1. Main points

The number of households in the private rented sector in the UK increased from 2.8 million in 2007 to 4.5 million in 2017, an increase of 1.7 million (63%) households.

Younger households are more likely to rent privately than older households; in 2017 those in the 25 to 34 years age group represented the largest group (35%).

Households in the private rented sector are getting older; between 2007 and 2017, the proportion of household reference persons aged 45 to 54 increased from 11% to 16% while those aged 16 to 24 dropped from 17% to 12%.

As at financial year ending (FYE) 2017, 62% of households in the private rented sector in the UK had spent under three years in the same accommodation and only a small proportion (4%) had been in the same residence for 20 years or longer.

Northern Ireland has the newest private rented dwelling stock (38% built after 1980) in the UK, while Wales has the oldest (43% built pre-1919).

2. Things you need to know

This article has been complied to provide users with a better understanding of the private rented sector across the UK, what statistics are available for this sector and where possible, how the sector (and the statistics produced) differs across each of the four UK countries. The article builds on the work started by a cross-government group, which formed in 2017 to improve the accessibility and coherence in housing statistics. Further articles are planned that will cover other important sectors of housing and planning statistics, such as homelessness and affordability.

We welcome your views on the content and format of this article. Please contact us using the email address hpi@ons.gov.uk to discuss any aspect, including your views on how we can improve this article.

In February 2019, we will be holding a Housing user event. While the exact timings and content for the event are to be agreed, the event will include presentations on this article and other recently published official statistics which relate to housing. To add your details to the distribution list, which will be sent out at a later date confirming the details, please contact hpi@ons.gov.uk.

Wider housing statistics

While this article focuses on the private rented sector (PRS), it is useful to understand what other statistics are currently available, not only for the PRS but also the wider housing system. The decentralised nature of the UK housing system means that different organisations produce various statistics about different aspects of housing. To assist users, a cross-government housings statistics group was formed to help improve the coherence and accessibility of statistics in this area, recently publishing a guide to UK housing and planning statistics (XLSX, 43.7KB).

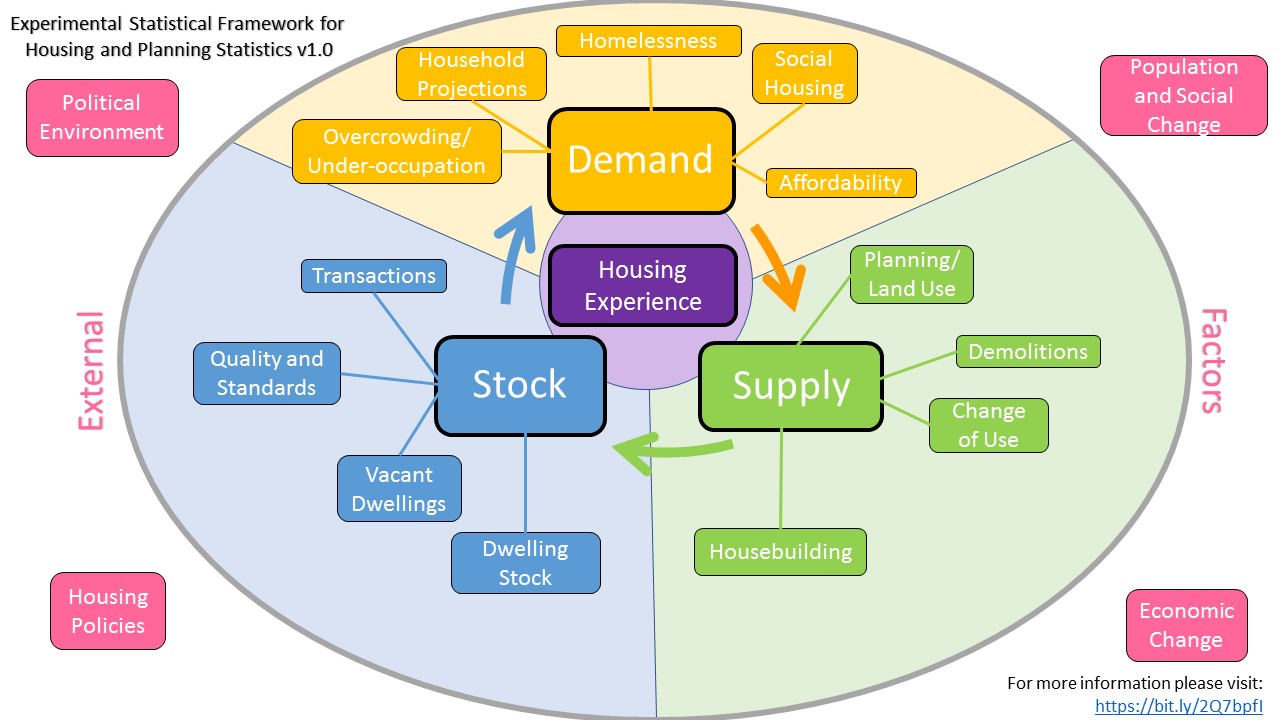

The guide, which will be reviewed and updated on a frequent basis, provides an overview of the statistics currently produced across the housing system classified as either contributing to the demand, stock or supply side of housing. In addition to this, users may be interested in the experimental UK housing and planning statistics framework (JPG, 124KB), which is intended to conceptually illustrate the areas of housing and planning that may be of interest across the UK official statistics landscape.

{kind=link}

Both the guide and the framework will be subject to further development. However, in their current form they should provide users with a better understanding of the statistics which are produced. One area where departments and devolved administrations are collaborating is to improve the coherence of housing statistics. This article on the private rented sector is part of this aim as published in the workplan (PDF, 101.18KB).

Back to table of contents3. Tenants

This section focuses on those living in the private rented sector. To enable national comparisons the Family Resources Survey (FRS) and Annual Population Survey (APS) have been used, which have UK coverage. Each country also publishes a separate breakdown based on their own housing surveys. Some information on the types of household, age of the head of household and economic activity is available from each nation’s surveys, albeit in slightly different forms. There is also information provided for some nations through their surveys that is not available on other nation's surveys. For example, English and Scottish surveys ask health-related questions, but this is not available from the Northern Ireland surveys.

In 2001, household reference person (HRP) replaced head of household (HOH) for most government social surveys. How the HRP is defined varies across surveys. In the FRS it is defined as the highest income householder. Pre-2011, the head of household referred specifically to the male member of a cohabiting household.

UK

Figure 1 shows the increase in the percentage of households in privately rented accommodation over the past decade from 13% in financial year ending (FYE) 2007 to 20% in FYE 2017. This contrasts with the percentage of owner occupiers, which has seen a decline over the same period. For the period FYE 2017, the most recent data available, private renters accounted for 20% of all households, compared with 62% for owner occupiers and 17% for social housing occupants.

Figure 1: Households by tenure, FYE 2007 to FYE, 2017, UK

Source: Family Resources Survey, Department for Work and Pensions

Download this chart Figure 1: Households by tenure, FYE 2007 to FYE, 2017, UK

Image .csv .xlsWhen considering absolute changes in households by tenure it is important to note that the total number of households in the UK has increased by 1.6 million homes (7%) over the past decade, from 25.6 million households in 2007 to 27.2 million households in 2017 (Families and Households: 2017, Labour Force Survey households dataset).

The number of households living in the private rented sector in the UK increased from 2.8 million in 2007 to 4.5 million in 2017, an increase of 1.7 million (63%). Over this period, the number of owner occupier households remained broadly consistent at 17.7 million households. However, households owned outright increased from 7.9 million to 9.4 million while households buying with a mortgage fell from 9.8 million to 8.3 million. The number of social rented households decreased by 200,000 households to 4.5 million (Annual Population Survey). The APS is not a stand-alone survey; it uses data combined from two waves of the main Labour Force survey and has a larger sample size than the FRS. It should be noted when comparing 2007 with 2017 figures that APS data from 2006 to 2011 is weighted with 2014 population estimates, while 2012 to 2017 data are weighted with 2017 population estimates.

Younger households are more likely to rent privately, with those in the 25 to 34 years age group representing the largest group (Figure 2). Households in the 45 to 54 years age group saw the biggest percentage increase from 11% in 2007 to 16% in 2017, an estimated increase of 384,000 households.

