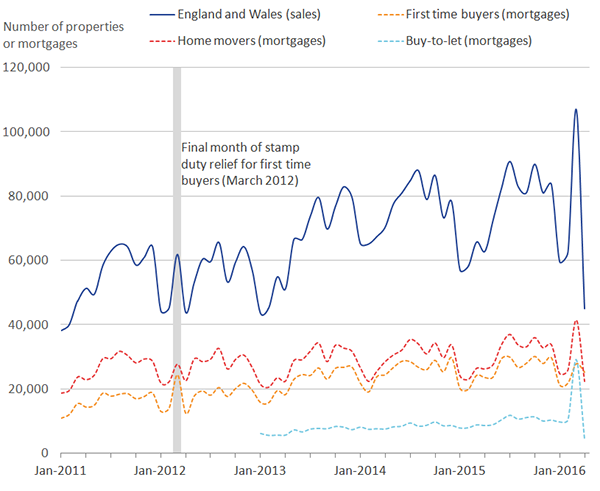

This isn’t the first time that changes to stamp duty have affected housing market activity. The 2-year stamp duty land tax relief for first-time buyers purchasing property for £250,000 or less ended in April 2012. The impact of these changes is visible in both the Council of Mortgage Lenders (CML) and House Price Statistics for Small Areas (HPSSA) data. Figure 6 shows a peak in both the number of property sales and the number of first-time buyer mortgages in March 2012 (the last month of the deal).

Figure 6: Number of property sales (England and Wales) and number of mortgage completions by type of borrower (UK)

January 2011 to April 2016

Source: Office for National Statistics, Land Registry, Council of Mortgage Lenders

Notes:

- Buy-to-let data is only available from January 2013

Download this image Figure 6: Number of property sales (England and Wales) and number of mortgage completions by type of borrower (UK)

.png (89.6 kB) .xlsx (104.5 kB){kind=link}

The largest peak in mortgage lending for March 2012 was to first-time buyers. However, in March 2016, buy-to-let mortgage completions had the largest peak – reflecting the target market of each of the stamp duty changes. In both cases home-movers’ mortgage completions also peaked, but to a lesser extent, which could simply reflect the larger number of first-time buyers (in 2012) and buy-to-let buyers (in 2016) who purchased property from home-movers.

Figure 7 shows the number of middle layer super output areas (MSOAs) within different price bands for 2014 and 2015. For 2014, the chart shows a large drop in the number of MSOAs in which the median price paid was a little over £250,000. This was most likely caused by the threshold for higher stamp duty land tax, payable on properties sold for £250,000 or more, making it less favourable to purchase property for more than £250,000. In December 2014, stamp duty rules changed so that properties sold for more than the £250,000 threshold were only subject to a higher stamp duty rate on the amount paid over £250,000, rather than on the entire purchase price as was previously the case. This new scheme made it more favourable to pay more than £250,000 for a property than in the previous stamp duty scheme and resulted in an increase in the number of properties sold for a little over £250,000 in 2015.

Figure 7: Number of MSOAs by median price paid band

England and Wales, 2014 and 2015

Source: Office for National Statistics, Land Registry

Notes:

- Each point relates to a range of property prices and is labelled with the upper price in its range

Download this chart Figure 7: Number of MSOAs by median price paid band

Image .csv .xls6. Sales of existing properties nearly double the 5-year average

The House Price Statistics for Small Areas (HPSSA) data provide information on the number of property sales for both existing properties and newly built properties. Transactions of newly built properties generally take longer to register than existing properties and so there is a registration lag for records of newly built properties. This lag affects more recent months’ data to a greater extent than older data and so sales of these properties are likely to be less complete than the data for existing properties.

Figure 8 shows that the number of sales of existing properties was greater than the 5-year monthly average throughout the last year (between 20 to 30% above average for much of the year). In March 2016, there were 102,034 sales of existing properties, up from 52,729 in February. The number of sales of existing properties in March was almost double the 5-year average, but was below the 5-year average in April.

For much of the last year, the number of sales of newly built properties was higher than the 5-year average. However, after December 2015, sales of new properties decreased and fell below the monthly 5-year average from February 2016.

Figure 8: Percentage difference between number of property sales in a single month and the 5-year average by property type

England and Wales, May 2015 to April 2016

Source: Office for National Statistics, Land Registry

Download this chart Figure 8: Percentage difference between number of property sales in a single month and the 5-year average by property type

Image .csv .xlsFigure 8 suggests that newly built properties were not part of the increased housing market activity in March 2016. One reason for this could be the fact that the stamp duty change was announced on 12 November 2015 for implementation on 1 April 2016. It is therefore unlikely that builders would have been able to increase the supply of housing quickly enough to accommodate a short-term rise in demand for buy-to-let properties. Another reason could be that those who purchase property with a buy-to-let mortgage are less likely to buy a newly built property than owner-occupiers. This is because newly built property is, on average, more expensive than the equivalent existing property, and so prospective landlords may generally prefer buying existing properties to maximise the yield on their investment.

