1. Main points

The price of services sold by UK companies, as estimated by the Services Producer Price Index (SPPI), increased 1.2% in the year to Quarter 2 of 2016, compared with an increase of 1.3% in the year to Quarter 1 of 2016.

Between Quarters 1 and 2 of 2016, SPPI rose by 0.3%, compared with an increase of 0.5% between Quarter 4 of 2015 and Quarter 1 of 2016.

Professional, scientific and technical activities showed the largest upward contribution to the annual and quarterly rate. Prices increased by 1.9% in the year to Quarter 2 of 2016 and 0.4% between Quarters 1 and 2 of 2016.

Water supply, sewerage and waste management services showed the largest downward contribution to the SPPI, decreasing by 3.7% in the year to Quarter 2 of 2016.

Back to table of contents2. What is Services Producer Price Inflation?

The Services Producer Price Indices (SPPI) provides a measure of inflation for the UK service sector. It is constructed from a statutory quarterly survey which measures changes in the price received for selected services provided by UK businesses to other UK businesses and government. Individual SPPIs are available which provide information on price change for a selection of service industries. These individual price indices are also aggregated together to create a service industry SPPI with limited coverage (it does not provide full coverage of the “service sector”).

The primary use of the SPPI is as a deflator in the UK National Accounts. However, it is also important as an inflationary measure to inform monetary policy and to account for inflation in long-term service procurement contracts. For more information on the use made of SPPI please see the separate document Users of Services Producer Price Index data.

The figures presented in this statistical bulletin are considered provisional for the latest 2 quarters (Quarters 1 and 2 of 2016) and may be revised as late data is received.

None of the indices presented in this bulletin are seasonally adjusted.

Coverage of SPPI

The service sector is estimated to account for around 78% of the UK economy based on its weight in gross domestic product (GDP). We do not produce an index for every industry in the service sector and so the SPPI is a partial, best estimate, of the overall inflation to UK businesses in the service sector. The SPPIs presented in this statistical bulletin are estimated to represent 59% of the total service sector at industry level. The indices' coverage of the service sector at standard industrial classification (SIC) class, division and section level is available in the SPPI coverage document. As resources allow, we will continue to review the existing indices and expand coverage through developing indices for new industries. As such, the SPPI will change composition from time to time but will always remain our best estimate of inflation in the UK service sector. The fact that coverage may change over time should be considered when deciding which indices best meet your needs.

Back to table of contents3. Summary

Between early-2006 and mid-2008, the annual rate of inflation in the service sector, as estimated by the Services Producer Price Index, rose steadily from an annual rate of 2.4% in Quarter 1 of 2006 to a peak of 3.7% during Quarters 1 and 2 of 2008. At the end of 2008, the rate of inflation fell rapidly, from annual inflation of 3.6% in Quarter 3 of 2008 to deflation (prices lower than they were in the same Quarter of the previous year) of 1.6% in Quarter 3 of 2009.

The annual rate of inflation began to move in an upward direction at the end of 2009, reaching a post-economic downturn high of 1.8% in Quarter 2 of 2010. Since mid-2010, inflation has tended to remain relatively steady at around 1%. In Quarter 2 of 2016, prices increased by 1.2%.

Looking at the latest estimates (Table A) of the index for Quarter 2 of 2016, the main movements were:

- prices received by UK service providers increased 1.2% in the year to Quarter 2 of 2016, down from an increase of 1.3% in Quarter 1 of 2016

- the main upward contributions to the annual rate came from increases in the prices charged for professional, scientific and technical activities, information and communication, and real estate activities

- service prices rose 0.3% between Quarters 1 and 2 of 2016, compared with an increase of 0.5% between Quarter 4 of 2015 and Quarter 1 of 2016

- the main upward contributions to the quarterly rate of inflation came from professional, scientific and technical activities, and information and communication

