Table of contents

- Main points

- Things you need to know about this release

- The total UK trade deficit narrowed by £2.1 billion to £6.2 billion in the three months to November 2017

- The narrowing of the trade in goods deficit was due to an increase in exports to non-EU countries, while exports to EU countries were relatively unchanged in the three months to November 2017

- Increase in goods export volumes had the largest impact on the narrowing of the trade in goods deficit in the three months to November 2017

- The total UK trade deficit widened by £0.5 billion between October 2017 and November 2017

- What are the revisions to trade values since our last release?

- Links to related statistics

- Quality and methodology

1. Main points

The total UK trade (goods and services) deficit narrowed by £2.1 billion to £6.2 billion in the three months to November 2017; excluding erratic commodities, the total deficit narrowed by £1.2 billion to £6.1 billion.

The £2.1 billion narrowing of the total trade deficit (goods and services) was due to a £1.2 billion narrowing of the trade in goods deficit; this was a result of increases in exports including works of art and cars, and a £0.9 billion widening of the trade in services surplus due to increases in exports.

The narrowing of the trade in goods deficit was due to a 5.3% (£2.3 billion) increase in exports to non-EU countries, partially offset by increases in imports, in the three months to November 2017.

A 1.9% increase in goods export volumes had a larger impact on the narrowing of the trade in goods deficit, in comparison with prices, in the three months to November 2017.

The UK total trade deficit (goods and services) widened by £0.5 billion between October 2017 and November 2017, due primarily to an increase in goods imports of fuels (mainly oil) from non-EU countries.

The UK total trade deficit (goods and services) narrowed by £4.3 billion between the three months to November 2016 and the three months to November 2017; this was due primarily to a 10.6% (£8.4 billion) increase in goods exports, which was higher than the increase in goods imports.

The downward revision to goods exports by £1.4 billion in October 2017 was mainly due to downward revisions to unspecified goods (including non-monetary gold) and fuels.

2. Things you need to know about this release

Unless otherwise stated, all trade values discussed in this release are in current prices. The time series dataset also includes chained volume measures (series for which the effects of inflation have been removed) and these are indexed to form the volume series presented in the publication tables.

Data are supplied by over 30 sources, including several administrative sources; HM Revenue and Customs (HMRC) covering trade in goods is the largest. For trade in services, data are less timely than trade in goods estimates and are sourced mainly from survey data and a variety of administrative sources. The services data are processed quarterly, so monthly forecasts are made to provide a complete trade total. The most recent monthly data can therefore be considered more uncertain.

Trade statistics for any one month can be erratic. For that reason, we recommend comparing the latest three months against the preceding three months and the same three months of the previous year.

Oil and other “erratic” commodities can make a large contribution to trade in goods, but often mask the underlying trend in the export or import values due to their volatility. The “erratics” series includes ships, aircraft, precious stones, silver and non-monetary gold. Non-monetary gold can have a particularly large impact on growth rates, due to the large volumes of gold traded on the London markets. Therefore, we also publish data exclusive of these commodities, which may provide a better guide to the emerging trade picture.

In accordance with the National Accounts Revisions Policy, data in this release have been revised from January 2016 to October 2017 for services and for October 2017 for goods data.

The UK Statistics Authority suspended the National Statistics designation of UK trade on 14 November 2014. We have now responded to all of the specific requirements of the reassessment of UK trade and are in the final stages of providing evidence to the Authority. We are undertaking a programme of improvements to UK trade statistics in line with the UK trade development plan that will also address anticipated future demands. While delivering against this plan, we will continue to work with the Office for Statistics Regulation team to regain National Statistics status for UK trade statistics. We welcome feedback on this development plan.

Back to table of contents3. The total UK trade deficit narrowed by £2.1 billion to £6.2 billion in the three months to November 2017

The total trade (goods and services) deficit narrowed by £2.1 billion to £6.2 billion in the three months to November 2017 (Figure 1). This was due mainly to goods exports, which increased 2.6% (£2.2 billion) to £87.6 billion. Unspecified goods (particularly non-monetary gold), and machinery and transport equipment were the largest contributors to the increase in exports, as both increased by £1.0 billion in the three months to November 2017.