Figure 2: Private renting sector by age of household reference person, 2007 and 2017, UK

Source: Annual Population Survey, requested table, Office for National Statistics

Download this chart Figure 2: Private renting sector by age of household reference person, 2007 and 2017, UK

Image .csv .xlsIn FYE 2017, 35% of one adult households with children were in the private rented sector, compared with 18% in FYE 2007. For households without children, the largest percentage increase has been for households comprised of one male adult. In FYE 2007, 16% were in the private rented sector compared with 27% in FYE 2017 (Family Resources Survey).

England

In FYE 2017, the private rented sector accounted for 21% of households in England (Family Resources Survey), similar to that of the UK (20%). The proportion of private rented sector households has doubled since FYE 1997 and the overall size of the private rented sector has increased from 2.6 million households in FYE 2007 to 4.7 million households in FYE 2017 (English Housing Survey). The sector grew a little between FYE 1997 and FYE 2007 (0.5 million), but growth accelerated after FYE 2007, with over two million additional households added to the sector. However, growth has slowed in more recent years.

In FYE 2017, household reference persons (HRP) in the private rented sector in England were, on average, younger than social renters and owner occupiers, with a mean age of 40 years (compared with 52 years for social renters and 57 years for owner occupiers). Whilst this is broadly unchanged over the past ten years, the distribution of the sector across age bands has shifted (English Housing Survey).

Over the past 20 years, the biggest change was in the proportion of 35- to 44-year-olds living in the private rented sector, increasing from 16% in FYE 1997 to 24% in FYE 2017 (Figure 3). There were more than three times as many 35- to 44-year-olds renting privately in FYE 2017 than 20 years ago: an increase from 331,000 households in FYE 1997 to 1.1 million in FYE 2017. The single largest group of private renter HRPs remains the 25 to 34 years age band, which represents 33% of the sector with 1.5 million households.

Figure 3: Age of household reference person in private rented sector, FYE 1997, FYE 2007 and FYE 2017, England

Source: English Housing Survey, Ministry of Housing Communities, and Local Government

Download this chart Figure 3: Age of household reference person in private rented sector, FYE 1997, FYE 2007 and FYE 2017, England

Image .csv .xlsHRPs in the private rented sector appear to be the most diverse in terms of ethnicity and nationality, compared with HRPs living in other tenures. In FYE 2017, the majority are white, at 82%, the same as social renters and lower than owner occupiers (92%). The next single grouping is black HRPs, who make up 5% of the private sector, compared with 8% of social renters and 1% of owner occupiers. Around three-quarters (74%) of private renters are UK or Irish nationals, the lowest of any sector; these being 91% of social renters and 97% of owner occupiers. Around 17% of private renting HRPs were EU citizens, compared with 4% and 2% of social renters and owner occupiers. The remaining 9% of the private rented sector’s HRPs have a nationality from outside the UK or EU (5% for social renters and 2% for owner occupiers).

Looking at economic activity, most private renter HRPs are in work (74%) compared with 61% of owner occupiers and 43% of social renters (Figure 4). The number of private renters in work has roughly doubled since FYE 2007. However, the number of households in the private rented sector has also increased over this period. Throughout this time, the increase in part-time workers is greater than for those in full-time employment.

In FYE 2017, the widest gap between HRPs in the private rented sector and all tenures is for those who are in retirement – 9% of private renters are retirees, compared with 28% across all households, although this may in part reflect the younger age profile of the private rented sector. The proportion of the private rented sector that are students has not changed much over the past decade – from 7% in FYE 2007 to 6% in FYE 2017.

Figure 4: Proportion of HRPs by economic activity, private rented sector and all tenures, FYE 2017, England

Source: English Housing Survey, Ministry of Housing, Communities, and Local Government

Download this chart Figure 4: Proportion of HRPs by economic activity, private rented sector and all tenures, FYE 2017, England

Image .csv .xlsThe English Housing Survey (EHS) also collects data by national statistics socio-economic classification, allowing analysis by occupation. Those in higher and lower managerial and professional occupations make up the largest segment of the private rented sector, accounting for 41% of HRPs, compared with 51% for owner occupiers and 15% for social renters. Routine and semi-routine occupations follow at 29% for the private rented sector, 56% in the social rented sector and 18% in the owner-occupied sector.

In FYE 2017, 38% (1.7 million) of households in the private rented sector had dependent children, similar to the proportion in the social rented sector (35%, 1.4 million). In the owner-occupied sector, 44% (2.9 million) of those buying with a mortgage had dependent children, compared with 9% (0.6 million) of those who own outright (EHS).

Scotland

In FYE 2017, the private rented sector accounted for 15% of households in Scotland, below the percentage for the UK (20%). While Scotland has the same proportion of households in the owner-occupied sector (63%) as the UK, it has a higher proportion of households in the social renting sector, 22% compared with 17% in the UK. The proportion of households in the private rented sector has increased from 9% in FYE 2007 to 15% in FYE 2017 (Family Resources Survey). Separate results from the Scottish Household Survey over the longer period 1999 to 2017 show that the private rented sector accounted for only 5% of homes in 1999. They also show that the increase from 5% to 15% between 1999 and 2017 has equated to an estimated extra 240,000 households living in the sector over this time period, an increase from 120,000 to 360,000 households. Alternatively, owner occupiers accounted for 61% of homes in 1999 (1.3 million households), and 62% in 2017 (1.5 million). Social renters made up 32% of households in 1999 (approximately 700,000) and 22% in 2017 (550,000).

The Scottish Household Survey collects information on the age of the highest income householder (HIH). In 2017, 33% of HIHs renting privately were in the 25 to 34 years age band (approximately 120,000 households), the same percentage as in 2007 (when it was 70,000 households).

Figure 5: Age of highest income householders in the private rented sector, 2007 and 2017, Scotland

Source: Scottish Household Survey, Scottish Government

Download this chart Figure 5: Age of highest income householders in the private rented sector, 2007 and 2017, Scotland

Image .csv .xlsAdults in the private sector are more ethnically diverse compared with adults in other tenures. In 2017 only 58% of those in the private rented sector had recorded their ethnicity as being White Scottish, compared with 78% across all sectors. A further 31% of HIHs in the private rented sector had recorded their ethnicity as White Other British, Polish or Other. The remainder of HIHs had recorded their ethnicity as being Asian, Asian Scottish or Asian British (6%), African, Caribbean or Black (1%), or Other Ethnic Group (2%).

With respect to economic activity, Scotland mirrors the England picture, whereby owner occupier (61%) and private renting (56%) adults are more likely to be working than social renters (38%). There has been a large increase in the number of full time employed adults who are living in the private rented sector, with the number of full time employed adults increasing by an estimated 180,000 people between 1999 and 2017, from 70,000 to 250,000 adults. Six percent of private renting adults were retired, compared with 24% across all households. A fifth of private renters are students, in comparison to a twentieth across all tenures.

There has also been an increase in the number of adults in further or higher education who are living in the private rented sector, rising by an estimated 90,000 people between 1999 and 2017. Despite this increase, the share of all private renting adults who are in further or higher education was at a similar level in 2017 (20%) as in 1999 (22%) due to the overall growth of the sector.

Since 1999, there has been a small four percentage point increase in the share of households with children, so that in 2017 nearly a quarter (24%) of all privately renting households were households with children. However, it is worth noting that the private rented sector has a smaller share of large families and so the proportion of all children living in the private sector is lower than 24%. There were an estimated 150,000 children living in the private rented sector in 2017, which equates to around 15% of all children in Scotland. The 150,000 children living in the sector in 2017 is an increase of 110,000 on the 40,000 children living in the sector in 1999.

Wales

Estimates from the Annual Population survey are used due to its sample being larger than the Family Resource Survey for Wales. In 2017, the private rented sector accounted for 13% of households in Wales, below the percentage for the UK (17%). While Wales has a slightly lower proportion of households in the social rented sector (15%) compared with the UK (17%), it has a higher proportion of owner-occupied households, 71% compared with 66% in the UK (42% in Wales and 35% in the UK were owned outright, while 29% in Wales and 31% in the UK were bought with a mortgage). The proportion of households in the private rented sector has increased from 9% (118,000 households) of households in 2007 to 13% (176,000 households) in 2017 (Figure 6).

