1. Executive summary

Financial intermediaries (FIs) charge for their services explicitly via commissions and fees, as well as implicitly via an interest margin. The methodology used to calculate the FIs’ output charged implicitly financial intermediation services indirectly measured (FISIM) has frequently been the topic of detailed debate in international national accounts discussions.

The purpose of this article is to:

- explain the concept of FISIM methodology, its historic development and its treatment in the national accounts in the UK and internationally

- provide an overview of the international debate and to consider recent debate on what FISIM should represent and thus how it should be calculated

- examine experimental statistics on FISIM at current prices (nominal FISIM), adjusted for risk attributable to defaulting loans, the results of which may provide a possible way forward for the enhancement of FISIM calculations in the UK in the future

FISIM is calculated as the difference between the effective rates of interest payable and receivable, and a “reference” rate of interest. The reference rate should represent the pure cost of borrowing funds and is calculated based on lending or borrowing relationships between FIs.

Sections 3 and 4 of the article explain that the use of a reference rate that should best reflect the maturity structure in transacted deposits and loans is a matter of international debate. In the wake of the financial crisis, the approach of calculating the reference rate using interbank transactions, that are mainly short-term, resulted in rather surprising outcomes. This included the occurrence of negative FISIM on deposits and, especially notably, high volatility in FISIM allocated into gross domestic product (GDP) components. Two main camps were formed: one supporting the use of a single reference rate, and another supporting the use of multiple reference rates. However, none of the methods proposed was agreed by consensus of international experts, and hence the internationally accepted national accounting standards remained unchanged.

Section 5 of the article deals with the treatment of risks in the FISIM measure that has also been debated internationally. There are various types and degrees of risks that could be excluded from the interest margin used in the FISIM measure. Experts agreed that, among these, the exclusion of that part of the FISIM margin that compensates for expected losses on loans going into default could be a possible way forward. This method was implemented in the United States National Accounts, which encouraged the Office for National Statistics (ONS) and the Bank of England (BoE) to compile experimental statistics on UK FISIM adjusted for default risk.

The results of the experimental statistics on default risk adjusted FISIM for the UK National Accounts show that in the aftermath of the recent financial crisis, FISIM output adjusted for default risk would be reduced between 15% and 33% and the impact of FISIM on GDP would be reduced between 25% and 50%. FISIM increases the nominal GDP level by approximately 2%, so the default risk adjustment could reduce this impact of FISIM on nominal GDP level by up to 0.7 percentage points.

The current measure of FISIM in the UK National Accounts is fully compliant with international and European national accounting standards. Further experimental refinements of methods, sources and economic reasoning underpinning the measure of FISIM adjusted for default risk as described in this article will hopefully contribute to discussions leading up to the next updates of national accounting standards.

Back to table of contents2. Introduction

Financial services, in particular services provided by banks, have long been a challenging area for those who develop international statistical standards. National accounts methodologies for calculation and allocation of financial intermediation services indirectly measured (FISIM) have frequently been the topic of detailed debate internationally.

The measurement of output of a market producer is based on a price or fee for which its good or service is sold. In the case of financial intermediaries (FIs), they explicitly charge commissions and fees to their customers. This measurement creates no special problem for the statisticians responsible for the compilation of the national accounts.

However, FIs also provide services for which they implicitly charge via an interest margin. They pay lower rates of interest (interest payable) to those that lend them money and charge higher rates of interest (interest receivable) to those who borrow from them. In this situation, the national accounts must use an indirect measure, called FISIM, to measure their output and contribution to economic activity.

The national accounts methods to calculate and allocate FISIM, were discussed and tested in the European Union (EU) in the late 1990s, and were subsequently laid down in the FISIM Regulation 448/98. In the aftermath of the recent financial crisis, the European and International Task Forces on FISIM conducted further tests. As a result, in Europe, the FISIM method was defined in Chapter 14 of the European System of Accounts 2010 (ESA 2010). This specified in particular:

- FISIM is calculated as the difference between the effective rates of interest payable and receivable, and a “reference” rate of interest; this reference rate represents the pure cost of borrowing funds – that is, a rate from which the risk premium has been eliminated to the greatest extent possible, and that does not include any intermediation services

- that FISIM is calculated and allocated among user sectors using:

- internal reference rate: for allocating domestic FISIM; this is determined as the ratio of interest receivable on loans, to stocks of loans between FIs

- external reference rate: for calculating imports and exports of the FISIM; this is the average interbank rate weighted by the ratios of loans and deposits between resident FIs on the one hand, and non-resident FIs on the other hand

The purpose of allocating FISIM by institutional sectors is to identify the purchase of these services by the respective sectors. Hence, FISIM output is allocated to the intermediate consumption of enterprises (including non-market units), final consumption of households, general government, NPISH1 and exports. FISIM allocated to final consumption and net trade increases the level of gross domestic product (GDP).

The purpose of this article is to explain the international developments of the FISIM methodology in the national accounts and to examine experimental statistics on FISIM adjusted for default risk.

Section 3 explains the concept of FISIM methodology and development since the 1950s. It also elaborates on the treatment of FISIM in the UK National Accounts and internationally.

Section 4 provides an overview of the international debate. It also addresses the recent debate over what FISIM should represent and thus how it should be calculated.

Section 5 examines experimental statistics on FISIM adjusted for risk attributable to defaulting loans. The results may provide a possible way forward for the enhancement of FISIM in any future updates to national accounting standards.

FISIM in real terms is calculated by applying the FISIM margins of the base period to the deflated stocks of loans and deposits. The calculation of FISIM in real terms is not examined in this article.

Notes for: Introduction

- The non-market units belonging to the sectors of general government and non-profit institutions serving households (NPISH) make only intermediate consumption that increases their output. Their output is calculated as a sum of costs, where intermediate consumption of FISIM is one of the costs. By convention, the output calculated at cost must also be recorded as final consumption of general government or NPISH sectors, because they consume their own outputs.

3. The evolution of methods on FISIM

National statistical institutions (NSIs) compile national accounts estimates in line with the international and European national accounts manuals, namely the System of National Accounts (SNA) and the European System of Accounts (ESA). Of particular note, European countries are legally obliged to follow the ESA, which is defined in a Regulation of the European Council and the European Parliament.

3.1 History of FISIM in the international and European National Accounting standards

The measurement of financial intermediation services indirectly measured (FISIM) or implicitly measured financial intermediation1 was addressed in the very early versions of the SNA and ESA2. The history of FISIM in the international and in the European manuals on national accounts can be summarised as follows.

3.1.1 1953 SNA

1953 SNA (chapter v, section 2) stated that if the output of banks and financial intermediaries were evaluated in the same way as other enterprises, they would make a negligible or even negative contribution to gross domestic product (GDP). Therefore, the 1953 SNA acknowledged that financial services should include an implicit, as well as explicit, measure of output. It recommended that implicitly priced financial services should be measured as a margin between interest received on loans and interest payable on deposits.

3.1.2 1968 SNA and ESA 1970 and 1978

In these international and European manuals, FISIM output was calculated as a spread between interest receivable by financial intermediaries (FIs) on loans and other investments, and payable on deposits. The 1968 SNA and ESA 1970, in contrast to their predecessors, stressed that income generated by own funds should not be used in the calculation of FISIM output (1968 SNA paragraph 6.33 and ESA 1970 and 1978 paragraphs 3.10 and 3.16). The allocation of FISIM output was not yet developed, thus the manuals (1968 SNA paragraph 6.35 and ESA 1970 and 1978 paragraph 322.d) recommended that, by convention, FISIM output generated by FIs should be entirely absorbed by a nominal (special) unit and recorded as intermediate consumption – hence not affecting the total economy gross value added (GVA) and GDP.

3.1.3 1993 SNA and ESA 1995

Similarly, the 1993 SNA recommended a method to calculate FISIM output as the interest spread (interest receivable less payable) by FIs, excluding income generated from investing own funds. The 1993 SNA, contrary to its predecessors, permitted the inclusion of interest from debt securities (1993 SNA paragraph 6.125). The same method was adopted by the ESA 1995 (paragraph 3.63).

With respect to the allocation of FISIM output, the 1993 SNA acknowledged the practical difficulty in developing a method of allocating FISIM between different users that was conceptually satisfactory, represented the economic reality, and was feasible based on available source data. Hence, the SNA offered flexibility in approach by offering two methods of adoption:

1) To not allocate FISIM into user sectors, as in previous SNAs, but to treat FISIM output as absorbed by the intermediate consumption of a “nominal industry” (1993 SNA, paragraph 6.126). The ESA 1995, as originally published, adopted this method of not allocating FISIM output.

2) To fully allocate FISIM to the consumers of FISIM across relevant sectors and industries.

“The purpose of allocation of FISIM by sectors and industries is to identify the use of these services explicitly and to classify them as intermediate consumption, final consumption expenditure or exports according to which sector incurs the expenditure.” (SNA 93, Annex III, paragraph 5)

According to the Regulation 448/98 of the European Council and the European Parliament, which amended the ESA 1995, FISIM output should be allocated into sectors in the national accounts as follows:

- intermediate consumption for the intermediation services consumed by non-financial corporations, other financial corporations, general government, households as owners of dwellings, households as owners of unincorporated enterprises, and non-profit institutions serving households (NPISH)

- final consumption expenditure for the intermediation services consumed by households, general government, NPISH3

- exports for the intermediation services consumed by non-residents

Furthermore, FISIM generated by non-resident FIs (import of FISIM) should be allocated into intermediate and final consumption of domestic sectors, accordingly.

The impact of FISIM on GDP consists of FISIM allocated into final consumption expenditure and exports less imports.

