1. Other pages in this release

Alongside this release, estimates of average household income in financial year ending 2020 are presented in a separate bulletin:

Back to table of contents2. Main points

In financial year ending (FYE) 2020, the income of the richest 20% of people was over six times higher than the poorest 20%, while the richest 10% received 50% more income than the poorest 40%.

Income inequality, as measured using the Gini coefficient, has been broadly stable over the past ten years with disposable income (post direct taxes and cash benefits) reaching 34.6% in financial year ending (FYE) 2020 after peaking at 38.6% in FYE 2008 just prior to the economic downturn; however, the Gini coefficient is 6.1 percentage points higher than average levels throughout the late 1970s and 1980s.

While income inequality is higher for non-retired people compared with retired people (34.9% and 31.7%), income inequality has increased more for retired people over recent years; 0.8 percentage points per year between FYE 2015 and FYE 2020, compared with negative 0.1 percentage points per year for non-retired people.

While the Gini coefficient of disposable income has remained stable, the measure for original income (before direct taxes and cash benefits) has fallen from 51.4% in FYE 2011 to 49.7% in FYE 2020; this reflects greater equality in earnings over this period, mitigated by a fall in the effectiveness of cash benefits at reducing income inequality.

3. Analysis of income inequality

This release presents provisional estimates of income inequality of people in the UK for the financial year ending (FYE) 2020.

These provisional figures are “nowcasts” produced using a microsimulation model based on Living Costs and Food Survey (LCF) data, up-to-date information on tax and benefit policy, and the latest economic data in FYE 2020. More information about this process can be found in the Measuring the data section.

There are several different indicators to summarise inequality of household income (Table 1).

Perhaps the most commonly used internationally is the Gini coefficient. The Gini coefficient ranges between 0% and 100%, where 0% indicates that income is shared equally among all households and 100% indicates the extreme situation where one household accounts for all income. Therefore, the lower the value of the Gini coefficient, the more equally household income is distributed. This is measured before accounting for housing costs.

The characteristics of the Gini coefficient make it particularly useful for making comparisons over time, between countries, and before and after taxes and benefits. However, no indicator is without limitations. One drawback of the Gini is that, as a single summary indicator, it cannot distinguish between differently shaped income distributions. For that reason, it is useful to look at this index alongside other measures of inequality.

One such measure is the S80/S20 ratio – the ratio of the total income received by the richest and poorest 20% of people. Another related measure is the P90/P10 ratio, which is calculated as the ratio of incomes of the person at the 90th percentile and the person at the 10th percentile.

A more recently developed measure is the Palma ratio. The Palma ratio is the ratio of the income share of the richest 10% of individuals to that of the poorest 40% of individuals.

| S80-S20 | P90-P10 | Palma Ratio | Gini | |

|---|---|---|---|---|

| 2018 to 2019 | 6.1 | 4.2 | 1.5 | 34.7 |

| 2019 to 2020 (p) | 6.1 | 4.2 | 1.5 | 34.6 |

Download this table Table 1: The income of the richest 20% of people was over six times higher than the poorest 20%

.xls .csvThe S80/S20 ratio highlights that the richest fifth of people had a share of income that was over six times that for the poorest fifth in both FYE 2019 and FYE 2020. The income of the person at the 90th percentile was over four times the income of the person at the 10th percentile, while the Palma ratio highlights that the richest 10% of people accounted for a greater share of income than the poorest 40%. These measures of inequality remain largely unchanged from the previous year (Table 1).

