1. Overview

Public sector net worth (PSNW) is a statistical aggregate summarising the total value of the public sector’s assets (both financial and non-financial) and its liabilities. It is more comprehensive than either the headline balance sheet aggregate, public sector net debt (PSND), or the supplementary aggregate public sector net financial liabilities (PSNFL).

PSNW is part of a set of internationally-recognised statistical aggregates that can be used to analyse the public sector finances. However, as there are different statistical frameworks and different analytical presentations within those frameworks, there are also several different versions of PSNW. The Office for National Statistics (ONS) currently produces two measures of PSNW, and we are working on a further measure that would be fully consistent with the headline fiscal aggregates published in the Public Sector Finances (PSF) bulletin.

This section outlines the rationale for introducing the new measure and describes how it will relate to existing fiscal aggregates and alternative measures of PSNW. Details of the new measure are laid out in Section 2, while Section 3 highlights additional data work required for its implementation.

Existing fiscal aggregates

The monthly PSF bulletin is the main statistical release relating to the public finances in the UK and is used by government and others to monitor the UK’s fiscal position. It is designated National Statistics status and is produced in accordance with the international statistical framework, the European System of Accounts 2010 (ESA 2010), an adaptation of the United Nations’ System of National Accounts 2008. Full details of the measures included in the PSF statistics and the associated methodology can be found in the PSF Methodological Guide.

Our PSF statistics contain two aggregates relating to the public sector balance sheet (that is, the stocks of assets and liabilities held by the public sector): PSND and a supplementary measure known as PSNFL. PSND is the narrower of these measures and is calculated as the value of the public sector’s loan liabilities, debt securities, currency and deposit holdings minus the value of the public sector’s liquid financial assets (mainly foreign exchange reserves and cash deposits). PSNFL is broader and includes all public sector financial assets and liabilities that are recognised in the national accounts, such as the liabilities associated with funded pension schemes or provisions for calls under standardised guarantee schemes.

In addition to these stock aggregates, the PSF statistics include a set of flow aggregates and their components (such as tax revenue collected by the government). These flows are conceptual counterparts of the balance sheet aggregates and are methodologically consistent, allowing for integrated analysis of stocks and flows. Although not all movements in balance sheet aggregates are explained by the flow aggregates – as other factors such as changes in the value of an asset or liability can also result in changes to the stock – together these statistics provide insights into the financial position of the public sector.

Rationale for public sector net worth

Although PSNFL is broader than PSND, it is not a comprehensive indicator of the public sector’s stock of assets and liabilities because it excludes non-financial assets, such as the road network or buildings owned by government. In flow terms, PSNFL captures the incurrence of a liability to pay for, for example, a new building, but it does not capture the counterpart acquisition of the building itself. A measure of public sector net worth (PSNW) would fill this gap, being an exhaustive aggregate (within the bounds of the relevant statistical framework) of the public sector’s financial and non-financial assets minus the total value of public sector liabilities1. As such, PSNW can provide a fuller picture of long-term fiscal sustainability and capture the impact of a wider range of government activities.

It is important to note that PSNW would not replace existing fiscal aggregates but would be used alongside them, allowing for a complete and integrated presentation of public sector finance statistics from opening to closing balance sheet. In this context, consistency with PSF flow estimates and other stock aggregates is important and this influences how we choose to measure PSNW, as described in the following section.

Ways of measuring public sector net worth

PSNW is an internationally-accepted statistical aggregate, but there are different approaches to its measurement within the overarching statistical framework, reflecting different analytical needs. The ONS already publishes two measures labelled PSNW, in the National Balance Sheet (NBS) and in supplementary statistics consistent with the International Monetary Fund’s Government Finance Statistics Manual 2014 (IMF GFSM). This section explains how these measures differ from the core public sector finance statistics and why an additional measure will be useful.