Table A: Output prices (gross sector) - Services Producer Price Index

| Quarter 4 (Oct to Dec) 2011 to Quarter 2 (Apr to Jun) 2016, | |||

| United Kingdom | |||

| Percentage change | |||

| Year | Quarter | ||

| 2011 | Q4 | 1.2 | 0.4 |

| 2012 | Q1 | 1.3 | 0.4 |

| Q2 | 0.8 | 0.5 | |

| Q3 | 1.5 | 0.2 | |

| Q4 | 1.5 | 0.4 | |

| 2013 | Q1 | 1.5 | 0.4 |

| Q2 | 0.8 | -0.2 | |

| Q3 | 0.8 | 0.2 | |

| Q4 | 1.3 | 0.9 | |

| 2014 | Q1 | 0.9 | 0.0 |

| Q2 | 1.5 | 0.4 | |

| Q3 | 1.5 | 0.2 | |

| Q4 | 0.6 | 0.0 | |

| 2015 | Q1 | 0.4 | -0.2 |

| Q2 | 0.4 | 0.4 | |

| Q3 | 0.3 | 0.1 | |

| Q4 | 0.7 | 0.4 | |

| 2016 | Q1 | 1.3 | 0.5 |

| Q2 | 1.2 | 0.3 | |

| Source: Services Producer Price Indicies (SPPI) - Office for National Statistics | |||

| Notes: | |||

| 1. The SPPI is calculated on a gross sector basis. | |||

| 2. The SPPI is an aggregate of the individual industry level indices (excluding Financial Intermediation) published in the SPPI Statistical Bulletin. It does not provide full coverage of the service sector. | |||

| 3. Not all of the industry level indices used to construct the SPPI are National Statistics. | |||

| 4. Q1 refers to Quarter 1 (January to March), Q2 refers to Quarter 2 (April to June), Q3 refers to Quarter 3 (July to September) and Q4 refers to Quarter 4 (October to December). | |||

Download this table Table A: Output prices (gross sector) - Services Producer Price Index

.xls (26.6 kB)

Figure A: Services Producer Price Index

Quarter 2 (Apr to Jun) 2006 to Quarter 2 (Jan to Mar) 2016, UK

Source: Services Producer Price Indices (SPPI) - Office for National Statistics

Notes:

- The SPPI is calculated on a gross sector basis.

- The SPPI is an aggregate of the individual industry level indices (excluding financial intermediation) published in the SPPI statistical bulletin. It does not provide full coverage of the service sector.

- Not all of the industry level indices used to construct the SPPI are National Statistics.

- Q1 refers to Quarter 1 (January to March), Q2 refers to Quarter 2 (April to June), Q3 refers to Quarter 3 (July to September) and Q4 refers to Quarter 4 (October to December).

Download this chart Figure A: Services Producer Price Index

Image .csv .xls4. Annual inflation

The Services Producer Price Index rose by 1.2% in the year to Quarter 2 of 2016, down from an increase of 1.3% in the year to Quarter 1 of 2016. Of the 10 sections (as defined by the 2007 Standard Industrial Classification) that are combined to form the SPPI, 7 showed price increases.

The main upward contributions to the annual rate of the SPPI came from professional, scientific and technical activities and information and communication. These increased 1.9% and 1.6% respectively, in the year to Quarter 2 of 2016, compared to increases of 1.8% and 1.5% in the year to Quarter 1 of 2016. Real estate activities also had a notable contribution to the increase of the index in the year to Quarter 2 of 2016, increasing by 3.6%.

There was a notable decrease in water supply, sewerage and waste management services where prices fell by 3.7% in the year to Quarter 2 of 2016, compared with a decrease of 6.0% in the year to Quarter 1 of 2016 (Table B and Figure B).

Table B: Annual growth in Services Producer Price Index (percentage change, latest quarter on corresponding quarter of previous year)

| Quarter 2 (Apr to Jun) 2016, United Kingdom | |

| Section | Annual percentage change |

| Water supply, sewerage and waste management | -3.7 |

| Repair and maintenance of motor vehicles | 1.7 |

| Transportation and storage | 0.7 |

| Accommodation and food | 0.0 |

| Information and communication | 1.6 |

| Real estate activities | 3.6 |

| Professional, scientific and technical activities | 1.9 |

| Administrative and support services | -0.2 |

| Education | 2.2 |

| Other services | 1.0 |

| SPPI | 1.2 |

| Source: Services Producer Price Indicies (SPPI) - Office for National Statistics | |

| Notes: | |

| 1. The section level indices are an aggregate of individual industry level indices (excluding Financial Intermediation) published in the SPPI Statistical Bulletin. They do not provide full coverage of the service sector. | |

| 2. Not all of the industry level indices used to construct the section level indices are National Statistics. | |

