Table of contents

- Main points

- Things you need to know about this release

- Labour productivity up for the eighth consecutive quarter compared with a year ago, though the pace of growth has slowed

- Output per hour up in both services and manufacturing, compared with a year ago

- Unit labour costs grow for the fourteenth consecutive quarter

- Experimental sectional unit labour costs

- Productivity by region

- Links to related statistics

- What’s changed in this release?

- Quality and methodology

1. Main points

Labour productivity for Quarter 3 (July to Sept) 2018, as measured by output per hour, grew by 0.2% compared with the same quarter a year ago; this was the weakest growth since Quarter 3 2016.

Whilst manufacturing experienced labour productivity growth of 1.7%, the significantly larger services only achieved 0.1%.

Compared with the previous quarter, UK labour productivity is estimated to have decreased by 0.4% in Quarter 3 2018; the decrease in productivity reflected an increase in the number of actual hours worked, which outpaced output growth for the quarter.

Productivity hours worked increased by 1.3% in Quarter 3 2018 compared with the same quarter a year ago, while the number of jobs increased by 1.0% over the same period.

Earnings and other labour costs outpaced productivity growth, resulting in unit labour cost growth of 2.8% in the year to Quarter 3 2018, compared with growth of 2.1% in the previous quarter; this was slightly higher than the 2.7% growth in the year to Quarter 1 (Jan to Mar) 2018.

2. Things you need to know about this release

This release reports labour productivity estimates for Quarter 3 (July to Sept) 2018 for the whole economy, the UK regions at NUTS1 level and a range of industries, together with estimates of unit labour costs. Productivity is important as it is considered to be a driver of long-run changes in average living standards.

This edition forms part of our quarterly productivity bulletin, which also includes an overarching commentary, quarterly estimates of public service productivity, quarterly estimates of multi-factor productivity and articles on productivity-related topics and data.

Labour productivity is calculated by dividing output by labour input. Output refers to gross value added (GVA), which is an estimate of the volume of goods and services produced by an industry. Labour inputs in this release are measured in terms of workers, jobs (“productivity jobs”) and hours worked (“productivity hours”).

This release also reports estimates of unit labour costs (ULCs), which capture the full labour costs – including social security and employers’ pension contributions – incurred in the production of a unit of economic output. Labour costs make up around two-thirds of the overall cost of production of UK economic output. Changes in labour costs are therefore a large factor in overall changes in the cost of production. If increases in labour costs are not reflected in the volume of output, this can put upward pressure on the prices of goods and services, therefore this is a closely watched indicator of inflationary pressure in the economy.

The equations for labour productivity and ULCs can be found in the quality and methodology section of this release.

The output statistics in this release are consistent with the latest GDP Quarterly national accounts published on 21 December 2018. Note that productivity in this release does not refer to gross domestic product (GDP) per person, which is a measure that includes people who are not in employment. Regional productivity figures presented in this release use the unbalanced income measure of current price gross value added and are consistent with the Regional GVA NUTS1 published on 12 December 2018.

The labour input measures used in this release are consistent with the latest labour market statistics as described further in the quality and methodology section of this bulletin.

Unless otherwise stated all figures are seasonally adjusted.

Back to table of contents3. Labour productivity up for the eighth consecutive quarter compared with a year ago, though the pace of growth has slowed

Compared with the same quarter a year ago, labour productivity on an output per hour basis grew by 0.2% and has been growing for the past eight consecutive quarters.

A 0.2% growth compared with the same quarter in the previous year represents a continuation of the UK's “productivity puzzle”, with productivity since the economic downturn in 2008 growing more slowly than during the long period prior to the downturn. This sustained stagnation contrasts with patterns following previous UK economic downturns, when productivity initially fell, but subsequently recovered to the previous trend rate of growth. There is wide and varied economic debate regarding the causes of this puzzle and further analysis of recent UK productivity trends can be found in the January 2016, May 2016 and June 2016 Economic Reviews, as well as in several standalone articles including: What is the productivity puzzle?, The productivity conundrum, explanations and preliminary analysis and The productivity conundrum, interpreting the recent behaviour of the economy.

This puzzle is shown in Figure 1, which presents two alternative measures of productivity – output per hour and output per worker – alongside their projected 1994 to 2007 trends. Following years of steady growth, each measure peaked prior to and fell during the economic downturn. However, due to a strong labour market performance accompanying a relatively weak recovery in output growth, productivity has not returned to its pre-downturn trend. Productivity in Quarter 3 (July to Sept) 2018, as measured by output per hour, was 18.2% below its pre-downturn trend – or, equivalently, productivity would have been 22.3% higher had it followed this pre-downturn trend1.