In order to allocate FISIM by user, both the SNA and the amended ESA defined FISIM to be calculated as the difference between the effective rates of interest payable and receivable, and a “reference” rate of interest.

“This reference rate represents the pure cost of borrowing funds – that is, a rate from which the risk premium has been eliminated to the greatest extent possible, and that does not include any intermediation services.” (1993 SNA paragraph 6.128)

In other words, the reference rate defined by the 1993 SNA can be interpreted as a rate in the context of the user cost of funds that FIs need to pay in order to raise funds for their lending to business. The cost of funds is one of the most important input costs for FIs, where a lower cost will generate better returns (given that interest rates on borrowing remain broadly exchanged), and when funds are used for short and long-term loans to borrowers. The margin between the cost of funds and the interest rate charged to borrowers represents one of the main sources of profit for most FIs4.

Regulation 448/98 required calculating FISIM on loans and deposits only and the use of the following reference rates:

- internal reference rate for allocating domestic FISIM: determined as the ratio of interest receivable on loans to stocks of loans between FIs

- external reference rate for calculating imports and exports of FISIM: defined as the average interbank rate weighted by the ratios of loans and deposits between resident FIs and non-resident FIs

3.1.4 2008 SNA and ESA 2010

The 2008 SNA further revised the FISIM methodology by restricting its calculation to loans and deposits (reflecting the practice in Europe) excluding, notably, debt securities. In order to allocate FISIM output by user sector, it recommended that the reference rate should contain no service element and therefore better reflect both the risk and maturity structure of deposits and loans. It suggested that the prevailing rate for inter-bank borrowing and lending may be a suitable choice as a reference rate. However, it further acknowledged that different reference rates may be needed for each currency in which loans and deposits are denominated, especially when a non-resident FI is involved. Also, the 2008 SNA clearly stressed that the reference rate cannot be calculated as a simple average of the rates on loans or deposits, because there is no necessary equality between the level of loans and deposits. (2008 SNA, paragraph 6.166).

The ESA 2010 adopted the method required by Regulation 448/98. While remaining consistent with the 2008 SNA, it recommended that, by convention, inter-bank FISIM between resident FIs, and between resident FIs and non-resident FIs should not be calculated. (ESA2010, paragraph 14.04e)

3.1.5 FISIM according to 2008 SNA and ESA 2010

The foundations for calculating and allocating FISIM are based on the theory of users cost of money5. In this theory the user cost of capital assets can be interpreted as corresponding to the value of an asset at the time of its theoretical rental rate rt covering interest costs plus depreciation δt less increase in price of the asset πt. Therefore, the user cost rate (uct) can be expressed as follows:

Equation 1

This theory was originally developed for measuring services of fixed assets, thus when applying the user cost theory to the financial assets the depreciation components (δt and πt) could be omitted. Hence the user cost rate on financial assets becomes the risk-free rate:

Equation 2

FISIM is compiled from the perspective of the FIs6 generating this implicit service in relation to the user sectors7 and separately for loans and deposits. It is calculated as the difference between loan or deposit rates and the reference rate, where the latter represents the user cost rate (from which the risk premium has been eliminated).

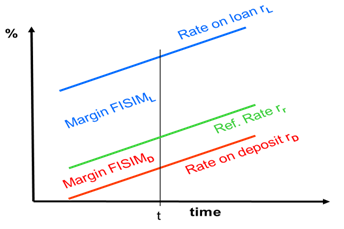

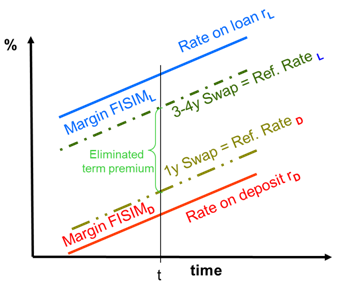

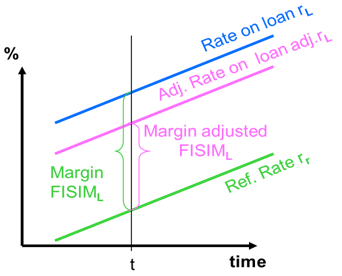

The calculation of FISIM for a given sector can be illustrated by Figure 1 and equation 6.

Figure 1: Illustration of FISIM margins based on a reference rate approach

(Linear evolution of rates is for illustration purposes only)

Source: Notional values

Download this image Figure 1: Illustration of FISIM margins based on a reference rate approach

.png (23.0 kB) .png (23.0 kB){kind=link}

Equation 3

Equation 4

where: SL – stock of loan

SD – stock of deposit

rL – rate on loan

rD – rate on deposit

rr – reference rate (corresponding to ut from equation2) , calculated based on interbank relationship as follows:

Equation 5

Hence the FISIM output for a given sector is given by equation 6:

Equation 6

To illustrate FISIM calculations, let us take an example of FISIM on loans and deposits:

A stock of loan is SL = £1,000:

- interest receivable by the FI rL= 9%

- reference rate rr = 4%

- FISIM on loan = (rr - rr)SL = (9% - 4%) x £1,000 = £50

A stock of deposit is SD £1,000:

- interest payable by the FI rD = 3%

- reference rate rr = 4%

- FISIM on deposit (rr - rD) SD = (4% - 3%) x £1,000 = £10

Total FISIM on loans and deposit = (rL - rr) SL + (rr - rD) SD = £60

3.2 History of compiling FISIM in the UK

3.2.1 Until mid-2008

Following international and European national accounting standards, FISIM output was calculated in the UK National Accounts as the difference between interest payable and interest received by FIs. The output of FISIM was not allocated between users, instead (by convention) it was treated as absorbed by the intermediate consumption of a special market producer unit classified in a “nominal sector”. In consequence, GDP was not affected by the size of FISIM output.

3.2.2 From mid-2008 until mid-2014

In the UK National Accounts, FISIM allocation between users was introduced in September 20088 (for the Blue Book9 2008). The calculation and allocation of FISIM used detailed sectorised data on stocks and interest receipts and payments for loans and deposits. The data were collected from various surveys but their degree of detail differed over time.

The calculation of nominal FISIM generated by UK monetary financial institutions (MFIs), that is banks and building societies, was, and still remains, the responsibility of the Bank of England (BoE). There were different data sources for two time periods:

- before 1999, detailed stocks data sourced from the BoE and interest data derived by the Office for National Statistics (ONS) from the effective interest rates used elsewhere in the national accounts

- from 1999, detailed data collected by the BoE from its own specially-designed surveys

For periods from 1999 onwards, allocation of MFIs’ FISIM by consumer sector was largely estimated from the sectoral breakdown reported in the BoE’s surveys. Banks and building societies directly provided information on the sectoral breakdown of stocks of loans and deposits and interest payments and receipts.

3.2.2.1 FISIM to resident consumer sectors

In the UK, it was recognised that the currency mix of interbank business was significantly different from that of the FISIM consuming sectors. Therefore, FISIM to resident consumer sectors was calculated separately for sterling and foreign currency.

The internal reference rates, for transactions denominated in sterling and foreign currency, used official interbank interest rates (for example, for FISIM on sterling loans and deposits Bank rate10 was used).

3.2.2.2 FISIM generated by UK “other financial intermediaries”

An additional calculation was made for FISIM on loans from UK “other financial intermediaries except insurance corporations and pension funds”. This was done by ONS, using FISIM margins (covering sterling only) supplied by the BoE and data on stocks of loans from “other financial intermediaries” based mainly on ONS surveys. The stocks data related to lending to individuals and thus all of the resulting FISIM was allocated to consumption by households. Within this, FISIM on loans secured on dwellings was allocated to intermediate consumption by households in their capacity as owner-occupiers of dwellings. FISIM from consumer credit was allocated to final consumption. There were separate FISIM margins and stocks series for each of these categories. The margins calculated by the BoE were based on the rates of return received by MFIs for sterling lending in the same categories.

Stocks data related to the closing levels for each quarter. The average of the current and previous quarters’ stock levels were therefore used to calculate the FISIM for a given quarter, as this represented the average level over that quarter.

3.2.2.3 FISIM with non-residents

The external reference rate should be used to calculate FISIM exports by FIs. This should be calculated as the ratio of accrued interest received on loans and paid on deposits between resident and non-resident FIs to the corresponding average stocks.

However, separate data for non-resident FIs were not available in the UK at that time. Therefore, the external reference rates for FISIM exports were calculated as the mid-rates between the calculated loan and deposit rates of return from the stocks and interest data.

Separate reference rates were calculated for sterling and foreign currency. The foreign currency reference rate was based on euro and US dollar official rates, weighted together according to the currency pattern of foreign currency loans to, and deposits from, non-residents.

There were also estimates of FISIM imports from non-resident FIs. These were calculated by ONS, using stocks obtained from the balance of payments statistics and fixed margins. The margins were estimated with reference to the margins earned by resident MFIs for domestically consumed and exported FISIM. Most FISIM imports were allocated to intermediate consumption by private non-financial corporations. The remainder were allocated to final consumption by households and intermediate consumption by insurance and pension corporations.

3.2.3 From mid-2014

In September 2014, the UK as well as the majority of other European countries were obliged to compile their national accounts according to the new standards (ESA 2010). Although the FISIM Regulation 448/98 was closely followed in the UK National Accounts, further improvements were necessary to fully align with the recommended FISIM methods to calculate the internal and the external reference rates. As a consequence of further improvements to source data, it was possible to improve the UK FISIM methods11 for calculating the internal and the external reference rates. These can be summarised as follows.