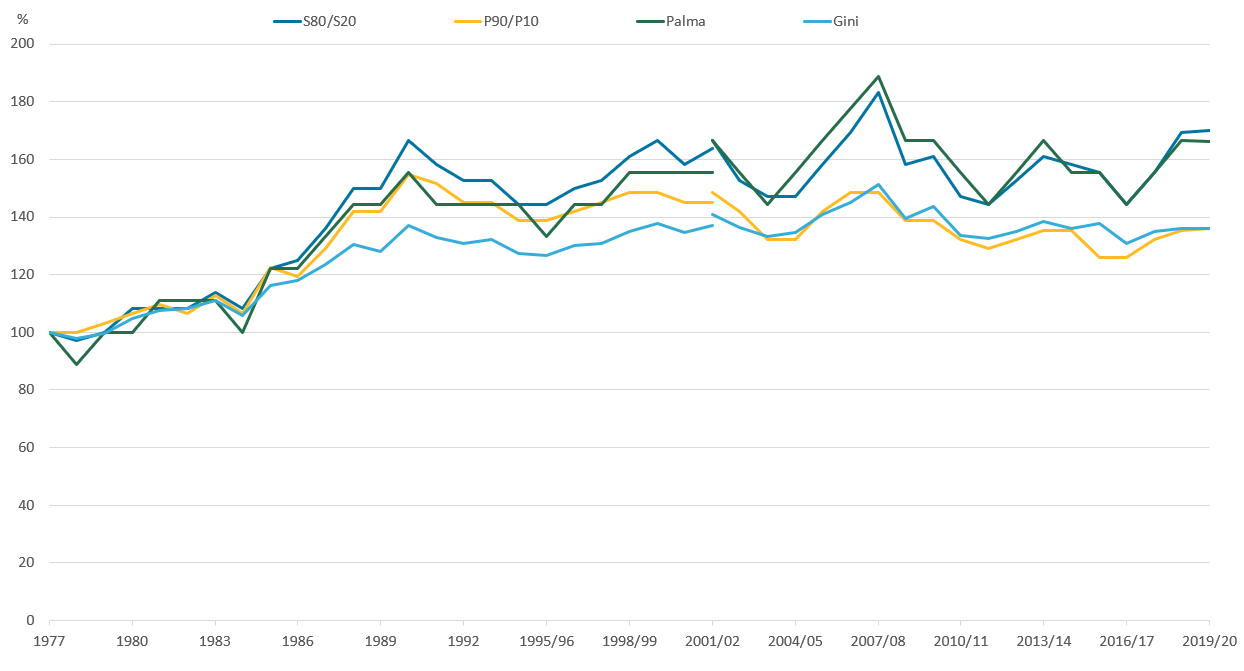

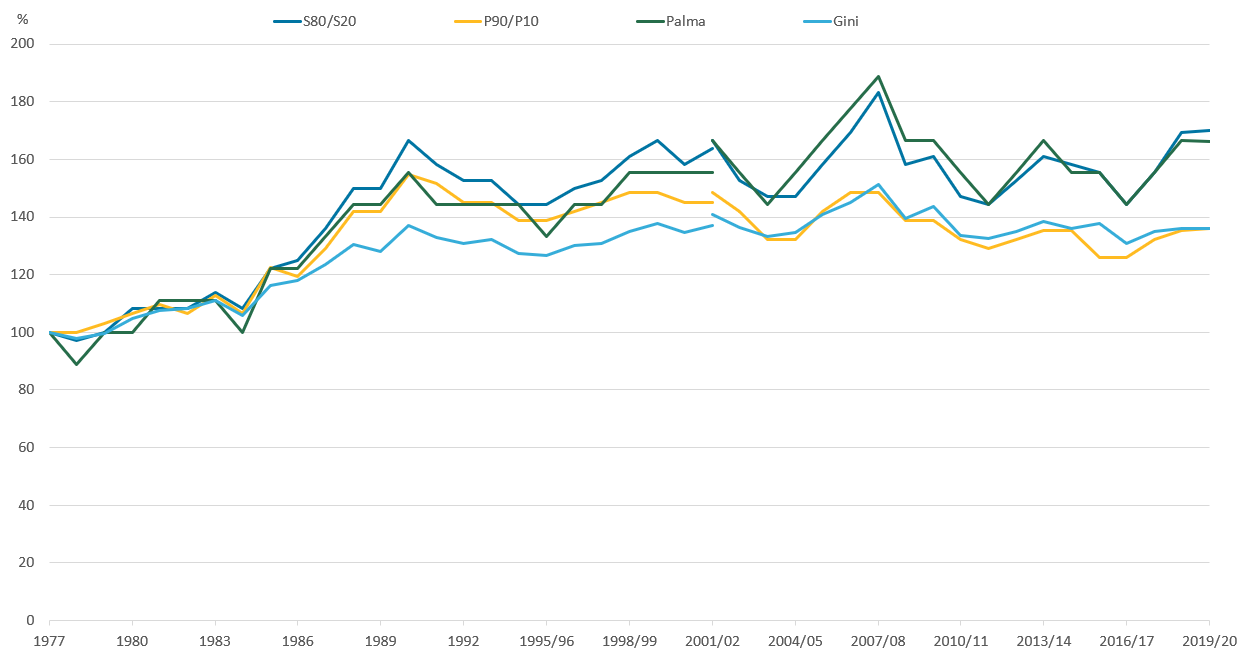

Figure 1: A range of measures show that income inequality is largely unchanged from levels reached 10 years ago

Gini coefficient, S80/S20 ratio, P90/P10 ratio and Palma ratio for equivalised disposable income, all individuals, 1977 to financial year ending (FYE) 2020, 1977 = 100

Source: Office for National Statistics

Notes:

- 2019/2020, which represents the financial year ending 2020, (April to March), and similarly for all other years expressed in this format.

- Results for FYE 2020 are provisional

- Estimates of income from FYE 2002 onwards have been adjusted for the under-coverage of top earners.

Download this image Figure 1: A range of measures show that income inequality is largely unchanged from levels reached 10 years ago

.png (60.6 kB) .xlsx (20.3 kB){kind=link}

Income inequality has been broadly stable over the past 10 years with the Gini coefficient reaching 34.6% in FYE 2020 after peaking at 38.6% just prior to the 2008 economic downturn. Income inequality increased during the 1980s across all these measures with some varying change in the late 1990s and 2000s. The Gini coefficient is 6.1 percentage points higher in FYE 2020 than average levels throughout the late 1970s and 1980s.

Across all measures, however, there has been a slight increase in income inequality since FYE 2017. The Gini coefficient has increased from 33.4% to 34.6%, while the S80/S20 ratio shows an increase from 5.2 to 6.1. This mainly reflects a fall in disposable income in for the poorest 20% of people between FYE 2018 and FYE 2019, highlighted in more detail in the Average household income, UK: Financial year ending 2019 (provisional) release.