Figure 6: Households by tenure, 2007 to 2017, Wales

Source: Annual Population Survey, requested table, Office for National Statistics

Download this chart Figure 6: Households by tenure, 2007 to 2017, Wales

Image .csv .xlsThe National Survey for Wales finds that the proportion of households in the private rented sector has decreased for those aged under 45 years between FYE 2013 and FYE 2018, with the biggest percentage point fall in the 16 to 24 years age group (Figure 7). In FYE 2013, 31% of HRPs in the 16 to 24 years age band were in the private rented sector, this has fallen to 25% in FYE 2018. The decrease in the private rented sector for this age group is offset by an equivalent increase in the owner-occupied sector (from 52% in FYE 2013 to 57% in FYE 2018). The social rented sector remained broadly unchanged for these years at 17% and 18%.

Figure 7: Age of households in the private rented sector, FYE 2013 and FYE 2018, Wales

Source: National Survey for Wales, Welsh Government

Download this chart Figure 7: Age of households in the private rented sector, FYE 2013 and FYE 2018, Wales

Image .csv .xlsAn alternative source, the Annual Population Survey (APS), also provides a breakdown by age of HRPs. In 2017, the highest number of households in the private rented sector was in the age band 25 to 34 years (57,000), followed by 35 to 44 years (36,000), while the lowest was 75 years and over (8,000).

Northern Ireland

In FYE 2017, the private rented sector accounted for 21% of households in Northern Ireland (NI), similar to that of the UK (20%). Over the past decade the private rented sector has increased from 13% of households in FYE 2007 to 21% in FYE 2017 (Family Resources Survey). According to the APS, in 2007 the private rented sector in NI stood at 76,000, while the social rented sector was at 115,000, those buying with a mortgage at 262,000, and those who owned outright at 232,000. In 2017, the private rented sector had almost doubled to 138,000, the social rented sector had increased only slightly to 117,000, those buying with a mortgage had decreased substantially to 224,000 and those who owned outright had increased to 261,000.

The NI House Condition Survey (PDF, 678KB) (NIHCS) provides information on household composition, age of household reference person (HRP), household religion and employment status. These data are collected from the HRP. References to private rented sector HRPs in the survey also include those in tied dwellings. The HRP is defined as the owner or rent payer of the property, or highest earner where ownership or tenancy is joint. Data in this section come from the 2016 NIHCS.

Similar to the other countries of the UK, the age distribution of private renters in NI skews towards the young. Sixty-eight percent of all 17- to 24-year-old HRPs are private renters, compared with 9% owner occupiers and 24% social renters. It must be noted, though, that the 17 to 24 year age group consisted of small numbers and so caution should be applied when interpreting these proportions. Private renters are most common in the aged under 40 years categories, whereas owner occupiers are more frequent in the aged above 40 years categories. Social renters take up a fairly equal portion across tenures in all age categories (ranging from 14% to 18%) except aged under 24 years where they account for 24% of households. In terms of absolute numbers and proportions within tenures, 59,000 out of 136,000 (43%; Figure 8) private renters were in the 25 to 39 years category, the highest out of all age ranges. For social renters this was 41,000 out of 119,000 (34%) in the 40 to 59 years category, and for owner-occupiers this was 175,000 out of 488,000 (36%) in the 40 to 59 years age range.

Figure 8: Age of household reference person in private rented sector compared to all tenures, 2016, Northern Ireland

Source: Northern Ireland House Condition Survey, Northern Ireland Housing Executive

Download this chart Figure 8: Age of household reference person in private rented sector compared to all tenures, 2016, Northern Ireland

Image .csv .xlsWith regards to economic activity, around one-fifth (21%) of all HRPs in work were private renters according to the NIHCS of 2016, compared with 71% of those in work being owner occupiers, leaving 8% of these as social renters. In 2006, 43% of private renters were in work, compared with 57% (78,000 of 136,000) in 2016. For owner occupiers this was 61% in 2006 down to 55% (269,000 of 488,000) a decade later, and for social renters this was 18%, which increased to 25% (30,000 of 119,000) in 2016. Those private renters not working remained at around 20% from 2006 to 2016. In this categorisation, not working refers to job seekers as well as those who are not seeking a job and students. Retired HRPs were more likely to be in the owner-occupied sector (38%) than in the private rented sector (11%), while social renters were almost as likely as owner occupiers to be retired (30%). The low proportion of retired households reflects the low representation of older age bands in the sector.

Looking at household compositions, the survey splits households into three categories: adult households, households with children and older households. Of these, adult households showed the largest increase in moving to the private rented sector over the past 10 years, from 12% of adult households choosing to rent privately in 2006 to 19% in 2016, so that they now make up just under 41% (55,000 of 136,000) of the sector. Most of this increase occurred between 2006 and 2011. The proportion of households with children in the sector has also increased, with 47% of private rented households with children in 2016; this is now the single largest group in the sector. Older households make up the rest of the sector, at just 13%. Just under a third (29%) of all households with children lived in the private rented sector. Adult households were most likely to be owner occupiers (64%) out of all tenures, similarly for households with children (55%), and older households most of all (78%), reflecting this being the predominating tenure in terms of size.

Back to table of contents4. Affordability

Affordability is an important issue facing households. A more detailed focus on affordability across all tenures will be explored in a future article. Data from the Family Resources Survey is used for comparisons across countries. Other national surveys are used within each country chapter to provide further details for each country, however these are not all fully comparable across nations.

Great Britain

As a simple measure, we can consider the growth in private rental prices relative to the growth in earnings over the same period. Figure 9 suggests that, at a Great Britain level, growth in private rental prices, as measured by the Index of Private Housing Rental Prices (IPHRP) rose above that of Average Weekly Earnings (AWE) up until 2016, however the gap has narrowed since then, driven by a slowdown in the growth of private rental prices.

Figure 9: Average Weekly Earnings and Index of Private Housing Rental Prices indices, January 2011 to October 2018, Great Britain

Source: Average Weekly Earnings and Index of Private Housing Rental Prices, Office for National Statistics

Notes:

- AWE equates to money paid per week, per job to employees in Great Britain, not including those who are self-employed. It is the lead measure for short-term earnings growth.

- IPHRP is an experimental index tracking prices paid for renting property from private landlords in the UK.

Download this chart Figure 9: Average Weekly Earnings and Index of Private Housing Rental Prices indices, January 2011 to October 2018, Great Britain

Image .csv .xlsWhile the IPHRP does measure inflation of private rental prices, average weekly earnings are not available with a split by tenure and therefore may not accurately reflect changes to earnings for those living in the private rented sector. In addition, average weekly earnings figures do not take into account income from other sources, including pensions or benefits.

A fairer comparison might be to consider rent relative to income for households in the private rented sector using a consistent data source such as a household survey. In interpreting survey data over time users should be aware that no adjustment is made for the quality of housing that these housing costs are associated with. For example, changes in the average size of properties or number of rooms over time are not adjusted for.

Figure 10 presents the average ratios of housing costs to income for each country in Great Britain country over the nine-year period from financial year ending (FYE) 2008 to FYE 2016 based on Family Resources Survey (FRS) data. Pooled samples across three years of data have been used to improve statistical reliability.

Net income is defined here as the total income received (including housing benefit payments) by the household excluding taxes such as income tax and council tax. Net income has not been adjusted (“equivalised”) for family size. Housing costs include rent gross of Housing Benefit, as well as water rates and service charges where applicable.

For the FYE 2014 to FYE 2016 period, private rented households in England paid more for housing costs as a proportion of income (32%) than households in Wales (29%) and Scotland (25%). This pattern has not changed much over the last ten years (Figure 10). This likely reflects those in England having higher housing costs. However, there is also some evidence that household incomes in the private rented sector (PRS) can vary between countries, with 37% of PRS households in Wales having a net annual income of £15,000 or less, compared with 30% in Scotland and 21% in England (FRS data). It is important to note that Wales has a smaller sample size and therefore greater margin of error than the other two countries, so this difference in ratios may not be statistically significant.

The median household weekly private rent payment for the UK, according to the Family Resource Survey FYE 2017, was £134. The highest median was in England at £138, with the lowest being in Northern Ireland at £97. Wales and Scotland stood at £105 and £112 respectively.

Figure 10: Median ratio of private rented housing costs to net unequivalised household income, FYE 2008 to FYE 2016, countries of Great Britain

Source: Social Tenants in Scotland 2016, Scottish Government, estimates based on Family Resources Survey data

Notes:

- Data for Northern Ireland is excluded as it is not available on a consistent basis.

