1. Introduction

Globalisation has led to an increase in the importance of multinational enterprises to national economies, whose activities and corporate structures often span many countries with varied degrees of complexity. The role of special purpose entities (SPEs) has also seen a rapid increase, as multinationals attempt to manage their access to capital markets, financial risks, and regulatory or tax burdens.

The measurement of SPEs is important for ensuring that foreign direct investment (FDI) statistics accurately capture financial flows and corporate structures, while the ability to isolate SPEs from headline statistics is increasingly required by users who wish to analyse the true beneficiaries and risk takers of cross-border investment.

The Office for National Statistics (ONS) uses quarterly and annual FDI surveys as the main source for producing UK FDI statistics. As a member of the International Monetary Fund’s Task Force on Special Purpose Entities (TFSPE), the ONS has explored available data sources along with the Task Force’s definition of SPEs to develop a decision tree for identifying resident SPEs in the UK’s FDI statistics.

This article outlines the agreed international definition of an SPE, summarises main findings of the TFSPE, and presents experimental estimates of UK inward FDI attributable to resident SPEs. The article also outlines considerations and challenges faced when producing these estimates, which we hope will inform future discussions and work.

Back to table of contents2. Special purpose entities: background and concepts

Foreign direct investment (FDI) refers to cross-border investment made by investors with the objective of establishing a lasting interest in an enterprise in an economy other than that of the investor.

An increasing globalised world with reduced capital controls, fewer barriers to trade and investment, deregulation of markets and technological progress have resulted in multinational enterprises becoming increasingly important for national and international economic stability and growth. The increasing importance of multinationals has also led to many governments adopting policies to attract direct investment into their economies for benefits such as increasing productive capacity, job creation, knowledge and technological transfers, and productivity.

Growth in multinationals’ international integration has also resulted in a rapid increase in the complexity of their corporate structures in terms of how they control investments, manage their risks, and exploit country-specific advantages. Country-specific advantages may be economic, such as an educated workforce or developed infrastructure, or financial, such as efficient capital markets or preferable tax regimes.

Managing these increasingly complex corporate structures and asymmetric financial, regulatory and tax regimes has led an increase in the use of special purpose entities (SPEs) – legal entities set up with the specific purpose of passing through financial investments or holding overseas assets and liabilities on behalf of a wider international multinational enterprise group. These entities have little to no physical presence in the economy they are based.

International manuals, including the European System of Accounts 2010; the Organisation for Economic Co-operation and Development’s (OECD’s) Benchmark Definition of Foreign Direct Investment, fourth edition; and the IMF’s Balance of Payments and International Investment Position Manual, sixth edition, all include definitions on SPEs and recommend national statistical institutes separately identify FDI transactions and positions undertaken by resident SPEs in their statistics.

The motive behind such recommendations is clear when FDI statistics are examined by partner country, where financial centres and offshore islands often have substantial FDI values relative to the size of their economies – reflecting the prevalence of SPEs.

Back to table of contents3. International Monetary Fund’s Task Force and decision tree

Although international manuals and organisations have emphasised the importance of separating out transactions and positions related to special purpose entities (SPEs) in foreign direct investment (FDI) statistics, there has been an outstanding requirement for an internationally agreed definition of SPEs. With this in mind, the International Monetary Fund (IMF) Committee on Balance of Payments Statistics created the Task Force on Special Purpose Entities (TFSPE) in 2016 with a two-year mandate. The TFSPE’s final report (PDF, 1.4MB) is available.

The TFSPE conducted a survey on the legal and national definitions of SPEs, their measurement and activity. Using this information, a SPE definition was proposed that included an upper limit of up to five employees, while no specific numerical threshold is recommended to account for physical presence and/or physical production.

SPEs were also defined to be directly or indirectly controlled by non-residents, who set them up with the objective of:

- accessing capital market of financial services

- isolating financial risk

- reducing regulatory or tax burden

- safeguarding the confidentiality of transactions

Using this definition and information gathered from the survey, the TFSPE produced a decision tree and typology. The decision tree was produced to allow national statistical institutes to classify entities as SPEs, while the typology was produced to provide context around the type of activities undertaken by SPEs – but was not designed to be an exhaustive list of activities undertaken by SPEs.

Back to table of contents4. Data sources

To estimate the proportion of foreign direct investment (FDI) attributable to special purpose entities (SPEs), data linking was undertaken using microdata from the FDI population and the Inter-Departmental Business Register (IDBR). FDI estimates used in this article are for the 2016 reference period, consistent with results published in December 2017.