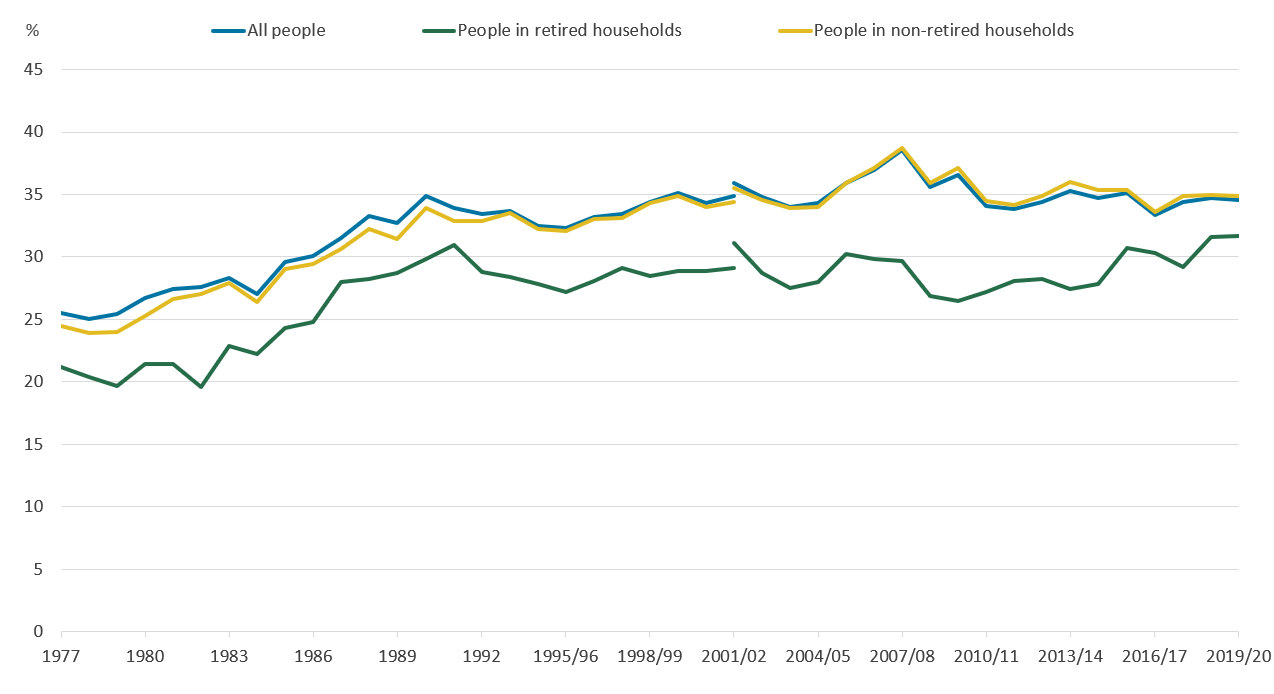

Figure 2: Income inequality for individuals in retired households has increased in recent years

Gini coefficients for equivalised disposable income by household type, 1977 to FYE 2020

Notes:

- 2019/2020, which represents the financial year ending 2020, (April to March), and similarly for all other years expressed in this format.

- Data for 2019/20 are provisional.

- Estimates of income from FYE 2002 onwards have been adjusted for the under-coverage of top earners.

Download this image Figure 2: Income inequality for individuals in retired households has increased in recent years

.png (50.0 kB) .xlsx (19.7 kB){kind=link}

Since comparable records began in 1977, income inequality for individuals in non-retired households has always been higher than those living in retired households. In FYE 2020, the Gini coefficient for individuals in non-retired households was 34.9% while the Gini coefficient for individuals in retired households was 31.7%. Income inequality for both groups remained at similar levels in FYE 2020.

Levels of income inequality for both retired and non-retired people increased during the late 1990s. While there has been some volatility, income inequality for individuals in non-retired households has remained broadly similar to that reached in FYE 2011. In recent years, income inequality for retired people has increased by an average of 0.8 percentage points per year since FYE 2015. Comparatively, income inequality for individuals in non-retired households has reduced by 0.1 percentage points.