Download this chart Figure 10: Median ratio of private rented housing costs to net unequivalised household income, FYE 2008 to FYE 2016, countries of Great Britain

Image .csv .xlsTo have a large enough sample size to look at the same affordability ratios across income deciles for countries in Great Britain, FRS data from FYE 2012 to FYE 2016 has been pooled. This analysis reveals that housing costs take up a much higher proportion of income for those in the lowest income decile (64% in England; 68% in Wales and 57% in Scotland), compared with the highest income decile (20% in England; 14% in Wales; 15% in Scotland). Figure 11 shows the downward trend in this affordability ratio as income increases; housing costs are a lot more affordable for those on higher incomes.

Figure 11: Median ratio of housing costs to net household income, by PRS income decile and country (combined five years of data FYE 2012 to FYE 2016), countries of Great Britain

Source: Calculation based on Family Resources Survey data, Department for Work and Pensions

Download this chart Figure 11: Median ratio of housing costs to net household income, by PRS income decile and country (combined five years of data FYE 2012 to FYE 2016), countries of Great Britain

Image .csv .xlsSeparate earnings-based rental affordability statistics are also available within Housing summary measures analysis: 2016, publishing England and Wales estimates down to a local authority level. Household income-based measures of affordability, as presented here, are more comprehensive but are not available for lower geographies at present.

Another element of affordability is financial support received. Housing Benefit is available to support eligible low-income households with the cost of renting their home. The benefit can cover the whole cost of rent or part of it, depending on income, circumstances, and other factors such as the type of landlord and local housing allowance rates.

Universal Credit (UC) is being introduced in stages across the UK. UC began a gradual rollout across the UK in 2013, starting with some postcodes in the North West of England. As of 2018, all new benefit claimants in England, Wales, Scotland and Northern Ireland will have to apply for Universal Credit, while existing claimants with no changes in circumstances will not be asked to switch over until at least 2019. It will eventually replace Housing Benefit, income support, income-related employment and support allowance, income-based jobseeker's allowance, child tax credits, and working tax credit. Some Universal Credit claimants will receive the housing element, which will provide help with rent costs.

Figure 12 shows the percentage of dwellings receiving housing benefit from 2011 to 2016 for the private rented sector for England, Scotland and Wales, using housing benefit claim estimates from the Department for Work and Pensions (DWP) and dwelling stock estimates from the Ministry of Housing, Communities and Local Government (MHCLG). The percentage of dwellings receiving housing benefit has decreased for Scotland between 2011 and 2016, with Wales decreasing since 2013 and England showing a broad decrease over this period. Wales had the highest percentage of households receiving housing benefit in 2016 at 40%, compared with 27% in England and 23% in Scotland. At the end of 2011, the total number of private renting housing benefit claimants in England was 1.4 million, while for Wales it was 82,000 and for Scotland 93,000. This decreased in 2016 for England to 1.2 million, for Wales to 76,000, and for Scotland to 84,000. Over this period the number of households and dwellings in the private rented sector also grew for all countries of the UK. The trend from 2013 onwards could be impacted by the introduction of UC and claimants switching from housing benefit to UC, along with new benefits claimants now claiming UC.

Figure 12: Housing Benefit claimants as a percentage of dwellings by country for private rented sector, countries of Great Britain

Source: Calculation based on Department for Work and Pensions housing benefit claim estimates and Ministry of Housing, Communities, and Local Government dwelling stock estimates

Notes:

- The decrease from 2013 onwards could be due to the introduction of Universal Credit (UC) and claimants switching from housing benefit to UC, along with new benefit claimants now claiming UC.

- These figures exclude those receiving the housing element of UC.

Download this chart Figure 12: Housing Benefit claimants as a percentage of dwellings by country for private rented sector, countries of Great Britain

Image .csv .xlsWhile not directly comparable due to differing sources and methodology, the Northern Ireland Housing Conditions Survey reports that 43% (53,000) of private rented households in Northern Ireland were in receipt of housing benefit in 2011, compared with 73% (81,000) of social rented households. In 2016 this was broadly unchanged at 42% (57,000) for private rented households, and slightly lower at 66% (78,000) for social rented households.

England

The proportion of household income (including housing benefit) that private renters spent on their rent has not changed between FYE 2011 and FYE 2017 (English Housing Survey, EHS). In FYE 2017, those privately renting spent 34% of their gross household income on rent, compared to 28% for social renters. Those buying their home with a mortgage spent 18% of their household income on mortgage payments.

Figure 13: Mortgage or rent as a ratio of household income (including and excluding housing benefit), by tenure, FYE 2017, England

Source: English Housing Survey, Ministry of Housing , Communities, and Local Government

Download this chart Figure 13: Mortgage or rent as a ratio of household income (including and excluding housing benefit), by tenure, FYE 2017, England

Image .csv .xlsWhen only household reference person and partner income is used (irrespective of whether there are other adults in the household), those buying their home with a mortgage spent, on average, 19% of their income on mortgage payments, whereas rent payments were 31% of income for social renters and 41% of household income for private renters including Housing Benefit. Excluding Housing Benefit, the average proportion of income spent on rent was 41% for social renters and 46% for private renters.

According to the EHS, median weekly rent in London is nearly twice that of the rest of England. In FYE 2017 London median weekly rent was £309 compared with £158 for England excluding London (Figure 14).

Figure 14: Median weekly rents, private renters, FYE 2009 to FYE 2017, London and England excluding London

Source: English Housing Survey, Ministry of Housing, Communities, and Local Government

Download this chart Figure 14: Median weekly rents, private renters, FYE 2009 to FYE 2017, London and England excluding London

Image .csv .xlsGrowth in private rental property rental prices in London has historically been above the rest of England but has slowed in recent years (Figure 15).

Figure 15: Index of Private Housing Rental Prices percentage change over 12 months, January 2006 to December 2018, London and England excluding London

Source: Index of Private Housing Rental Prices, Office for National Statistics

Notes:

- IPHRP is an experimental index tracking prices paid for renting property from private landlords in the UK.

Download this chart Figure 15: Index of Private Housing Rental Prices percentage change over 12 months, January 2006 to December 2018, London and England excluding London

Image .csv .xlsThe mean weekly gross household income for private renters, according to the EHS for FYE 2017 was £696, higher than social renters’ income (£403), and lower than owner occupiers’ income (£884). The medians were £551, £326, and £720 respectively.

The distribution of net household annual income bands in England over the period FYE 2014 to FYE 2016 (FRS data) finds that the highest proportion of private renters (nearly one-fifth, 19%) fell in the over £40,000 band, compared with social renters who were more likely to fall into the £10,001-£15,000 band (26%). Almost half of those buying with a mortgage earned over £40,000 (44%), while this was one in five for those who owned outright (20%). Figure 16 shows the distribution in more detail.

Figure 16: Household income bands by tenure, FYE 2014 to FYE 2016, England

Source: Family Resources Survey, Department for Work and Pensions

Download this chart Figure 16: Household income bands by tenure, FYE 2014 to FYE 2016, England

Image .csv .xlsAccording to the EHS, in FYE 2017, just over one-fifth (22%) of private renters received housing benefit to help with rent payment. Of those that receive housing benefit, one-fifth (19%) report that this fully covers their rent. In comparison, approximately three-fifths (59%) of social renters received housing benefit in 2016 to 2017.

Since FYE 2009 the percentage of private renters receiving housing benefit has remained broadly unchanged (20% in FYE 2009, with a steady increase to 27% in FYE 2015 before falling to 22% in FYE 2017, as shown in Figure 17). These estimates differ to those presented for countries of Great Britain (31% for FYE 2008 to FYE 2010) as these are calculated from surveys rather than administrative sources such as Department for Work and Pensions (DWP). The reason survey data (such as the EHS) differ from DWP data is that surveys ask questions of the household reference person and in so doing might miss other household members in receipt of benefits. In contrast, as the DWP is the administrative source of data it has definitive information about all “benefit units”, that is, all people who receive benefits, and is therefore more complete.

The mean amount received per week for private renters in 2016 was £103 (£100 in FYE 2009, showing an unsteady increase over the years until it peaked in FYE 2016 at £111 then dropped slightly). For social renters this was £82 in FYE 2017, an increase from £62 in FYE 2009 which has steadily increased over the past eight years.