Download this table Table B: Annual growth in Services Producer Price Index (percentage change, latest quarter on corresponding quarter of previous year)

.xls (25.6 kB)

Figure B: Contribution to Services Producer Price Index annual growth rate

Quarter 2 (Apr to Jun) 2016, UK

Source: Services Producer Price Indices (SPPI) - Office for National Statistics

Notes:

- The section level indices are an aggregate of individual industry level indices (excluding financial intermediation) published in the SPPI statistical bulletin. They do not provide full coverage of the service sector.

- Not all of the industry level indices used to construct the section level indices are National Statistics.

Download this chart Figure B: Contribution to Services Producer Price Index annual growth rate

Image .csv .xlsPrice increases for professional, scientific and technical activities, information and communication, and real estate activities, provided the main contributions to the rise in the SPPI in the year to Quarter 2 of 2016.

Professional, scientific and technical activities prices increased by 1.9% in the year to Quarter 2 of 2016. Prices rose in all indices within this section, but the largest contributions to the rise were seen in business management and consultancy and advertising services. Business management and consultancy prices increased by 3.0% in the year to Quarter 2 of 2016, compared with an increase of 2.8% in the year to Quarter 1 of 2016. This rise is mainly a result of companies increasing their charges for providing human resource consultancy services. Advertising services increased 2.7% in the year to Quarter 2 of 2016, compared with an increase of 0.9% in the year to Quarter 1 of 2016. This increase is due to a rise in the price of media buying services and advertising creation.

Information and communication prices increased 1.6% in the year to Quarter 2 of 2016. Increases in the prices of computer software and book publishing services contributed towards this increase, with prices increasing 1.5% and 3.4% respectively in the year to Quarter 2 of 2016. The increase in computer software prices was due to a rise in the prices for maintenance and support of software systems and applications.

Real estate activities continued to show increases in the year to Quarter 2 of 2016, with prices rising by 3.6%. Real estate agency and property rental prices have both contributed to the increase. Real estate agency prices increased 5.9% in the year to Quarter 2 of 2016, compared with an increase of 10.3% in the year to Quarter 1 of 2016. Property rental prices increased 2.3% in the year to Quarter 2 of 2016, compared with an increase of 1.9% in the year to Quarter 1 of 2016.

Water supply, sewerage and waste management services showed the largest downward contribution within the SPPI. Prices fell 3.7% in the year to Quarter 2 of 2016, compared with a fall of 6.0% in the year to Quarter 1 of 2016, which is the smallest decrease seen in this index since Quarter 4 of 2014. This decrease was largely a result of the fall in prices for sorted recovered materials services, where prices fell 15.5% in the year to Quarter 2 of 2016, up from a decrease of 27.8% in the year to Quarter 1of 2016 (Figure C).

Figure C: Services Producer Price Index for sorted recovered materials services

Quarter 2 (Apr to Jun) 2011 to Quarter 2 (Apr to Jun) 2016, UK

Source: Services Producer Price Indices (SPPI) - Office for National Statistics

Notes:

- Q1 refers to Quarter 1 (January to March), Q2 refers to Quarter 2 (April to June), Q3 refers to Quarter 3 (July to September) and Q4 refers to Quarter 4 (October to December).

Download this chart Figure C: Services Producer Price Index for sorted recovered materials services

Image .csv .xlsThe SPPI increased 1.2% in the year to Quarter 2 of 2016, compared with an increase of 1.3% in the year to Quarter 1 of 2016. Figure D shows how the SPPI sections have contributed towards this 0.1 percentage point change. Decreases in the prices for accommodation and food, real estate activities, and administrative and support services were offset by increases in the prices for water supply, sewerage and waste management, information and communication, professional, scientific and technical services, and transportation and storage.

Figure D: Contribution to the change in the 12-month growth rate between Quarter 1 (Jan to Mar) 2016 and Quarter 2 (Apr to Jun) 2016

Source: Services Producer Price Indices (SPPI) - Office for National Statistics

Notes:

- The section level indices are an aggregate of individual industry level indices (excluding financial intermediation) published in the SPPI statistical bulletin. They do not provide full coverage of the service sector.