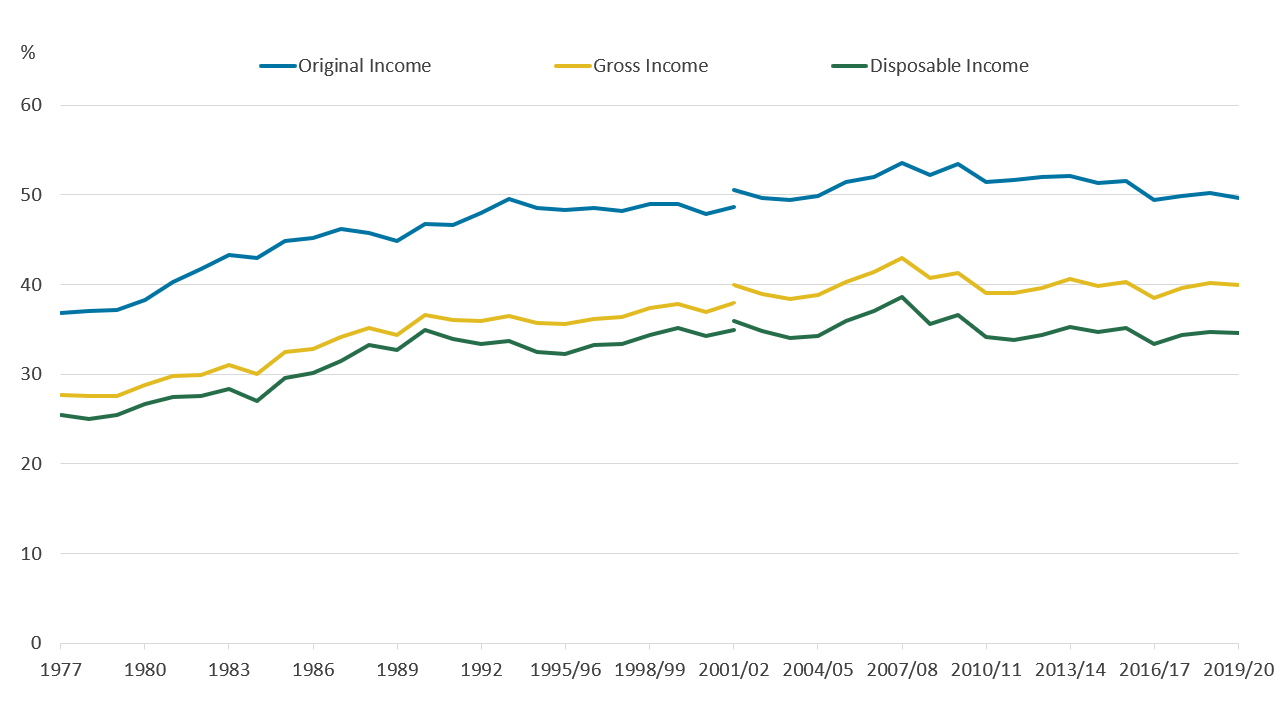

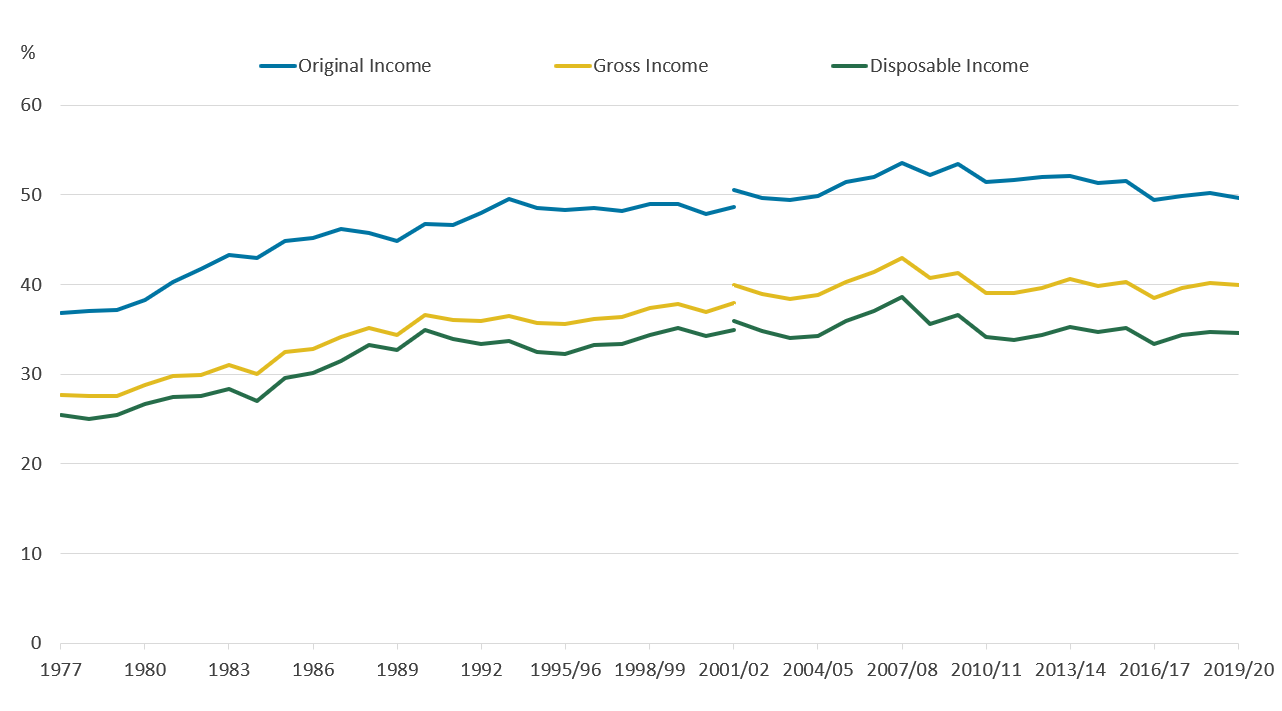

The previous sections focused on inequality of disposable income (after direct taxes and cash benefits). Figure 3 compares this measure against the Gini coefficients for original (pre direct taxes and benefits) and gross (original income plus cash benefits) income over time to highlight how taxes and benefits affect income inequality.

Figure 3: Inequality of original income has fallen over recent years

Gini coefficients for equivalised original, gross, and disposable income of all individuals, 1977 to FYE 2020

Source: Office for National Statistics

Notes:

- 2019/2020, which represents the financial year ending 2020, (April to March), and similarly for all other years expressed in this format.

- Data for 2019/20 are provisional.

- Estimates of income from FYE 2002 onwards have been adjusted for the under-coverage of top earners.

Download this image Figure 3: Inequality of original income has fallen over recent years

.png (41.2 kB) .xlsx (19.7 kB){kind=link}

Overall, cash benefits reduce income inequality; in FYE 2020, income inequality fell from 49.7% to 40% after cash benefits were included. Direct taxes further reduce income inequality to 34.6% (Gini coefficient on disposable income).

Between FYE 2011 and FYE 2020, original income inequality fell by 1.7 percentage points to 49.7%. This likely reflects more evenly distributed earnings over this period as highlighted in Low and high pay in the UK: 2019, using data from the Annual Survey of Hours and Earnings (ASHE). This release shows that the proportion of low-paid hourly jobs fell from 21.3% in 2010 to 16.2% in 2019. Furthermore, while the pay differential between the 5th and 95th percentile of full-time employees was 4.7 in 2019, this has fallen from 5.4 since 2010.

The Gini coefficient of gross income (which includes cash benefits) increased over the same period (FYE 2011 to FYE 2020), up by 1.0 percentage points. This means that the gap between the Gini coefficients of original and gross income has fallen over this period, highlighting a fall in the effectiveness of cash benefits. This is likely to reflect that poorer income groups have received a progressively lower amount of income from cash benefits over this period.