Figure 17: Percentage of private and social renters in receipt of housing benefit from FYE 2009 to FYE 2017, England

Source: English Housing Survey, Ministry of Housing , Communities, and Local Government

Download this chart Figure 17: Percentage of private and social renters in receipt of housing benefit from FYE 2009 to FYE 2017, England

Image .csv .xlsAlmost half of private renters said they find paying rent fairly easy (49%), with few saying it is very difficult (9%), 4% are currently in arrears, and 5% have been in arrears in the past year. Those in receipt of housing benefit (8%) were more likely to be in arrears than those not (3%) (EHS).

Just over one-third of private renters (36%) said they have savings or money invested, and of these approximately 70% had between £1,000 and £16,000 in savings. As would be expected (Figure 18), the oldest generations were more likely to have savings or money invested (50% of 65- to 74-year-olds, and 46% of under-75-year-olds). The least likely to have savings or money invested were 45- to 64-year-olds (30%).

Figure 18: Percentage of private renters with or without savings by age of household reference person, financial year ending 2017, England

Source: English Housing Survey, Ministry of Housing, Communities, and Local Government

Download this chart Figure 18: Percentage of private renters with or without savings by age of household reference person, financial year ending 2017, England

Image .csv .xlsIn terms of how much money each age group of private renters is saving, the highest proportion across all age groups had £5,000 to £16,000 in savings, however of those in the 45 to 64 years age group, 23% had savings of £50,000 and above.

Scotland

The proportion of household income (including housing benefit) that households in the private rented sector spent on their rent has remained relatively constant since FYE 2007, whilst the proportion for those owning with a mortgage dropped after FYE 2010. This is likely to be have been due to lower mortgage interest rates in more recent years. Across the three-year period from FYE 2014 to FYE 2016, privately rented households in Scotland spent 25% of their net household income on housing costs, a similar proportion to the social sector (24%). Those households owned with a mortgage spent 9% of their income on housing costs, whilst those owned outright spent 3% (Figure 19).

Figure 19: Median ratio of housing costs to net unequalised household income for the period FYE 2007 to FYE 2016 across tenures, Scotland

Source: Family Resources Survey, Department for Work and Pensions

Notes:

- Net income is defined here as the total income received (including housing benefit payments) by the households excluding taxes such as Income Tax and Council Tax. Net income has not been adjusted (“equivalised”) for family size. Housing costs include rent gross of Housing Benefit, as well as water rates and service charges where applicable.

Download this chart Figure 19: Median ratio of housing costs to net unequalised household income for the period FYE 2007 to FYE 2016 across tenures, Scotland

Image .csv .xlsAnalysis of the same data finds that 39% of private rented households spent more than 30% of their net household income on housing costs.

The median household weekly rent payment in the private rented sector in Scotland was £112, compared with £71 in the social rented sector, and mortgage repayments of £120 for owner occupiers (FRS FYE 2017).

The Private Sector Rent Statistics 2010 to 2017 report shows median monthly rent for two-bedroom properties (the most common property in the private rental sector) in Scotland in 2017 was £595 (mean £645). For three-bedroom properties (the second most common type) the median rent in 2017 was £700 (mean £787).

Private rental growth in Scotland weakened since mid-2015 but has started to strengthen again since 2017 (Figure 20).

Figure 20: Index of Private Housing Rental Prices percentage change over 12 months, January 2012 to December 2018, Great Britain and Scotland

Source: Index of Private Housing Rental Prices, Office for National Statistics

Notes:

- IPHRP is an experimental index tracking prices paid for renting property from private landlords in the UK.

Download this chart Figure 20: Index of Private Housing Rental Prices percentage change over 12 months, January 2012 to December 2018, Great Britain and Scotland

Image .csv .xlsFigure 21 shows the distribution of net household annual income across tenures, from the Scottish Household Survey (SHS) 2017. The highest proportion of private renters (30%) earned in the £10,001 to £20,000 category. A very small proportion of private renters earned over £60,000. Social renters had the highest proportion in the £10,001 to £20,000 category (49%). Owner occupier households are more likely to be at the higher end of the income spectrum than either private or social renters, with 17% of them earning over £50,001 (compared with 4% of private renters and 1% of social renters).

Figure 21: Household income bands by tenure, 2017, Scotland

Source: Scottish Household Survey, Scottish Government

Notes:

- The data period in the title for Figure 21 has been updated from 2016 to 2017.

Download this chart Figure 21: Household income bands by tenure, 2017, Scotland

Image .csv .xlsWales

Figure 22 shows the median ratio of housing costs as a proportion of net household income over the period FYE 2014 to FYE 2016 for each tenure category. Across the three-year period from FYE 2014 to FYE 2016, private rented households in Wales spent 29% of their net household income on housing costs, a similar proportion to the social sector (28%). These figures compare with equivalent figures of 9% for households owned with a mortgage and 3% for households owned outright.

The similar relative housing expenses between the privately rented sector and social households is likely to reflect those in the private rented sector having higher average rental costs but also having higher average income levels than those in social housing.

Figure 22: Median ratio housing costs to net unequivalised household income, FYE 2014 to FYE 2016, by tenure, Wales

Source: Family Resources Survey, Department for Work and Pensions

Notes:

- Net income is defined here as the total income received (including housing benefit payments) by the households excluding taxes such as income tax and council tax. Net income has not been adjusted (“equivalised”) for family size. Housing costs include rent gross of Housing Benefit, as well as water rates and service charges where applicable.

Download this chart Figure 22: Median ratio housing costs to net unequivalised household income, FYE 2014 to FYE 2016, by tenure, Wales

Image .csv .xlsThe FRS shows that in the private rented sector, the median weekly household expenditure in Wales (for FYE 2017) is £105, whereas for the social rented sector this is £84, and £115 for owner occupier mortgage repayments.

The latest Private sector rents data from the Welsh Government are from 2017. The median monthly rent in Wales for two-bedroom properties (the most common property in the private rental sector) is £500 (£525 mean), and £550 (£576 mean) for three-bedroom properties (the second most common).

Private rental growth in Wales has historically been below the rent of Great Britain but has strengthened in recent years (Figure 23).

Figure 23: Index of Private Housing Rental Prices percentage change over 12 months, Wales and Great Britain, January 2012 to December 2018

Source: Index of Private Housing Rental Prices, Office for National Statistics

Notes:

- IPHRP is an experimental index tracking prices paid for renting property from private landlords in the UK.

Download this chart Figure 23: Index of Private Housing Rental Prices percentage change over 12 months, Wales and Great Britain, January 2012 to December 2018

Image .csv .xlsThe distribution of household income bands in Wales over the period FYE 2014 to FYE 2016 (using FRS data) finds that highest proportion of private renters (20%) fell in the £10,001 to £15,000 band (Figure 24), while social renters were even more likely to fall into the £10,001 to £15,000 band (31%). For those who own outright incomes were more evenly distributed across the £10,000 to £40,000 plus income ranges. Those buying with a mortgage were more likely to earn over £40,000 (35%).

Figure 24: Household income band by tenure (FYE 2014 to FYE 2016), Wales

Source: Family Resources Survey, Department for Work and Pensions

Download this chart Figure 24: Household income band by tenure (FYE 2014 to FYE 2016), Wales

Image .csv .xlsJust over a quarter (27%) of private rented sector households were in the lowest income quintile for Wales, compared with 29% in the social rented sector, 23% for those who owned outright and 6% of those who owned with a mortgage.

Data from the National Survey for Wales FYE 2018, found that 22% of private renters received housing benefit, whereas for social housing renters this was 57%.

For the three-year period FYE 2015 to FYE 2017, 42% of privately rented households were in relative income poverty (household income below 60% of the UK median household income after housing costs are paid), compared with 48% in the social rented sector and 13% of owner occupiers (Households below average income data).

Northern Ireland

Family Resource Survey (FRS) data shows that in FYE 2017, median household weekly rent payments in the private rented sector for Northern Ireland (NI) were £97, in contrast to £77 in the social rented sector, and £110 for owner occupiers’ mortgage repayments. Mean weekly rent in the 2016 Private Tenant Survey (PTS) (PDF, 537KB) was £106 (up from £99 in 2012). According to the Performance of the Private Rental Market (PPRM) report 2017 (PDF, 465KB), average monthly rent across NI was £598 in latter half of 2017, a 0.5% increase on the previous half of the year (£595), and a 3.3% increase on the latter half of 2016 (£579). Over the full year, average rents rose by 4.4% in 2017 (£596) compared with 2016 (£571).