Labour productivity decreased by 0.4% in Quarter 3 2018 compared with the previous quarter. This increase left productivity 1.6% above its peak in Quarter 4 (Oct to Dec) 2007, prior to the economic downturn.

Figure 1: Output per hour and output per worker

Seasonally adjusted, Quarter 1 (Jan to Mar) 1994 to Quarter 3 (July to Sept) 2018, UK

Source: Office for National Statistics

Download this chart Figure 1: Output per hour and output per worker

Image .csv .xlsFigure 2 breaks down the growth in productivity between Quarter 1 2008 and Quarter 3 2018 into contributions from different industry groupings and an “allocation effect” due to changes in the share of output and labour in each grouping. All else being equal, stronger productivity growth in any given industry, or a movement of output and labour towards higher productivity industries will tend to increase aggregate productivity growth, while the opposite would reduce it.

Non-financial services were the main positive contributor to productivity growth over this period, partly offset by negative contributions from non-manufacturing production and finance. The negative allocation effect – suggesting that output and labour have been moving from higher to lower productivity industries in recent years – includes the falling share of output in mining and quarrying, which has among the highest levels of productivity of UK industry. This is partially a result of the falling reserves of oil and gas in the North Sea. Although negative for the period as a whole, the allocation effect was initially positive following the downturn, but turned negative in recent years.

Figure 2: Contributions to growth of whole economy output per hour

Seasonally adjusted, cumulative changes, Quarter 1 (Jan to Mar) 2008 to Quarter 3 (July to Sept) 2018, UK

Source: Office for National Statistics

Notes:

- Non-manufacturing production refers to: agriculture, forestry and fishing; mining and quarrying; electricity, gas, steam and air-conditioning supply; and water supply, sewerage, waste management and remediation activities.

Download this chart Figure 2: Contributions to growth of whole economy output per hour

Image .csv .xlsNotes for: Labour productivity up for the eighth consecutive quarter compared with a year ago though the pace of growth has slowed

- Differences between these two measures are due to differences in the denominator used in the calculation. Using the actual output per hour series as the denominator, rather than the trend series, results in a higher percentage gap. This is due to the actual series being lower than the trend series post-downturn.

