1. Key points

The intermediate estimate of the value of UK manufacturers’ product sales in 2013 was £354.5 billion, a 3.7% increase on the final 2012 estimate of £ 342.0 billion

UK manufacturers’ product sales were 18.3% higher in 2013 than in 2009

The product with the largest value of sales in 2013 was motor vehicles with a medium or large petrol engine at £13.8 billion

The industry which contributed most to manufacturing sales growth between 2012 and 2013 was the manufacture of motor vehicles, trailers and semi-trailers

The UK contributed between 5% and 10% of total EU manufacturers’ product sales in 2012, behind Germany, France and Italy

2. Overview

Manufacturers’ value of sales continued to grow in 2013, continuing the recovery in values of sales seen since 2009. The divisions which have driven most growth in the value of product sales are the manufacture of motor vehicles, the manufacture of other transport equipment and the manufacture of food products. Products with high manufacturers’ sales value for 2013 include both petrol and diesel motor vehicles, beer, soft drinks and the manufacture of parts for all types of aircraft, for civil use.

This statistical bulletin and associated data provide intermediate estimates for manufacturers’ product sales in 2013, from businesses based in the UK. It also provides final estimates for 2012. Manufacturers’ Sales by Product (PRODCOM) surveys are carried out annually by all European Union (EU) member states, under EU regulation, to enable comparison and, where possible, produce a picture of emerging developments of an industry or product in a European context; the latest data for all EU member states can be found on the Eurostat website.

All estimates of the value of sales are presented in current prices, meaning they have not been adjusted for inflation. Due to an update of the Standard Industry Classification (SIC), estimates prior to 2008 may not be comparable with those after 2008 - see background note 2. Total UK product sales estimates prior to 2008 are included in this release but care should be taken when comparing estimates over this period.

ONS makes every effort to provide informative commentary on the data in this release. Where possible, the commentary draws on evidence from businesses or other reputable sources of information to help explain possible reasons behind the observed changes. However, in some instances it can prove difficult to establish detailed reasons for movements, for example, businesses may state a ‘change in the production strategy’ or ‘products being made under a new contract order’. Consequently, it is not possible for all data movements to be fully explained.

Back to table of contents3. Your views matter

We continuously aim to improve this release and its associated commentary. We would welcome any feedback you might have and would be interested in knowing how you make use of these estimates to inform your work.

In particular we welcome any comments or feedback on the following:

The new format of the excel tables

The Open Data format of the PRODCOM reference tables

The user interpretation manual

Background note 1 has further information

Please provide comments via email: prodcompublications@ons.gov.uk or telephone William Barnes on +44 (0)1633 455711

Back to table of contents4. UK manufacturers’ sales by product 2013

The intermediate results for UK manufacturers’ sales by product in 2013 show there was growth of 3.7% in the value of sales, at £354.5 billion, up from £342.0 billion in 2012. This is a continuation of the recovery seen since 2009 (see Figure 1). The final estimated value of UK manufacturers’ product sales in 2012 of £342.0 billion is a downward revision of 0.5% from the £343.8 billion published as part of the 2012 intermediate estimate in December 2013.

Figure 1: Total value of UK Manufacturers’ Product Sales, 2003 - 2013

Source: Office for National Statistics

Notes:

- Care should be taken when comparing estimates prior to 2008 with those after 2008 due to an industry reclassification.

Download this chart Figure 1: Total value of UK Manufacturers’ Product Sales, 2003 - 2013

Image .csv .xlsBetween 2008 and 2009, there was a reduction of nearly 10% in the value of UK manufacturers’ product sales, equivalent to £32.2 billion. Since 2009, the value of product sales has increased in each year, in current prices. In the four years since 2009, the value of UK manufacturers’ product sales has increased by 18.3%, a value of £54.9 billion. The fall between 2008 and 2009, and the subsequent recovery in the value of industrial product sales, is broadly in line with movements seen in other data sources such as the Annual Business Survey and National Accounts.

Back to table of contents5. Results by product

Figure 2 shows the 10 products with the highest sales value for 2013 and highlights the change in rankings compared with 2012.

Figure 2: Top 10 UK manufactured products with the highest production by sales value

Source: Office for National Statistics

Download this image Figure 2: Top 10 UK manufactured products with the highest production by sales value

.png (554.3 kB) .xls (31.7 kB)There are several core products that have been present in the top 10 of UK manufacturers’ sales in value terms since 2008. For example, eight of the top 10 products in 2008 also feature in the 2013 list. These include both petrol and diesel motor vehicles, beer, soft drinks and the manufacture of aircraft. In 2013, one product features in the top 10 for the first time since the series began; the manufacture, installation and repair of military vessels (or parts there of).