Differences in purpose, methodology and scope mean that neither the NBS statistics nor the IMF GFSM statistics are fully consistent with the main PSF statistics. Consequently, the measures of PSNW that come from them cannot be integrated with either the flows or other stock aggregates that come from the core PSF statistics. The reasons for these differences are summarised below. Section 2 then expands on the planned methodology for a PSF-consistent measure of PSNW.

Public sector net worth in the UK National Accounts

NBS forms part of the UK National Accounts suite of outputs and provides data on stocks of assets and liabilities for the whole of the UK economy. Although general government (made up of central and local government) is the standard sector used for analysis in National Accounts, tables are also provided for the public sector, including public sector net worth. The NBS is produced on a similar conceptual basis to the core PSF statistics but is subject to the persistent technical differences that exist between the UK National Accounts and PSF statistics. These differences stem from different application of public sector boundary (the UK National Accounts do not separately identify public financial corporations and only include non-financial corporations within the public sector). They also stem from different approaches to revisions and reclassifications, and different valuation bases for liabilities (the NBS values debt securities at market value compared with face value in the PSF statistics).

Public sector net worth based on the International Monetary Fund’s Government Finance Statistics Manual 2014

A measure of PSNW consistent with IMF GFSM is also released as experimental statistics within the PSF suite of tables. It aligns with the PSF revisions policy and mostly aligns with the application of the public sector boundary. However, it is based on an alternative international framework and is not a direct extension of PSND and PSNFL. In particular, PSNW in the IMF GFSM supplementary statistics includes unfunded pensions liabilities and certain public-private partnerships that are not recognised on the public sector balance sheet under ESA 2010. There are also differences in valuation; debt securities are recorded at market value in the GFSM-consistent measure of PSNW compared with face value in the core PSF statistics (although supplementary valuations of debt at nominal and face value are provided in the GFSM-consistent tables).

It should be noted that the GFSM guidance is less detailed and allows a broader interpretation than the more comprehensive manuals accompanying ESA 2010, on which PSF statistics are based. In compiling our GFSM-consistent statistics, we make use of the detailed ESA 2010 guidance in areas where no contradictions with GFSM exist. This ensures consistency in classifications and methodology between the two sets of statistics.

Notes for: Overview

- Note that this results in PSNW taking the opposite sign from PSNFL and PSND, with a positive value showing more assets than liabilities, whereas a positive value of PSNFL or PSND implies a greater stock of liabilities than assets.

2. New measure of public sector net worth

The substantial differences between existing measures of public sector net worth (PSNW) and the fiscal aggregates complicate comparisons between them. We therefore plan to develop a measure of PSNW that would be a direct extension of public sector net financial liabilities (PSNFL) and public sector net debt (PSND) and would be fully comparable with existing stock and flow estimates. This would complete our suite of European System of Accounts 2010 (ESA 2010)-based public finance statistics (as illustrated in Figure 1). The new measure would also incorporate improved data, addressing some of the issues faced by existing measures (see Section 3).

The following subsections outline some key aspects of the methodology for the new measure of PSNW, covering:

- the underlying statistical framework and approach to revisions

- how the public sector boundary will be defined

- the types of assets and liabilities in scope

- valuation of debt instruments

- presentation and periodicity of the new measure

- a summary of the differences between the new and existing measures of PSNW

In most respects, the new measure will follow the existing balance sheet aggregate, PSNFL, but with the addition of non-financial assets.

Statistical framework

The UK’s core fiscal statistics are conceptually based on the UK National Accounts (while maintaining some technical differences), which are in turn based on the ESA 2010 framework. The new measure will be compliant with ESA 2010 – as is the existing National Balance Sheet (NBS) aggregate – but will also be consistent with the public sector finance (PSF) statistics in its approach to revisions, sector boundary, valuation and other factors contributing to the misalignment between the PSF and National Accounts outputs.