Inter-Departmental Business Register

The IDBR is a comprehensive list of 2.6 million businesses in all parts of the UK economy, other than the very small businesses and some non-profit making organisations. The two main sources of input are Value Added Tax (VAT) and Pay As You Earn (PAYE) income tax data from HM Revenue and Customs. Additional input comes from Companies House, Dun and Bradstreet, business surveys and businesses profiling.

Foreign Direct Investment population and survey

The FDI population is produced from four sources:

- combining IDBR and Dun and Bradstreet (D&B) data to identify cross-border business relationships between UK businesses and their foreign parents or subsidiaries (where the parent controls more than 50% of the subsidiary’s ordinary shares)

- a separately maintained database for enterprises that have previously been identified through the FDI or Mergers and Acquisitions surveys; this database includes minority share relationships (where the parent controls 50% or less of the subsidiary’s ordinary shares) that are not included in the IDBR and D&B

- the FDI population is also updated regularly using information from the ONS Mergers and Acquisitions Survey, which is conducted on a quarterly basis

- FDI estimation methods predict values for all non-sampled businesses, allowing for analysis of sampled and non-sampled businesses at a microdata level

Decision tree

The FDI population and IDBR were matched to produce a dataset of cross-border FDI variables along with economic variables and UK employment and turnover for enterprise groups in the inward FDI population. More detail on the method used to match the two populations is available in Annex C of the article UK foreign direct investment, trends and analysis: July 2018.

It was also not possible to match all the inward FDI population to the IDBR, as some entities did not have enterprise identifiers, such as banks and bank holding companies (aggregates provided by the Bank of England), residential property, and public corporations. There were also some enterprises in the remainder of the FDI population that could not be linked to the IDBR – which were part of the separately maintained FDI population. Domestic balance sheet data are also not available via the IDBR; therefore, the decision tree used turnover as a proxy for physical UK operations.

Using the data available, the decision tree was produced using the definition from the International Monetary Fund’s (IMF) Task Force on SPEs with data available at the time of analysis.

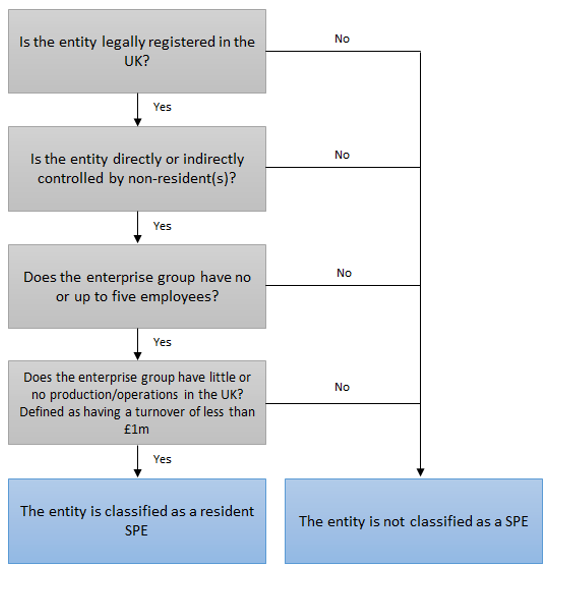

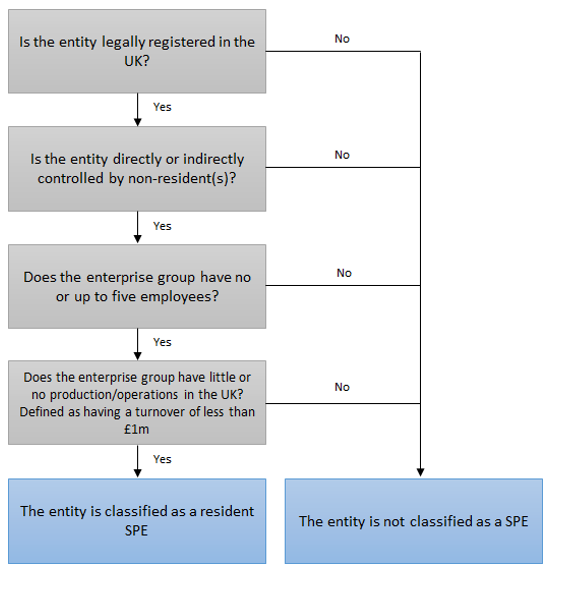

Figure 1: Decision tree classifying a resident special purpose entity

Source: Office for National Statistics, IMF Task Force on SPEs

Download this image Figure 1: Decision tree classifying a resident special purpose entity

.png (71.6 kB){kind=link}

5. High-level results

Using the definition developed by the International Monetary Fund’s Task Force on Special Purpose Entities (TFSPE) and data sources available at the time of analysis, this article estimates that £74 billion, or 8.4%, of the UK’s inward foreign direct investment (FDI) position in 2016 was attributable to special purpose entities (SPEs).