When erratic commodities are excluded, the value of the total UK trade deficit narrowed by £1.2 billion to £6.1 billion in the three months to November 2017. The narrowing was due primarily to trade in goods exports increasing 2.1% (£1.7 billion) to £81.7 billion, alongside a 1.2% (£0.8 billion) increase in trade in services exports. Although trade in goods imports increased 1.2% (£1.4 billion) to £116.0 billion, the increase in exports was larger, therefore the total trade deficit excluding erratic commodities narrowed.

The main commodity contributors to the increase in exports excluding erratic commodities were works of art manufactures, cars and mechanical machinery, which increased 43.3% (£0.5 billion), 3.8% (£0.3 billion) and 3.6% (£0.4 billion) respectively. Some of the increases in exports were offset by a decrease of 5.1% (£0.7 billion) in chemical exports.

Over the last year, the UK’s total trade deficit (goods and services) narrowed by £4.3 billion between the three months to November 2016 and the three months to November 2017. This was due primarily to increases in goods and services exports, by 10.6% (£8.4 billion) and 6.7% (£4.4 billion) respectively. Although imports of goods and services increased, by 6.1% (£7.0 billion) and 3.7% (£1.5 billion) respectively, these increases were offset by the larger increases in goods and services exports.

Figure 1: Three-month on three-month UK trade balances, May 2013 to November 2017

Source: Office for National Statistics

Download this chart Figure 1: Three-month on three-month UK trade balances, May 2013 to November 2017

Image .csv .xls4. The narrowing of the trade in goods deficit was due to an increase in exports to non-EU countries, while exports to EU countries were relatively unchanged in the three months to November 2017

The UK trade in goods deficit narrowed by £1.2 billion to £34.4 billion in the three months to November 2017. This was due primarily to a 2.6% (£2.2 billion) increase in goods exports to £87.6 billion.

The increase in goods exports was mainly due to non-EU export trade, which increased 5.3% (£2.3 billion) to £44.7 billion, while non-EU imports increased 1.6% (£0.9 billion) to £55.8 billion between the three months to August 2017 and the three months to November 2017. As exports increased by more than imports, the deficit with non-EU countries narrowed by £1.4 billion to £11.0 billion. This follows a £4.1 billion widening of the deficit in the three months to August 2017, when exports decreased as imports increased.

Figure 2 shows the contribution of goods exports to total EU and non-EU exports in the three months to November 2017. The increase in exports to non-EU countries was due to machinery and transport equipment (£0.8 billion), unspecified goods (£0.7 billion) including non-monetary gold, and miscellaneous manufactures (£0.7 billion).

The main contributors to non-EU machinery and transport equipment exports were cars and mechanical machinery, which increased 8.5% (£0.4 billion) and 2.4% (£0.2 billion) respectively. Of miscellaneous manufactures, works of art manufacture (particularly painting and sculpture) exports was the largest contributor, increasing by 45.6% (£0.5 billion).

While exports to EU countries increased for certain goods, such as unspecified goods, material manufactures and mechanical machinery, other commodity exports fell, particularly fuel and chemicals, meaning exports overall were relatively unchanged at £42.9 billion. Imports from the EU increased 0.3% (£0.2 billion) meaning the deficit with EU countries widened by £0.2 billion to £23.3 billion. This follows three consecutive three-month periods when the deficit narrowed.

Figure 2: Contribution of goods exports to total EU and non-EU exports, three-months to November 2017 on previous three-months to August 2017

Source: Office for National Statistics

Download this chart Figure 2: Contribution of goods exports to total EU and non-EU exports, three-months to November 2017 on previous three-months to August 2017

Image .csv .xlsFigure 3 shows the contribution of goods imports to total EU and non-EU imports in the three months to November 2017. Imports of goods from non-EU countries increased 1.6% (£0.9 billion) to £55.8 billion, while imports from EU countries increased 0.3% (£0.2 billion) to £66.2 billion in the three months to November 2017. The increases in imports from both non-EU and EU countries were due primarily to fuel commodities (particularly oil), which increased by £1.1 billion and £0.4 billion respectively.

Figure 3: Contribution of goods imports to total EU and non-EU imports, three-months to November 2017 on previous three-months to August 2017

Source: Office for National Statistics

Download this chart Figure 3: Contribution of goods imports to total EU and non-EU imports, three-months to November 2017 on previous three-months to August 2017

Image .csv .xlsWhen excluding erratic commodities, the latest three-month trends are unchanged for both the non-EU and EU trade in goods deficits. The non-EU trade deficit narrowed by £0.9 billion to £9.5 billion, while the EU deficit widened by £0.6 billion to £24.8 billion between the three months to August 2017 and the three months to November 2017.

