Table of contents

- Main points

- Background

- The use of financial accounts

- Explaining the financial accounts framework

- The flow of funds framework

- How financial accounts and flow of funds data help policymakers and economists

- Data challenges

- Conclusions

- Authors

- References

- Appendix 1: Data source articles for the enhanced financial accounts

1. Main points

The global financial crisis in 2008 highlighted how the integrated nature of modern financial systems can transmit financial shocks through domestic and global economies, impacting the real economy – and reinforcing the importance of compiling comprehensive financial information.

The first experimental estimates of the UK Financial Accounts incorporate new experimental commercial and regulatory data sources and, where possible, replaced or improved existing ones – these contain over 10 new data sources, which improve the sector/instrument relationships within the financial matrices.

New experimental data suggest increased annual balance sheet estimates for assets and liabilities of the investment and other financial institutions sectors (S.123 to S.127) by approximately £3 trillion.

While significant progress has been made, further work is required to increase the granularity and improve the quality and coverage of counterparties relationships ahead of the planned implementation of the flow of funds in the UK National Accounts in 2021 and beyond; over the coming years, we will seek to implement these new sources into the UK National Accounts, following further and appropriate quality assurance.

2. Background

"We all recognise that finance is the lifeblood of commerce. At its best, it waters the seeds of innovation and facilitates the churning that every healthy ecosystem needs. At its worst, it becomes a deluge that sweeps away all that stands in its path."

These views from the then IMF Managing Director crystallises both the vital role of finance in, and the dangers it can pose to, the economic system. And yet in the UK, compiling comprehensive estimates on the financial activities of an economy have traditionally been given a lower profile than those on the real economy.

The global financial crisis in 2008 highlighted how the integrated nature of modern financial systems can transmit financial shocks through domestic and global economies, impacting the real economy. So, attitudes have changed at the domestic and international level as to the importance of compiling comprehensive financial information so policymakers can assess potential financial risks, including where vulnerabilities may be building.

The financial accounts provide a way to understand these prospective financial risks. Their ability to provide policy insights is particularly relevant for the UK, whose financial system has increased markedly over the last few decades (Figure 1) and whose size is large by international standards.

Burrows and others (2015) (PDF, 1.42MB) explain how understanding the structure and nature of the financial system and its links to borrowers and savers in the real economy is important in considering a wide range of policy questions. In particular, it highlights how this requires information on the "balance sheets of the various sectors that together make up the financial system, as well as the connections between those sectors".

Figure 1: Size of the UK financial system

Total financial assets of financial corporations as a per cent of gross domestic product, including financial derivatives

Source: Office for National Statistics

Notes:

- The latest figures from the Organisation for Economic Co-operation and Development show that the size of total financial assets held by UK financial corporations was 1,056% of nominal GDP in 2017. This was the largest amongst the G7 countries – this was followed by Japan (739%), France (649%), Canada (648%), the United States (509%), Germany (461%) and Italy (396%).

Download this chart Figure 1: Size of the UK financial system

Image .csv .xlsIn response, we are undertaking a multi-year project to enhance the UK's Financial Accounts in cooperation with the Bank of England, placing a higher priority on these financial data as part of the transformation of the UK National Accounts.

The first combined results from this work were published in November 2019, but this is only the first step. More ambitiously, work is underway towards implementing a new conceptual framework -- the "flow of funds" -- that would provide full counterparty breakdown of all financial transactions (ONS, 2015). Progress has been made in exploring potential of commercial and regulatory administrative data, ahead of the planned implementation of the flow of funds in 2021 and beyond.

The structure of this article is as follows:

explain the use of the UK Financial Accounts in monitoring financial flows

provide an overview of the structure of the financial accounts and flow of funds

illustrate how this framework can help policymakers and economists enhance their understanding of the financial system in the UK

progress so far in producing counterpart information by financial transaction and how we will look to incorporate this into the UK National Accounts

3. The use of financial accounts

The importance of finance for the real economy has long been recognised. UK policymakers have traditionally focused on analysing financial conditions through a range of indicators such as money supply and bank lending, market interest rates, and exchange rates. While earlier crises led to an increased focus on financial stability, it was the global financial crisis that caused policymakers to re-assess its regulation and analysis, with implications for official statistics.