As shown in Table 1, the UK’s inward FDI position was £1,200 billion in 2016, of which £323 billion related to entities that did not have employment and turnover data available at the time of analysis – see previous section for more information on why.

Over two-thirds of the groups in the FDI population were matched to the Inter-Departmental Business Register (IDBR), who in turn accounted for £877 billion of UK inward FDI in 2016. Of these, £82 billion of inward FDI positions were held by groups with five or fewer employees, which fell to £74 billion when the threshold of £1 million was applied.

| Positions | Income | |

|---|---|---|

| Total inward population | 1,200 | 52 |

| Banks, bank holding companies, property, public corporations, and unmatched businesses | 323 | 15 |

| Analysed population | 877 | 38 |

| Those meeting employment threshold | 82 | 2 |

| Those meeting employment and turnover threshold | 74 | 1 |

Download this table Table 1: High-level estimates of resident SPEs in the inward FDI population, £ billion, 2016

.xls .csv6. Characteristics

Comparing the characteristics of enterprise groups classified as resident special purpose entities (SPEs) to non-SPEs can help provide more context to their structure and use.

Figures 2a and 2b1 present the geographical composition of resident SPEs and non-SPEs respectively. There is a clear distinction between the two, with the immediate parents of SPEs largely residing in “remainder” – a grouping comprising North America and non-EU Europe that has been supressed to mitigate disclosure. In contrast, a large proportion of inward foreign direct investment (FDI) positions belonging to non-SPEs are attributable to immediate parents based in the EU.

Figure 2a: Geographical composition of resident special purpose entities, UK

2016

Source: Office for National Statistics

Notes:

- Figures presented in this chart exclude banks, bank holding companies, property, public corporations, and entities with no employment or turnover information unless otherwise specified.

Download this chart Figure 2a: Geographical composition of resident special purpose entities, UK

Image .csv .xls

Figure 2b: Geographical composition of non-special purpose entities, UK

2016

Source: Office for National Statistics

Notes:

- Figures presented in this chart exclude banks, bank holding companies, property, public corporations, and entities with no employment or turnover information unless otherwise specified.

Download this chart Figure 2b: Geographical composition of non-special purpose entities, UK

Image .csv .xlsFigures 3a and 3b consider the industry composition of resident SPEs and non-SPEs respectively. There are clear distinctions between the two classifications, with a notably larger proportion of enterprise groups classified as resident SPEs sitting within the financial and insurance services industries (89%). In contrast, non-SPEs appear to be more diverse, with the majority sitting in manufacturing (32%), mining and quarrying (11%), and financial and insurance services (11%) industries.

Figure 3a: Industry composition of resident special purpose entities, UK

2016

Source: Office for National Statistics

Notes:

- Figures presented in this chart exclude banks, bank holding companies, property, public corporations, and entities with no employment or turnover information unless otherwise specified.

Download this chart Figure 3a: Industry composition of resident special purpose entities, UK

Image .csv .xls

Figure 3b: Industry composition of non-special purpose entities, UK

2016

Source: Office for National Statistics

Notes:

- Figures presented in this chart exclude banks, bank holding companies, property, public corporations, and entities with no employment or turnover information unless otherwise specified.

Download this chart Figure 3b: Industry composition of non-special purpose entities, UK

Image .csv .xlsNotes for: Characteristics

- Note that figures presented in this chart and thereafter exclude banks, bank holding companies, property, public corporations, and entities with no employment or turnover information unless otherwise specified.

7. Considerations

Results presented in this article are experimental estimates produced through using the definition produced by the International Monetary Fund’s Task Force on Special Purpose Entities (TFSPE) and data that were available at the time of research. Given these are initial estimates, there are a number of areas that could be investigated in future to improve the accuracy of estimates.

An area for future consideration is the sensitivity of the thresholds used. The TFSPE classifies entities as SPEs based on assumptions regarding their characteristics – particularly employment and physical presence. To illustrate the sensitivity of these assumptions, Figure 4 presents the cumulative value of UK inward foreign direct investment (FDI) positions attributable to businesses by employment size.