The 2013 intermediate estimates show that the manufacture of motor vehicles with a medium or large petrol engine remains the leading product in terms of value of sales; this has remained unchanged since 2010.

Motor vehicles

The sale of motor vehicles contributed 9.6% to total manufacturer sales, valued at £33.9 billion an increase of £5.9 billion on 2012. The motor vehicle products in the top 10, with their position shown by the number in brackets, were:

motor vehicles with a petrol engine greater than 1500cc (1)

motor vehicles with a diesel engine between 1500cc and 2500cc (2)

Cars with medium and large petrol engines had the highest value product sales at £13.8 billion, an increase of £0.6 billion since 2012. Conversely, the volume of motor vehicles of this type sold decreased over the same period by 61,000 items. This shows consumers are spending on average approximately 12.7% more per unit, a trend likely to be influenced by the sales of luxury cars and demand for improved technology in motor vehicles.

The value of sales of diesel cars between 1500cc and 2500cc also increased between 2012 and 2013, by £4.2 billion to £10.2 billion, an increase of 69.8%. The demand for more fuel efficient vehicles as fuel costs increased may be a contributory factor. Whereas the volume of petrol cars sold decreased between 2012 and 2013, the volume of diesel cars sold increased over the same period by 70,000 items, an increase of 15.6% (see Figure 3). As the value increased at a faster rate than the volume, the average unit value also increased from around £13,300 to £19,500.

Figure 3: Sales of petrol and diesel cars manufactured in the UK, 2008 - 2013

Source: Office for National Statistics

Notes:

- Petrol cars in this chart refers to product code 29102230 - motor vehicles with a spark ignition internal combustion engine greater than 1500cc, excluding goods vehicles, motor caravans and those for carrying 10 or more people.

- Diesel cars in this chart refers to product code 29102330 - motor vehicles with a diesel or semi-diesel engine greater than 1500cc but not exceeding 2500cc, excluding goods vehicles, motor caravans and those for carrying 10 or more people.

Download this chart Figure 3: Sales of petrol and diesel cars manufactured in the UK, 2008 - 2013

Image .csv .xlsThe Society of Motor Manufactures and Traders (SMMT), the UK car industry’s trade body, reported that in 2013, UK car manufacturers had their best performance since 2007, reporting a number of recent investment projects, including £2.0 billion investment in R&D as reported by the ONS Business Enterprise Research and Development (BERD) survey. The growth in the UK motor industry is in contrast to its European counterparts, with industry sales among many EU members having fallen since the economic downturn. While growth in the UK motor vehicle industry is still reliant on exports, it has been suggested that the upturn in the domestic market has been assisted by cheaper credit deals for consumers, specifically personal car plans directly offered by manufacturers.

Aerospace and Defence

The UK has the largest aerospace industry in Europe in terms of the number of businesses. The products in this group ranking within the top ten products in 2013, as shown by the number in brackets, were:

parts for all types of aircraft, for civil use (3)

manufacture, installation and repair of military aircraft and parts thereof (4)

repair and maintenance of civil aircraft and civil aircraft engines (6)

manufacture, installation and repair of military vessels and parts thereof (10)

There has been considerable year on year growth in the value of product sales in the manufacture of air and spacecraft. For example, between 2012 and 2013 the value of sales for products in this industry increased by 17.4%, from £17.3 billion to £20.3 billion. This is the fourth consecutive year of growth in the value of product sales. A key product driving this growth is the manufacture of parts for all types of aircraft for civil use, with an increase in sales of £1.2 billion. This product has moved up the product rankings every year since 2009 and currently sits third in the 2013 product list.

The strength of the UK aerospace industry is further highlighted by sales of the repair and maintenance of civil aircraft and engines, appearing at number 6 in the product list, with 5.8% growth in the value of product sales between 2012 and 2013, from £3.3 billion to £3.5 billion.

Figure 4: Values of sales of civil aircraft parts manufacture, and repair and maintenance of civil aircraft and engines, 2008 - 2013

Source: Office for National Statistics

Notes:

- The full description of product code 30305090 is parts for all types of aircraft, for civil use, excluding propellers, rotors, under-carriages, aircraft engines and parts thereof, for military aircraft.

- The full description of product code 33161000 is the repair and maintenance of civil aircraft and civil aircraft engines.

