Table of contents

1. Introduction

The CPIH is a measure of UK consumer price inflation that includes owner occupiers’ housing costs (OOH). These are the costs of housing services associated with owning, maintaining and living in one’s own home. On 10 November 2016, the National Statistician published a statement, confirming the intention for CPIH to become our preferred measure of inflation from March 2017.

CPIH is currently being re-assessed by the UK Statistics Authority as a National Statistic; before CPIH becomes the preferred measure we are taking the opportunity to introduce improvements and revisions to the statistic, to ensure that it is of the highest quality.

The 2 changes that are being made to the index are to revise the CPIH weights to align the expenditure used in the calculation of the OOH weight with revised national accounts data published in the Blue Book 2016 and the inclusion of Council Tax. This article describes the background to the inclusion of these elements in CPIH; it then presents an analysis of the impact these have on the index.

When revising CPIH, it has been agreed that only the expenditure for OOH and Council Tax would be updated in line with the latest national accounts data published in Blue Book 2016 and no further revisions to other areas of CPIH would be taken on. This ensures that CPIH continues to be consistent with the current headline measure of inflation, the Consumer Prices Index (CPI), the only difference being the OOH and Council Tax series.

Back to table of contents2. Background

Council Tax

Council Tax is not currently included in CPI or CPIH. On 9 March 2016, following an opening consultation on the recommendations of the Johnson Review, the National Statistician stated in a letter to the chair of the UK Statistics Authority that Council Tax would be incorporated into CPIH. As it is a cost associated with owning, maintaining and living in one’s own home, it will not be included in CPI.1

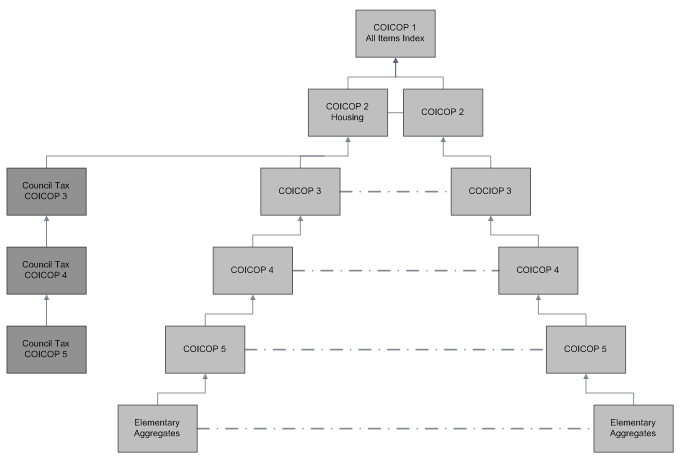

Items in the CPIH are categorised and aggregated using the Classification of Individual Consumption According to Purpose (COICOP). There are currently 4 COICOP levels and items within these levels are aggregated together using their expenditure as weights; COICOP 1 is the headline measure of inflation. In 2016, a new COICOP 5 class will be incorporated into CPI and CPIH. This is one of 2 changes that will be made to CPI and CPIH to ensure they are consistent with European best practice. More details of this can be found in the article Assessing the impact of methodological improvements on the Consumer Prices Index.

Following advice from the September Advisory Panels for Consumer Prices (APCP), it was agreed that Council Tax would be included in its own separate class for COICOP levels 5 to 3 and would then feed into COICOP 2: Housing. The index would then be calculated the normal way to produce the final CPIH index. Figure 1 illustrates how Council Tax will be incorporated into the COICOP structure. The Council Tax expenditure used to derive the weight is taken from Table 10.1 of the National Accounts Blue Book 2016.

Figure 1: COICOP structure including COICOP level 5 and Council tax

Source: Office for National Statistics

Download this image Figure 1: COICOP structure including COICOP level 5 and Council tax

.png (18.8 kB){kind=link}

Imputed rents

The OOH component of CPIH is calculated using a method called rental equivalence. This uses private rental data as a proxy for the cost of services associated with home ownership and asks the question: “How much would I have to pay in rent to live in a home like mine?” For more information on the methodology, please refer to our CPIH compendium.

The OOH component is aggregated with other items in the fixed basket of goods and services to form the headline CPIH. As with other items, expenditure weights are used to aggregate the indices and these are taken from the household final consumption expenditure (HHFCE) section of the National Accounts Blue Book publication. The expenditure of an item therefore determines how much that item contributes to CPIH and consequently how much of an impact changes to the price of an item will have on the overall headline measure.