Disposable income inequality remained stable during this time, which suggests that direct taxes had a larger impact in reducing income inequality during this period compared with cash benefits.

Back to table of contents4. Comparisons of provisional and final estimates

Figure 4 highlights the accuracy of the provisional estimates of income inequality over the five years during which subsequent outturn data is available.

Figure 4: Provisional estimates of income inequality are broadly in line with final estimates

Final estimates of the Gini coefficient and their 95% confidence intervals and the provisional estimates FYE 2015 to FYE 2019

Embed code

Notes:

These are measured on an individual level.

These estimates have been adjusted for the under-coverage of top earners. This was introduced in FYE 2019, and so they are not comparable with previous provisional estimates.

Figure 4 highlights that the provisional estimate of the income inequality provides a good indication of the final estimate over time. Over the five years in which they can be compared, the provisional estimate consistently lies within the 95% confidence intervals of the final estimate.

Back to table of contents5. Household income inequality data

The effects of taxes and benefits on household income, provisional estimates

Dataset | Released 26 July 2019

Provisional estimates of income and inequality measures for financial year ending 2019, alongside historical data.

6. Glossary

Disposable income

Disposable income is the amount of money that households have available for spending and saving after direct taxes (such as Income Tax and Council Tax) have been accounted for. It includes earnings from employment, private pensions and investments, as well as cash benefits provided by the state. More information on the different stages of income can be found in the Things you need to know about this release section of Effects of taxes and benefits on UK household income: financial year ending 2017.