Back to table of contents5. Increase in goods export volumes had the largest impact on the narrowing of the trade in goods deficit in the three months to November 2017

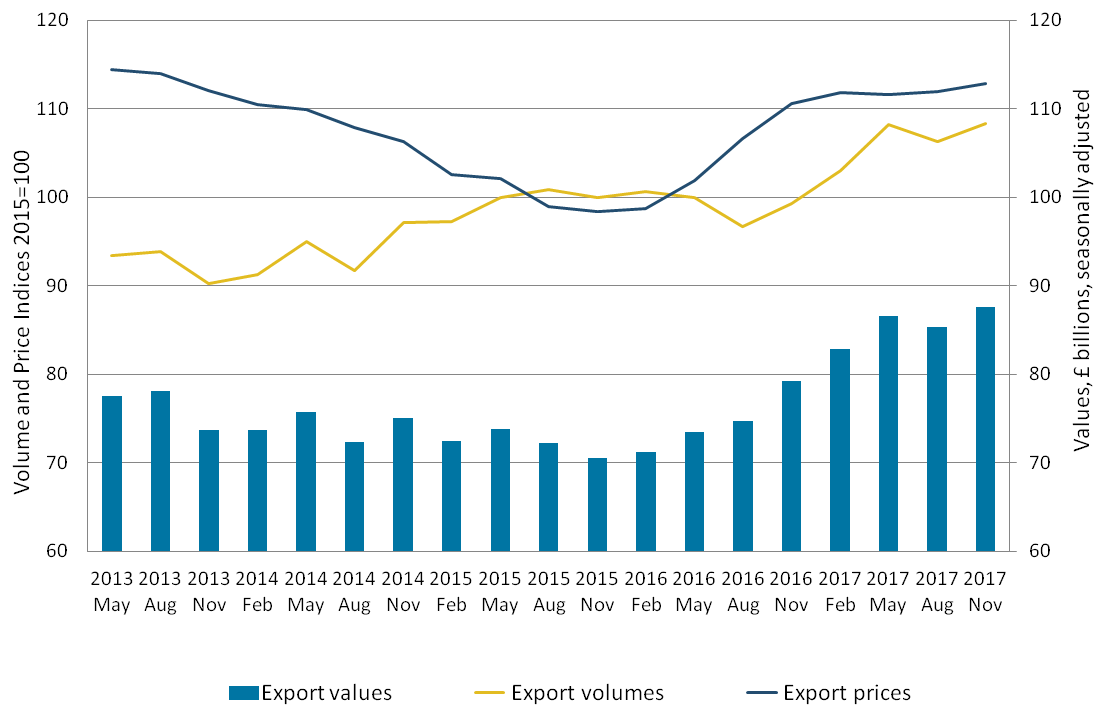

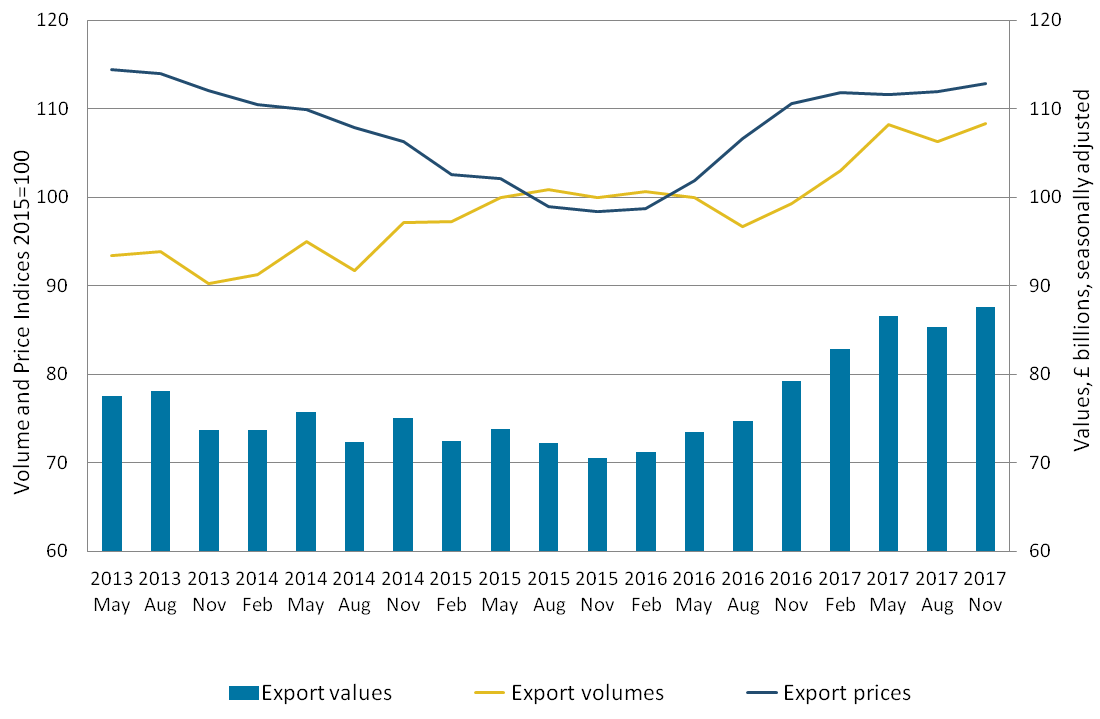

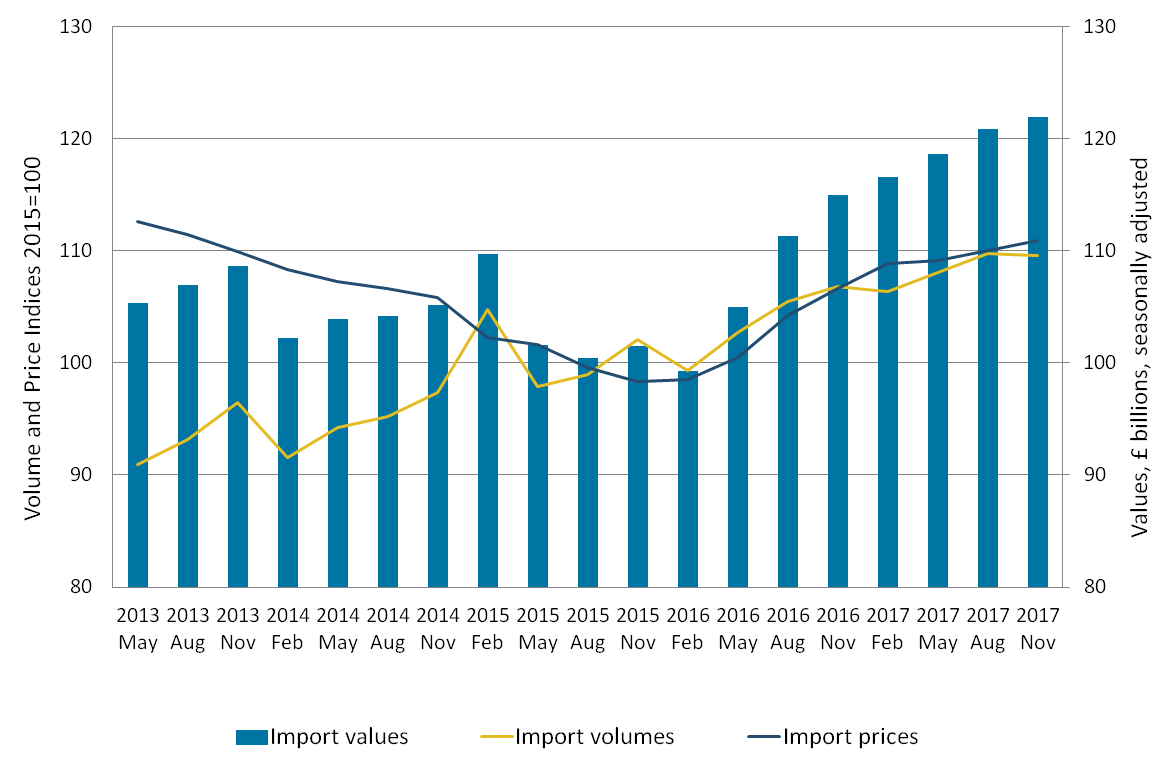

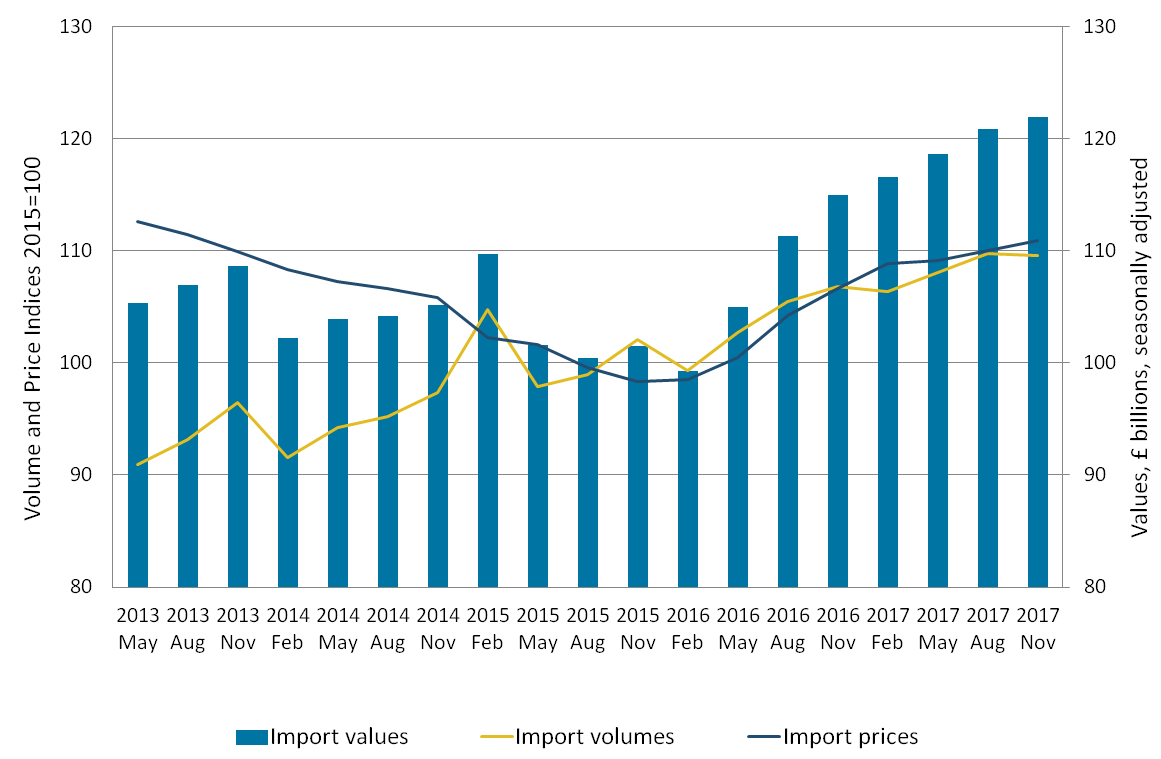

Figures 4 and 5 show three-month on three-month UK goods export and import values, volumes and prices respectively from May 2013 to November 2017.

The £2.2 billion (2.6%) increase in the value of total goods exports to £87.6 billion in the three months to November 2017 was due primarily to volume increases. Total goods export volumes increased 1.9% in the three months to November 2017, which followed a 1.8% decrease in export volumes in the three months to August 2017.

Export and import prices increased 0.9% and 0.8% respectively in the three months to November 2017. The £1.1 billion (0.9%) increase in goods import values to £122.0 billion was due to price movements, as import volumes decreased 0.2% following two consecutive increases.

The combined effect of export volumes increasing more than import volumes, while prices were relatively flat, was a £1.2 billion narrowing of the trade in goods deficit to £34.4 billion. This coincides with an increase in the value of sterling in the three months to November 2017.

While simple economic theory suggests an increase in the value of sterling should result in an increase in export prices (exports decreasing in competitiveness) and a decrease in import prices, in practice the impact of a sterling change is likely to be much more complex. Our Economic review has detailed the economic theory of the expected impact of sterling exchange rate movements on export and import volumes and prices.

Although the increase in import prices may appear contrary to economic theory, while increases in export prices are in line with economic theory, it is important to note that export prices are reported in sterling for the UK rather than foreign currency terms. As detailed in the Economic review, changes in prices (on a sterling basis) are likely to be largely attributable to the amount of trade conducted on a foreign currency basis (with EU and non-EU countries) as price changes are lagged in the short-term – therefore, it is possible there may be no change in the price in foreign currency terms.