Private rental growth in Northern Ireland has historically been weaker than the UK but has strengthened since the end of 2017.

Figure 25: Index of Private Housing Rental Prices percentage change over 12 months, January 2016 to October 2018, UK and Northern Ireland

Source: Index of Private Housing Rental Prices, Office for National Statistics

Notes:

- IPHRP is an experimental index tracking prices paid for renting property from private landlords in the UK.

- Northern Ireland annual growth is only available from January 2016.

Download this chart Figure 25: Index of Private Housing Rental Prices percentage change over 12 months, January 2016 to October 2018, UK and Northern Ireland

Image .csv .xlsThe 2016 Northern Ireland House Condition Survey (NIHCS) reports that within the private rented tenants (and “others”) category, most private renters were in the £10,400 to £15,599 annual salary income band (29%), and the least were in the £46,800 or more income band (5%). Meanwhile social renters were predominantly in the lower two income categories (up to £15,599, 75%), and owner occupiers were more likely to be in the higher income categories (22% earning £20,800 to £31,199 and 19% earning £31,200 to £46,799). More owner occupiers were in the higher income bands, with social housing tenants showing the opposite trend. See Figure 26 for a further breakdown by income band.

A quarter of all households with an annual income of up to £10,399 were in the private rental sector, alongside just under a quarter (24%) of all households with an annual income of £15,600 to £20,799.

Figure 26: Household income band by tenure, 2016, Northern Ireland

Source: Northern Ireland House Condition Survey, Northern Ireland Housing Executive

Download this chart Figure 26: Household income band by tenure, 2016, Northern Ireland

Image .csv .xlsNI Housing Rights published a research briefing on affordability in the private rented sector in 2016 (PDF, 252KB), which demonstrated that low income households are motivated to rent privately due to location, less segregation, availability of fully furnished properties, and social housing stigma.

The NIHCS showed 42% of private rented households received housing benefit in 2016, broadly unchanged from 2011 (43%). This represents approximately 53,000 households in 2011 and around 57,000 in 2016.

Back to table of contents5. Household flows between tenure sectors

This section focuses on the time spent living in the private rented sector and the flows between the private rented sector, owner-occupied sector and social housing sector. Most of the data in this section comes from national surveys such as the English Housing Survey, Scottish Household Survey, National Survey for Wales and the Northern Ireland Private Tenants survey. Differences in survey design and context may affect comparability.

UK

According to the Family Resource Survey (FRS), sixty two percent of households in the private rented sector spent under three years in the same accommodation and only a small proportion (4%) had been in the same residence for more than 20 years (Figure 27).

Figure 27: Length of residency of head of household in private rented sector, FYE 2017, UK

Source: Family Resources Survey, Department for Work and Pensions

Download this chart Figure 27: Length of residency of head of household in private rented sector, FYE 2017, UK

Image .csv .xlsComparing across nations, 32% of private rented sector households in Scotland had been in their accommodation for less than 12 months, compared with 28% in Wales, 26% in England and 25% in Northern Ireland.

Households in the private rented sector in England and Scotland remained in their accommodation for an average (mean) of four years, compared to an average of five years for Wales and Northern Ireland.

England

Private renters have lived at their current address for an average (mean) of 3.9 years. The majority (90%) of household reference persons (HRP) in the private rented sector have been resident in their home for less than 10 years, and one-quarter (25%) have lived in their home for less than a year (Figure 28). This has fallen from five years ago where nearly one-third had lived at their current address for less than a year. In financial year ending (FYE) 2017, half (50%) of private renters had lived in the private rented sector for less than five years while 24% had been in the sector for five to nine years and 27% for 10 or more years.

Figure 28: Length of residence (years) of household reference person by tenure, FYE 2017, England

Source: English Housing Survey, Ministry of Housing, Communities, and Local Government

Download this chart Figure 28: Length of residence (years) of household reference person by tenure, FYE 2017, England

Image .csv .xlsThe average length of residence for tenants at their current address in the private rented sector differs according to age. Younger people (aged 16 to 24 years) have stayed in their current residence for a shorter amount of time, an average of 9.6 months. Older people (aged 75 years and over) on the other hand are more likely to have lived at their current private rented accommodation for an average of 17 years (Figure 29).

Figure 29: Length of residence in current home by age in private rented sector, FYE 2017, England

Source: English Housing Survey, Ministry of Housing, Communities, and Local Government

Download this chart Figure 29: Length of residence in current home by age in private rented sector, FYE 2017, England

Image .csv .xlsThere is greater churn within the private rented sector (that is, moving from one privately rented home to another) than between sectors (Figure 30). Over the past 10 years, movers within the private rented sector increased from 532,000 households in FYE 2007 to 860,000 in FYE 2017, an increase of 62%. Some of this increase may be due to an increase in the overall number of households in England which increased 6% between 2007 and 2017 from 21.3 million to 22.7 million.

In 2016 to 2017 there were 179,000 moves into the sector, of which 80% (143,000) were from owner occupation. Movement from owner-occupied housing to the private rented sector has been gradually decreasing over the past 10 years, falling from 177,000 households in 2006 to 2007. There were 266,000 moves out of the sector, with 68% (182,000) of these moving to owner-occupied accommodation.

Figure 30: Trends in previous tenure for movers within the private rented sector, FYE 2007 to FYE 2017, England

Source: English Housing Survey, Ministry of Housing, Communities, and Local Government

Download this chart Figure 30: Trends in previous tenure for movers within the private rented sector, FYE 2007 to FYE 2017, England

Image .csv .xlsOut of all private renters who have moved from a private rented home in the past year, the main reasons for moving were job-related reasons (16%) and wanting a larger house or flat (13%).

Young people (aged 16 to 24 years) were most likely to move for job related reasons or for neighbourhood related reasons (15% and 11% respectively), whereas those between 45 and 65 years were most likely to move because the landlord gave notice (16%), or because of divorce or separation (13%). For those with dependent children, the most prominent reason for moving was because the landlord gave notice (13%), followed by job-related reasons (11%).

Scotland

In 2017, over one-third (35%) of adults in private rented properties had lived at their current address for less than a year (Figure 31), equating to a total of 220,000 adults. More than half (55%) of these had moved from another private rented household, and 24% moved from a parental-family home, with lower proportions having moved from buying with a mortgage (8%), owning outright (5%), renting from a local authority (3%), renting from a housing association (2%), or being in another tenure (3%).

A further 32% of adults in the private rented sector had lived at their current address for one to two years with only 6% of private renters having lived at their current address for over 10 years.

In 2017, 6% of adults in owner occupier properties had lived at their address for less than one year, with around one-quarter of these coming from the private rented sector (26%). Approximately one in ten of social renters (9%) had lived at their current address for less than one year, with 22% of these having moved from the private rented sector.

Figure 31: Length of time at current address by tenure, Scotland

Source: Scottish Household Survey, Scottish Government

Download this chart Figure 31: Length of time at current address by tenure, Scotland

Image .csv .xlsAdults in households in the private rented sector spent the shortest time at their current address with an average (mean) of three years, which compares with 16 years for owner occupiers and 11 years for the social rented sector. The average length of time at current address for adults in private rented households shows a slight decrease between 1999 and 2017, however this is likely to reflect the change in the composition of the sector in terms of the growth in the number of properties in urban areas; households that generally have shorter lengths of stay on average compared with properties in small towns or rural areas. The average length of stay for adults living in private rented households in urban areas has been relatively steady between 1999 and 2017, with averages of two years being seen for most years.

Under one-third of households (30%) in the private rented sector don’t expect to move, while more than half (55%) expected to move within the next five years, higher than other tenures (Figure 32). In the owner occupier sector, 13% expect to move in the next five years and 16% of social renters expect to move in the next five years.

Figure 32: When private rented sector householders expect to move, Scotland

Source: Scottish Household Survey, Scottish Government

Download this chart Figure 32: When private rented sector householders expect to move, Scotland

Image .csv .xlsAround 10% of private rented households stated they were on a housing list for social sector housing and of these over half (56%) had been on a housing list for three years or fewer. A tenth had been on a housing list for more than 10 years. For the 10% of private rented households on a housing list, the main reason stated was because they could not afford current housing or would like cheaper housing (27%) (Scottish Household Survey 2017).