The internal reference rate in sterling is now calculated using accrued interest receivable in sterling on loans by MFIs divided by the corresponding average stock on loans. As part of the process a few outliers were identified and eliminated from the calculations, so that the internal reference rate is comparable and slightly above the LIBOR sterling 3 month rate. Similarly an internal reference rate in foreign currencies is calculated.

The external reference rate in sterling and foreign currency is the same as the internal reference rate. This approach differs from that defined in international standards, which indicates that the external rate should be the rate of return on non-resident interbank loans. Following analysis of results obtained using the recommended methodology, it was agreed with Eurostat that this was not an appropriate measure of UK MFIs’ non-resident funding costs, as it included not only significant intra-group business, but also intra-bank business reflecting London’s role as a major financial centre. The resulting FISIM data was thought to be implausible as persistent negative deposit FISIM was generated due to an artificially low reference rate12.

The new methods also eliminated inter-bank FISIM between resident FIs and non-resident FIs.

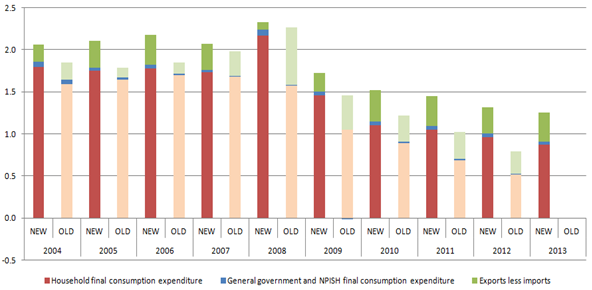

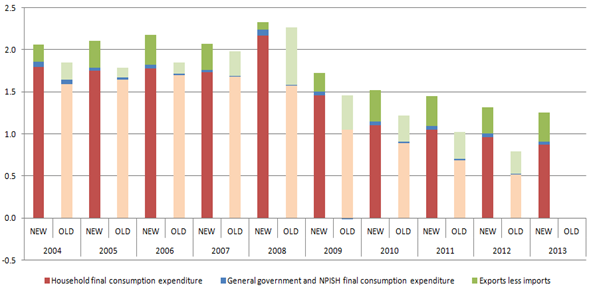

As a result of the new methods, continuous negative FISIM on deposits is much less of an issue. This had affected household final consumption expenditure in particular. The volatility of FISIM’s impact on GDP has also been reduced. As presented in Figure 2, GDP was revised slightly upwards, due to larger upward revisions to FISIM on deposits partly offset by downwards revisions to FISIM on loans.

Figure 2: FISIM effect on GDP after (NEW) and before (OLD) improvement of FISIM methods (in %)

Source: Calculations based on Office for National Statistics, Blue Book 2014 and Blue Book 2013

Download this image Figure 2: FISIM effect on GDP after (NEW) and before (OLD) improvement of FISIM methods (in %)

.png (38.7 kB) .xls (20.0 kB){kind=link}

Notes for: The evolution of methods on FISIM

The term “FISIM” was not introduced until 1993 SNA. Before then “imputed output of banks” was used.

Worldwide standards for national accounts can be traced back to 1947, when a Sub-Committee on National Income Statistics of the League of Nations Committee of Statistical Experts, under the leadership of Richard Stone, drafted the first report for international statistical standards. The aim of this report was to provide national accounting standards to compile and update comparable statistics in support of a large array of policy needs.

The first SNA was published in 1953. It was revised in 1960 and further revised in 1964, to improve consistency with the Balance of Payments Manual.

The next edition of SNA was published in 1968, when the manual was substantially expanded, mainly to include input-output accounts and balance sheets.

In 1993, the SNA was further developed and harmonised with other international statistical standards to a greater extent than earlier versions. For example, the harmonisation process has been particularly effective in respect of balance of payments statistics, government finance statistics and money and banking statistics, for which the IMF has responsibility.

The 2008 SNA took into account changes in the economic environment and advances in methodological research – and, in particular, placed a clear emphasis on the needs of users.

The European national accounting standards (the European System of Accounts - ESA) were developed in parallel to, and published shortly after, the SNA. Whereas SNA has a global focus, the purpose of ESA was to better reflect European requirements. The corresponding ESA manuals were as follows:

1968 SNA – published in ESA 1970 and further revised in 1978

1993 SNA - published in ESA 1995

2008 SNA - published in ESA 2010The non-market units belonging to the sectors of general government and non-profit institutions serving households (NPISH) make only intermediate consumption that increases their output. Their output is calculated as a sum of costs, where intermediate consumption of FISIM is one of the costs. By convention, the output calculated at cost must also be recorded as final consumption of general government or NPISH sectors, because they consume their own outputs.

Barnett W.A. (1978)

Barnet W.A. (1978), Fixler D., Fixler D., Reinsdorf M., Smith G.,(2008), and Hood K.K. (2010)

Financial intermediaries (FIs) generating this implicit service (FISIM) consist of deposit-taking monetary financial institution, and other financial intermediaries like special credit and mortgage lenders.

User sectors of FISIM consist of non-financial corporations, other financial corporations (other than FIs generating the implicit service), general government, households, non-profit institutions serving households, and rest of the world.

Akritidis L. (2007)

The Blue Book is an important annual publication of the Office for National Statistics on national accounts statistics and the essential data source for users concerned with macroeconomic policies and studies.

The Bank rate is the official UK central bank rate.

Bowers L., Farrell K. (2014) and Grovell K. Wisniewski D. (2014).

It should be noted that work on developing an appropriate external reference rate is in progress.

4. International debate on calculating and allocating FISIM

4.1 Restricting the calculation of FISIM to deposits and loans

The 2008 System of National Accounts (SNA) restricted the calculation of financial intermediation services indirectly measured (FISIM) to loans and deposits only. The same approach was adopted in the European System of Accounts (ESA) 2010, chapter 14. The restriction to loans and deposits was determined by the following arguments:

- the banks control the interest rates of loans and deposits only, and do not control the interest rates of other financial instruments, such as bonds and other securities1

- interest rates on loans and deposits are easily identifiable with a clear distinction of interest rate charged on loans (being higher) and on deposits (being lower); this distinction is very important because the calculation method of FISIM allocation is based on the difference between the effective interest rate and reference rate (representing the pure cost of borrowing funds) – this distinction is not very clear for bonds or other securities

- in some cases, the calculation of FISIM on bonds resulted in negative FISIM margins; this is because the reference rate is not always lower than the effective interest rate received on bonds2 – for example, sometimes banks hold treasury bonds issued some years ago with very low interest rates

It was further argued that financial services are generated in connection to financial assets and liabilities, where the service providers (banks) are in direct contact with their customers and hence such implicit services are applicable to deposits and loans. Most loans involve risk management, monitoring and advice, thus are not a passive provision of finance as in the case of bonds. Furthermore, if a bank purchases a bond on the open market, the bank does not generate services for the bond’s issuers3.

It should be stressed that the inclusion of other securities, such as bonds, into the calculation of FISIM allocation, might lower the value of FISIM, and in some cases lead to negative FISIM margins. This concept was tested by various EU countries4. The results showed that the difference in calculating FISIM allocation including and excluding securities is negligible. This served to prove that there is not much service element indirectly measured in other financial instruments provided by financial intermediaries (FIs). In many cases, for example, trading companies (such as undertakings for collective investment in transferable securities – UCITS) involved in trading securities do not even have employees.

Similar evidence was provided by the US Bureau of Economic Analysis (BEA) – that with the introduction of 2008 SNA it had to remove services generated on bonds from the measure of FISIM. BEA confirmed that the impact of this restriction of FISIM to loans and deposits was marginal5.

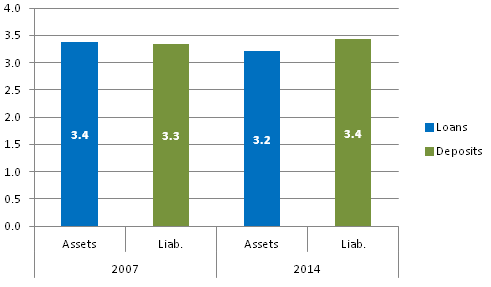

It is also evident that deposits are a stable and reliable source of funding for banks’ lending. In the aftermath of the financial crisis, the interbank market did not work well enough and thus raising funds on the interbank market became increasingly difficult. As a result, banks had to increase their efforts to attract depositors increasing their importance as a source of financing their business.

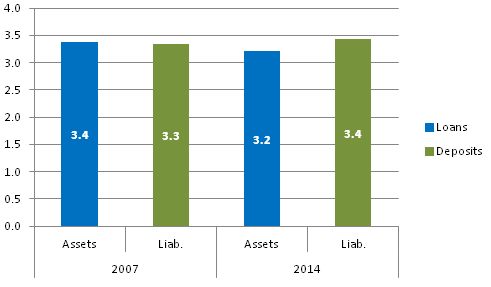

In the wake of the recent financial crisis in September 2008, banks became more reliant on deposits for fundraising, on which a bank paid little or no interest at all6. The balance sheets of UK FIs showed that levels of deposits increased in the post-crisis periods. For example, stocks of deposits with UK monetary financial institutions (MFIs) increased slightly from £3.3 trillion in 2007 to £3.4 trillion in 2014, while stocks of loans granted by UK MFIs decreased from £3.4 trillion in 2007 to £3.2 trillion in 20147 (see Figure 3). Although MFIs do not entirely finance their loans from deposits (MFIs raise additional funds from the inter-bank market), they are their most stable and increasingly important source of funding.