A fuller understanding of the build-up of systemic risk would have helped provide further economic insights pre- and post-crisis¹. Lai and others (2017) explain how such financial information can potentially give early warning signs of a rise in financial instability, particularly in the context of viewing the interconnectedness of these financial transactions at a global level. These insights include the "rapid balance sheet expansion of the banking sector, its increased interconnectedness with the shadow banking sector and the rest of the world, and the shift in banking business model towards a more vulnerable structure involving trading more derivatives against the rest of the world".

Whilst there is a wide range of financial information that is needed to monitor financial stability, a full set of financial accounts complemented by counterparty information provides a consistent, comparable, and holistic view of financial activity of an economy. Consequently, these data are crucial for conducting financial stability analysis, for informing monetary policy, and promoting transparency on the financial economy to analysts, investors, and the public more broadly.

In the UK, the need for improved financial accounts was recognised in the National Statistics Quality Review: National Accounts and Balance of Payments (2014). It highlighted that the experience of the financial crisis had led to:

"increased demand from regulators and supervisors for information on financial flows and the whereabouts of assets and liabilities across all sectors"

specifically the need for:

"expanded articulation of the sectors within the financial sector of the economy and most particularly asking for information on which sectors hold the assets/liabilities of which other sectors of the economy".

This was also a core theme in the Independent Review of UK Economic Statistics (2016) (PDF, 5.13MB), also known as the Bean Review, which noted that "the access to a detailed breakdown of the institutional sectors with fine detail on assets and liabilities by specific financial instruments, is essential for the effective evaluation of the risks to financial stability."

This need is also recognised internationally. Recent analysis by the International Monetary Fund explains the framework that underpins its assessment of global financial stability, specifically the role of macro-financial linkages. The role of the financial accounts is integral to the ability of policymakers to track the level of, and change in, financial vulnerabilities, including borrower leverage and maturity mismatches of financial intermediaries, as well as currency exposures. Various international initiatives and reports have reinforced the importance of financial accounts data².

Consequently, these are considered a priority under the G20 Data Gaps Initiatives (DGI), the internationally coordinated data project led by the International Monetary Fund (IMF) and Financial Stability Board (FSB) that arose from the global financial crisis, and one of the datasets that countries need to compile under the IMF's Special Data Dissemination Standard (SDDS) Plus³. Not only are such data important for domestic policymakers but given potential financial spill-overs from advanced economies such as the UK to the rest of the world, important for international financial stability.

Notes for: The use of financial accounts

- The reaction of the UK authorities, other major economies, and the international financial institutions to the GFC has been to (1) implement a financial sector reform programme, (2) a closer monitoring of the financial system -- covering institutions and markets -- through enhanced financial stability analysis, and (3) strengthen data sources to better monitor financial risks and interconnections.

- See in particular, The Financial Crisis and Information Gaps Data Gaps, FSB and IMF, 2015; Understanding Financial Accounts, OECD, 2017; and An Integrated Framework for Financial Flows and Positions on a From-Whom-to-Whom Basis, Shrestha and Mink, 2011,

- The SDDS Plus is the most advanced international data dissemination framework designed to support domestic and international financial stability. The UK is not yet an adherent to the SDDS Plus.