Wales

A third of those in the private rented sector have lived in their current address for fewer than 12 months (33%), while 7% have lived at their address for more than 10 years (Figure 33). Most of those in the owner-occupied sector have lived at their address for over 10 years (65%), with 5% living there fewer than 12 months. The social rented sector followed a similar pattern; whereby the highest share spent over a decade in their present accommodation (43%), while 10% had lived there under 12 months.

Figure 33: Length of residence at current address by tenure, Wales

Source: National Survey for Wales, Welsh Government

Download this chart Figure 33: Length of residence at current address by tenure, Wales

Image .csv .xlsThe 2014 to 2015 National Survey for Wales found that 57% of private renters came from rented accommodation previously. One-tenth owned their previous property on their own or jointly, and 2% came from a property owned by their partner. In the social housing sector nearly three-fifths (59%) rented privately previously.

Northern Ireland

The Private Tenants Survey (PTS) 2016 reports that 69% of private tenants moved into their current accommodation less than five years ago. Two-thirds (66%) of private tenants who had moved within the last five years were previously in private rented accommodation (up from 49% in 2006), 20% lived with family, 7% had a mortgage and 2% owned a property outright (Figure 34). Five percent moved from social rented housing (down from 14% in 2006). The most common reason for those who left behind a mortgage or owned property was that their previous partner lives there (44%).

Figure 34: Previous accommodation of private rented households, Northern Ireland

Source: Northern Ireland Private Tenants Survey 2016, Northern Ireland Housing Executive

Download this chart Figure 34: Previous accommodation of private rented households, Northern Ireland

Image .csv .xlsOf those who had moved within the past five years, the most common reason for private tenants leaving their previous home was wanting a larger property (13%), because their home was in a bad state of repair (11%), or they wanted to set up a home of their own (10%).

Ninety-one percent of private rented households expected to be able to stay in their property for as long as they wanted in 2012, this fell to 83% in 2016. The majority (86%) described their relationship with their landlord or letting agent as on good terms, with 4% on poor terms.

Regarding future intentions, the majority (64%) intended to stay in the private rented sector for the next five years, three-fifths of these (80%) intended to stay in their current property for the next five years. Of the 25% of households that did not intend or did not know whether they intended to stay in the private rented sector, 56% intended to buy their own home in the next five years, with 41% of these hoping to buy in between one and three years’ time.

Back to table of contents6. Characteristics and quality of dwellings

The condition and quality of dwellings are covered within national housing condition surveys. Housing standards are not assessed in the same way across the four countries and so many measures are not directly comparable. However, it is possible to compare some characteristics such as age, dwelling type, energy efficiency rating band and hazards to an extent. Some national standards which differ are summarised below;

England

Dwelling condition is examined using housing quality indicators such as the Decent Homes Standard (DHS) and evaluating damp and disrepair. Their safety is assessed using the Housing Health and Safety Rating System (HHSRS), electrical safety, working smoke alarms and carbon monoxide detectors. For a home to be classed as decent according to the DHS it must meet the statutory minimum standard for housing, provide a reasonable degree of thermal comfort (related to effective insulation and heating efficiency), be in a reasonable state of repair (fails if one or more key building components need replacing), and have reasonably modern facilities and services (based on factors such as age of kitchen, bathroom and so on).

Scotland

Scotland – the tolerable standard is a minimum standard for habitability introduced in the 1969 Housing (Scotland) Act, and later updated. The definition of tolerable includes characteristics such as the dwelling being structurally stable and free from damp, and having provision for lighting, ventilation and heating, electrical installations that are adequate and safe, and satisfactory insulation.

Private landlords are also required to comply with The Repairing Standard, whereby the property: must be wind and water-tight and fit for people to live in; structure and exterior must be in a reasonable state of repair and proper working order; installations for water, gas, electricity, sanitation, space heating and heating water must be in a reasonable state of repair and proper working order; furnishings provided by landlord must be capable of being used safely for their designated purpose; must have a satisfactory fire detection and warning in the event of a fire; and must have satisfactory provision for giving warning if carbon monoxide is present in a concentration hazardous to health. The Repairing Standard has a degree of overlap with elements that are required under the tolerable standard.

The Scottish Housing Quality Standard (SHQS) was introduced in 2004, and is one of the main ways that housing quality is measured in Scotland. Under the SHQS, Social landlords must make sure that their tenants' homes are in a good state of repair, energy efficient, healthy, safe and secure. Private owners and private landlords are currently under no obligation to bring their properties up to this standard. However the data is collected across all dwellings to allow comparison across the whole housing stock. It comprises 55 elements across these five areas and failure on just one of these 55 elements is enough to fail the entire standard.

Wales

There is no explicit tolerable standard for private rented homes as there is for social housing (Welsh Housing Quality Standard (WHQS)), but local authorities, under the Housing Act 2004, can assess housing conditions and improvement works as required under HHSRS. Dwelling condition is examined in this article using the WHCS for privately rented properties, which focuses predominantly on the HHSRS and Category 1 hazards.

Northern Ireland

To meet the Decent Homes Standard applicable to Northern Ireland, a dwelling must: meet the current minimum fitness standard for housing, be in a reasonable stage of repair, have reasonable modern facilities and services, and provide a reasonable degree of thermal comfort.

NI Decent Homes Standard are not comparable with that of England and Wales due to the different fitness standard applied.

UK

For comparisons across countries, 2016 surveys were used for England, Scotland, and Northern Ireland as this was the most recent data available for England and Northern Ireland and this year was available for Scotland. For Wales, the 2017 to 2018 Welsh Housing Conditions Survey was used as the data required for the comparisons were not collected in previous years.

Northern Ireland’s private rented sector has the newest dwelling stock in the UK with that built post-1980 at 38%, compared with 24% for Scotland and Wales and 25% for England. The oldest dwelling stock was in Wales with 43% built pre-1919 compared with 39% in Scotland, 35% in England and 12% in Northern Ireland (Figure 35).

Figure 35: Age of dwellings in the private rented sector, countries of the UK

Source: English Housing Survey financial year ending 2017, Ministry of Housing, Communities, and Local Government; Scottish House Condition Survey 2016, Scottish Government; Welsh Housing Conditions Survey 2017 to 2018, Welsh Government; Northern Ireland House Condition Survey 2016, Northern Ireland Housing Executive

Notes:

- Scotland figures relate to 1965 to 1982 and post-1982

Download this chart Figure 35: Age of dwellings in the private rented sector, countries of the UK

Image .csv .xlsRegarding types of dwelling, terraced houses made up the highest proportion of private rented sector dwellings for England (36%), Wales (47%) and Northern Ireland (44%), with detached houses being the lowest (6% in England; and 8% in Wales and Northern Ireland). The highest proportion of private rented dwellings in Scotland were flats (63%), with the lowest proportion being semi-detached houses (10%). It is important to note, however, that bungalows are not accounted for separately for Scotland data and so are recorded in the house categories.

Figure 36: Type of dwellings in the private rented sector for England, Scotland, Wales and Northern Ireland

Source: English Housing Survey financial year ending 2017, Ministry of Housing, Communities and Local Government; Scottish House Condition Survey 2016, Scottish Government; Welsh Housing Conditions Survey 2017 to 2018, Welsh Government; Northern Ireland House Condition Survey 2016, Northern Ireland Housing Executive

Notes:

- Bungalow numbers for Wales too low to estimate so percentages do not add up to 100.

- Bungalows cannot be separately identified for Scotland data and so these are included in the other house sub-categories.

Download this chart Figure 36: Type of dwellings in the private rented sector for England, Scotland, Wales and Northern Ireland

Image .csv .xlsStandard Assessment Procedure (SAP) is the approach used by the government to assess and compare the energy and environmental performance of dwellings. SAP ratings are divided into bands A to G. These are the bands used for Energy Performance Certificates (EPC). The highest values (that is, the highest levels of energy efficiency) are assigned to Band A and the lowest values are assigned to band G.