Download this chart Figure 4: Values of sales of civil aircraft parts manufacture, and repair and maintenance of civil aircraft and engines, 2008 - 2013

Image .csv .xlsIn July 2012, the Department of Business, Innovation and Skills published an article highlighting new investment in the aerospace industry and positive forecasts for growth in the future. This was followed in March 2013 with the announcement of a £2 billion investment, aimed to secure over 100,000 jobs and outlining plans for a UK aerospace technology institute. Investment projects such as these, alongside forecasted growth in air travel as highlighted by the International Air Transport Association, may have resulted in increased opportunities for UK businesses in this sector.

It has further been reported that the UK aerospace industry is benefiting from strong domestic orders for parts for civil aircraft, with businesses holding a backlog of more than 11,000 aircraft and 20,000 engines, an estimated nine years' work for the UK industry.

The value of product sales for the manufacture, installation and repair of military aircraft showed a large increase of 22.8% between 2012 and 2013, following a period of stability between 2010 and 2012. This product currently sits at number 4 in the top 10 product sales for 2013, with sales totalling £7.5 billion.

The manufacture, installation and repair of military vessels and parts thereof also sits within the top 10 products in 2013, entering for the first time at position 10 with sales of £3.1 billion. There was a steady increase in the value of sales from 2012 on the back of continued growth since 2008 (see Figure 5).

Figure 5: Values of sales of the manufacture, installation and repair of military vessels and military aircraft, and their parts thereof, manufactured in the UK, 2008 - 2013

Source: Office for National Statistics

Notes:

- The full description for product code 30309999 is the manufacture, installation and repair of military aircraft and parts thereof.

- The full description for product code 30119999 is the manufacture, installation and repair of military vessels and parts thereof.

Download this chart Figure 5: Values of sales of the manufacture, installation and repair of military vessels and military aircraft, and their parts thereof, manufactured in the UK, 2008 - 2013

Image .csv .xlsIf you would like to find out more about aerospace and defence statistics, you can read more ONS analysis in the related links.

Drinks

In 2013, the drinks industry generated £12.4 billion in product sales, 3.5% of all UK manufactured product sales. The industry has three key products that consistently appear in the top 10 manufacturers’ sales; as signified by the number in brackets.

waters, with added sugar, other sweetening matter or flavoured (7)

beer made with malt (8)

whisky (9)

In 2013, ‘Waters with added sugar’ (soft drinks) dropped one position from sixth to seventh place in the top 10, with sales totalling £3.4 billion, a 5.9% decrease from 2012 sales of £3.7 billion. Despite the drop in value of sales, the volume of sales has increased over the same period, from 7.0 billion litres sold to 7.3 billion litres sold. This increase in volume has been largely attributed to a warmer summer by the British Soft Drinks Association.

Following a number of years of contraction in the value of beer sales in the UK, beer product sales increased marginally between 2012 and 2013 totalling £3.2 billion in 2013, an increase of 4.7% from 2012. However, the volume of beer sold has continued to decrease since 2011; see Figure 6.

Figure 6: Litres sold of beer manufactured in the UK, 2008 - 2013

Source: Office for National Statistics

Notes:

- Data in this chart refers to product code 11051000 - Beer made from malt (EXCLUDING alcohol duty) EXCLUDING: - non-alcoholic beer - beer containing not more than 0.5% by volume of alcohol.

Download this chart Figure 6: Litres sold of beer manufactured in the UK, 2008 - 2013

Image .csv .xlsWhisky sales saw a slight value increase in 2013 of £40.7 million, from £3.1 billion in 2012 to £3.2 billion, ensuring it maintained its position as ninth in the top 10 products. However, this is a rise of only 1.3%, compared with an 8.1 % rise between 2011 and 2012. Following a decade of growth, it appears the demand for Scotch whisky is levelling off in some markets and in general the value of Scotch whisky exports during 2013 remained steady.

Other drinks outside the top 10, such as unsweetened mineral and aerated waters, have also shown significant growth over recent years (see Figure 7). Since 2010, the volume sold of UK manufactured mineral water has increased by 59.0% from 973 million litres to 1,546 million litres sold in 2013. This continues the trend seen since 2008.

Figure 7: Litres sold of unsweetened mineral and aerated water manufactured in the UK, 2008 - 2013

Source: Office for National Statistics

Notes:

- Data in this chart refers to product code 11071130 - Mineral waters and aerated waters, unsweetened.