Figure 4: Three-month on three-month UK goods export values, volumes and prices, May 2013 to November 2017

Source: Office for National Statistics

Download this image Figure 4: Three-month on three-month UK goods export values, volumes and prices, May 2013 to November 2017

.png (42.3 kB) .xls (24.6 kB){kind=link}

Figure 5: Three-month on three-month UK goods import values, volumes and prices, May 2013 to November 2017

Source: Office for National Statistics

Download this image Figure 5: Three-month on three-month UK goods import values, volumes and prices, May 2013 to November 2017

.png (50.4 kB) .xls (24.6 kB){kind=link}

The volume of goods exported to and imported from non-EU countries increased 5.2% and 0.2% respectively, while non-EU export prices decreased 0.2% and import prices increased 1.1%. When excluding oil, non-EU export and import prices decreased 1.0% and 1.1% respectively, which coincides with total fuels (mainly oil) export and import sterling prices increasing 17.1% and 14.2% respectively in the three months to November 2017.

Over the same period, the volume of goods exported to and imported from other EU countries decreased 1.4% and 0.4% respectively in the three months to November 2017, while EU export and import prices increased 1.9% and 0.5% respectively. When excluding oil, EU export and import prices remained flat, which coincides with total fuels (mainly oil) export and import sterling prices in the three months to November 2017.

The value increase in fuel imports (mainly oil) from EU and non-EU countries, 16.9% (£0.4 billion) and 14.4% (£1.1 billion) respectively, had a large impact on the 0.9% (£1.1 billion) increase in total trade in goods imports. This was due mainly to a 14.2% increase in total fuels import prices while volumes were flat.

As a result of the large increase in non-EU export volumes (alongside smaller decreases in EU import volumes and import prices), trade with non-EU countries had a large contribution to the total trade in goods deficit narrowing (by £1.2 billion to £34.4 billion).

Back to table of contents6. The total UK trade deficit widened by £0.5 billion between October 2017 and November 2017

The total trade (goods and services) deficit widened by £0.5 billion to £2.8 billion between October 2017 and November 2017. This is due primarily to trade in goods imports increasing 2.1% (£0.8 billion) to £41.3 billion. The increase in trade in goods imports was mainly a result of unspecified goods imports (£0.8 billion) including non-monetary gold and fuels (£0.6 billion) largely from non-EU countries.

Excluding erratic commodities, the total trade deficit widened by £0.6 billion to £2.4 billion between October 2017 and November 2017. This was due mainly to a 2.8% (£1.1 billion) increase in goods imports to £39.1 billion. The main contributor to the increase in imports was a 15.9% (£0.4 billion) increase in imports of fuels (mainly oil) from non-EU countries.

Back to table of contents7. What are the revisions to trade values since our last release?

In accordance with the National Accounts Revisions Policy, services data in this release have been revised from January 2016 and trade in goods data have been revised for October 2017.

Revisions to the total trade balance (goods and services) as a result of services data revisions are relatively small and mainly upward (narrowing of the deficit) from January 2016 to October 2017, although April to June 2017 saw downwards services revisions, with the largest downward revision occurring in May 2017 (£0.04 billion). Services revisions from January 2016 to October 2017 are mainly due to revisions to services exports.

The trade in goods revision in October 2017 is largely due to downward revisions of £1.4 billion to exports. This is due mainly to downward revisions to unspecified goods (including non-monetary gold) and fuels, by £0.9 billion and £0.3 billion respectively. Revisions to goods imports were down by £0.5 billion, due mainly to a £0.4 billion downward revision to finished manufactures imports.

The downward revisions in goods exports were partially offset by downward revisions to goods imports and upward revisions to the trade in services surplus (by £0.03 billion) in October 2017. This resulted in a downward revision to the total trade balance by £0.9 billion over the period.

Back to table of contents9. Quality and methodology

Trade is measured through both imports and exports of goods and/or services. Data are supplied by over 30 sources including several administrative sources, HM Revenue and Customs (HMRC) being the largest.

This monthly release contains tables showing the total value of trade in goods together with index numbers of volume and price. Figures are analysed by broad commodity group (values and indices) and according to geographical area (values only). In addition, the UK trade statistical bulletin also includes early monthly estimates of the value of trade in services.

Further qualitative data and information can be found in the attached datasets. This includes data on:

Detailed methodological notes are published in the UK Balance of Payments, The Pink Book 2017.

The UK trade methodology web pages have been developed to provide detailed information about the methods used to produce UK trade statistics.

The UK trade Quality and Methodology Information report contains important information on:

the strengths and limitations of the data and how it compares with related data

uses and users of the data

how the output was created

the quality of the output including the accuracy of the data