Northern Ireland had the highest percentage of dwellings within the A to C energy efficiency rating bands (43%), followed by Scotland (38%). England and Wales had the highest proportion of private rented dwellings in band D (49% and 54% respectively), according to SAP 2012. Very few (7% to 8%) were in the F to G bands for England, Scotland and Wales, with 1% of Northern Ireland’s private rented dwellings falling into these categories (Figure 37).Some caution is advised when interpreting estimates for Wales due to smaller sample sizes. Mean SAP 2012 rating in the private rented sector in England was 60.3, which was the same for Wales, while Scotland was slightly higher at 61.5 and Northern Ireland higher again at 65.3.

The differences in energy efficiency between the UK nations could be attributed, at least in part, to the age and or type of the dwelling stock, along with improvements to building standards over time: Wales has the oldest stock and the joint lowest average SAP rating; Northern Ireland has the newest stock and the highest average SAP rating.

Figure 37: Energy efficiency rating bands in the private rented sector for countries of the UK, 2016 to 2018

Source: English Housing Survey financial year ending 2017, Ministry of Housing, Communities, and Local Government; Scottish House Condition Survey 2016, Scottish Government; Welsh Housing Conditions Survey 2017 to 2018, Welsh Government; Northern Ireland House Condition Survey 2016, Northern Ireland Housing Executive

Download this chart Figure 37: Energy efficiency rating bands in the private rented sector for countries of the UK, 2016 to 2018

Image .csv .xlsThe Housing Health and Safety Rating System (HHSRS) is a risk-based evaluation tool to help local authorities identify and protect against potential risks and hazards to health and safety from any deficiencies identified in dwellings. It is used to determine whether residential premises are safe to live in, or whether a hazard exists that may cause harm to the health and safety of a potential occupant.

The System assesses 29 types of housing hazard and provides a rating for each one. Those which score highly on the scale (and are therefore the greatest risk) are called Category 1 hazards – if, after a local authority inspection, a dwelling contains a Category 1 hazard the local authority has a duty to take the appropriate enforcement action. Those that fall lower down the scale and pose a lesser risk are called Category 2 hazards.

In 2016, 85% of England’s private rented dwellings were free from Category 1 hazards compared with 76% for Wales. Although HHSRS is not formally adopted in Northern Ireland, in 2016, 91% of all dwellings were free from Category 1 hazards. Scotland does not have a comparable measure to HHSRS Category 1 hazards, although other measures of disrepair and quality are collected and monitored on, as covered in the Scotland section.

England

The highest portion of private rented sector dwellings were built prior to 1919 (35% or 1.7 million dwellings) while a quarter (25% or 1.2 million dwellings) of private rented sector homes were built after 1980. Compared with other tenures, private rented stock tends to be older, with 21% of owner occupier homes built before 1919 and 7% of social rented homes (4% local authority and 8% housing association).

Figure 38: Age of dwelling by tenure, financial year ending 2017, England

Source: English Housing Survey, Ministry of Housing, Communities, and Local Government

Download this chart Figure 38: Age of dwelling by tenure, financial year ending 2017, England

Image .csv .xlsIn financial year ending (FYE) 2017, flats were the most prevalent dwelling type in the private rented sector (37%). The proportion of purpose built, low rise flats (where the building is only a few stories tall and shorter than a high rise which is usually over 35 metres tall) in the private rented sector increased from 17% in 1996 to 23% in FYE 2017. Alongside the rise in newly built flats in the sector, there has been a drop in the proportion of converted flats (house or other large building which has been converted into flats), from 19% in 1996 to 11% in FYE 2017 (although the number of converted flats increased from 382,000 to 539,000 over this period). Semi-detached houses were most prevalent in the owner-occupied sector (31%), with high rise purpose-built flats the least common (1%). Purpose built low rise flats were the most widespread dwelling type in the housing association and local authority sectors (both 38%), with detached houses the least common (1% and less than 1% respectively).

Figure 39: Dwelling type by tenure, financial year ending 2017, England

Source: English Housing Survey, Ministry of Housing, Communities, and Local Government

Download this chart Figure 39: Dwelling type by tenure, financial year ending 2017, England

Image .csv .xlsFrom financial year ending (FYE) 2007 to FYE 2017, the percentage of non-decent homes fell across all the tenures. In the private rented sector, nearly half were non-decent in (FYE) 2007, which fell to 27% in FYE 2017. The private rented sector had the highest proportion of non-decent homes in FYE 2017 (27%), while owner-occupied and social rented stood at 20% and 13%.

Figure 40: Non-decent homes, by tenure, 2006 to financial year ending 2017, England

Source: English Housing Survey, Ministry of Housing, Communities, and Local Government

Download this chart Figure 40: Non-decent homes, by tenure, 2006 to financial year ending 2017, England

Image .csv .xlsBased on surveyor assessment, between 1996 and FYE 2017 there has been a decrease in the occurrence of damp in all tenures, but this was particularly notable in the private rented sector where the prevalence of damp fell from 26% to 8%. In FYE 2017, owner-occupied dwellings had lowest levels of damp at 2%, and social rented households stood at 6% for local authority and 4% for housing association properties in FYE 2017.

Disrepair, measured as basic repair costs in square metres (pounds per metre squared) fell between 1996 and FYE 2017 in the private rented sector from £69 per metre squared to £24 per metre squared. Despite this, levels of disrepair are still highest for the private rented stock compared to other tenures.

In FYE 2017, the average SAP 2012 rating of private rented accommodation was 60.3, similar to owner-occupied homes (60.7), but lower than social rented homes which were more energy efficient (67.3). This could be due to the private rented sector having an “older” housing stock which are normally less well insulated.

There has been a decrease in the proportion of private rented homes with the poorest energy efficiency since 1996, partly reflecting the growth of newer homes in the stock (Figure 41). In 1996, 39% of private rented homes were in energy efficiency ratio (EER) bands F or G, falling to 25% in (FYE) 2007 and falling again to 7% in FYE 2017. Since 1 April 2018 there has been a requirement for private rented homes to have a minimum energy performance rating of band E, which applies to most but not all domestic private rented sector properties in England and Wales (Department for Business, Energy, and Industrial Strategy). These regulations will be enforced by local authorities.

At the other end of the scale, in FYE 2017, around a quarter of private rented homes (27% or 1.3 million) had the highest EER bands of A to C, a similar proportion to owner-occupied homes (25%), but a much lower proportion compared with social rented homes (51%; Figure 42).

Figure 41: Energy efficiency ratio band for the private rented dwellings in England, 1996 to 2016

Source: 1996 and 2006: English House Condition Survey, Ministry of Housing, Communities, and Local Government, 2016: English Housing Survey, Ministry of Housing, Communities, and Local Government

Download this chart Figure 41: Energy efficiency ratio band for the private rented dwellings in England, 1996 to 2016

Image .csv .xls

Figure 42: Energy efficiency ratio band by tenure, financial year ending 2017, England

Source: English Housing Survey, Ministry of Housing, Communities, and Local Government

Download this chart Figure 42: Energy efficiency ratio band by tenure, financial year ending 2017, England

Image .csv .xlsScotland

Dwellings built pre-1919 are the most prevalent in the private rented sector, accounting for 41% of all dwellings (Figure 43). Newer builds, those built after 1982, account for 24% of private sector dwellings (Scottish House Condition Survey (SHCS), 2017).

In comparison, 20% of owner-occupied dwellings were built pre-1919 and 5% of social rented dwellings.

Figure 43: Age of dwelling by tenure, Scotland, 2017

Source: Scottish House Condition Survey additional analysis, Scottish Government

Download this chart Figure 43: Age of dwelling by tenure, Scotland, 2017

Image .csv .xlsMost tenants in the private rented sector live in a tenement or flat (61%), similar to the social rented sector (57%). Fifty-eight per cent (unrounded figure) of owner-occupiers live in detached or semi-detached houses, with just over one-fifth (22%) in flat (Figure 44).

Figure 44: Type of dwelling by tenure, Scotland, 2017

Source: Scottish House Condition Survey additional analysis, Scottish Government

Download this chart Figure 44: Type of dwelling by tenure, Scotland, 2017

Image .csv .xlsThe majority (79%) of private rented sector households are located in large urban areas or other urban areas. The rest reside in accessible or remote small towns, and accessible or remote rural locations. The growth of the private rented sector between 1999 and 2017 has largely been concentrated in urban areas. The increase in the private rented sector in these areas has equated to an increase of 200,000 households, from 80,000 households in 1999 to 280,000 households in 2017. This equates to nearly four-fifths (79%) of privately rented households living in urban areas in 2017 (Scottish Household Survey).