Public sector boundary

In line with the sector coverage of the PSF statistics, the new measure would include the assets and liabilities of central government, local government, public non-financial corporations and public financial corporations (including funded public sector pension schemes and the Bank of England). As is the case for existing fiscal aggregates, we would follow ESA 2010 guidance on the classification of assets and liabilities associated with public-private partnerships (PPPs) to the public sector; this is somewhat more restrictive than international financial accounting standards.

There is potential for flexibility regarding the inclusion of public sector banks – a sub-type of public financial corporations – in the measure. Certain banks were brought into public sector ownership following the 2008 financial crisis, and were excluded from the main fiscal aggregates, such as PSND, so that the conventional fiscal metrics were not distorted by such a large scale but temporary fiscal intervention. Most banks have reverted to private ownership and the only remaining banking group within the public sector is the NatWest Group (formerly the Royal Bank of Scotland Group). As PSNW is intended to be a comprehensive measure, the inclusion of public sector banks may be less distortive than it is for PSND. While our priority will be to produce ”PSNW ex” (excluding public sector banks), we intend to explore their inclusion in future.

Coverage of assets and liabilities

The new PSNW measure would include all assets and liabilities covered by the ESA 2010 framework, where these data are available (see Section 3 for a discussion of data availability). Being an internationally-recognised statistical aggregate, an ESA-based PSNW can only include assets and liabilities within the scope of the statistical framework, although it is possible to present even broader supplementary measures including additional items.

In this context, it is worth noting that the statistical asset recognition boundary differs somewhat to that used in financial reporting. For example, ESA 2010 explicitly excludes most contingent liabilities from the main accounts, as well as obligations under unfunded pension schemes; these are presented in supplementary tables but would not affect the value of PSNW. Similarly, some non-financial assets – for example, contracts or licenses and goodwill – are valued very differently to financial reporting. Others, such as some environmental assets, currently lie outside the public finance statistics frameworks, although could feature in expanded, experimental, supplementary measures of public sector assets in the future.