As shown, enterprise groups meeting the employment threshold of up to two employees accounted for £57 billion of the UK’s inward FDI position in 2016. Increasing the threshold to five employees raises this to £82 billion, to £86 billion for six employees, and £103 billion when the threshold is set to 10 employees.

Figure 4: Sensitivity of employment thresholds, cumulative £ billion, UK

2016

Source: Office for National Statistics

Notes:

- Figures presented in this chart exclude banks, bank holding companies, property, public corporations, and entities with no employment or turnover information unless otherwise specified.

Download this chart Figure 4: Sensitivity of employment thresholds, cumulative £ billion, UK

Image .csv .xlsA further consideration was that, using the data sources available at the time of the research, it was not possible to separate enterprises that met the definition of a SPE but were also part of a wider enterprise group that had operations in the UK through other enterprises. For example, an enterprise group may control a special purpose entity in the UK to manage their international finances; however, they may also control several other enterprises undertaking economic output.

Of approximately 19,000 groups analysed, slightly over 1,400 had an aggregate employment level that exceeded five when combining all their enterprises, but also had at least one enterprise meeting the employment threshold. Inclusion of these other enterprises would likely increase the value of inward FDI positions; however, it is unclear whether they should be considered SPEs.

A further area is the use of balance sheet information as part of the decision tree. Balance sheet data are not currently available via the Inter-Departmental Business Register (IDBR), therefore, the decision tree developed is arguably less sophisticated than that developed by the Task Force. Using wider data sources in future would allow for better measurement of UK physical presence, rather than the use of turnover as a proxy.

A further consideration was that, given resident SPEs are not currently identified, the FDI sample design and estimation methods do not currently treat resident SPEs separately. As such, businesses with low turnover can be grouped in smaller stratums unless previously identified through random sampling. Table 2 presents the sampling proportions for enterprise groups classified as resident SPEs and non-SPEs in this analysis. As can be seen, a smaller proportion of SPEs are sampled compared with non-SPEs – possibly due to fewer sitting in sampling stratums reserved for larger businesses according to turnover. Furthermore, while fewer are sampled, those that are account for a larger proportion of the overall value estimated for groups classified as SPEs.

| SPE | Non-SPE | |

|---|---|---|

| Percentage of groups sampled | 16 | 19 |

| Percentage of inward positions sampled | 95 | 90 |

Download this table Table 2: Sampling and estimation of resident special purpose entities (SPEs) and non-SPEs

.xls .csvFinally, an important area for future research is to classify all entities within the FDI population. As noted in the article, not all entities in the FDI population were classified as it was not possible to link them all to the IDBR. A future review of the data sources used for these estimates may help improve the results.

Back to table of contents8. Conclusions

Accurate coverage and separation of special purpose entities (SPEs) has become ever more important for ensuring FDI statistics are accurate and remain useful to users – who increasingly need to separate SPEs from headline statistics to understand the true beneficiaries and risk takers of FDI.

While international manuals and organisations have emphasised the importance of measuring SPEs in foreign direct investment (FDI) statistics, there has been an outstanding requirement for an internationally agreed definition. As such, the International Monetary Fund’s Task Force on Special Purpose Entities (TFSPE) proposed definition, decision tree and typology are a welcome development that provides a clear framework for classifying SPEs.

Results presented in this article have been produced through using definitions produced by the TFSPE and available data sources. The experimental results estimate that £74 billion of the UK’s inward FDI positions were attributable to enterprise groups classified as SPEs, or 8.4% of the positions analysed. The results also suggested these groups’ economic activity and their immediate parents are distinct from groups not classified as SPEs.

While these results are a positive step towards being able to separate resident SPEs from UK FDI statistics, the article also highlighted a range of areas for future development to help improve these results. These largely focus on increasing the availability of data regarding multinationals conducting FDI in the UK, particularly on their UK operations and intra-group transactions.

Back to table of contents9. Acknowledgements

The author Sami Hamroush (Office for National Statistics (ONS)) would like to thank Rachel Jones (ONS), Andrew Jowett (ONS), Marc John (ONS), Freddy Farias Arias (ONS), Rishi Attri (ONS), Tjeerd Jellema (ECB) and the membership of the International Monetary Fund’s Task Force on Special Purpose Entities for their contributions to this work.

Back to table of contents