Figure 3: UK MFIs balance sheets excluding domestic inter-MFIs positions (in £ trillion)

Source: Calculations based on Office for National Statistics, Blue Book 2015

Download this image Figure 3: UK MFIs balance sheets excluding domestic inter-MFIs positions (in £ trillion)

.png (7.0 kB) .xls (18.4 kB){kind=link}

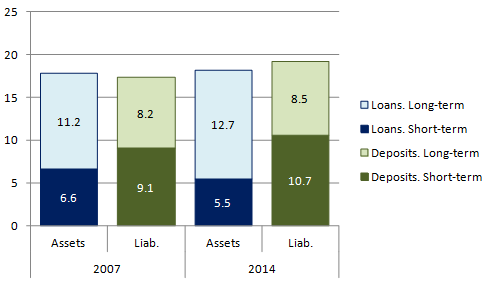

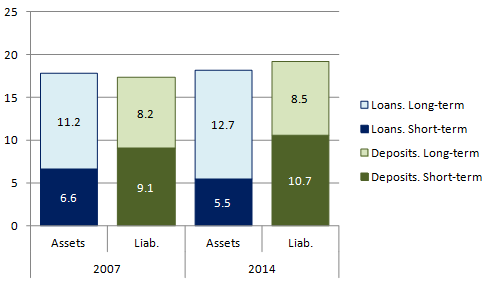

Similar evidence can also be found in the European Union market, where the deposit liabilities of the European Union’s MFIs increased by €1.9 trillion, while their stocks of loans increased proportionally less by €0.4 trillion between 2007 and 2014 (see Figure 4). Figure 4 also shows evidence of channelling of funds and maturity transformation of short-term deposits into long-term loans that are inherent functions of the FIs. It is worthwhile noting that the proportion of short-term deposits and long-term loans increased in the aftermath of the financial crisis.

Figure 4: European Union MFIs balance sheets excluding domestic inter-MFIs positions1 (in € trillion)

Source: Calculations based on Eurobase, Eurostat

Notes:

- Short-term deposits were assumed to correspond to transferable deposits, which largely consist of sight deposits. Long-term deposits were assumed to correspond to non-transferable deposits, which largely consist of time-deposits.

Download this image Figure 4: European Union MFIs balance sheets excluding domestic inter-MFIs positions^1^ (in € trillion)

.png (10.8 kB) .xls (18.9 kB){kind=link}

4.2 Reflecting maturity structure of loans and deposits in the measure of FISIM

In the wake of the financial crisis, the approach of measuring FISIM using interbank transactions (see equation 6 in section 3.1.5), that are mainly short-term, resulted in rather surprising outcomes. This included the occurrence of negative FISIM on deposits and, especially notably, high volatility in FISIM allocated into gross domestic product (GDP) components.

FISIM measures the financial services provided on both short-term as well as long-term loans and deposits. Hence, it was argued that the coverage of the (internal and external) reference rates could be expanded to also reflect not only the short-term but also long-term operations.

Two main camps were formed promoting the above argument and supporting the use of either a single reference rate or multiple reference rates. In theory the new reference rate or rates would also better reflect maturity transformation in the measure of FISIM, especially in the aftermath of the recent financial crisis.

4.2.1 The story behind the FISIM surge in the aftermath of the crisis

The recent financial crisis that started around 2008 and the subsequent failure of Northern Rock spread fear on the interbank market of further possible contagion. This resulted in commercial banks becoming very cautious in entering the interbank market to provide funds. Hence, the availability and access to funds from the interbank market was significantly reduced. This was mainly due to a loss of confidence and trust between banks. This had a big impact on the behaviour of interest rates, and interbank rates in particular.

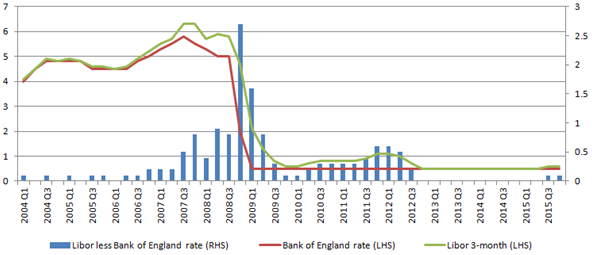

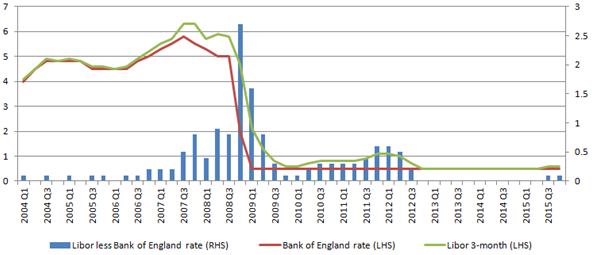

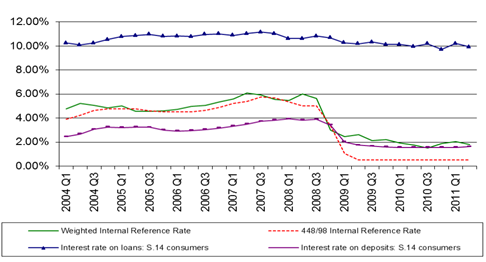

This is best illustrated by Figure 5 which shows the effect of liquidity dry-up of the interbank market on interest rates, with significant differences between the Bank of England's Bank rate and the Libor rate. The Libor is a rate at which commercial banks lend to one another, whereas the Bank rate (amongst other functions) seeks to stimulate money or funds supply, for example, lowering of the rate should also lead to reducing costs of funds rising on the interbank market.

However, the evidence from the financial crisis paints a different picture from this. Due to a lack of trust and confidence in the market by lenders, the availability of funds on the interbank market was severely rationed. Unless borrowers were willing to pay a higher than normal margin above Bank rate that incorporated a significant premium to reflect prevailing conditions of the market it was almost impossible to access funds on the market. One observes a much higher spread between the Libor and Bank rate during the period, in particular in Quarter 4 (Oct to Dec) 2008 and Quarter 1 (Jan to Mar) 2009.

Figure 5: Bank rate and Libor 3 month rate (in % on left hand side scale – LHS) and differences in % on the right hand side scale (RHS)

Source: Bank of England and British Bankers' Association

Download this image Figure 5: Bank rate and Libor 3 month rate (in % on left hand side scale – LHS) and differences in % on the right hand side scale (RHS)

.png (53.6 kB) .xls (22.0 kB){kind=link}

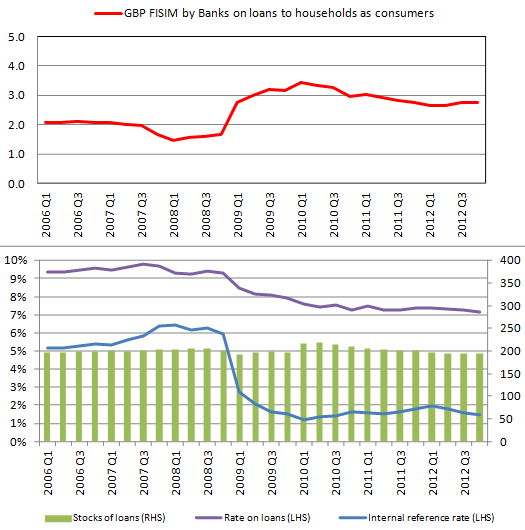

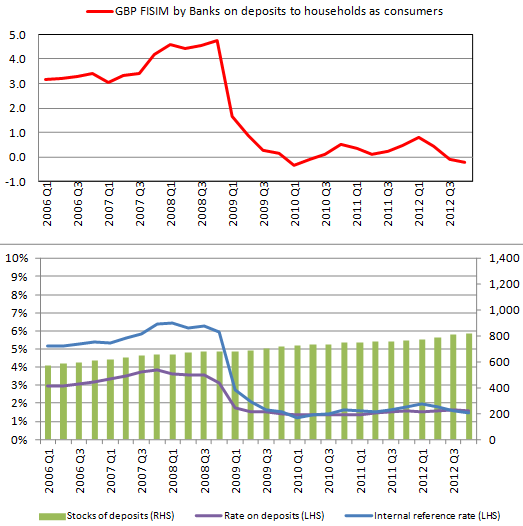

Figure 6 illustrates FISIM in pounds sterling (GBP) on consumers’ loans that increased sharply in Quarter 1 2009 and remained at a high level.

In late 2008, the interbank market rates were significantly reduced, which is reflected in the reference rate (blue line) used in the FISIM calculation. However, the rate that banks charge their customers (households) on consumer loans (purple line) did not immediately realign with the reference rate, instead it decreased slowly compared with the movement in the reference rate. This resulted in a sharp increase in the FISIM margin on loans (difference between blue and purple lines), that when applied to a rather stable stock of loans (green bars), generated an unprecedented surge in FISIM allocated to households as consumers.

Figure 6: GBP FISIM by Banks on loans allocated to households as consumers (in £ billion)

Source: Bank of England

Download this image Figure 6: GBP FISIM by Banks on loans allocated to households as consumers (in £ billion)

.png (27.6 kB) .xls (20.5 kB){kind=link}

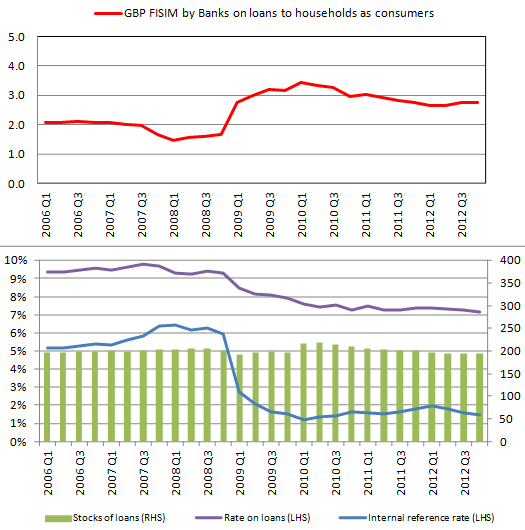

In contrast to FISIM on consumer loans, the revision to FISIM generated on consumer deposits was the opposite (Figure 7). In line with the reduction of the reference rate (blue line), the rate on deposits that banks pay to their customers (households) on consumer deposits (purple line) was also reduced to its record low level. This resulted in a sharp decrease in the FISIM margin on deposits (difference between blue and purple lines), that when applied to a rather stable stock of deposits (green bars) generated an unprecedented reduction in FISIM on consumers’ deposits.