Download this chart Figure 7: Litres sold of unsweetened mineral and aerated water manufactured in the UK, 2008 - 2013

Image .csv .xlsPharmaceuticals

- Medicaments (5)

Medicaments (excluding antibiotics, hormones, steroids, alkaloids and vitamins) remain a top five product in terms of value of sales, with sales totalling £5.9 billion in 2013. However, this is a significant decrease from 2012 sales which totalled £7.1 billion, equivalent to a fall of 16.5%. A reason cited by some businesses was the expiry of medicament patents, which allow competing businesses to manufacture medicaments previously owned by only one company. This drop follows a decreasing trend seen in product sales in the manufacture of pharmaceutical preparations since 2010, where sales have fallen from £14.2 billion in 2010 to £11.3 billion in 2013, a fall of 20.4% (see Figure 8).

Figure 8: Value of product sales in the manufacture of pharmaceutical preparations, 2008 - 2013

Source: Office for National Statistics

Notes:

- Data in this chart refer to total product sales for SIC 21200 - Manufacture of pharmaceutical preparations.

Download this chart Figure 8: Value of product sales in the manufacture of pharmaceutical preparations, 2008 - 2013

Image .csv .xls6. Results by industrial division

The UK estimate of manufacturers’ sales by product covers 25 ‘Divisions’ in the manufacturing sector (see background note 7 for more details on coverage).

There are two ways to consider the PRODCOM estimates; in terms of businesses classified to an industry and in terms of products corresponding to an industry. In this release product information, either individual products or total product sales relate to products corresponding to an industry irrespective of which industry the business making the product is classified to.

Products associated with an industry have been reasonably consistent over the past five years. The manufacture of motor vehicles, trailers and semi-trailers, other transport equipment and food have consistently had the highest manufacturing product sale values.

Divisions’ contribution to growth

Table 1: Contribution to total value of industry sale growth between 2012 and 2013

| Division | Percentage contribution to growth | |

| 29 | Manufacture of motor vehicles; trailers and semi-trailers | 45.09 |

| 30 | Manufacture of other transport equipment | 28.99 |

| 10 | Manufacture of food products | 22.46 |

| 22 | Manufacture of rubber and plastic products | 9.09 |

| 33 | Repair and installation of machinery and equipment | 4.33 |

| 16 | Manufacture of wood and of products of wood and cork | 3.78 |

| 8 | Other mining and quarrying | 1.66 |

| 31 | Manufacture of furniture | 1.41 |

| 25 | Manufacture of fabricated metal products; except machinery and equipment | 1.11 |

| 23 | Manufacture of other non-metallic mineral products | 0.81 |

| 14 | Manufacture of wearing apparel | 0.66 |

| 32 | Other manufacturing | 0.65 |

| 15 | Manufacture of leather and related products | 0.56 |

| 11 | Manufacture of beverages | 0.07 |

| 19 | Manufacture of coke and refined petroleum products | -0.05 |

| 17 | Manufacture of paper and paper products | -0.14 |

| 13 | Manufacture of textiles | -0.15 |

| 20 | Manufacture of chemicals and chemical products | -0.16 |

| 12 | Manufacture of tobacco products | -0.56 |

| 26 | Manufacture of computer; electronic and optical products | -1.27 |

| 21 | Manufacture of basic pharmaceutical products and pharmaceutical preparations | -1.74 |

| 27 | Manufacture of electrical equipment | -1.96 |

| 28 | Manufacture of machinery and equipment n.e.c. | -3.62 |

| 24 | Manufacture of basic metals | -4.82 |

| 18 | Printing and reproduction of recorded media | -6.19 |

| Source: Office for National Statistics | ||

Download this table Table 1: Contribution to total value of industry sale growth between 2012 and 2013

.xls (27.1 kB)Table 1 shows the contribution to growth in manufacturing product sales between 2012 and 2013. The manufacture of motor vehicles; trailers and semi trailers contributed more than any other division to product sale growth, consistent with the industry high year on year product sales. In contrast, the printing and reproduction of recorded media provided the largest negative contribution to growth between 2012 and 2013.

Divisions driving growth in overall manufacturing product sales

Manufacture of motor vehicles, trailers and semi-trailers

Manufacture of other transport equipment

Manufacture of food products

As mentioned previously, there has been considerable growth in manufacturers’ product sales within the motor industry, which has been mainly driven by the manufacture of motor vehicles, in particular cars with medium and large sized engines. In contrast, other industries contributing to this division (manufacture of coaches, trailers and semi-trailers; electrical and electronic equipment for motor vehicles; other parts and accessories for motor vehicles) all experienced negative growth in product sales over the same period (see Table 2).