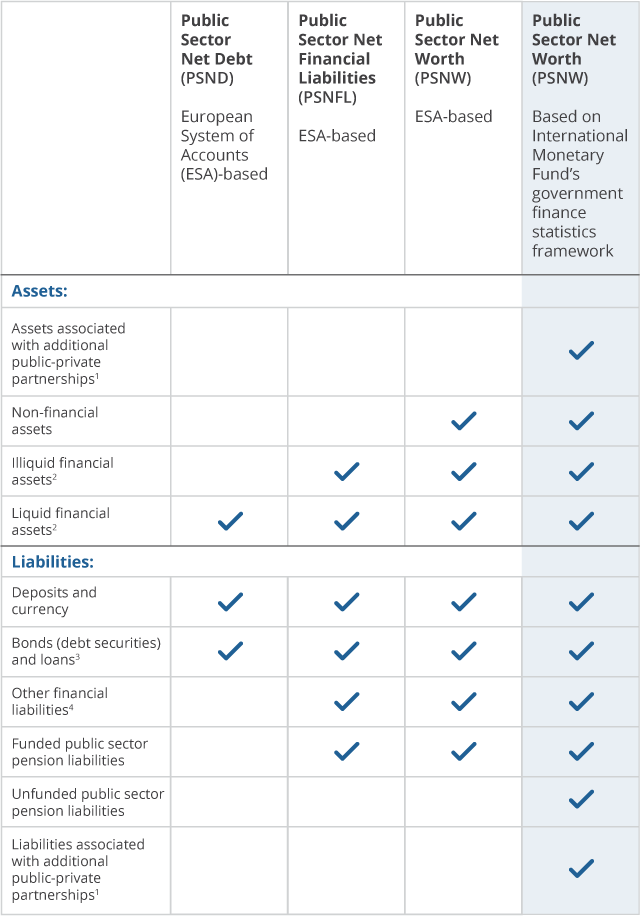

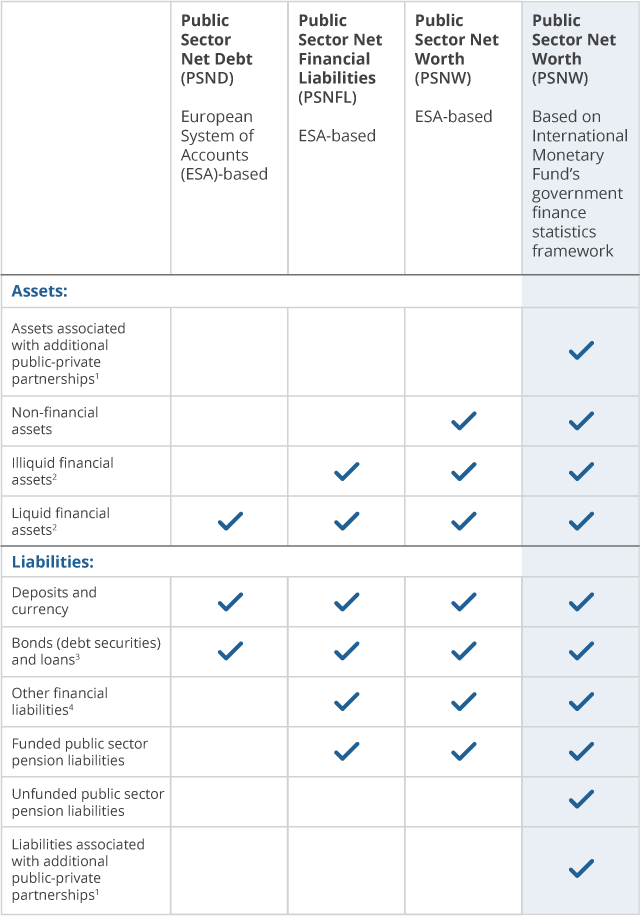

For the measure described in this paper, we intend to limit our presentation to only those assets and liabilities within the ESA framework, with additional assets and liabilities covered by the International Monetary Fund’s government finance statistics framework shown via reconciliation tables. Figure 1 shows the coverage of assets and liabilities in the new ESA-based PSNW compared with both the existing ESA-based aggregates and the broader IMF GFSM-based PSNW.

Figure 1: Assets and liabilities included in different measures of the public sector balance sheet, including the new ESA-based public sector net worth

Source: Office for National Statistics

Notes:

- The IMF GFSM supplementary statistics include assets and liabilities associated with public-private partnerships (PPPs) that are considered “off-balance sheet” under ESA 2010 but “on-balance sheet” by international accounting standards.

- “Liquid financial assets” mainly consists of foreign exchange reserves and cash deposits. “Illiquid financial assets” includes assets such as loans, financial derivatives and other accounts receivable.

- There are differences in the valuation of debt securities between the IMF GFSM-consistent measure of PSNW and the core public sector finance statistics, as detailed in the text.

- “Other financial liabilities” includes monetary gold and special drawing rights, standardised guarantees, financial derivatives and other accounts payable.

Download this image Figure 1: Assets and liabilities included in different measures of the public sector balance sheet, including the new ESA-based public sector net worth

.png (75.0 kB){kind=link}

Valuation

The largest component of liabilities is debt securities issued by central government. Debt securities can be measured at market, face or nominal value. The PSF statistics follow Eurostat’s Manual on Government Deficit and Debt (MGDD) 2019 and value debt securities at face value. The new PSNW measure would record them in the same way. It is possible to present alternative valuations as supplementary items alongside the main measure; however, we do not currently intend to do so as this information is available in the IMF GFSM presentation. We will continue to review the inclusion of supplementary information once the measure is introduced.

The value of produced non-financial assets will, wherever possible, be estimated using the perpetual inventory method (PIM). This is a method of estimating the value of the stock of non-financial assets (NFAs) using available data on capital flows (capital formation) and asset lives. The value of non-produced assets will be estimated following National Balance Sheet methodology where available; however, there are significant data limitations in this area (discussed in Section 3).