4. Output per hour up in both services and manufacturing, compared with a year ago

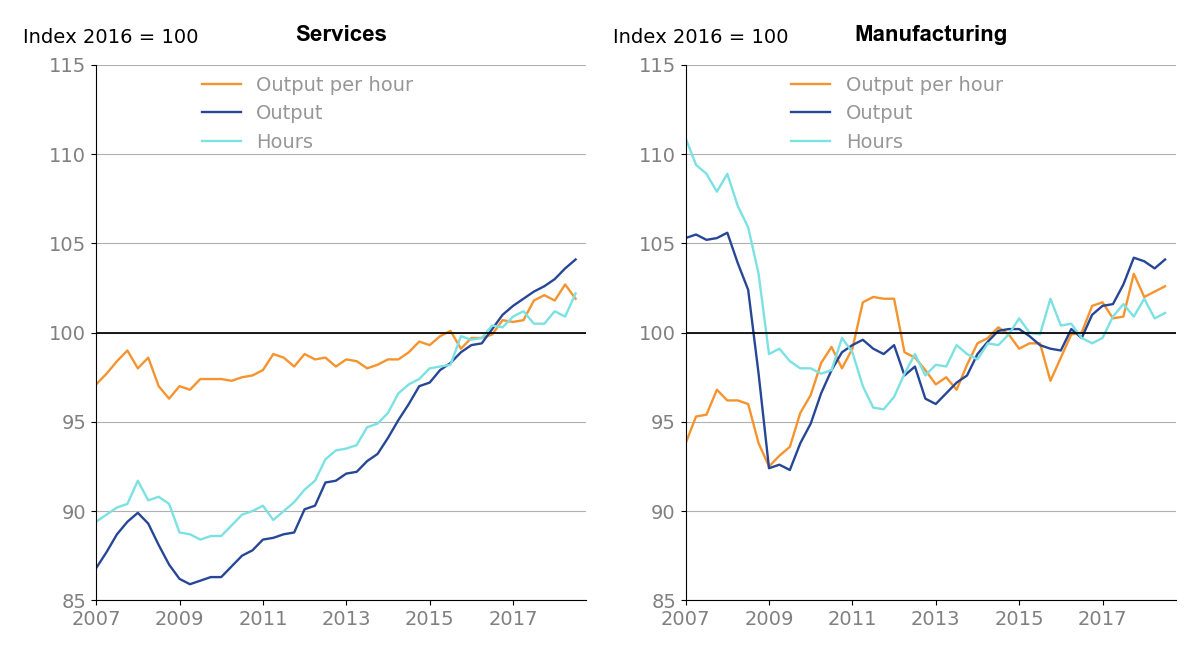

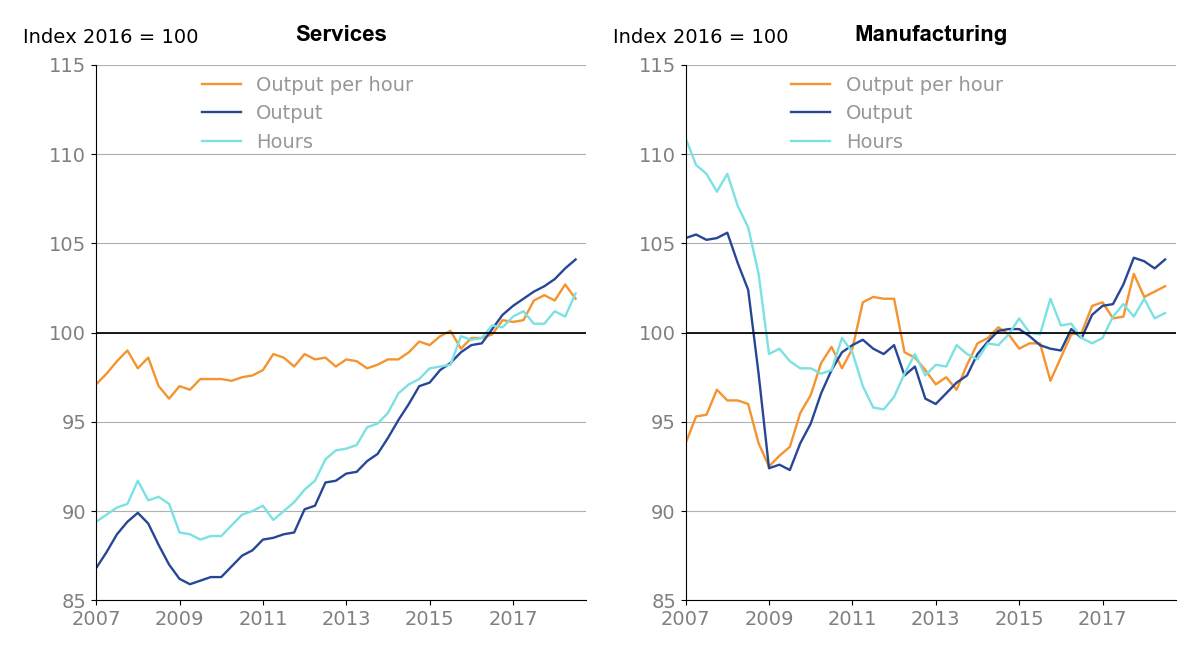

Services output per hour, compared with the same period a year ago, increased by 0.1% in the latest quarter (Quarter 3 (July to Sept) 2018), with output increasing slightly faster than hours worked. In manufacturing over the year labour productivity increased by 1.7%, because output grew while hours worked decreased. Compared with the previous quarter, output per hour in services decreased by 0.7% while manufacturing output per hour increased by 0.3%.

Figure 3 shows longer-term trends for output per hour and its components since Quarter 1 (Jan to Mar) 2007. Services are represented in the left-hand panel, while manufacturing is represented in the right. Manufacturing output per hour has been more volatile than services in recent years. This reflects a degree of divergence in manufacturing between gross value added (GVA) and hours, most noticeable in 2009 and between 2011 to 2012, whereas in services, GVA and hours follow fairly similar trends.