- Not all of the industry level indices used to construct the section level indices are national statistics.

- Q1 refers to Quarter 1 (January to March), Q2 refers to Quarter 2 (April to June), Q3 refers to Quarter 3 (July to September) and Q4 refers to Quarter 4 (October to December).

Download this chart Figure D: Contribution to the change in the 12-month growth rate between Quarter 1 (Jan to Mar) 2016 and Quarter 2 (Apr to Jun) 2016

Image .csv .xls

Figure E: Services Producer Price Index by section

Quarter 2 (Apr to Jun) 2012 to Quarter 2 2016, UK

Source: Services Producer Price Indices (SPPI) - Office for National Statistics

Notes:

- Q1 refers to Quarter 1 (January to March), Q2 refers to Quarter 2 (April to June), Q3 refers to Quarter 3 (July to September) and Q4 refers to Quarter 4 (October to December).

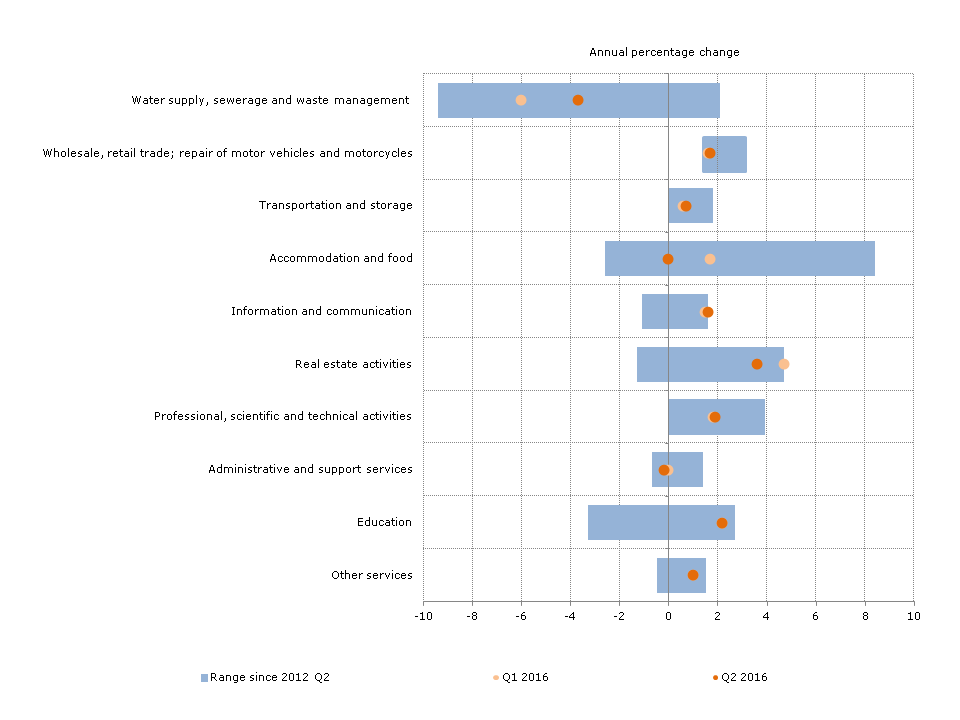

Download this image Figure E: Services Producer Price Index by section

.png (9.4 kB) .xls (29.2 kB){kind=link}

Examining inflation for each of the sections that contribute to the SPPI reveals a diverse set of trends. Figure E shows both the range of annual inflation rates experienced by each of the sections since Quarter 2 of 2012 and the annual rates of inflation for the 2 most recent quarters.

One notable difference between each section is the range of inflation rates that have been experienced since 2012. Water supply, sewerage and waste management services, accommodation and food, and real estate activities have experienced a relatively wide range of inflation rates over this period. Although all sections have experienced some variance in inflation, certain industries have experienced inflation consistently higher than others. Vehicle repair and maintenance has not experienced inflation lower than 1.6% at any point in the past 5 years, while administrative and support services have not experienced inflation higher than 1.4%.

Back to table of contents5. Quarterly inflation

Prices received for the services included in the Services Producer Price Index rose 0.3% between Quarter 1 and Quarter 2 of 2016, compared with an increase of 0.5% between Quarter 4 of 2015 and Quarter 1 of 2016. Of the 10 sections that make up the SPPI, 9 showed increases in prices between Quarter 1 and 2 of 2016.