In 2015, CPIH was revised back to 2005 to take on improvements to the private rental price series. At the same time it was identified that methodological improvements to the measurement of imputed rentals in National Accounts would be published in the 2016 Blue Book (BB2016). These improvements would considerably increase imputed rentals expenditure across all years of the series, so a decision was made to revise the OOH weight to reflect as far as possible the planned BB2016 changes. These revised weights were implemented alongside the revisions to the OOH price series.

The revised weights were based on best estimates at the time, calculated outside of the national accounts production system. Following the publication of the revised OOH weights in 2015, further improvements to the measurement of imputed rentals in national accounts were implemented. The final BB2016 expenditure proved to be lower than the estimates used in the OOH weights revision; it is this finalised BB2016 expenditure that will be used as the new weights for CPIH and revised back to 2005.

In addition to bringing the OOH weights in line with the updated imputed rentals expenditure, the previous calculation of weights was based on expenditure for the COICOP class 04.2.1 “Imputed rentals for owner occupiers”. This class, along with class 04.2.2 “other imputed rentals” forms the aggregate group 04.2 “Imputed rentals for housing”, with expenditure split roughly 95% to 5% in favour of class 04.2.1. We have reviewed the potential inclusion of class 04.2.2 in the calculation of OOH weights as “other imputed rentals” is made up of “owned secondary residences” and “households paying free or reduced rent”. There is a strong conceptual argument that both these components also represent owner occupiers’ costs and as such their expenditure should be included in the calculation of the OOH weight. Therefore the new weight for OOH will be based on the total expenditure for group 04.2 “imputed rentals for housing”.

Notes for Background section:

- Following advice from our Advisory Panels for Consumer Prices (APCP), it was additionally agreed that Council Tax would not be included in CPIHY, a measure of CPIH that measures underlying price movement by omitting taxes on consumption by omitting direct taxes.

3. Analysis

3.1 Overview

The following section presents analysis showing the impact of introducing Council Tax and revised imputed rents expenditure into CPIH. The effect of Council Tax alone is presented first, followed by the effect of revised OOH expenditure and finally the impact that both improvements together will have on the index. Please note that the analysis is based on best estimates produced outside of the CPIH production system. As such, there may be small differences to this analysis when the live data is published in March 2017.

When calculating CPIH, each class is allocated a weight, based on the expenditure spent on that class. This is used to determine the impact that price movements of items in that class have on the overall CPIH index. The total weights for all classes must be equal to 1,000. Therefore when weights for a particular class are increased or decreased, as is the case for imputed rents, minor adjustments are required to other classes to ensure that the total is still equal to 1,000.

Once new imputed rentals and Council Tax rates were applied, this rounding was applied to weights from 2005 to 2016 to ensure that weights for all years sum to 1,000.

3.2 Effect of Council Tax

Council Tax weights have been included for the period from 2005 to 2015 (Table 1). Weights for 2016 have been calculated and will be included in the live figures released in March 2017. The following analysis shows the impact of including just this component into CPIH, with no changes to OOH expenditure (so the OOH expenditure is based on the estimated expenditure introduced in early 2015).

Table 1: Estimated council tax weights based on current published CPIH

| 2005 to 2015 | ||||

| Part-per thousand | ||||

| Year | Estimated council tax weight | |||

| 2005 | 26 | |||

| 2006 | 26 | |||

| 2007 | 26 | |||

| 2008 | 26 | |||

| 2009 | 26 | |||

| 2010 | 26 | |||

| 2011 | 26 | |||

| 2012 | 25 | |||

| 2013 | 25 | |||

| 2014 | 25 | |||

| 2015 | 25 | |||

| Source: Office for National Statistics | ||||

| Notes: | ||||

| 1. All numbers are in part-per-thousand (ppt). | ||||

Download this table Table 1: Estimated council tax weights based on current published CPIH

.xls (24.6 kB)Figure 2: CPIH published and CPIH including Council Tax 12 month change 2005 to 2015

Source: Office for National Statistics

Download this image Figure 2: CPIH published and CPIH including Council Tax 12 month change 2005 to 2015