Figure 3: Components of services and manufacturing productivity measures

Seasonally adjusted, UK, Quarter 1 (Jan to Mar) 2007 to Quarter 3 (July to Sept) 2018, UK

Source: Office for National Statistics

Download this image Figure 3: Components of services and manufacturing productivity measures

.png (90.6 kB) .xls (23.0 kB){kind=link}

5. Unit labour costs grow for the fourteenth consecutive quarter

Unit labour costs (ULCs) reflect the full labour costs, including social security and employers’ pension contributions, incurred in the production of a unit of economic output. Changes in labour costs are a large factor in overall changes in the cost of production. If increased costs are not reflected in increased output, for instance, this can put upward pressure on the prices of goods and services – sometimes referred to as “inflationary pressure”. ULCs grew by 2.8% in the year to Quarter 3 (July to Sept) 2018, reflecting a larger percentage increase in labour costs per hour than output per hour, although this growth level has been fairly consistent over the last three years, as shown in Figure 4.

Figure 4 shows changes in ULCs since Quarter 1 (Jan to Mar) 2008 compared with the same quarter a year earlier. Holding other factors constant, increasing output per hour reduces ULCs as total labour costs remain constant while output rises. As a result, output per hour has its sign reversed in Figure 4. In this presentation, positive output per hour growth has a negative effect on ULC growth, while negative output per hour growth has a positive effect on ULC growth.

While growth in ULCs has been broadly positive since the onset of the economic downturn, averaging around 1.5% since Quarter 1 2008, there has been substantial variation during this period. During the recent economic downturn, ULCs began to grow at a relatively high rate, reaching a peak of 6.3% by the end of the downturn in Quarter 2 (Apr to June) 2009 and remaining elevated until Quarter 1 2010. Figure 4 shows that the initial increase in ULC growth during the downturn was driven by falling output per hour, but from Quarter 2 2009 onwards, increasing labour costs per hour were the driving factor. Following the downturn, growth in ULCs began to slow, eventually becoming negative in Quarter 2 2010.

Following a period of low or negative growth, ULC growth has fluctuated around 2% for the past two years. This increase broadly reflects higher hourly labour cost growth, with relatively little offsetting output per hour growth.

Figure 4: Whole economy unit labour costs and their compositions, growth on quarter a year ago

Seasonally Adjusted, UK, Quarter 1 (Jan to Mar) 2008 to Quarter 3 (July to Sept) 2018

Source: Office for National Statistics

Notes:

Labour costs per hour estimates will differ from those in our Index of Labour Costs per Hour bulletin, due to differences in methodology.

Output per hour has its sign reversed in Figure 4. In this presentation, positive output per hour growth has a negative effect on ULC growth, while negative output per hour growth has a positive effect on ULC growth.

Download this chart Figure 4: Whole economy unit labour costs and their compositions, growth on quarter a year ago

Image .csv .xls6. Experimental sectional unit labour costs

In November 2012, we introduced a dataset of sectional unit labour costs. These experimental statistics provide estimates of sectional unit labour costs, returns to self-employed workers, the labour share of mixed income and the total value of labour costs. Although the methodology employed differs from the National Statistics estimates presented in this release, the datasets have been welcomed by users and we plan to incorporate a more regular section in the labour productivity statistical bulletin. We are also working in co-operation with the UK Statistics Authority to badge these datasets as National Statistics. For more information on the methodology of these experimental statistics, please see this article.

ULC increased 2.9% compared with the same quarter a year ago, with production recording the largest increase in ULC of 4.1%. This is the highest quarter on year growth for production industries since Quarter 3 (July to Sept) 2013. The latest growth in unit labour costs for the production industries was due to a weak output growth of 0.7% and a stronger growth in wages and salaries, the latter reflecting a strong growth in nominal average weekly earnings (including bonuses). This was also seen in manufacturing and services. During the past three years sectional unit labour costs for the whole economy have averaged 2.1%, with production, manufacturing and services averaging slightly higher during the same period, 2.8%, 2.3% and 2.2% respectively. The whole economy measure is lower than the industries because of the allocation effect – as labour and other inputs are moving towards lower productivity industries. Therefore, despite each sector evidencing growth, the overall effect on the whole economy is weaker than that of the parts.

Figure 5 shows the annual average cumulative growth in sectional unit labour costs over the last three years (since Quarter 3 2015), for the whole economy, manufacturing, production and services.

Figure 5: Average annual cumulative growth in sectional unit labour costs

Quarter 3 (July to Sept) 2015 to Quarter 3 (July to Sept) 2018, UK

Source: Office for National Statistics

Notes:

- Section Unit Labour costs per hour estimates will differ from the National Statistics Unit Labour Costs, due to differences in methodology.