The largest increase in the quarterly rate came from water supply, sewerage and waste management, which increased by 2.9% between Quarters 1 and 2 of 2016 (Table C and Figure F).

Table C: Quarterly growth in Services Producer Price Index (percentage change, latest quarter on previous quarter)

| Quarter 2 (Apr to Jun) 2016, United Kingdom | |

| Section | Quarterly percentage change |

| Water supply, sewerage and waste management | 2.9 |

| Repair and maintenance of motor vehicles | 0.6 |

| Transportation and storage | 0.2 |

| Accommodation and food | 0.5 |

| Information and communication | 0.2 |

| Real estate activities | 0.6 |

| Professional, scientific and technical activities | 0.4 |

| Administrative and support services | 0.0 |

| Education | 0.2 |

| Other services | 0.3 |

| SPPI | 0.3 |

| Source: Services Producer Price Indicies (SPPI) - Office for National Statistics | |

| Notes: | |

| 1. The section level indices are an aggregate of individual industry level indices (excluding Financial Intermediation) published in the SPPI Statistical Bulletin. They do not provide full coverage of the service sector. | |

| 2. Not all of the industry level indices used to construct the section level indices are National Statistics. | |

Download this table Table C: Quarterly growth in Services Producer Price Index (percentage change, latest quarter on previous quarter)

.xls (25.6 kB)

Figure F: Contribution to Services Producer Price Index quarterly growth

Quarter 2 (Apr to Jun) 2016, UK

Source: Services Producer Price Indices (SPPI) - Office for National Statistics

Notes:

- The section level indices are an aggregate of the individual industry level indices (excluding financial intermediation) published in the SPPI statistical bulletin. They do not provide full coverage of the section listed.

- Not all of the industry level indices used to construct the section level indices are National Statistics.

Download this chart Figure F: Contribution to Services Producer Price Index quarterly growth

Image .csv .xlsProfessional, scientific and technical activities showed the largest contribution to the SPPI rate between Quarters 1 and 2 of 2016, with prices rising by 0.4%, compared with an increase of 1.1% between Quarter 4 of 2015 and Quarter 1 of 2016. The main contributions to this increase were from advertising prices, and engineering services which increased by 1.9% and 1.0%, respectively, between Quarters 1 and 2 of 2016. The movement in advertising prices was driven by media planning and buying. The increase in engineering services prices was driven by civil, structural and other engineering services.

Back to table of contents6. Economic context

Comparison with average weekly earnings

The Services Producer Price Index (SPPI) captures changes in the prices received by UK business for the provision of a selection of services to other UK businesses and the public sector. For many services, the cost of labour is the largest component of the price charged by businesses for providing the service, rather than the cost of goods or fuels. As a result, a change in the wage structure of the workforce can have an important impact on the SPPI. It is expected that the price charged for services should move in a similar way to the wages received by the UK workforce. Figure G shows the annual percentage change of the fees received by UK businesses for the provision of services, as estimated by the SPPI, with an indicator of salaries received by the UK workforce who are employed in the service sector, as estimated by the average weekly earnings (AWE) “services” pay index (excluding bonuses).

Figure G: Comparison of Services Producer Price Index and "services" Average Weekly Earnings Index

Quarter 2 (Apr to Jun) 2003 to Quarter 2 (Apr to Jun) 2016, UK

Source: Services Producer Price Indices (SPPI) and Annual Weekly Earnings (AWE) – Office for National Statistics

Notes:

- The SPPI includes the water supply; sewerage and waste management sector not included in the AWE.

- The AWE index includes financial and insurance activities, public administration and defence; compulsory social security, human health and social work activities and arts, entertainment and recreation sectors not included in the SPPI.

- Q1 refers to Quarter 1 (January to March), Q2 refers to Quarter 2 (April to June), Q3 refers to Quarter 3 (July to September) and Q4 refers to Quarter 4 (October to December).