Equivalisation

Comparisons across different types of individuals and households (such as retired and non-retired, or rich and poor) or over time is done after income has been equivalised. Equivalisation is the process of accounting for the fact that households with many members are likely to need a higher income to achieve the same standard of living as households with fewer members. Equivalisation considers the number of people living in the household and their ages, acknowledging that while a household with two people in it will need more money to sustain the same living standards as one with a single person, the two-person household is unlikely to need double the income.

This analysis uses the modified-Organisation for Economic Co-operation and Development (OECD) equivalisation scale (PDF, 165KB).

Mean and median income

The mean measure of income divides the total income of individuals by the number of individuals. A limitation of using the mean is that it can be influenced by just a few individuals with very high incomes and therefore does not necessarily reflect the standard of living of the “typical” person. However, when breaking down changes in income and direct taxes by income decile or types of households, the mean allows for these changes to be analysed in an additive way.

Many researchers argue that growth in median household incomes provides a better measure of how people’s well-being has changed over time. The median household income is the income of what would be the middle person, if all individuals in the UK were sorted from poorest to richest. Median income provides a good indication of the standard of living of the “typical” individual in terms of income.

Retired households

A retired person is defined as anyone who describes themselves (in the Living Costs and Food Survey) as “retired” or anyone over minimum State Pension age describing themselves as “unoccupied” or “sick or injured but not intending to seek work”. A retired household is where the combined income of retired members amounts to at least half the total gross income of the household.

Back to table of contents7. Measuring the data

Statistics that reflect the experience of a typical person, such as median income reported here, are important to properly understand changes in material living conditions. However, the complexities involved in collecting, processing and analysing household and individual financial survey data mean indicators concerning the distribution of income are typically only available with a sizeable time lag.

For example, estimated median income (estimated using survey data) for the financial year ending (FYE) 2019 was published more than 11 months after the end of the reference period. Meeting the considerable user demand for more timely data on the distribution of household income, we have developed these Experimental Statistics, which are produced using so-called “nowcasting” techniques.

Nowcasting is an increasingly popular approach for providing initial estimates of economic indicators, such as median income. In contrast to forecasting, which relies heavily on projections and assumptions about future economic circumstances, nowcasting uses data that are more timely and already available for the period of study.

Although, at the time of producing these statistics, detailed survey data on household incomes are not yet available for FYE 2020, a lot is known about its individual components and the factors that affect them. This includes data on earnings, employment and inflation, as well as details of how changes to the tax and benefits system affect different types of households and individuals. This information is used to adjust income survey data for recent years to reflect the current period and measures such as median income are published earlier than was previously possible.

While nowcast estimates do not perfectly reflect changes in the distribution of income, particularly when examining smaller sub-groups of the population, they provide an early indication of what the full survey-based data may show when published later this year, or early next.

The methodology used in this bulletin has undergone significant testing and benefitted from having a range of external experts to ensure it is as robust as possible. As Experimental Statistics, the content of this bulletin and the associated dataset will continue to be evaluated to ensure that user needs are met.

How are these estimates adjusted?

All measures of income for the UK given in this article are calculated without adjusting for expenses relating to housing costs. The measures have been deflated to FYE 2020 prices using the Consumer Prices Index including owner occupiers’ housing costs (CPIH), excluding Council Tax, to give a better comparison of households’ standards of living. These deflated measures are referred to as “real”. This contrasts with “nominal” measures, which have not been deflated. Changes in income in this publication are “real” changes unless explicitly stated.

The provisional estimate income publication requires a deflator dating back to 1977. The CPIH, excluding Council Tax, is currently available from January 2005. The Consumer Prices Index (CPI) is available from 1996, with a modelled historical series available from 1950. For this analysis, the owner occupiers’ housing costs (OOH) component is estimated using the actual rental series available from the Retail Prices Index (RPI). The OOH component is factored into the CPI (and modelled CPI prior to 1996) using the average OOH weight. Prior to 2005, this series is classed as experimental.