Download this chart Figure 5: Average annual cumulative growth in sectional unit labour costs

Image .csv .xls7. Productivity by region

In 2017, productivity measured in output per hour varied significantly across the regions with London and the South East being 30.4% and 7.1% respectively above the UK, while Wales and Northern Ireland were 16.2% and 15.9% below the UK.

Output per job also varied across the regions with London and the South East being 39.2% and 5.1% higher than the UK, while Wales and the East Midlands, were 18% and 14.7%, below the UK.

Figure 6 shows output per hour by region compared with the UK.

Figure 6: Output per hour by region

Nominal GVA per unit of labour, 2016 and 2017

Source: Office for National Statistics

Download this chart Figure 6: Output per hour by region

Image .csv .xls9. What’s changed in this release?

Revisions

This release reflects revisions to gross value added and income data resulting from quarterly national accounts, affecting time periods since 2017. Revisions to jobs data resulting from an annual benchmarking to the Business Register and Employment Survey, as well as revisions to public sector employment estimates, affect hours and jobs in all time periods. Revisions to regional productivity estimates resulting from regional gross value added statistics, affect periods since 2017. Revisions resulting from seasonal adjustment affect all periods, where seasonal adjustment is applied.

Commentary on experimental unit labour costs by industry sections

The bulletin introduces commentary on unit labour costs by industry sections comparing growth rates over the past three years.

Commentary on relative productivity for regions and nations within the UK

The bulletin introduces commentary on productivity for regions introducing the 2017 estimates for output per hour and output per job by NUTS1 regions.

In this release we will not be presenting the experimental industry by region productivity statistics. We have moved the publication of these datasets to 6 February 2019 to coincide with the Regional and sub-regional productivity in the UK: February 2019 release.

Back to table of contents10. Quality and methodology

The measure of output used in these statistics is the chained volume (real) measure of gross value added (GVA) at basic prices, with the exception of the regional analysis in Table 9, where the output measure is nominal GVA (NGVA), using the income approach. These measures differ because NGVA is not adjusted to account for price changes; this means that if prices were to rise more quickly in one region than the others, then the measures of productivity for that region could show relative growth in productivity compared with other regions purely as a result of the price changes.

Labour input measures used in this bulletin are known as “productivity jobs” and “productivity hours”. Productivity jobs differ from the workforce jobs (WFJ) estimates, published in Table 6 of our Labour market statistical bulletin, in three ways:

to achieve consistency with the measurement of GVA, the employee component of productivity jobs is derived on a reporting unit basis, whereas the employee component of the WFJ estimates is on a local unit basis

productivity jobs are scaled so industries sum to total Labour Force Survey (LFS) jobs – note that this constraint is applied in non-seasonally adjusted terms; the nature of the seasonal adjustment process means that the sum of seasonally adjusted productivity jobs and hours by industry can differ slightly from the seasonally adjusted LFS totals

productivity jobs are calendar quarter average estimates, whereas WFJ estimates are provided for the last month of each quarter

Productivity hours are derived by multiplying employee and self-employed jobs at an industry level (before seasonal adjustment) by average actual hours worked from the LFS at an industry level. Results are scaled so industries sum to total unadjusted LFS hours and then seasonally adjusted. Labour productivity is then derived using growth rates for GVA and labour inputs in line with the following equation:

Industry estimates of average hours derived in this process differ from published estimates (found in Table HOUR03 in the Labour market statistics release), as the HOUR03 estimates are calculated by allocating all hours worked to the industry of main employment, whereas the productivity hours system takes account of hours worked in first and second jobs by industry.

Whole-economy unit labour costs (ULCs) are calculated as the ratio of total labour costs (that is, the product of labour input and costs per unit of labour) to GVA. Further detail on the methodology can be found in Revised methodology for unit wage costs and unit labour costs: explanation and impact.

The equation for growth of ULCs can be calculated as:

Manufacturing unit wage costs are calculated as the ratio of manufacturing average weekly earnings to manufacturing output per filled job. On 28 November 2012 we published Productivity measures: sectional unit labour costs, describing new measures of ULCs below the whole-economy level and proposing to replace the currently published series for manufacturing unit wage costs with a broader and more consistent measure of ULCs. A research note, Sources of revisions to labour productivity estimates, is available and further commentary on the nature and sources of the revisions introduced in this quarter is available in the UK productivity bulletin – introduction.

The Labour productivity Quality and Methodology Information report contains important information on:

the strengths and limitations of the data and how it compares with related data

uses and users of the data

how the output was created

the quality of the output including accuracy of the data