.png (35.1 kB) .xlsx (18.2 kB){kind=link}

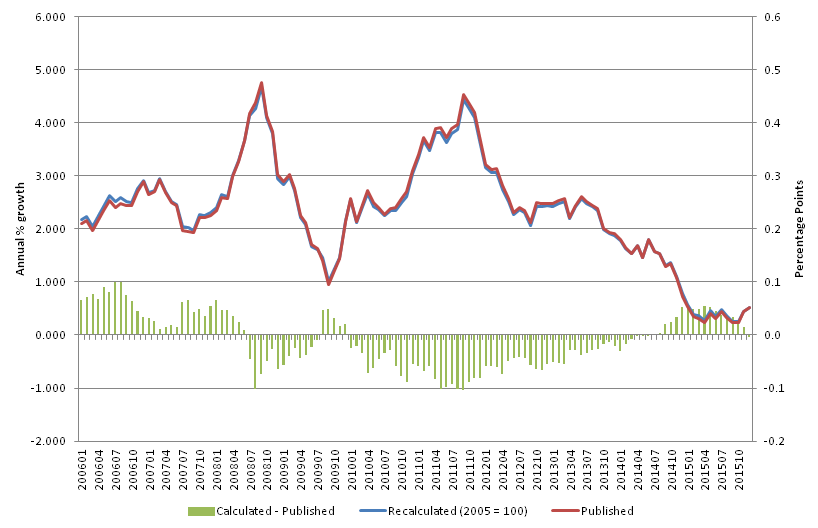

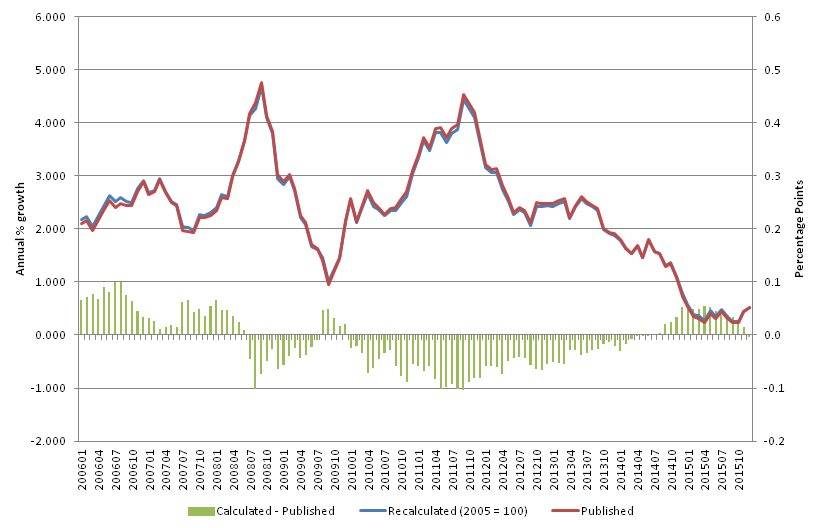

Figure 2 shows the likely impact that introducing Council Tax has on the 12 month growth rate for the CPIH headline measure to a one decimal place level of accuracy. The published series shows the current published CPIH index; the recalculated series shows the index when Council Tax is included. The new index follows the same underlying trend as the old, and the absolute magnitude of the deviations between the recalculated and published figures when rounded do not exceed 0.1 percentage points. The right hand scale shows the difference between the calculated and published index. Due to rounding procedures, the revisions would only have had an effect on the headline figure in certain months. With Council Tax included, CPIH would have differed in 51 months, with 33 of these being lower than the published figure. The average difference over the period when rounded was 0.0 percentage points.

Figure 3: CPIH published and CPIH including Council Tax index 2005 to 2015

Source: Office for National Statistics

Download this image Figure 3: CPIH published and CPIH including Council Tax index 2005 to 2015

.png (22.7 kB) .xlsx (18.4 kB){kind=link}

Figure 3 shows the cumulative impact on the index level from the inclusion of Council Tax. The right hand scale shows the difference between the calculated and published index. The largest impact on the index occurs in April 2008, with a difference of 0.186 index points. In December 2015, the cumulative difference between the indices is negative 0.126 index points, indicating that the inclusion of Council Tax has a minor impact on the index.

3.3 Effect of imputed rents expenditure revision

The revisions to CPIH weights, to incorporate new Blue Book 2016-consistent imputed rents expenditure and the “other imputed rents” class, are calculated back to 2005. To ensure consistency over time, the revised weights have been calculated as though they were run in real time, that is, following the standard process of price updating expenditure to the December of the previous year; this ensures that the CPIH time series and methodology is consistent across all components.