4. Explaining the financial accounts framework

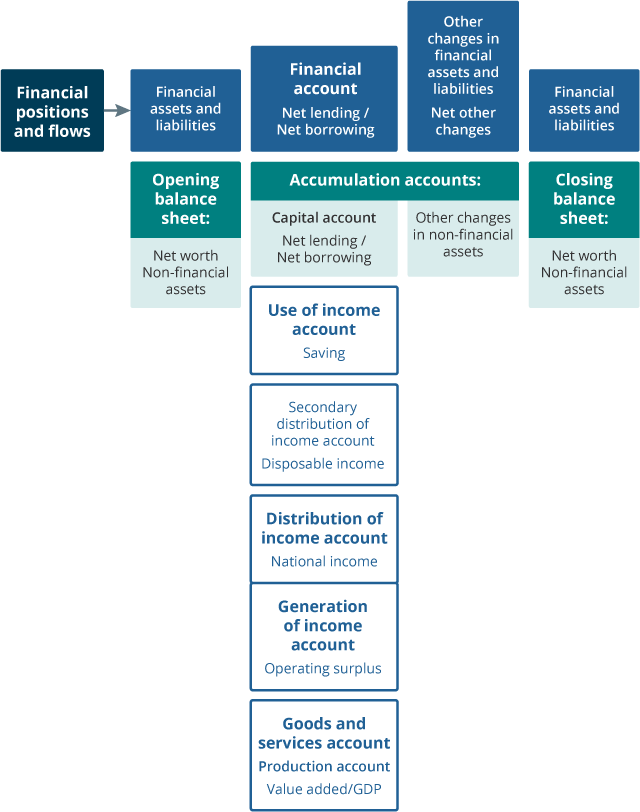

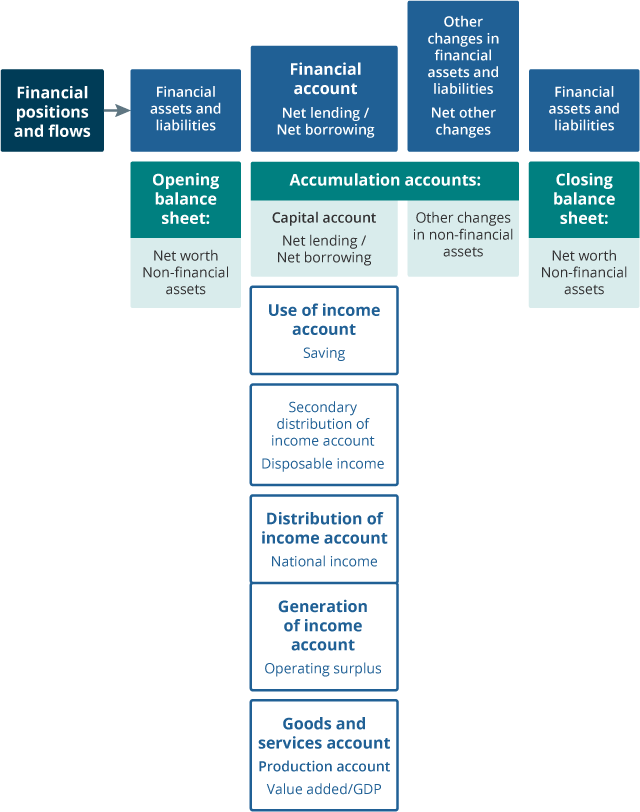

The financial accounts play an important role in monitoring the dynamics of the real and financial economy, capturing the financial transactions within an economy. It comprises a system of transactions, other flows, and stocks that form an integrated picture of financial activity within an economy and with the rest of the world. To appreciate the types of analysis that can be undertaken, it is necessary to understand the framework and its core elements¹.

Framework

Transactions

Financial transactions in a reference period capture the change of ownership in financial assets. It shows how net borrowing is funded or net lending is invested by recording changes in the net acquisition of financial assets and net incurrence of financial liabilities. Transactions are recorded for asset and liabilities on a gross basis, allowing for the full scale of financial activity to be captured. There may sometime be analytical interest in presenting these as net figures, which net out intra-sectoral transactions and positions, such as for general government.

Balance sheets

These record the value of financial assets and liabilities held at the start and end of a reference period. Start- and end-period stock levels are linked by a flow-stock relationship involving transactions, revaluation effects (for example, fluctuations in exchange rates or equity markets) and other flows (such as debt write-offs). The stocks data within the financial accounts framework are known as “sectoral balance sheets”.

Other flows

Whilst the need to analyse transactions and stocks is typically well-established, the analytical importance of other flows is less obvious but important for financial stability analysis and the potential impact on economic activity. For instance, increases or decreases in asset values may affect investment and consumption decisions; and sharp movements in the exchange rate can boost or depress activity depending on the currency structure of resident’s stock of assets and liabilities.