The theoretical implication of the implicit service on consumers’ deposits may be disputed. In this section, we argue that banks dedicated a lot of human resources and engaged in developing new technologies (like e-banking) to retain existing depositors and attract new depositors as one of the most stable sources of financing their lending business. Hence, there must be significant amounts of FISIM on deposits, which unfortunately are not reflected by the current FISIM method.

Figure 7: FISIM by Banks on deposits allocated to households as consumers (in £ billion)

Source: Bank of England

Download this image Figure 7: FISIM by Banks on deposits allocated to households as consumers (in £ billion)

.png (31.3 kB) .xls (20.5 kB){kind=link}

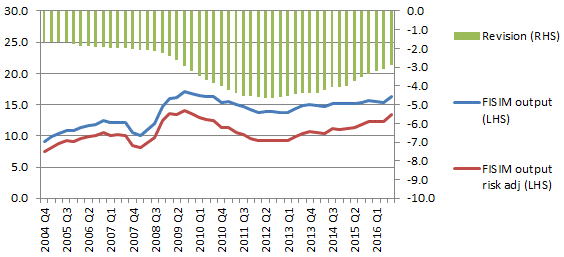

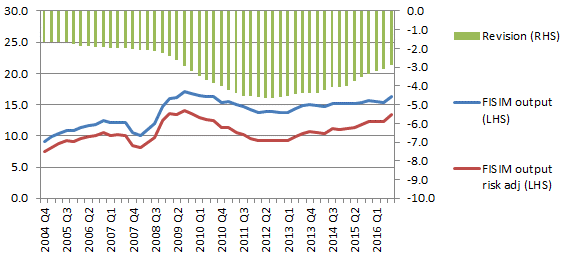

Households, as consumers, are largely deposit givers, thus FISIM on deposits determined the evolution of their FISIM on deposits and loans, which significantly reduced in the aftermath of the financial crisis impacting the level of GDP (see Figure 8).

Figure 8: GBP FISIM by Banks on deposits and loans allocated to households as consumers (in £ billion)

Source: Bank of England

Download this chart Figure 8: GBP FISIM by Banks on deposits and loans allocated to households as consumers (in £ billion)

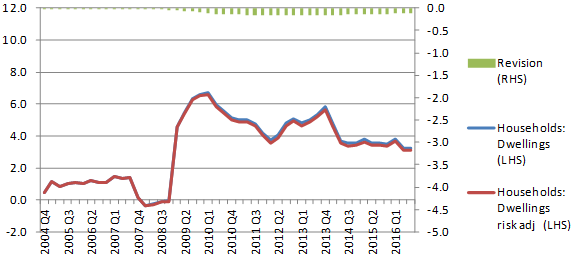

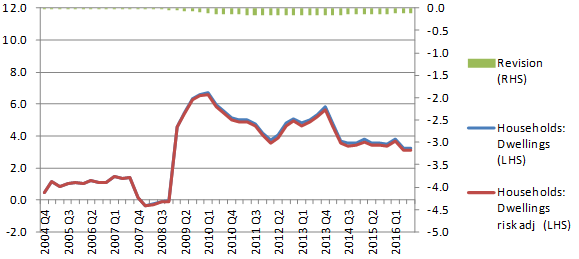

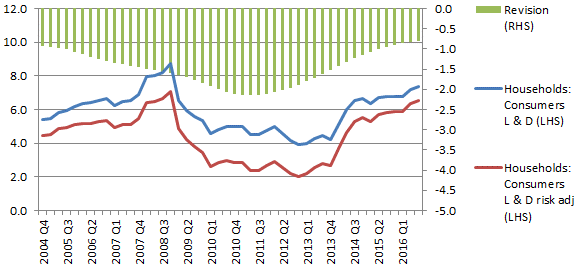

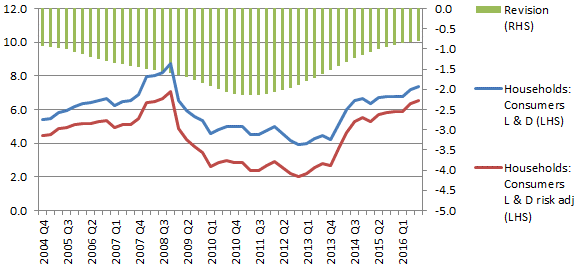

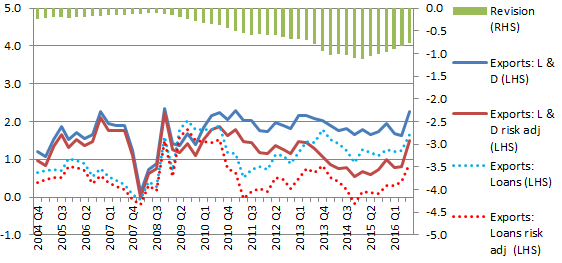

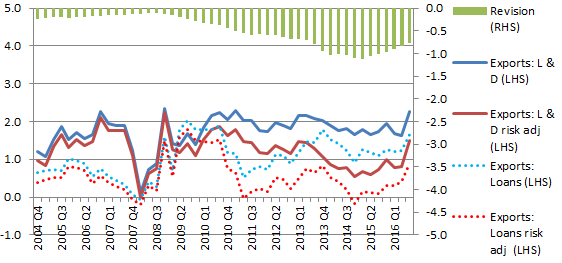

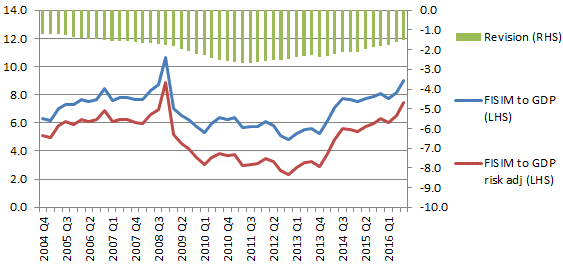

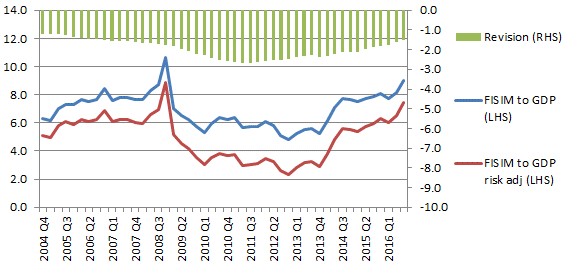

Image .csv .xlsIt is worthwhile noting that a very similar development of FISIM on loans by households as consumers was observed on FISIM on dwelling loans, which generated increased levels in Quarter 1 2009 and remained at a high level. FISIM on dwelling loans (see Figure 19) determined the sharp increase of the total FISIM output on loans and deposits (see Figure 17) in the aftermath of the recent financial crisis.

4.2.2 Single reference rate approach

When it came to establishing the most appropriate reference rate to use, two camps were formed. The first camp supported the use of an augmented single reference rate (that would reflect short- and long-term operations) to calculate and allocate FISIM. The rate would fit between the implied rate charged by FIs on loans and the implied rate paid by FIs on deposits. Hence, the level of this augmented reference rate was higher than the reference rate currently in use, which represents only short-term interbank operations.

The use of a single reference rate incorporates matching benefits and term premium (concepts that reflect maturity transformation) in the measure of FISIM. The channelling of funds from lenders (for example, deposit givers) to borrowers (for example, loan takers) is a fundamental function of banks. Households and businesses (deposit givers) prefer their deposits with short maturities giving them instantaneous access to highly liquid assets. However, they prefer receiving loans with long maturities when they are the debtor. Hence, banks, in order to accommodate their customers’ preferences, finance less liquid long-term loans using highly liquid short-term liabilities that must continually be rolled over or replaced8. Hence, maturity transformation is inherent to banks and FIs alike.

A number of attempts were made to calculate the single reference rate, alternative to the reference rate proposed by the European Commission (see equation 3 in section 3.1.5).

Diewert (2014) proposed a method of calculating a reference rate that represents the user cost of funds from the perspective of a non-financial firm. The reference rate is calculated by decomposing the FIs’ gross operating surplus into: pure profits, value of non-financial capital services, user cost of holding deposits less net margins earned by the firm on its financial investments, cost of rising financial capital (by issuing debt securities and equities) relative to raising the same amount of capital at a reference rate. This reference rate is expected to lie between rate on debt and rate on equity. “A natural choice for the reference rate is the average cost of raising financial capital from debt and equity financing” calculated as ratio of interest on debt and equity divided by the corresponding stock9.

Zieschang (2013) proposed a similar method of calculating a reference rate based on cost of funds approach calculated from the perspective of FIs. The reference rate represents an average return that the FI pays to the holders of all its liabilities. The reference rate is calculated using: directly available data from FIs’ income statements (profit and loss) and balance sheets, derived security equivalent returns on deposit liabilities.10

A number of countries suggested using a government debt security rate as a reference rate, which in “portfolio theory” is considered a risk-free rate and hence meeting the requirement of the SNA or ESA definition of the reference rate. Such a reference rate was tested by the European Task Forces on FISIM and it was not considered as a suitable choice for the FISIM method adopted in ESA 201011.