Presentation and periodicity

An ESA-based PSNW will be part of an integrated presentation of the public sector balance sheet. As detailed in the previous sections, we will limit presentation of supplementary versions of PSNW; however, we will present full reconciliation with other measures, including IMF GFSM PSNW.

PSNFL is currently produced on a quarterly basis and is published four months after the quarter end. Full data on NFA is currently only available on an annual basis, although quarterly data are available for some assets. As of this year, provisional NFA statistics are available in the National Balance Sheet four months after the (calendar) year end. Although these estimates were initially experimental statistics, introduced to meet imminent user needs during COVID-19, we are exploring the possibility of continuing to produce these preliminary estimates in the future.

In the first instance, we plan to produce an annual (financial year) series of PSNW, updated quarterly. We will then work towards producing quarterly estimates, with estimates available four months after quarter end.

Summary of relationship with other measures

The most important substantive differences between the new measure and existing measures of public sector net worth can be summarised as follows.

Sectoral coverage:

- the new measure of PSNW will define the public sector as central government, local government, public non-financial corporations, and public financial corporations, including the Bank of England and public sector funded pension schemes but excluding public sector banks

- the public sector in the National Balance Sheet (NBS) differs as it excludes public financial corporations and has a different timeline for implementation of reclassifications

- the public sector in the IMF GFSM-consistent statistics is broadly aligned with the new measure but includes additional public-private partnerships

Asset and liability coverage:

- the new measure will include financial assets and liabilities, and non-financial assets in line with ESA 2010; this excludes unfunded public pension liabilities and contingent liabilities

- this aligns with PSNW in the National Balance Sheet

- PSNW in the IMF GFSM-consistent statistics includes unfunded public pension liabilities

Valuation:

- the new measure values debt securities at face value (and follows MGDD 2019 in valuation of other liabilities)

- in NBS PSNW debt securities are valued at market value

- in IMF GFSM PSNW debt securities are valued at market value (although nominal and face values are available)

Reconciliation with IMF GFSM-consistent PSNW

We will continue to produce IMF GFSM-consistent statistics, including IMF GFSM PSNW, as supplementary to the PSF statistics. Where improvements to balance sheet data are made, particularly to the non-financial balance sheet (see Section 3), these will be applied across both ESA- and IMF GFSM-based measures.

The IMF GFSM public sector balance sheet includes both additional assets and additional liabilities compared with its ESA-based equivalent (see Figure 1). The different valuation of debt securities also increases the total value of liabilities recorded in the IMF GFSM statistics. For example, IMF GFSM net financial worth at market value shows, by design, considerably higher net liabilities than its equivalent PSNFL, with unfunded pension liabilities driving a large part of the difference. Similarly, IMF GFSM PSNW would be significantly lower than an ESA- and PSF-consistent measure of PSNW (noting that the value of liabilities is subtracted from the value of assets to produce PSNW, and so higher liabilities lead to lower net worth).

A reconciliation between PSNFL, IMF GFSM net financial worth and IMF GFSM PSNW is available in Appendix E of the PSF Bulletin. The reconciliation between an ESA-based PSNW and GFSM PSNW would be as follows:

This again illustrates that we would expect GFSM PSNW to be lower than the new ESA-based PSNW.

Back to table of contents3. Implementing public sector net worth in the public sector finance statistics: data issues and further work required

The measure of public sector net worth (PSNW) described in the previous section is an extension of existing statistical aggregates. Consequently, most of its components are already available and are used to compile the existing set of public sector finance (PSF) statistics. However, some further work is needed before the measure can be implemented. We expect to introduce the new measure in some form within the next 18 months, though the implementation plan will depend on the outcome of this further work.

The primary area for development is the production of a non-financial balance sheet that is consistent with PSF statistics in its coverage (in other words, is not subject to the misalignment between the UK National Accounts and PSF statistics). Ongoing work to improve the quality of some financial data will also feed into production of PSNW. Finally, there is work needed to better understand the drivers of changes in PSNW that may not be captured by the available data.