Figure 2 shows that the financial accounts is part of a wider national accounts framework that integrates both the real and financial economies in a comprehensive manner. This is an important benefit as the real economy impacts on financial activity, and the other way around. Activity in the real economy, including current and capital investment activity, impacts net borrowing and lending that is financed in the financial account; while, for example, a slowdown in real economy consumption and investment might be the consequence of a restriction in available finance.

Figure 2: The national accounts framework, financial flows and positions

Source: Bank for International Settlements

Download this image Figure 2: The national accounts framework, financial flows and positions

.png (49.9 kB){kind=link}

Core elements

The main elements to the financial accounts are institutional sectors, financial instruments, and maturity.

Institutional sectors

These combine institutional units with broadly similar characteristics and behaviour:

- households

- non-profit institutions serving households (NPISH)

- non-financial corporations

- financial corporations

- general government

- rest of the world (RoW).

This level of granularity is needed to capture the different functions and objectives – for example, the nature of government is to produce non-market output for individual and collective consumption (such as health, education and defence), whilst households typically consume goods and services. Similarly, an insurance company has different economic objectives than a deposit-taker such as a bank. Given the complexity of the UK economy, over time, we are aiming to publish counterparty estimates for the full range of institutional sectors shown.

Financial instruments

Debt and equity instruments are the two main types of financial instruments. Debt instruments involve a requirement to repay the amount owed, with loans, deposits, debt securities, and trade credit the most common forms. As such, even if the borrowers’ financial situation worsens, the debt remains. In contrast, equity represents a claim on the residual value of an entity, so if the entity issuing the equity fails, and so the equity becomes worthless, the owner of the equity has no claim.

As corporations fund their activities with a combination of debt and equity, financial accounts data can be used to monitor the extent of gearing (debt-to-equity), so-called “leverage”, on the liability side of corporations’ balance sheets and how it is evolving over time. High levels of gearing open the risk that corporations, particularly financial corporations, may not have sufficient equity cushion in the event of adverse financial conditions that undermine the value of their assets. Strengthening the capital cushion of deposit-takers has been one of the main regulatory responses to the global financial crisis.

An important characteristic of financial instruments is that one party has a claim and another a liability. As a consequence, if the value of a financial instrument changes, one party loses value, the other gains value, so value stays within the financial accounts system allowing analysts to monitor which economic sectors gain and which lose from financial events.

Maturity

Maturity of instruments is shown on a short-term and long-term basis, with one year the cut-off. This is captured on an “original” maturity basis – that is, the maturity at inception, rather than in real time. So, a debt security issued with a five-year maturity is always classified as long-term even if it has less than one year to maturity. This gives an indication of whether borrowers are borrowing short- or long-term, which itself has potential implications for financial stability.

For example, it would capture whether increased short-term borrowing raises the risk of not being able to refinance when the debt falls due. To monitor this roll-over risk more effectively, information on the “remaining” maturity is also needed – that is, the time to when payments are due . More broadly, maturity mismatches between assets and liabilities potentially creates liquidity risk. The global financial crisis highlighted the importance of monitoring this risk as it can lead to financial stress if market liquidity dries up.

Notes for Explaining the financial accounts framework

- The framework is set out in the System of National Accounts, 2008 (2008 SNA), the European System of Accounts (ESA 2010), and the Monetary and Financial Statistics Manual and Compilation Guide.

5. The flow of funds framework

As highlighted in the Bean Review, the UK has historically only provided “an incomplete picture of bilateral financial relationships between sectors, with an incomplete breakdown of bilateral from-whom-to-whom transactions and only limited detail in different subsectors within the financial sector”. In line with international best practice, we are developing from-whom-to-whom statistics for financial account transactions and balance sheet levels (ONS, 2015). It would provide for the first time an improved counterparty breakdown of the financial assets and liabilities by each sector.

For example, it would identify household borrowing through loans from deposit-takers. The purpose of the Flow of Funds is to understand who is borrowing or investing from whom and in what type of instrument.

Embed code

At the international level, work is being undertaken to extend the from-whom to-whom matrix further to get a better understanding of cross-country financial inter-relationships not least to monitor potential financial sector spill-over implications. The concept of the "global flow-of-funds (PDF, 274KB) " requires national data as well as data from internationally coordinated Bank for International Settlements (BIS) and International Monetary Fund (IMF) data collections.