It was noted that deposits are stable and a reliable source of funding for the lending business of banks. Indeed, in the aftermath of the financial crisis, banks put a lot of effort and were engaged in developing new technologies (like e-banking) to retain existing depositors and attract new depositors, which implies that there are a lot of services provided by banks on deposits. Lots of deleveraging was also observed on the markets from risky assets such as securities into deposits12. So FISIM on deposits should not be negative or close to zero. Hence, the reference rate must be higher than the short-term interbank rate (for example, LIBOR) rate to avoid such an outcome.

The Bank of Portugal proposed a method where FISIM is calculated on loans and deposits for short- and long-term maturities, using LIBOR13 and ISDAFIX14 as reference rates, respectively. The approach of blending the ISDAFIX rate into the reference rate, they argued, developed a rate representing the opportunity cost of funds, whereas using a rate on government securities (a similar approach adopted in the US prior to 2008 SNA) would lead to a reference rate that represented the costs of funds. In a cash flow analysis, the cost of funds approach should only be considered if funds are scarce, as in this case the issuance of new debt is involved. Otherwise, the cost of funds should be neglected, as this is considered as sunk costs. In a discounted cash flow analysis, the reference rate should reflect the liquidity and risk of the cash flow being analysed15.

The European Task Force on FISIM of 2010 to 2012 used an augmented method based on the work of the Bank of Portugal and used a single weighted average reference rate of LIBOR (3-month) and ISDAFIX weighted by stocks of loans and deposits. The results of the original method proposed by the Bank of Portugal and the single weighted average reference rates were very similar. The method of using a single weighted average rate improved FISIM on deposits to households as consumers by reducing its volatility and solving the issue of continuous negative values in the aftermath of the financial crisis.

The European Task Force on FISIM tested this method and the results of the tests using the single weighted average reference rates for the UK are shown in Figure 9. It shows very similar results as in the test for Portugal, where the weighted reference rate (green line) fits well between the implied rates on loans and deposits. The continued occurrence of negative FISIM on deposits was solved, except for a one-off occurrence of negative FISIM on deposits in Quarter 4 2008. At that time the internal reference rate was based on Bank rate (red dotted line) and was below the rate on deposits (purple line) causing a negative FISIM margin on deposits, which reduced FISIM's contribution to GDP in the aftermath of the financial crisis. The volatility of FISIM on GDP was also reduced.

Figure 9: GBP FISIM by MFIs allocated into households as consumers

Source: 'Results on the FISIM tests on maturity and default risk', Eurostat 2012

Download this image Figure 9: GBP FISIM by MFIs allocated into households as consumers

.png (41.6 kB){kind=link}

Some EU member states argue that the tested method using the Single Weighted Average Reference Rate delivered only very marginal improvements, even though some issues were solved (like negative FISIM). Furthermore, the LIBOR blended into the calculation of the Weighted Average Reference Rate was subject to manipulation as highlighted in the media in 201216.

This method was not accepted by the EU member states as the results of FISIM calculated using the Weighted Average Reference Rate did not lead to significant improvements that would justify the replacement of the present method. Hence, this method was not adopted in the ESA 2010 manual.

4.2.3 Multiple reference rates approach

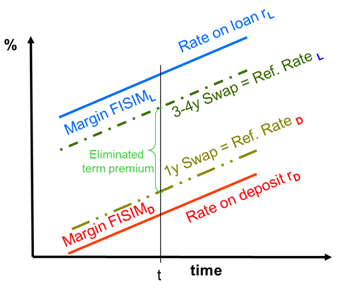

A second camp supporting the use of multiple rates or rates matching the corresponding sectorised loans and deposits implied rates are of the view that term premium should be excluded from the measure of FISIM. This is largely determined by the fact that FISIM is, by convention, restricted to loans and deposits. Maturity transformation is not restricted to loans and deposits, but includes debt securities17.

The Bank of Japan developed a method based on two reference rates, matching the implied rates on deposits and loans. The average maturity of deposits is 1 year thus the 1 year yen-yen swap rate was used for deposits, whereas loans granted in Japan have a maturity between 3 to 4 years, thus the average of the 3 and 4 year yen-yen swap rates was used to match the rate on loans.

Figure 10 illustrates the approach tested in Japan. Following this approach, where term premium was eliminated from the measure of FISIM, the output of FISIM was reduced by approximately 20% compared with the method using a single reference rate18.

Figure 10: Illustration of FISIM margins based on two reference rate approach

(Linear evolution of rates is for illustration purposes only)

Source: Notional values

Download this image Figure 10: Illustration of FISIM margins based on two reference rate approach

.png (37.7 kB){kind=link}

However, the two reference rate method described was not introduced into the national account in Japan; instead the single reference rate approach was implemented.

The European Central Bank (ECB) performed tests for the Euro Area using multiple reference rates matching a variety of deposits and loans by type and by maturity. For example, in the calculation for FISIM consumed by non-financial corporations and households, 13 separate reference rates were used to match implied rates on loans and 14 reference rates to match implied rates on deposits. Given that non-financial corporations and households represent 80% of the total financial balance sheet of the non-financial counterparties, FISIM output (calculated using the multiple reference rates) was reduced by 28%19.

4.3 FISIM adjusted for default risk

The recent financial crisis consisted of a number of critical events that brought many of the world largest financial institutions close to collapse. Around Quarter 4 2008, equity prices of the major global banks fell on average by approximately 50%, impacting the level of world GDP and trade.

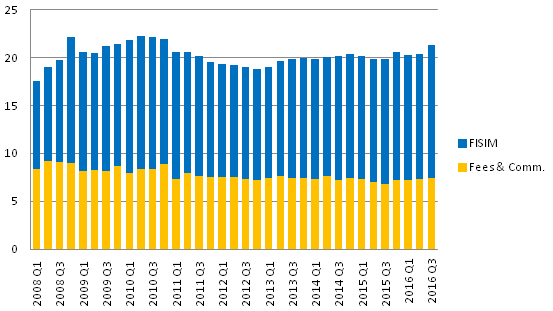

However, official statistics determined by international accounting standards, showed a rather different picture20. For example, ONS statistics showed that FISIM (implicit output of MFIs) in Quarter 4 2008 increased and remained at a historically high level until the end of 2010, while fees and commissions (explicit output of MFIs) remained broadly unchanged (see Figure 11).

Figure 11: Explicit (fees and commissions) and implicit (FISIM) output of MFIs (in £ billion)

Source: Bank of England

Download this image Figure 11: Explicit (fees and commissions) and implicit (FISIM) output of MFIs (in £ billion)

.png (7.2 kB){kind=link}

The reason behind the increase in FISIM in Quarter 4 2008 has already been explained in this article. In short, this substantial increase was driven by an increase in the FISIM margins on loans. This was the result of only a very modest decrease in the effective rates on loans following the significant cut in Bank rate (see section 4.2.1).

This phenomenon attracted lots of attention in the press and in academia. Haldane (2010), the BoE’s Chief Economist, argued that at times when risk is rising, the contribution of the financial sector to the real economy may be overestimated, thus conceptually, it is not clear that risk-based income flows should be represented in the bank output.

The recent Independent Review of UK Economic Statistics by Prof. Sir C. Bean also favoured an approach of measuring FISIM from which risk is eliminated: “An important limitation of FISIM lies in its inadequate treatment of risk. The margin a bank charges on its loans over what it can earn by investing instead in a risk-free asset is meant to cover not just any costs of administering the loan but also the risk of default. The loan spread will therefore be higher if the perceived risk of default rises”. Although the review acknowledged that FISIM in the UK is compiled in line with the up-to-date international and European accounting standards, it supported research to “consider alternative approaches to further improve the present calculation of FISIM”, and encouraged ONS and BoE to take a leading role in shaping the next generation of international standards21.

Risks in the measurement of FISIM can be associated with both services attributable to deposits as well as to loans. For example22:

- liquidity risk occurs when a financial instrument cannot be transacted

- market risk occurs when the value of financial instruments fluctuates over time and may not meet expectations of generated returns

- default risk occurs when the counterpart does not meet the terms and conditions of the corresponding contract

Risk on deposits is very small, as it is unlikely that depositors, in high numbers, would create a run on the banks to withdraw or liquidate their deposits. It was argued earlier in this article (section 4.1.) that in the aftermath of the financial crisis, investors were quick to move their assets from securities into deposits, diversifying their portfolio by reducing the quantity of risky financial instruments.

Risk on loans can be attributed to non-performing loans (loans that are overdue by more than 90 days) where a substantial proportion of non-performing loans may ultimately be written-off23. In consequence, FIs always anticipate such an eventuality that some proportion of total loans granted may not be repaid in full or at all. Hence, part of the interest charged by FIs on loans includes a margin for loan principal that is attributable to expectations that a proportion of loans granted will default in the future. Hence, FIs blend into the interest rate of a given loan, a risk element for that loan defaulting based on their past experiences.

It was argued that the revenues that FIs generate indirectly (implicitly) should correspond to the amounts needed to compensate factors of production, such as labour used in generating services24. In other words, funds used to cover for losses on defaulting loans’ principal are not available to cover costs of labour needed for production, so they should be out-of-scope for measuring output25.

This type of risk in FISIM on loans was examined by the European Task Force on FISIM in 2010 to 2012. It was agreed that among various types and degrees of risks that could be excluded from the measure of FISIM, the exclusion of the risk that compensates for expected losses on loans going into default could be a possible way forward. However, the results of the test of eliminating default risk from the calculations of FISIM margin proved to be inconclusive, in particular due to the unavailability of sectorised source data on write-offs and provisions for bad and doubtful loans in most countries26.