Table 2: Sales and growth in the manufacturing of motor vehicles; trailers and semi-trailers division

| 2012 Sales | 2013 Sales | Growth | |

| Manufacture of motor vehicles | 28,004 | 33,860 | 5,856 |

| Manufacture of bodies (coachwork) for motor vehicles; manufacture of trailers and semi-trailers | 2,153 | 2,127 | -26 |

| Manufacture of electrical and electronic equipment for motor vehicles | 346 | 313 | -33 |

| Manufacture of other parts and accessories for motor vehicles | 8,794 | 8,650 | -144 |

| Total | 39,297 | 44,950 | 5,653 |

| Source: Office for National Statistics | |||

Download this table Table 2: Sales and growth in the manufacturing of motor vehicles; trailers and semi-trailers division

.xls (18.9 kB)The growth in the other transport equipment division was in part led by the increase in the value of product sales for self-propelled railway or tramway passenger coaches, whose sales totalled £769 million in 2013.

There was a 17.7% fall in the volume sold of sausages from 411 million kilos to 338 million kilos. However, the industry has been buoyed by the growth in volume sales of fresh cuts of chicken (up 12.5%) as well as fresh cuts of beef and veal (9.1%). Elsewhere, the value of sales of fresh bread showed one of the biggest areas of growth for any product in the division, alongside milk and cream with a fat content above 1%.

Divisions restricting growth in overall manufacturing product sales

Printing and reproduction of recorded media

Manufacture of basic metals

The division acting as the largest drag on overall manufacturers’ sales growth between 2012 and 2013 was the printing and reproduction of recorded media, where sales fell from £8.7 billion to £7.9 billion, a fall of 9.0%. The product within this division with the largest fall in sales was the printing of paper trade advertising material where sales fell from £1.8 billion to £1.5 billion, a fall of 18.9%. This is likely due to the rise in Internet advertising. The printing of newspapers, journals and periodicals at least four times a week has also seen a large comparative drop in value of sales, a fall of 5.4%, to £159 million in 2013. This is likely to be a result of the growth in online news at both a local and national level.

The manufacture of basic metals also contracted between 2012 and 2013, a £605 million fall (8.1%) in sales. Particular industry products in this division reporting reductions in product sales included the production of silver in semi manufactured forms and unwrought aluminium alloys; the latter saw a drop in value of almost £190 million (32.0%) and a drop in volume of 140 million tonnes (30.5%).

Back to table of contents7. European comparison

The PRODCOM survey on production of manufactured goods is carried out annually by all EU member states, under EU regulation, to enable comparison and, where possible, produce a picture of emerging developments in an industry or product in a European context.