Methodology

The input data for this analysis come from the Living Costs and Food Survey (LCF) and the Effects of taxes and benefits on household income (ETB) dataset, which is derived from the LCF. Together, these provide information on income, expenditure and important family characteristics.

There are four main steps involved to produce nowcast estimates of disposable income. These are:

compile base data – this involves joining three years of historical LCF data

uprate base data – adjust the base data to reflect changes in the macro-economic conditions that have affected households at different points of the income distribution; for instance, taking into account wage growth from more timely earnings growth data

model tax and benefit changes – apply rules of the current tax and benefit system to the uprated base data

recalibrate weights – account for changes in labour market participation and the socio-demographic characteristics of the population between base data and reference period

For this analysis, historical LCF data covering the financial years ending (FYE) 2014, 2015, and 2016 were combined to produce nowcast estimates of disposable income for different household types and measures of inequality for FYE 2019 and FYE 2020. The growth rate between the various nowcasts are applied to the published FYE 2019 estimates presented within Average household income, UK: Financial year ending 2019.

While no explicit adjustment for the under-coverage of the richest earners is applied in the nowcasting model, the growth rates are applied to published FYE 2019 estimates that have been adjusted. A more detailed description of the methodology is provided in the accompanying article, Nowcasting household income in the UK: Methodology, 2016, and methodology provides a detailed overview of the adjustment for the under-coverage of the richest earners.

The historical data in this article are based on the Effects of Taxes and Benefits (ETB) series, produced by the Office for National Statistics (ONS), which itself is derived from the LCF. This series has been chosen for this article because of its long time series and its use as the primary input for the Intra-Governmental Tax and Benefit Model (IGOTM) used for producing the FYE 2019 provisional estimates.

More information about the accuracy and reliability of these statistics is contained in the Quality and methodology section of Effects of taxes and benefits on UK household income – flash estimate: financial year ending 2018.

How do these estimates fit in with other official statistics on household incomes?

These experimental estimates have been developed to serve as early or provisional estimates of figures that are currently published in within Average household income, UK: Financial year ending 2019. When the survey-based estimates for FYE 2019 are available they will supersede these estimates. We will also use these survey-based figures to evaluate the accuracy of these nowcasts.

The figures published in this bulletin use the same definition of disposable income used in these other releases, which in turn is consistent with the concepts set out in the second edition of the United Nations Economic Commission for Europe Canberra Handbook (UNECE, 2011); this sets out the main international standards in this area.

Back to table of contents8. Strengths and limitations

The nowcast estimates are subject to the same degree and types of statistical error as any other analysis based on survey data. As the LCF data are a sample survey, the estimates are subject to sampling error. Surveys gather information from a sample rather than from the whole population. The sample is designed carefully to allow for this and to be as accurate as possible given practical limitations such as time and cost constraints, but results from sample surveys are always estimates, not precise figures. This means that they are subject to a margin of error, which can have an effect on how changes in the numbers should be interpreted, especially in the short-term. In practice, this means that small, short-term movements should be treated as indicative and considered alongside medium- and long-term patterns in the series.

As well as sampling error, all statistics, including these nowcast estimates, are also subject to non-sampling error. Non-sampling error includes all sources of data error that are not a result of the way the sample is selected. There are a wide number of different types of potential non-sampling error, including coverage error, non-response and measurement error. It is not possible to provide a measure of non-sampling error.

Using micro-simulation and nowcasting techniques to estimate distribution of income provides an additional source of non-sampling error in the estimates due to, for instance, approximations in the simulation of tax benefit rules, adjustments for non-take up, uprating of financial parameters and socio-demographic characteristics to the simulation year or ignoring behavioural responses (see, for example, Navicke and others, 2013). On the other hand, simulation can arguably improve the accuracy of results relative to survey-based estimates through simulating the exact rules of the tax and benefit system.

A 95% confidence interval is a range within which the true population would fall for 95% of the times the sample survey was repeated. It is a standard way of expressing the statistical uncertainty of a survey-based estimate.

Back to table of contents