Back to table of contents6. How financial accounts and flow of funds data help policymakers and economists

The financial accounts and flow of funds provide a rich source of information that have multiple analytical uses including studying how financial imbalances are evolving, the level and composition of public and private debt, and the role of financial intermediaries in an economy (European Central Bank, 2009 (PDF, 1.46MB) ).

Sectoral imbalances

Recent analysis has highlighted the role of the business and financial cycle (PDF, 943KB), specifically how "business cycles can be first amplified and then imperilled by growing imbalances in the real economy" and how "imbalances at the heart of the financial cycle have been the best predictors of downturns in recent decades." The net lending or borrowing balances of households, corporations, government and the rest of the world can provide insights into the sustainability of investment and consumption patterns.

Figure 4 shows the large movements in UK sectoral balances following the financial crisis. Reflecting the low level of national saving in the UK economy today, the UK is having to borrow or run down its savings to finance its consumption and investment. The rest of the world is a net lender to the UK at levels that are high by historical and international standards.

Recent analysis looks at the extent to which the UK's fiscal and current account deficits are closely related. It explains that these could potentially pose a risk to financial stability, if there was a shock to investor confidence that may "find the government struggling to fund its deficit due to reduced domestic appetite and little scope to find alternative funding abroad" or if it led to "the likelihood of default to increase could lead foreign investors to withdraw from the UK, making it harder for the government to fund the deficit through both domestic and foreign channels". It found that these potential amplification mechanisms are not currently a problem for the UK.

Figure 4: The UK is reliant on the rest of the world being a net lender

Source: Office for National Statistics

Notes:

- Households include non-profit institutions serving households; corporations comprise of financial and non-financial corporations; government comprise of central and local government.

- Households, corporations and government comprise the UK domestic economy.

Download this chart Figure 4: The UK is reliant on the rest of the world being a net lender

Image .csv .xlsSystemic vulnerabilities

Systemic vulnerabilities can arise from risks embedded in sectoral balance sheets that build up over time. As noted by the International Monetary Fund (PDF, 1.1MB), "balance sheet analysis captures the role of financial frictions and mismatches in creating fragility, amplifying shocks, and generating spillovers within and across economies." After a financial crisis, "the process of recovery entails a process of deleveraging, as the private sector restructures its balance sheets by increasing savings, curtailing spending, and paying back debt".

Household debt has been a topic of interest as a potential source of financial system vulnerability. The level of household debt-to-income is high by historical standards, whilst its distribution is also of importance in monitoring risks to the UK financial system and economy. The latest Financial Stability Report (PDF, 7.53MB) explains that the most indebted households tend to cut their consumption in response to adverse shocks -- and these effects may be amplified further if it leads to losses to lenders on all forms of lending, who in turn restrict the availability of credit.

Resilience of the financial sector

Prudential supervision and financial regulatory policy are central to ensuring the resilience of the financial sector. Through the flow of funds framework, the relationship among the financial sector, such as deposit-takers lending to non-bank financial institutions (NBFI), can be carefully monitored as a potential source of vulnerability to the real economy; for example, the possible negative implications for NBFIs of funding investments in securities through short-term borrowing from deposit-takers if market liquidity dries up and the securities can only be sold a loss, or not at all. Past experience informs that a shock to one part of the financial sector can be amplified by interconnections within the sector.

Information on the type of asset and liability instruments as well as maturity provides some insights on the markets in which financial institutions operate, including whether domestic or foreign, and how investment activity is changing over time. Furthermore, the financial accounts allows for the monitoring of relative shifts in financial intermediation over time, be it towards or from bank finance from/to intermediation through NBFI, towards or from security markets. These data can also help identify the impact on the financial system of regulatory changes, such as tightening capital requirements of deposit-takers.

Financial interconnectedness

This is a complex area of analysis in that financial connections between different sectors can be complicated by second or third round interlinkages. As capital flows have become increasingly international in nature, the scope of transmission channels to the real economy have increased.

Flow of funds matrices provide information on who is lending to whom, who owns whose debt, and who has a claim on whom, allowing analysis of potential contagion through inter-sectoral relationships.