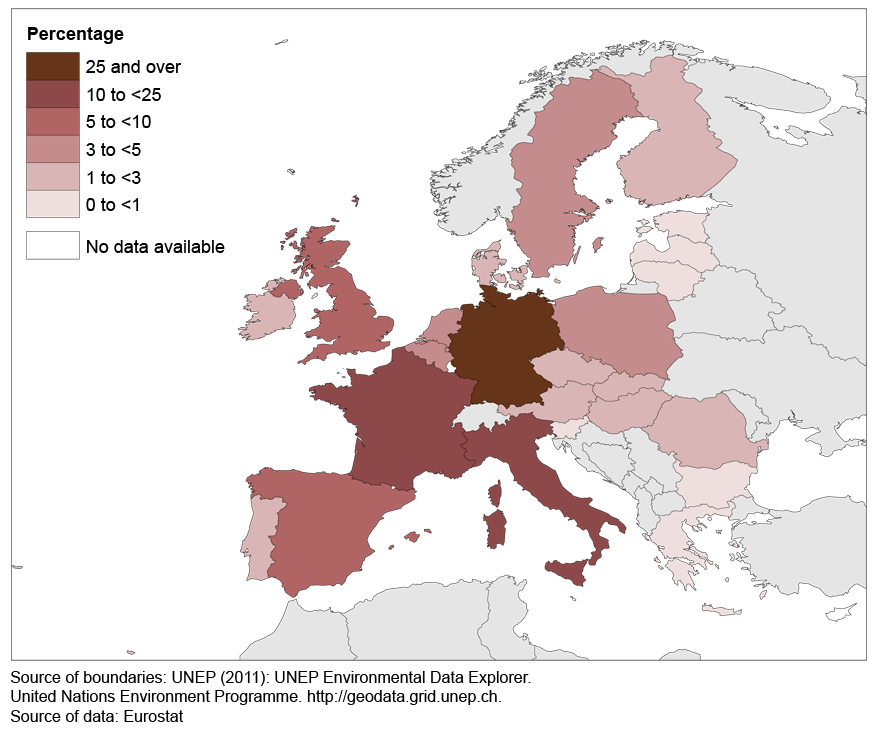

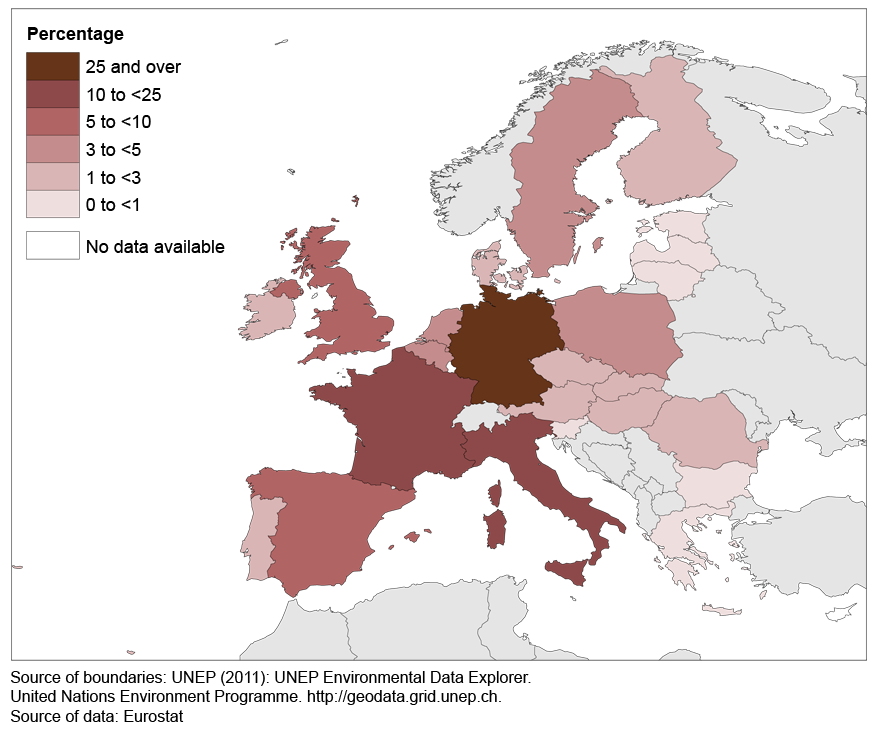

Map 1: EU27 countries share of sold production value

Source: Eurostat

Notes:

- Map 1 is based on the 2012 intermediate estimates, not the most recent data available for the UK, as this is the most recent comparable data across all EU Member States.

- Data are not available for Cyprus, Luxembourg and Malta. According to the terms of the PRODCOM Regulation, these countries are exempt from reporting PRODCOM estimates to Eurostat and zero product sales is recorded for them on all products in the Eurostat total.

Download this image Map 1: EU27 countries share of sold production value

.png (161.7 kB)Map 1 shows the latest available estimates for the share of total value of EU-27 manufacturers’ product sales for each member state, using intermediate 2012 estimates. Germany accounts for almost a third of all EU-27 sold industrial production, while Italy and France each contribute more than 10% of total EU manufacturers’ sales. The UK and Spain each contribute between 5 and 10% of EU production. The five countries provided 69.7% of all EU sold production in 2012.

Eurostat report that in 2012, of the 30 highest ranked products in terms of the value of European manufacturers’ sales, the UK is a top five producer of 21 products but does not lead in the product sales value of any of these products.

The UK does lead EU product sales in many products outside the top 30, although comparisons can be difficult to make as often estimates from other countries are suppressed, disclosive or largely estimated.

In products where the majority of manufacturers’ sales estimates are available for other EU countries, the UK leads in several food products including: savoury bakers’ products; condiments; sandwiches and other food preparations; and chocolate biscuits. Outside of food products, the UK also leads product sales of soft drinks and flavoured waters; printed books and brochures; curtains and blinds made from woven materials; and base metal sign plates and name plates.

A more detailed comparative data for EU countries can be found on the Eurostat website.

Back to table of contents

{kind=link}

{kind=link}

{kind=link}

{kind=link}