Table 2 shows the published and revised weights for imputed rents when the expenditure is updated.

Table 2: CPIH - Current published and revised owner-occupier housing (OOH) weights

| 2005 to 2015 | |||||

| Part-per thousand | |||||

| Current OOH weight | Estimated revised OOH weight | ||||

| 2005 | 195 | 196 | |||

| 2006 | 194 | 192 | |||

| 2007 | 197 | 186 | |||

| 2008 | 196 | 183 | |||

| 2009 | 184 | 181 | |||

| 2010 | 184 | 176 | |||

| 2011 | 184 | 175 | |||

| 2012 | 182 | 173 | |||

| 2013 | 179 | 171 | |||

| 2014 | 180 | 174 | |||

| 2015 | 178 | 174 | |||

| Source: Office for National Statistics | |||||

| Notes: | |||||

| 1. All numbers are in part-per-thousand (ppt). | |||||

Download this table Table 2: CPIH - Current published and revised owner-occupier housing (OOH) weights

.xls (24.6 kB)Figure 4: CPIH published and CPIH including revised OOH expenditure 12 month change 2005 to 2015

Source: Office for National Statistics

Download this image Figure 4: CPIH published and CPIH including revised OOH expenditure 12 month change 2005 to 2015

.png (33.7 kB) .xlsx (18.3 kB){kind=link}

Figure 4 shows that the absolute magnitude of the deviations between the recalculated and published figures does not exceed 0.04 percentage points. When rounding procedures are implemented, all months show a difference of 0.0 between the indices, indicating that the revisions have no effect. Before rounding is implemented the difference ranges between negative 0.04 and 0.04 percentage points.

Figure 5: CPIH published and CPIH including revised OOH expenditure index 2005 to 2015

Source: Office for National Statistics

Download this image Figure 5: CPIH published and CPIH including revised OOH expenditure index 2005 to 2015

.png (22.6 kB) .xlsx (18.4 kB){kind=link}

Similarly Figure 5 shows the cumulative impact on the CPIH index level from the change in the weights without accounting for the inclusion of Council Tax. The largest impact on the index occurs in February 2014 where the recalculated CPIH index was 0.036 index points higher than the published CPIH. In December 2015, the cumulative difference between the indices was 0.022 index points signifying a relatively small overall impact on the index figures.

3.4 Effect of Council Tax and OOH expenditure revision

The following analysis for the period 2005 to 2015 shows the likely impact of including both Council Tax and updated imputed rents expenditure in CPIH. The index shown here will be the one published when improvements are implemented in 2017 (subject to some potential minor changes due to rounding). To accommodate the new weights and in line with standard practice, minor adjustments were made to the weights of other classes as they were reapportioned to accommodate the changes.

Table 3 shows the published and revised weights for imputed rents when the expenditure is updated and Council Tax is included.

Table 3: CPIH - Current published and revised owner-occupier housing (OOH) weights including council tax

| 2005 to 2015 | |||||

| Part-per thousand | |||||

| Current OOH weight | Estimated revised OOH weight | Estimated council tax weight | |||

| 2005 | 195 | 191 | 26 | ||

| 2006 | 194 | 187 | 26 | ||

| 2007 | 197 | 181 | 26 | ||

| 2008 | 196 | 179 | 26 | ||

| 2009 | 184 | 176 | 26 | ||

| 2010 | 184 | 171 | 26 | ||

| 2011 | 184 | 170 | 27 | ||

| 2012 | 182 | 169 | 26 | ||

| 2013 | 179 | 167 | 25 | ||

| 2014 | 180 | 169 | 25 | ||

| 2015 | 178 | 170 | 26 | ||

| Source: Office for National Statistics | |||||

| Notes: | |||||

| 1. All numbers are in part-per-thousand (ppt). | |||||

Download this table Table 3: CPIH - Current published and revised owner-occupier housing (OOH) weights including council tax

.xls (25.1 kB)Figure 6 presents OOH weights between 2005 and 2015 after each change is implemented.