Research by Statistics Canada shows that the movement of funds through the financial system can also be monitored (PDF, 468KB). Furthermore, with the use of data from internationally coordinated exercises such as the Bank for International Settlements's (BIS's) and the International Monetary Fund's (IMF's) Coordinated Portfolio Survey, it is feasible to analyse cross-border financial interconnections of the financial sector in more depth as these data sources provide information on financial links with counterpart countries¹.

Notes for How financial accounts and flow of funds data help policymakers and economists

- Under the G-20 DGI, a common data template for global systemically important banks, including those from the UK, has also been developed to better understand their financial inter-linkages given their importance to the global economy.

7. Data challenges

Whilst the analytical benefits of rich and comprehensive financial accounts are clear, there are practical challenges for national statistical institutes in compiling these data. This is particularly true for the UK with its large, complex and constantly evolving financial system.

The Organisation for Economic Co-operation and Development (2017) explains that "the compilation of the accounts is a time consuming exercise of data confrontation and reconciliation" and that "the absence of high frequency data for some of the sectors and poor timeliness of some of the data sources can make the compilation of quarterly financial accounts a very challenging endeavour".

Whilst the financial accounts can indicate where closer examination of trends and developments may be warranted, firm-level information may be needed to assess risks to financial stability. The flow of funds requires a detailed breakdown of the holding of assets and liabilities by specific financial instruments for each institutional sector, including counterparty information. This is also complicated as the financial system is constantly evolving and so it requires being able to monitor the interconnectedness in a more agile manner than traditional surveys may be capable of.

These challenges largely reflect the inherent data requirements of the flow of funds matrices, as there tends to be as much focus on monitoring financial stability at a more local level. Pockets of vulnerability are not always apparent at the macro level, but rather build up at the micro level.

Developing data sources for the flow of funds

To monitor the financial activities of the sectors of the economy, we have traditionally collected data from multiple sources to build up a macroeconomic picture at a point in time. These broadly consist of financial surveys¹, central and local government administrative sources² as well as information from the Bank of England, industry bodies, financial institutions and international organisations, such as the European Investment Bank and Bank for International Settlements.

Whilst this helps provides us with an overall position of financial transactions, analysis of financial stability requires a more detailed accounting of the flows of assets and liabilities. The Bean Review notes that "greater use of public and private administrative data has the potential to transform the provision of economic statistics in the long term" -- and this is particularly pertinent for the Flow of Funds.

We have engaged with a wide range of stakeholders, including those European countries that already publish flow of funds estimates and the European Central Bank, to understand better how this might be carried out in practice. In our work so far, commercial and regulatory information has been identified as potential avenues to replace or complement our existing survey information and help monitor new trends in the financial economy.

The first experimental estimates contain over 10 new data sources, which improve the sector and instrument relationships within the financial matrices. These initial findings show an increase in the annual balance sheet estimates of the investment and other financial institutions sectors by approximately £3 trillion, reflecting the exploitation of this information on financial transactions. More information can be found in Investment and Other Financial Institutions (DOC, 43KB).

Articles published today (26 November 2019) show how we have looked into the potential of the European Market Infrastructure Regulation (EMIR) dataset in compiling derivatives statistics in the Financial Accounts. This provides highly granular information about the derivative contracts held by UK entities, and has increasingly been used by central banks and authorities in Europe as a tool in financial stability policymaking. While this finds that the scope and coverage of contracts reported under EMIR is different from what is required for the financial accounts, further avenues have been explored where it might be possible to "combine the strengths of the different datasets for the future compilation of derivative statistics in the national accounts".