However, under-reporting due to registration lag could partly explain the number of sales of newly built properties in these data for recent months. Therefore, it is possible that when more complete April 2016 data for newly built properties become available in the future, market activity for newly built properties will be slightly less subdued than it currently appears.

Figure 9 shows that there was an unusually high number of sales of newly built properties in March 2012, ahead of the end to the stamp duty relief for first-time buyers in April 2012. In April 2012, the number of sales of newly built properties fell below the level of April the previous year by 9.4%. This suggests that both housing developers and first-time buyers took advantage of the last month of the scheme, and so led to a temporary spike in activity within the new property market. This increased activity was most likely made possible by the fact that the duration of the scheme, and therefore its end date, was known a long time in advance and so allowed developers enough time to increase the supply of new housing.

Figure 9: Number of sales of newly built properties by month

England and Wales, 2010, 2011 and 2012

Source: Office for National Statistics, Land Registry

Download this chart Figure 9: Number of sales of newly built properties by month

Image .csv .xls7. Sales of flats more than double the 5-year average in March 2016

Figure 10 shows that, in March 2016, the number of sales of all property types increased but sales of flats and terraced properties increased the most. The number of sales of flats surpassed the number of sales of detached and semi-detached properties in March.

Figure 10: Number of property sales by type, England and Wales

England and Wales, May 2015 to April 2016

Source: Office for National Statistics, Land Registry

Download this chart Figure 10: Number of property sales by type, England and Wales

Image .csv .xlsFigure 11 shows the percentage difference between the numbers of sales in each month with the 5-year average for each property type. It shows that, in March 2016, the number of property sales was notably higher than average for all property types, but particularly so for flats and maisonettes.

In April 2016, the number of sales of all property types fell below the average for April, although sales of flats, having had the largest increase in March, had the largest decrease in April.

Figure 11: Percentage difference between number of property sales in a single month and the 5-year average by property type

England and Wales, May 2015 to April 2016

Source: Office for National Statistics, Land Registry

Download this chart Figure 11: Percentage difference between number of property sales in a single month and the 5-year average by property type

Image .csv .xls8. Effect of stamp duty changes in major towns and cities

The private rented sector tends to comprise a larger share of the dwelling stock in urban areas than in rural areas, and so the impact of stamp duty changes on housing market activity in major towns and cities in England and Wales is pertinent.

Generally, the number of property sales in all major towns and cities increased in March and fell in April 2016. This is perhaps to be expected given the national coverage of the stamp duty change. Prospective landlords across the country were faced with a choice of either purchasing a buy-to-let property before the end of March or delaying their purchasing but paying a 3% additional stamp duty charge on the full purchase price.

The monthly House Price Statistics for Small Areas (HPSSA) data explored here suggests the housing market responded differently to these changes depending on overall house prices in different towns and cities. Figures 12 and 13 compare the 5 towns and cities with the highest median price paid for property with the 5 towns and cities with the lowest price paid. They show that the towns and cities with the highest property prices tended to have a lower than average number of property sales in February and April, and a higher than average number of sales in March. Meanwhile, the number of sales in the 5 towns and cities with the lowest property prices was close to the historic average in April. Although by no means a definitive geographical pattern, it does suggest that the more expensive towns and cities have had a larger fall in housing market activity than in less expensive areas. This may be the result of the higher impact of additional stamp duty charges on more expensive properties.

Figure 12: Percentage difference between the number of property sales in individual months and the 5-year average for the 5 towns and cities with the highest median price paid

England and Wales, February 2016 to April 2016

Source: Office for National Statistics, Land Registry

Download this chart Figure 12: Percentage difference between the number of property sales in individual months and the 5-year average for the 5 towns and cities with the highest median price paid

Image .csv .xls

Figure 13: Percentage difference between the number of property sales in individual months and the 5-year average for the 5 towns and cities with the lowest median price paid

England and Wales, February 2016 to April 2016

Source: Office for National Statistics, Land Registry

Download this chart Figure 13: Percentage difference between the number of property sales in individual months and the 5-year average for the 5 towns and cities with the lowest median price paid

Image .csv .xlsThe HPSSA data shows how both recent and historic changes in stamp duty land tax can have short-term affects on the number of residential property sales. The availability of more property sales data in the future will provide additional insight into whether or not the most recent stamp duty changes will result in a protracted period of historically low activity in the buy-to-let housing market.

Back to table of contents