The BoE had been collecting statistical data on provisions for bad and doubtful debts, and thus proposed a method to the European Task Force, where the sectorised FISIM margin on loans is adjusted for default risk. This method was developed using data on write-offs of loans and derived provisions for bad and doubtful loans. A similar method to calculate risk adjustments were developed by the US Bureau of Economic Analysis (BEA) using charge-offs of loans. Developments of these methods are explained in section 4.3.1.

The European FISIM Task Force of 2010 to 2012 considered and tested the method of FISIM adjusted for default risk amongst EU countries. The results of the tests showed considerable problems with the availability of detailed sectorised information in the majority of EU countries. As such, the outcomes of the FISIM tests on default risk eliminated from the calculations of FISIM margin were inconclusive. This was particularly due to the lack of availability of sectorised source data on write-offs and provisions for bad and doubtful loans (non-performing loans)27.

Other researchers like Colangelo and Inklaar estimated and eliminated risks by empirically developing reference rates matching the detailed sectorised loans and deposit rates. As a result, FISIM output of the euro area was reduced significantly. For example, in section 4.2.3, it was explained that FISIM output in the euro area calculated using the multiple reference rates, that eliminated term premium, was reduced by 28%. However, by further adjusting these reference rates for default risk, using Merrill Lynch indexes, FISIM output was further reduced by 54% compared with unadjusted FISIM output28. A similar approach was elaborated by Basu, Inklaar and Wang29, where besides eliminating default risk they also eliminate term premium from the measure of FISIM30.

In the US, the BEA introduced a method of eliminating default risk (margin)31 from the FISIM measure by adjusting the corresponding margin on loans. The default risk adjustment reduced the implied rate on loans between approximately 0.5% and 1% pre-2008, but in the aftermath of the financial crisis, the default risk adjustment reduced the rate on loans by approximately 50% of the margin between the rate of loans and the reference rate32.

Some national accountants, however, argued that the issue of setting prices to allow for risks is not unique to the banking industry, and may be observed for many goods and services. To make adjustments for banking services, whilst not making adjustments elsewhere, would lead to a non-harmonised approach.

Furthermore, as illustrated earlier in this article, the output of banks consists of explicit charges for fees and commissions, and implicit charges that must be calculated using a FISIM model. To date, there have been no attempts to eliminate risk from fees or commissions, instead researchers have concentrated on the possibility of eliminating risk from FISIM.

In 2016, the Advisory Expert Group on National Accounts discussed this issue of excluding default risk from the measure of FISIM. It concluded that in case default risk should indeed be excluded, further economic reasoning underpinning the FISIM adjusted for default risk should be provided and in particular including practical compilation methods33.

While some arguments on the rationale and theoretical methods for eliminating default risk from the measure of FISIM were elaborated earlier in this article, a practical method for FISIM adjusted for default risk is examined in section 5.

4.3.1 FISIM adjusted for default risk

The methods for compiling FISIM adjusted for default risk require developing adjustments at user sector level representing risk attributable to defaulting loans (non-performing loans).

The default risk adjustments should consider FIs’ approach in developing the rates on loans. FIs take into account the proportion of total loans that would default and thus be written-off from their balance sheets – hence provisioning against these expected losses. FIs also take into account aspects related to repricing of loans that impact their future returns – an additional element that is embedded in rates of loans. Given that in national accounts, FISIM is compiled on all sectorised loans, expectations of current losses will depend not only on the current period, but also on the past periods (observations). Therefore, in order to develop default risk adjustments, a relevant smoothing technique must be used to convert past information into an expectation function – such as adaptive expectation or rational expectation functions. The time horizon used in a smoothing technique must be indicated by the time lag between provisions and write-offs blended together – with time of repricing of loans based, for example, on detailed stocks partitioned into repricing bins.

The following options could be used to compile adjustments using write-offs of loans and provisions for bad and doubtful loans, converted into expected losses on defaulting loans.

Option 1

The formula to calculate expected default risk adjustments using a blend of write-offs of loans and provisions was elaborated and provided in the Eurostat recommendations for testing FISIM adjusted for the default risk34. Using both write-offs and provision considers an average lag difference of provisioning against write-offs that is represented in the default risk adjustments.

It is explained by the following two steps.

First, we calculate variable DR (default risk adjustment or margin) for a given quarter q as the share of 4-quarter average of the write-offs to the corresponding 4-quarter average of provisions, then outcome is exponentially weighted by the corresponding 4-quarter provisions. This is shown by equation 7:

Equation 7

Then, we calculate the risk adjustment for a given quarter q by taking a 2-quarter moving average of the variable DR for additional smoothing. This is shown by equation 8:

Equation 8

Option 2

If provision data are not available, the exponential smoothing35 also known as exponentially weighted moving average (EWMA) could be used. It is a moving average method with weight declining exponentially, putting more emphasis on values of the recent quarters and less on those of less recent quarters. This is shown by equation 9 – where β represents the weights declining exponentially and spread over 16 quarters36 and W represents the write-offs of loans:

Equation 9

Where weights are in range of 0 < β < 1, and they sum up to one.

Further smoothing is also applied to the DR in option 1 to calculate the risk adjustment DR_adjq for a given quarter q by taking a 2-quarter moving average following equation 8.

Option 3

Another similar approach to calculate FISIM adjusted for the default risk was examined and implemented by the BEA in the US37. The risk adjustment developed by BEA is based on adaptive expectation model that can be explained by equation 10:

Equation 10

where d is the Default Risk margin/adjustment and c is the charge-offs38 of loans.

This formula sets the estimated default risk adjustment (default margin) of the current quarter q by cumulating the estimated default risk adjustment from the preceding quarter (q-1) plus 0.075 times the difference between the observed charge-off rate in the current period cq and the estimated default margin from the previous period. The 0.07539 per quarter figure is chosen to match the average maturity and repricing dates of loans on banks’ books, which is about 3 years (more precisely 13.3 quarters).

The default risk adjustment (DR_adj.) calculated as previously indicated, would then be used to eliminate the default risk from the rate on loans (rL) of a given sector. This results in an adjusted rate on loans (adj. rL). This would reduce the FISIM margin of loans as illustrated by Figure 12.

Figure 12: Illustration of FISIM margin on loan adjusted for default risk

(Linear evolution of rates is for illustration purposes only)

Source: Notional values

Download this image Figure 12: Illustration of FISIM margin on loan adjusted for default risk

.png (31.5 kB){kind=link}

Following from equation 6 in section 3.1.5, as explained earlier, the FISIM output adjusted for default risk can therefore be amended as follows:

Equation 11

Where, the adjusted rate on loans for default risk is given as:

Equation 12

It is expected that the default risk would be significantly higher during times of financial distress, thus reducing the total FISIM output.

4.3.2 Non-performing loans and impairment reflected in FISIM adjusted for default risk

The timing of the impairment has until recently followed the guidance of the International Standard Board in the International Accounting Standards section 39 (IAS39 guidance), which states that a financial asset is impaired, and impairment losses are incurred, only after a loss event has occurred and this loss event has a reliably measurable impact on the future cash flows. Such loss events include significant financial difficulty, breach of contract (failing to meet interest or principal payments), likely bankruptcy, and loss of active market for a specific asset.

Going forward, financial institutions will adopt International Financial Reporting Standards section 9 (IFRS9), which is more forward-looking in terms of the recognition of impairments. IFRS9 has adopted the “expected loss” approach, whereby expected losses are recognised before they are incurred, rather than after a loss event has been identified. Hence, under the expected loss approach, losses are recognised earlier than the incurred loss model. The reporting of impairments on an IFRS9 basis will be mandatory from 2018 but reporting institutions have the option to adopt earlier if they so wish.

In terms of the timing of the ultimate write-off, an entity will write-off a debt when it considers that debt is uncollectable. A debt is considered uncollectable if the entity has no reasonable expectation of recovery. As such, entities will write-off a debt or part of that debt in the period in which the entity has no reasonable expectation of recovery of the debt (or part of the debt).

Notes for: International debate on calculating and allocating FISIM

- Christian Ravets (2003)

- Hill P. (1996)

- Reinsdorf M. (2011a)

- Christian Ravets (2003)

- Hood K.K. (2013)

- Cambell D. (2010)

- It should be noted that MFIs’ balance sheets were subject to depreciation of sterling over the period, which had an effect on increased the level of deposit liabilities. The impact of the depreciation was asymmetric across loans and deposits.

- Diamond W. and Dybvig (1983) defined liquidity transformation as desire for the security and convenience that comes from having access to funds causes households and businesses to prefer short maturities when they are the creditor but long maturities when they are the debtor. Banks accommodate their customers’ preference by financing illiquid long-term loans with short-term liabilities that must continually be rolled over or replaced.

- Diewert E.(2014)

- Zieschang K. (2013)

- Ravets C.(2003) and Akritidis L (2012)

- Cambell D. (2010)

- Or other equivalent interbank rates in other currencies, like EURIBOR, STIBOR, PRIBOR, WIBOR.

- ISDAFIX rate is a worldwide common reference rate for fixed interest rate swap rates collected by the International Swaps and Derivatives Association (ISDA). ISDAFIX rate is used by banks as a leading benchmark rate for long-term operations, and it is analogous to LIBOR rate used for short-term operations.