In November 2019, we published our most granular experimental information to date. These estimates incorporate such content and, where possible, have replaced or improved our existing sources. For example, we have provided additional granularity for financial corporations, where for the first time we are publishing estimates for money market funds, non-money market funds, other financial institutions except insurance corporations and pension funds, financial auxiliaries, and captive financial institutions and money lenders. At the instrument level, the new data primarily improve the existing data sources. Table 1 provides an overview of the updates that have been incorporated in these new flow of funds estimates.

| New Source | Institutional Sector | Instrument |

|---|---|---|

| New Monetary Financial Institutions Dataset (Bank of England) | Financial corporations (deposit taking corporations) | All instruments |

| Bank Holding Companies (Bank of England) | Captive financial institutions and money lenders | All instruments |

| New Bank of International Settlements estimates | Rest of World – specifically Banks | Deposits, short-term and long-term loans |

| Solvency II (Prudential Regulatory Authority) | Insurance corporations | All instruments |

| Financial Services Survey (ONS survey) | Other financial intermediaries, except insurance corporations and pension funds; Financial auxiliaries; Captive financial institutions and money lenders | All instruments |

| Thomson Reuters (Refinitiv), Crest, Equiniti (Commercial data as a service, survey) | All | Listed shares issued by UK companies |

| Equifax (Commercial data as a service) | Other financial intermediaries, except insurance corporations and pension funds; Financial auxiliaries, lending to households | Long term and short term loans |

Download this table Table 1: An overview of the new data sources in the flow of funds

.xls .csvWhile significant progress has been made, further work is needed to increase the sector and instrument granularity. There also needs to be more work to improve the quality and coverage of counterparties relationships before the flow of funds data are complete. Integration of these matrices into the UK National Accounts will begin in 2021.

Notes for Data challenges

We operate 21 financial surveys, which collects balance sheet information as well as income and expenditure estimates. These are run on a monthly, quarterly and annual basis and cover operating profits, financial assets and liabilities of the private non-financial corporations, insurance, pensions, unit trusts, investment trusts, consumer credit grantors, occupational pension schemes, financial register, financial services, and share ownership.

The majority of central government estimates are provided primarily from administrative sources including Her Majesty's Revenue and Customs and the Debt Management Office, while local government information is a combination of government accounts, the Ministry of Housing, Communities and Local Government (MHCLG), devolved administrations and our surveys.

8. Conclusions

The flow of funds provide a framework that has multiple analytical uses, which can be particularly relevant for the purpose of looking at financial stability. The global financial crisis in 2008 highlighted how the integrated nature of modern financial systems can transmit financial shocks through domestic and global economies. The financial accounts provide a way to understand financial risks.

Helping to provide policy insights is particularly relevant for the UK, and understanding the financial system and its links to borrowers and savers in the real economy is important in considering a wide range of policy questions. In response to this increased demand for enhanced financial information, we have looked to develop “for-whom to-whom” matrices for the first time in the UK.

In line with the strategy Better Statistics, Better Decisions, the original ambition was to improve the quality, coverage and granularity of the UK Financial Accounts, including counterparty information on all financial transactions. Where possible, we will incorporate administrative, regulatory and commercial information.

In collaboration with the Bank of England, we have made considerable progress in recent years. Our experimental estimates provide our most granular experimental information to date for the UK financial accounts, incorporating over 10 new data sources, which provide greater insight into the sector and instrument relationships within the financial matrices. Further work is planned to increase the granularity and improve the quality and coverage of counterparties relationships ahead of the implementation of the flow of funds in the UK National Accounts in 2021 and beyond.

Back to table of contents10. References

Bean, Charles, 2016, Independent Review of UK Economic Statistics

Bank of England Discussion Paper, 2009, The role of macroprudential policy

Bank of England, Financial Stability Report, November 2018 (PDF, 6.75MB)

Bank of England, Inflation Report, February 2019

Cerovic, Svetlana and Jose Saboin Dominican Republic: Sectoral Financial Positions, IMF Working Paper, 16/208

Crockett, Andrew, April 2000, Search of anchors for financial and monetary stability, Vienna

Drehmann, Mathias Total credit as an early warning indicator for systemic banking crisis, BIS Quarterly Review, June 2013

Errico, Luca, Richard Walton, Alicia Hierro, Hanan AbuShanab and Goran Amidzic, Statistics Department, International Monetary Fund, 2013, Global Flow of Funds: Mapping Bilateral Geographic Flows (PDF, 274KB)," 59th International Statistical Institute (ISI) World Statistics Congress

Frecaut, Oliver 2004, Indonesia Banking Crisis: A new perspective on $50 billion of losses, Bulletin of Indonesian Economic Studies, Volume 40, Issue 1