Non-financial balance sheet

We currently publish estimates of non-financial asset stocks by sector and asset type in the annual National Balance Sheet (NBS). Statistics on produced non-financial asset stocks are compiled following the Organisation for Economic Cooperation and Development (OECD) Measuring Capital manual 2009. A perpetual inventory method (PIM) is used to estimate the value of capital stocks based on available information on flows, in line with internationally recommended practice. Statistics on land are compiled using a residual method. The methodology used to compile net worth in the NBS is currently being reviewed. The review will include the sources and methods used to estimate land, using international guidance from the Eurostat-OECD compilation guide on land estimation (2015).

The NBS data are produced on a basis consistent with the UK National Accounts, and not with the PSF statistics. As explained earlier, this means that the available estimates do not separately identify public financial corporations – these units are reported jointly with private financial corporations in the National Accounts publications. Their holdings of non-financial assets would need to be estimated separately to ensure PSNW covers the entirety of the UK public sector, as defined for statistical purposes. This adjustment is currently done on an ad hoc basis for the experimental International Monetary Fund’s Government Finance Statistics Manual 2014 (IMF GFSM)-consistent statistics, but further work is needed to ensure consistent treatment of non-financial assets between public financial corporations and the rest of the public sector.

Another area of future work concerns certain historic classification and methodology decisions affecting non-financial assets (such as the treatment of nuclear decommissioning) that have not been implemented in the UK National Accounts but need to be accounted for in the estimation of public sector’s asset stock.

Alongside these major conceptual differences, there are limited data sources available to exhaustively account for some types of non-produced assets (such as mineral resources owned by the public sector), inventories, and some types of intangible assets, such as marketing and goodwill. It should be noted that the statistical approach to many of these asset types lies further apart from their accounting treatment, rendering some of the conventional data inputs – for example, statutory accounts – less useful.

Finally, methodology for interpolation of the data available on an annual basis would need to be developed to ensure that higher periodicity PNSW estimates are meaningful.

Financial balance sheet

In recent years, we have made considerable progress in recording public sector financial assets and liabilities, particularly those beyond the scope of public sector net debt (PSND). Wider balance sheet aggregates require robust data on financial instruments such as equity, derivatives or pension liabilities, which had not been used to derive the fiscal measures historically. In response to the introduction of public sector net financial liabilities (PSNFL) in 2016, we launched a review into the wider areas of the public sector balance sheet. The most significant improvement to date has been to the estimates of government liabilities in relation to funded public sector pension schemes.

Continuous improvement of the financial balance sheet remains our priority, with the current focus on improving coverage of the public corporations subsector. This review was postponed in 2020 to prioritise the recording of the government coronavirus (COVID-19) support schemes and we now expect to implement the improved public corporation dataset in 2022. More details about this work are available in our looking ahead article.

In the longer term, we expect to consider the quality and exhaustiveness of the local government data. The advent of separate organisations, such as Local Authority Trading Companies, creates some challenges to our established data collection methods.

Understanding changes to PSNW

Changes to net worth may result from a number of factors besides government actions, at least in the short-term. Financial instruments which are recorded at market value are affected by price fluctuations, and even those that are not may be sensitive to changes in economic assumptions and modelling methods. For example, a change in labour market assumptions would likely result in a change in the value of student loan assets held by government; equally, a change in life expectancy or the discount rate would be transmitted to the valuation of pension liabilities.

Historically, there has been less interest in such non-transactional changes in the context of fiscal statistics. Consequently, the breakdown of balance sheet changes necessary to separate transactions and non-transactional (value) changes is not always available in existing data sources.

With an increased interest in the broad balance sheet measures and their reconciliation with the flow aggregate public sector net borrowing, movements in value will need to be reported transparently and their role in changes to PSNW distinguished from public sector transactions (such as expenditure on subsidies or receipt of tax revenue). New statistical methods will need to be developed in instances where the source data is not granular enough to fully support statistical needs.

Back to table of contents