Download this chart Figure G: Comparison of Services Producer Price Index and "services" Average Weekly Earnings Index

Image .csv .xlsFigure G shows the growth rates of both wages and services prices slowed considerably during 2008 and 2009, with services inflation falling from an average of 3.5% in 2008 to minus 0.8% in 2009, while growth in services wages slowed from 3.9% to 1.8% on average during the same period. Following the downturn, services prices and wages have followed similar trends, diverging slightly during 2015, as wages grew faster than services prices from the end of 2014. Looking at the most recent data, earnings have continued to grow faster than services producer prices, with services wages growing by 1.9% in Quarter 2 of 2016, compared to services prices, which had grown by 1.2% over the same period.

Although labour cost is a significant factor determining services output prices, competitive pressures will also have some bearing on services prices. As wage growth has picked up during 2014 and 2015, on-going competitive pressures in the services market may have limited the extent to which businesses can pass on those increasing labour costs.

The rise in service sector wage growth reflects some wider tightening in the UK labour market. Following strong employment growth over the past 2 years, the unemployment rate among those aged 16 and above fell to 4.9% in the 3 months to June 2016, below the pre-downturn (2000 to 2007) average of 5.1%. The employment rate rose further to 74.5% in the 3 months to June 2016 for those aged between 16 and 64, which is the highest rate since comparable records began.

In parallel with the fall in the unemployment rate, labour demand (as measured by the number of vacancies) has been relatively strong. The number of unemployed people per vacancy has fallen quite considerably since 2011, from 5.8 in the 3 months to December 2011 to 2.2 in the 3 months to June 2016, indicating that there are fewer unemployed workers for each vacancy. In relation to the services industry, the number of vacancies has been rising since mid-2012 and increased by 2.9% in the 3 months to June 2016, compared with a year earlier.

While the tightening labour market may be exerting upward pressure on wages, the productivity of labour also influences wage growth. Improvements in productivity creates capacity for output to rise faster than the corresponding rise in inputs, thereby allowing firms to produce more output per unit of labour employed. Productivity growth allows for output prices to rise more gradually, all else being equal. Unit labour costs in the services sector – which measures the labour cost per unit of output produced – increased by 0.1% in Quarter 1 of 2016 compared with the previous quarter. This was slightly higher than the quarterly growth in unit labour cost in Quarter 4 of 2015, which contracted by 0.2%. This could indicate labour costs exerting upward pressure on services prices.

While there are a number of factors affecting services prices, the demand for goods and services in the UK economy could also have an impact on services prices. The latest estimate has shown GDP increasing by 0.6% in Quarter 2 of 2016, compared with 0.4% in the previous quarter. Much of this growth has been concentrated in the services industry, with services output increasing by 0.5%, only slightly slower than growth in the previous quarter, which was 0.6%.

Comparison with Consumer Price Index

While the SPPI measures the amount received by a company for services they’ve provided to other businesses, the prices paid by households is estimated by the Consumer Price Index (CPI). While the costs associated with providing services to both businesses and households will be broadly similar, there may be different costs associated with providing services to different customers. Figure H shows a comparison with the “all services” sector of the Consumer Prices Index (CPI) which measures the prices paid for services by households.

Figure H: Comparison of Services Producer Price Index and “all services” Consumer Price Index

Quarter 2 (Apr to Jun) 2003 to Quarter 2 (Apr to Jun) 2016, UK

Source: Services Producer Price Indices (SPPI) and Consumer Price Index (CPI) – Office for National Statistics

Notes:

- SPPI measures changes in the price received by a company, CPI measures changes in the price paid by a consumer. Therefore CPI figures may include taxes and fees that are not retained by the service provider.

- SPPI measures the price received for services provided by UK-based suppliers only, excluding imports from non-UK suppliers. CPI aims to measure the price paid by consumers in the UK, who may use non-UK based suppliers.

- SPPI uses standard industrial classification 2007 (SIC 07) to produce its aggregate, CPI uses classification of individual consumption according to purpose (COICOP). This means that the structure of each index may not always correlate at more detailed levels.

- Q1 refers to Quarter 1 (January to March), Q2 refers to Quarter 2 (April to June), Q3 refers to Quarter 3 (July to September) and Q4 refers to Quarter 4 (October to December).