Financial Stability Board, 2018, Global Shadow Banking Monitoring Report 2017 (PDF, 2.1MB)

Financial Stability Board, 2018, Implementation and Effects of the G-20 Financial Regulatory Reforms (PDF, 2.9MB)

Financial Stability Board and IMF, 2015, The Financial Crisis and Information Gaps Data Gaps

Guibaud, Stephane, Yves Nosbusch, and Dimitri Vayanos, 2013, Bond Market Clienteles, the Yield Curve, and the Optimal Maturity Structure of Government Debt (PDF, 425KB), NBER Working Paper Series 18922

Heath, Robert and Evrim Bese Goksu, 2017, Financial Stability Analysis: What are the Data Needs? IMF Working Paper 17/153

Lagarde, Christine, March 28, 2019, The Euro Area: Creating a Stronger Economic Ecosystem

IMF Policy Paper, 2015, Balance Sheet Analysis in Fund Surveillance

IMF, 2013, External Debt Statistics Guide, 2013

IMF, 2016, Monetary and Financial Statistics Manual and Compilation Guide

Inter-Agency Group on Economic and Financial Statistics reference document, October 2015, Consolidation and corporate groups: an overview of methodological and practical issues (PDF, 637KB)

Kynaston, David, 1994, The City of London: A World of Its Own, 1815 to 1890, OECD: 2013, OECD Framework for Statistics on the Distribution of Household Income, Consumption and Wealth

OECD: 2013, OECD Guidelines for Micro Statistics on Household Wealth

OECD, 2017, Understanding Financial Accounts, Ridgeway, Art, 2011, Development and Use of Flow of Funds Data: Canada (PDF, 468KB)

Shrestha, Manik and Reimund Mink, 2011, An Integrated Framework for Financial Flows and Positions on a From-Whom to-Whom Basis (PDF, 519KB)

Tissot, Bruno, 2016, Development of financial sectoral accounts: new opportunities and challenges for supporting financial stability analysis, BIS working paper 15

UN, System of National Accounts, 2008 (PDF, 9.8MB)

Back to table of contents11. Appendix 1: Data source articles for the enhanced financial accounts

| Source | Potential coverage | Additional information |

|---|---|---|

| Solvency II insurance data | Insurance, pensions, | Bank of England: Solvency II Experimental financial statistics for insurance using Solvency II regulatory data - enhanced financial accounts |

| Commercial data as a service | Equity, debt securities, | Equifax data to visualise patterns of borrowing across the UK Thomson Reuters data to better understand the economy Beauhurst data to better understand the economy Equifax data to better understand the economy |

| European Market Infrastructure Regulation EMIR (derivatives) | Derivatives | EMIR reporting obligations Financial Conduct Authority: EMIR data derivatives market policies Progress on financial derivatives data |

| New ONS pensions survey | Pensions, insurance | Pension estimates of unfunded schemes Pensions in the national accounts, a fuller picture of the UK’s funded and unfunded pension obligations: 2010 to 2015 Money in funded pensions and insurance in the UK National Accounts: 1957 to 2015 |

| ONS Financial Services survey (FSS) | Other financial institutions | Financial Services Survey 266 - return of assets and liabilities, Quarter 4 2018 Shadow banking – S.124 non-money market investment funds Financial Services Survey 266 - quarterly return of assets and liabilities Shadow banking, money market funds Shadow banking introduction |

| Banking sector (Bank of England) | Monetary financial institutions | Banking sector transformation |

| Other sources: Equifax Crest Equiniti | Equity | Economic Statistics Transformation Programme: enhanced financial accounts (UK flow of funds) – using Equifax data to visualise patterns of borrowing across the UK Patterns of borrowing using Equifax data, by local authority district, UK: 2015 and 2017 |

| Historic Data | Pre-1987 time series | Historical households and non-profit institutions serving households (NPISH) sectors’ data on loans and equity and investment fund shares or units Historic households and non-profit institutions serving households (NPISH) sectors data on debt securities Historic households and non-profit institutions serving households (NPISH) sectors data on currency and deposits Reconciling sources of historic data for the households and the non-profit institutions serving households (NPISH) sectors Historical estimates of financial accounts and balance sheets |