Figure 6: Effect on OOH weights of introducing Council Tax and imputed rent revisions

Source: Office for National Statistics

Download this chart Figure 6: Effect on OOH weights of introducing Council Tax and imputed rent revisions

Image .csv .xlsFigure 6 shows the weights for imputed rents over a 10-year period in parts per 1,000. The CPIH published series shows OOH weights in the current, published CPIH. The Council Tax series shows the weights over the same period once the adjustments have been made to include Council Tax. It can be seen that the trend is similar, but slightly lower. The updated expenditure series shows the effect on OOH weights once the updated expenditure has been implemented. The result is generally lower weights that follow a smoother trend than previously. The updated expenditure and Council Tax series shows OOH weights once Council Tax and the new imputed rents expenditure has been implemented; the smoothed effect of introducing updated expenditure remains, whilst the adjustments made for Council Tax lower it slightly.

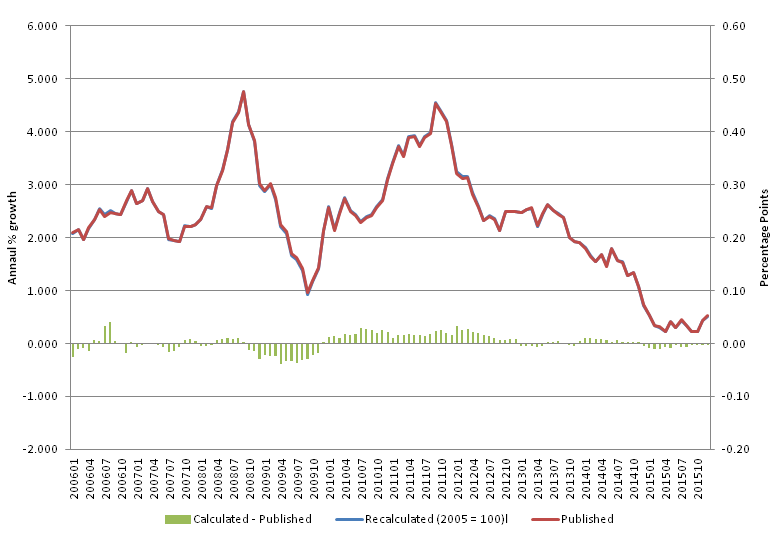

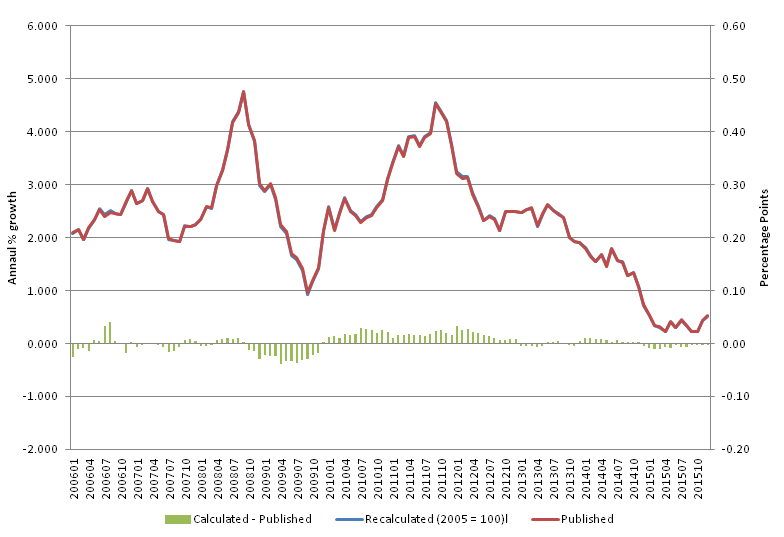

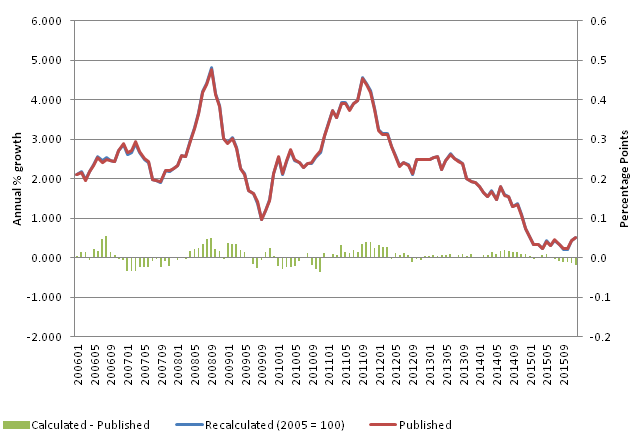

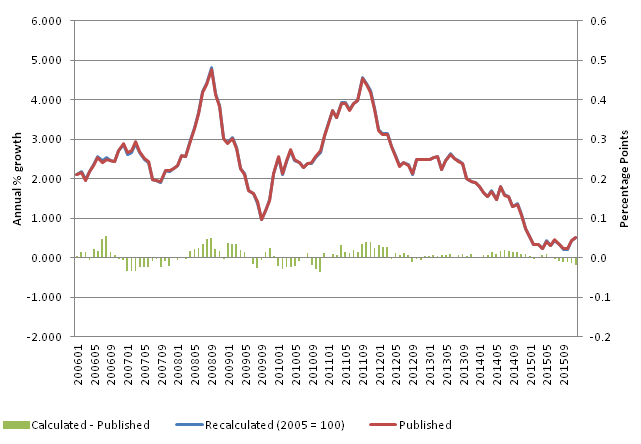

Figure 7: CPIH published and CPIH including Council Tax plus revised OOH expenditure 12 month change 2005 to 2015

Source: Office for National Statistics

Download this image Figure 7: CPIH published and CPIH including Council Tax plus revised OOH expenditure 12 month change 2005 to 2015

.png (27.3 kB) .xlsx (19.4 kB){kind=link}

Figure 7 shows the published CPIH annual growth against the revised CPIH including Council Tax and new imputed rents weights to a one decimal place level of accuracy. The right hand scale shows the difference between the 2 time series. A similar trend is followed and the absolute magnitude of the deviations between the recalculated and published CPIH does not exceed 0.1 percentage points. Due to rounding procedures, the revisions would only have had an effect on the headline figure in one month; in August 2006 the index would be 0.1 percentage points higher.