Download this chart Figure H: Comparison of Services Producer Price Index and “all services” Consumer Price Index

Image .csv .xlsGenerally inflation in the CPI “all services” index runs at a higher rate than the SPPI. Between late 2005 and 2008 the gap between the SPPI and CPI annual rate of inflation narrowed before widening again from 2009 to present. During the economic downturn in 2008 to 2009, the annual rate of inflation for both indices decreased, with prices falling by as much as 1.6% for services sold by UK businesses, while the prices paid by households continued to grow, although at a much lower rate, reaching a low of 2.3% in Quarter 4 of 2009. Since Quarter 4 of 2010 both indices have shown growth; however, the SPPI has shown significantly lower growth than CPI.

Other measures of service sector inflation

There are other measures of service sector inflation available such as the Chartered Institute of Procurement and Supply (CIPS) Purchasing Managers’ Index and the Confederation of British Industry (CBI) Service Sector Survey. There are significant methodological differences between these surveys and SPPI; therefore, direct comparisons cannot be made.

International comparison

All countries within the European Union are required to produce a measure of producer price inflation for the services sector under the Short Term Statistics Regulation. Figure J shows the growth rates of service producer prices for a selection of EU countries from Quarter 1 of 2011 to Quarter 1 of 2016; this is the latest comparable data available for most of the countries represented.

The UK and Sweden recorded largely stable service producer price indices, growing by 1.5% and 1.0% respectively over the total period, whereas Austrian prices increased more rapidly. These experiences contrast with France and Spain. France experienced negative SPPI inflation until Quarter 2 of 2015 and Spain experienced negative SPPI inflation until Quarter 1 of 2015 and again in Quarter 1 of 2016.

Figure I: Services Producer Price Index international comparison

Quarter 1 (Jan to Mar) 2011 to Quarter 1 (Jan to Mar) 2016, UK and selected EU countries

Source: Eurostat

Notes:

- The UK growth in this chart does not match that published as the gross sector SPPI. This is because the indices shown in this comparison only include sections G to N, as per the standard industrial classification 2007 (SIC 07). The gross sector SPPI also includes industries classified to sections E and G of SIC 07. A full list of all SIC codes included can be found in the SPPI coverage document.

- Q1 refers to Quarter 1 (January to March), Q2 refers to Quarter 2 (April to June), Q3 refers to Quarter 3 (July to September) and Q4 refers to Quarter 4 (October to December).

Download this chart Figure I: Services Producer Price Index international comparison

Image .csv .xlsFrance and Spain experienced the lowest average inflation rates across the period between Quarter 1 2011 and Quarter 1 2016, with both countries witnessing falling prices for extended periods. More recently, France witnessed a rise in prices between Quarter 3 (July to Sept) 2015 and Quarter 1 2016 and Spain between Quarters 2 and 4 of 2015, although Spain then saw prices fall again in Quarter 1 2016. Austria experienced the highest average inflation rate across the period, ranging from a high of 2.6% in Quarter 4 of 2011and a low of 0.9% in Quarter 3 of 2015.

Back to table of contents7. Net sector

At the aggregate level, both a net and gross sector Services Producer Price Index (SPPI) is produced. The prices used to construct both of these indices are the same, but different weights are used to construct the net sector index compared with the gross sector.

Summary of net sector movements

In Quarter 2 of 2016, movements in the net sector SPPI were:

- annual inflation rose 1.2%, unchanged from the year to Quarter 1 of 2016

- between Quarters 1 and 2 of 2016, quarterly inflation stood at 0.3%, compared with 0.5% between Quarter 4 of 2015 and Quarter 1 of 2016

Generally, the movements of the net sector SPPI are similar to those of the gross sector indices (Figure J).

Figure J: Services Producer Price Index (net and gross sectors)

Quarter 2 (Apr to Jun) 2003 to Quarter 2 (Apr to Jun) 2016, UK

Source: Services Producer Price Indices (SPPI) - Office for National Statistics

Notes:

- The SPPI is an aggregate of the individual industry level indices (excluding Financial Intermediation) published in the SPPI statistical bulletin. It does not provide full coverage of the service sector.

- Not all of the industry level indices used to construct the SPPI are National Statistics.

- Q1 refers to Quarter 1 (January to March), Q2 refers to Quarter 2 (April to June), Q3 refers to Quarter 3 (July to September) and Q4 refers to Quarter 4 (October to December).