- Santa S.F. (2011)

- Akritidis L. (2012)

- Colangelo A, Inklaar R. (2010) and Hagino S. Sonnoda K.(2010)

- Hagino S. Sonnoda K.(2010)

- Colangelo A. Inklaar R. (2010)

- Haldane A, Brennan S., Madouros V. (2010) and Burgess S. (2011)

- Bean C.(2015)

- Zieschang K. (2011)

- Loan write-offs and provisions generally follow IAS39 that would soon to be replaced by IFFRS9 (see section 4.3.2).

- Corrado C, Reinsdorf, M., Hood K. (2014)

- Hood K.K.(2013)

- Akritidis L. (2012)

- Akritidis L. (2002)

- Colangelo A. Inklaar R. (2012) and Colangelo A. Inklaar R. (2010)

- Basu S., Inklaar R. and Wang C.(2011)

- It must be stressed that term premium is a concept related to maturing transformation (explained in section 4.2.3). It must not be conflated with default risk (margin) on loans. Only the latter is considered in this article as possible risk that could be eliminated from the measure of FISIM.

- It is worthwhile noting some differences is terminology used, Hood (2013) referrers to the amounts of expected losses on loan defaults as “default margin”, while in this article we used “default risk” to realign mainly with the terminology used by the European Task Force on FISIM. Colangelo A. Inklaar R. (2012) also used the terminology “default risk”, while the ISWGNA Task Force on FISIM used “credit default risk”.

- Hood K.K. (2013)

- AEG (2016)

- Akritidis L. (2012)

- Carnot N., Koen V., Tissot.(2011)

- A 4 year average (16 quarters) was chosen to reflect the period over which most loans are assumed to be repriced. Furthermore, this assumption was also tested empirically giving the best outcome and it is also in line with the method adopted in the US.

- Hood K.K.(2010) and Reinsdorf M. (2011b)

- Charge-offs of a loan still give the right to FIs to pursue collection of outstanding balance, contrary to write-offs where the loans are forgotten (see more in section 5.1).

- The average coefficient is calculated as 1/13.3 quarters.

5. Experimental estimates of FISIM adjusted for default risk

As explained in section 4.3 of this article, financial intermediation services indirectly measured (FISIM) could be adjusted for default risk by reducing the FISIM margin on loans. Financial intermediaries (FIs) determine the rates on loans, which they charge their customers for, by taking into account expected losses on loan defaults. Therefore, in adjusting FISIM for default risk, we must take this rationale into consideration.

5.1 Underlying statistics that could be used in developing default risk adjustments

(Net) provisions on bad and doubtful loans (net of releases and recoveries): these are amounts made against impaired loans including interest. These loans (including interest) are assessed individually and/or collectively as impaired loans that would be written-off in a later period.

Please note that further changes will be implemented for provisions when new accounting standards on impairment from International Financial Reporting Standards section 9 (IFRS9) are adopted (see section 4.3.2).

(Net) write-offs of loans (net of recoveries): these are amounts related to reduction of the recognised value of loans, which become non-collectable resulting from reassessment of the creditworthiness of a debtor by the loan granting institution. Write-offs do not result from market valuation or exchange rates changes. Specifically, a loan is recognised by the granting institution as non-performing after the first missing instalment or repayment, then after a period of 180 days of non-performance of the loan, the granting institution decides to remove that loan from its balance sheet, as it can no longer be collected, for example, due to bankruptcy or liquidation of the debtor.

(Net) charge-offs of loans (net of recoveries): these are similar to write-offs, except the loan granting institution still reserves the right to pursue the collection of the outstanding balance. A charge-off is often mistakenly interpreted as a debt or loan that is forgotten, as in the case of “write-off”. Charge-off is simply a reclassification of the loan from performing to non-performing, and the debtor still owes the money even if the account has been charged off.

5.2 Developing and testing default risk adjustments

In the UK, only sectorised write-offs on loans are collected from monetary financial institutions (MFIs). Provisions are collected on all bad and doubtful debts, where the sectoral breakdown is not detailed enough for calculating FISIM by required sectoral level of detail. Although it was possible to model provisions to eliminate non-loan provisions and to arrive at a satisfactory sectoral split, the results show that the derived provisions on loans do not match well the corresponding write-offs.

Figure 13 shows that estimated MFIs’ provisions on loans to households as consumers increased sharply during the financial crisis, but their level was substantially higher compared with the level of the corresponding write-offs. This indicates that MFIs had continuously been slightly over-provisioning until the eruption of the financial crisis in the UK in Quarter 4 (Oct to Dec) 2008 – when they increased already high provisions. From late 2013, the situation changed – the provisions were slightly below the corresponding write-offs. Here it could be argued that MFIs were lenient in allowing households plenty of time to manage their finances before ultimately writing off the loan. Hence the lead time between provisions and write-offs around the time of crisis decreases provisions below the level of write-offs in recent years.

Figure 13: Annualised1 MFIs provisions and write-offs of loans to households as consumers

(Non-seasonally adjusted - in £ billion)

Source: Calculations based on Bank of England data

Notes:

- Annualised time series data are calculated as simple four quarters moving averages. This technique allows comparability of time series by averaging out possible seasonal effects, short-term volatility or potential measurement problems (Carnot N., Koen V., Tissot B.(2011)). This technique does not remove seasonal effect if detected.

Download this chart Figure 13: Annualised^1^ MFIs provisions and write-offs of loans to households as consumers

Image .csv .xlsFigure 13 also illustrates a lag between provisions and write-offs. In order to identify a number of quarters that the write-offs were lagging behind the provisions, a number of models were applied for detecting the relation of the write-offs at different lags to the provisions. The regressions with autoregressive residuals were estimated according to the Cochrane and Orcutt procedure. However, as none of the coefficients of any order were statistically significant, there is no clear evidence of the relationship between provisions and write-offs at different lags. Hence, there is no useful information that indicates the relevant time horizon of past quarters that could be used for the expectation function (see section 4.3.1).

Based on this analysis, it is assumed that provisions are not fit for purpose to calculate default risk adjustments, because the level of estimated provisions was substantially higher compared with the level of the corresponding write-offs – furthermore there was no evidence to indicate the relevant time horizon of past quarters to be used in the expectation function. However, this assumption will need to be looked at after 2019 to 2020 because reporting of provisions should improve when MFIs implement new accounting standards on impairment according to IFRS9 in 2018 (see section 4.3.2).

For the purpose of developing the default risk adjustments, the options-based write-offs will be examined. The MFIs’ sectorised write-offs of loans are presented in Figure 14.

Figure 14 shows that MFIs’ write-offs1 increased over the period of the financial crisis. Write-offs peaked in 2009 for households as consumers and in 2010 for private non-financial corporations, while write-offs attributable to non-residents did not peak until 2013. It is only in 2015 that loans write-offs for private non-financial corporations and non-residents returned to pre-crisis levels. Write-offs of loans to households are now lower than pre-crisis levels possibly reflecting tight lending conditions, especially in relation to dwelling loans following the introduction of the Mortgage Credit Directive in 2014.

Figure 14: Annual MFIs write-offs of loans by sectors (in £ billion)

FISIM on the scale on the left hand side (LHS), revisions on the right (RHS)

Source: Bank of England

Download this chart Figure 14: Annual MFIs write-offs of loans by sectors (in £ billion)

Image .csv .xlsIn order to adjust the measure of FISIM for default risk, relevant adjustments by user sectors need to be compiled, which represent the expected proportion of total loans granted by the FIs that would go into default and thus be written-off from their balance sheets. The sectorised default risk adjustments were developed in line with the formulae explained in section 4.3.1.

The following methods were used to develop the default risk adjustment.

4y EWMA: the provisions were assumed not fit for purpose for developing default risk adjustments, so the next best smoothing method is 4-year exponentially weighted moving average of the annualised write-offs calculated separately for each sector and by currency. Hence, this smoothing method is chosen as a benchmark method, subject for further testing in the present article. It is calculated as elaborated in section 4.3.1 with weights spread exponentially over 16 quarters q to take into account the relevant lagging function to allow for average repricing of loans. This is shown by equation 12, where W represents write-offs of loans:

Equation 12

Then, we calculate the risk adjustment for a given quarter q by taking a 2-quarter moving average of the variable DR for additional smoothing, as equation 13:

Equation 13

This article also examines the following alternative smoothing methods.

US method: is the method implemented in the US Bureau of Economic Analysis (BEA), where the risk adjustment (separately for each sector and by currency) is calculated by accumulating the adjustment from the preceding quarter (q-1) plus 0.075 times the difference between the observed annualised loans write-off in the current period Wq and the estimated adjustment from the previous period (see section 4.3.1). This is shown by (equation 14):

Equation 14

4y CUMULATIVE: is similar to the US method, where the risk adjustment (separately for each sector and by currency) is calculated by accumulation of the adjustment from the preceding quarter (q-1) plus 0.063 times the difference between the observed annualised write-off in the current period and the estimated adjustment from the previous period. The 0.0632 per quarter figure is chosen to match the average repricing of loans corresponding to 16 quarters (equation 15).

Equation 15

1y EWMA: is the 1 year exponentially weighted moving average of the annualised write-offs calculated separately for each sector and by currency (sterling and foreign currency). For a given quarter q it is calculated as moving averages, exponentially weighted, by the corresponding preceding 4-quarters of write-offs. This is shown by (equation 16), where W represents write-offs of loans:

Equation 16

Then, we calculate the risk adjustment for a given quarter q by taking a 2-quarter moving average of the variable DR for additional smoothing to eliminate unnecessary volatility that should not be passed into FISIM. This is shown by (equation 17):

Equation 17

These default risk adjustments (DR_adj.) are then used to eliminate the default risk of a given sector, thus reducing the FISIM margin of loans as illustrated by Figure 12.