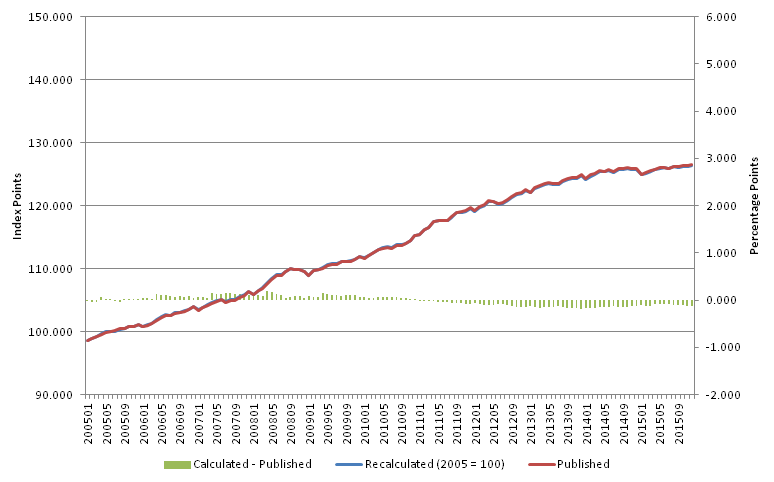

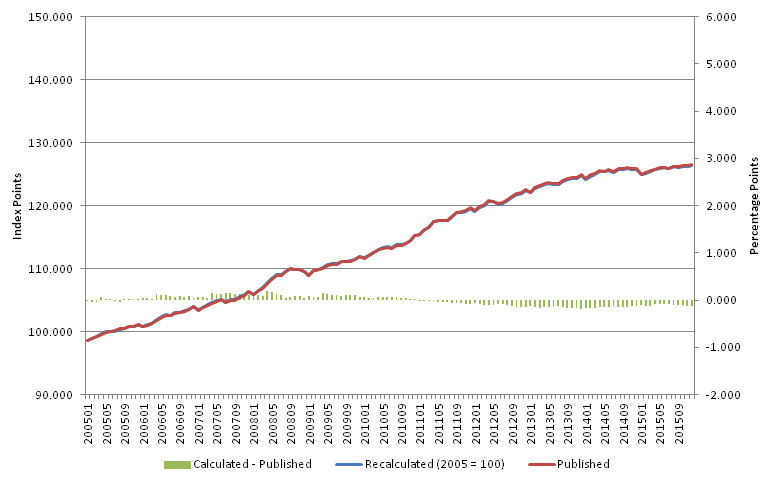

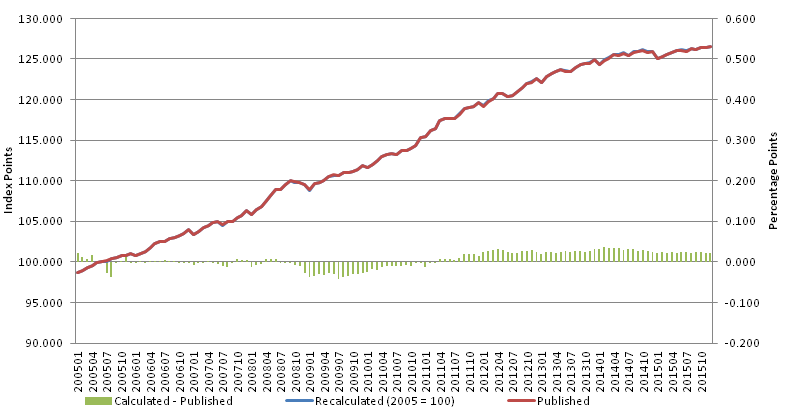

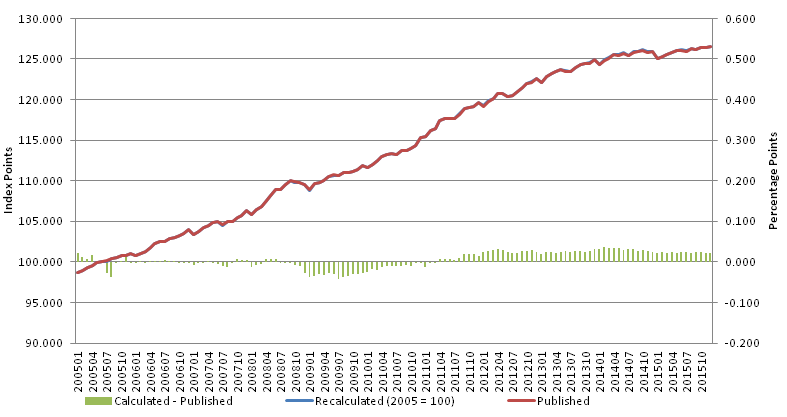

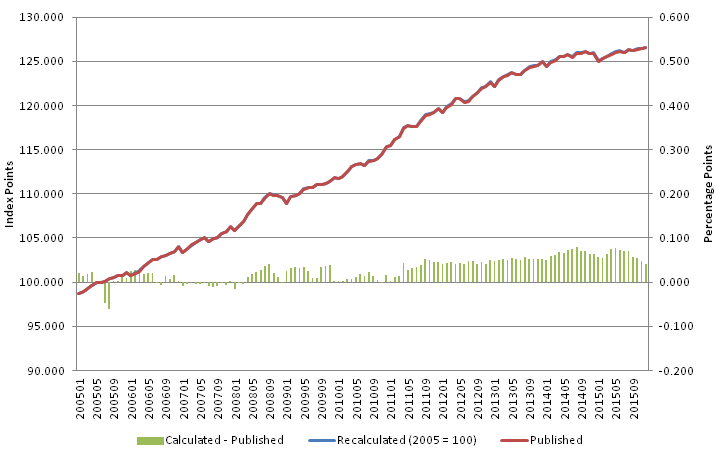

Figure 8: CPIH published and CPIH including Council Tax plus revised OOH expenditure index 2005 to 2015

Source: Office for National Statistics

Download this image Figure 8: CPIH published and CPIH including Council Tax plus revised OOH expenditure index 2005 to 2015

.png (23.4 kB) .xlsx (19.4 kB){kind=link}

Figure 8 shows the cumulative impact on the CPIH index level from the change in accounting for the revised expenditure and the inclusion of Council Tax. The right hand scale shows the difference between the 2 indices and indicates that the difference remained within the region of negative 0.1 and 0.1. The largest impact on the index occurs in August 2014, with a 0.079 percentage point difference. In December 2015, the cumulative difference was 0.042, indicating that the inclusion of Council Tax and revised OOH weights has a minimal impact on CPIH.

Back to table of contents4. Summary

The above analysis indicates that when revised imputed rent expenditure from the Blue Book 2016 and Council Tax are implemented into CPIH, there is a minimal impact on the index. Council Tax has the more noticeable impact, however, this is offset by the updated weights expenditure, highlighted by there being only one month between 2005 and 2015 where the index changed by 0.1 percentage points after rounding procedures have been implemented. This analysis may be subject to change once live data is published in March 2017.

Back to table of contents