1. Background

In the Labour Force Survey (LFS) respondents are interviewed for five consecutive quarters over a 12- month period, with 20% of the sample being replaced at each quarter. This allows for a longitudinal dataset to be created over a limited time interval, where respondents’ characteristics can be tracked over their time in the survey.

We publish population-weighted longitudinal datasets for each calendar quarter. These are available for each quarter since 1997 and can be used to analyse changes in labour market characteristics over two or five quarters. The datasets include "flow" variables, which estimate the size of the movements between the three main labour market statuses of employment, unemployment and economic inactivity.

Monitoring changes in the labour market status of respondents to the LFS aids the understanding of the quarterly changes in the levels of employment, unemployment and economic inactivity. These indicators are published as stocks for a given period, with changes expressed as the difference between successive quarters. These quarterly comparisons represent the net changes between the three labour market statuses. The underlying gross flows are usually considerably larger and may not correspond with those implied by the net changes. Estimates of the gross flows between the statuses can be derived from the LFS longitudinal datasets and are summarised in this article.

Back to table of contents2. Method

There are two types of Labour Force Survey (LFS) longitudinal datasets: two-quarter and five-quarter. These are weighted using the same population estimates as those used in the main quarterly LFS datasets, although the weighting methodology differs (see technical note). Consequently, the estimates are broadly consistent with the published aggregates, but not entirely. Also, the datasets are limited to people aged 16 to 64 years.

Both types of dataset contain a flow variable with 11 categories, with all combinations of employment, unemployment and economic inactivity accounted for, plus two categories for those entering and leaving the 16 to 64 population over the quarter. For the purpose of this analysis, those entering or leaving this population are excluded from the measured sample. The stock of the employed, unemployed and inactive at each quarter can therefore be estimated by summing the corresponding flow categories.

For this analysis, the two-quarter datasets have been used to gain some insight into the quarterly changes in the headline published aggregates.

Back to table of contents3. The charts provided

The charts in this article show the estimated gross flows, that is, the total inflow or outflow for aged 16 to 64 employment, unemployment and inactivity from one calendar quarter to the next. They are seasonally adjusted. Analysis of the net flows, that is, the difference between the total inflow and outflow, are also included and these are compared with the quarterly changes in the published aggregates, partly to give an indication of the robustness of the flows analysis.

Back to table of contents4. Main points for Quarter 3 (July to Sept) 2017:

the gross flow into employment has decreased for two consecutive quarters

the flow from unemployment into employment is at its lowest since 2008; however, the proportion of people flowing from unemployment to employment (as shown by the hazard rates) is higher than a year ago

the inactivity net flow is positive for the first time since 2010

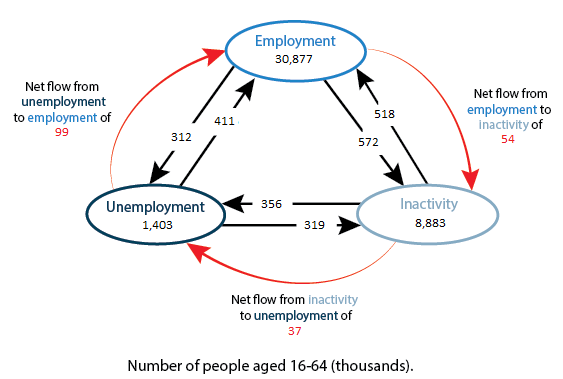

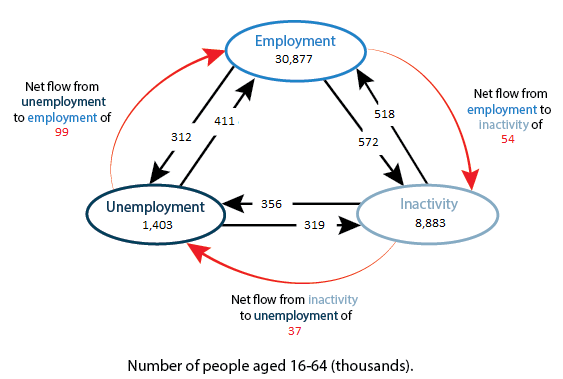

5. Quarterly gross flows

The diagram shows the gross flow between each economic status between Quarter 2 (Apr to June) 2017 and Quarter 3 (July to Sept) 2017. The stocks for each status represent the latter period and are the seasonally adjusted aggregates for people aged 16 to 64 years.

Figure 1: Quarterly flows, UK, seasonally adjusted

April to June 2017 to July to September 2017

Source: Office for National Statistics

Download this image Figure 1: Quarterly flows, UK, seasonally adjusted

.png (34.7 kB){kind=link}

6. Unemployment

Figure 2 shows the gross flow to unemployment has increased slightly in the latest quarter, driven by an increase in the flow from employment to unemployment, which more than offset the fall in the flow from inactivity to unemployment.

Figure 2: Inflow to unemployment, seasonally adjusted (aged 16 to 64), UK

Source: Office for National Statistics

Download this chart Figure 2: Inflow to unemployment, seasonally adjusted (aged 16 to 64), UK

Image .csv .xlsThe unemployment gross outflow has decreased slightly as the decrease in the flow from unemployment to employment has more than offset the increase in the flow from unemployment to inactivity.

Figure 3: Outflow from unemployment, seasonally adjusted (aged 16 to 64), UK

Source: Office for National Statistics

Download this chart Figure 3: Outflow from unemployment, seasonally adjusted (aged 16 to 64), UK

Image .csv .xlsFigure 4 shows that both the unemployment net quarterly flow and the unemployment quarterly change in stock have increased in Quarter 3 (July to Sept) 2017, following decreases in two consecutive quarters. However, both the net flow and the quarterly change remain negative.

Figure 4: Unemployment: net flow versus change in stock, seasonally adjusted (aged 16 to 64), UK

Source: Office for National Statistics

Download this chart Figure 4: Unemployment: net flow versus change in stock, seasonally adjusted (aged 16 to 64), UK

Image .csv .xls7. Employment

The flow from unemployment to employment has decreased to its lowest since Quarter 3 (July to Sept) 2008 which, together with a decrease in the flow from inactivity to employment, has led to a decrease in the employment gross inflow.

Figure 5: Inflow to employment, seasonally adjusted (aged 16 to 64), UK

July to September 2012 to July to September 2017

Source: Office for National Statistics

Download this chart Figure 5: Inflow to employment, seasonally adjusted (aged 16 to 64), UK

Image .csv .xlsIncreases in the flows from employment to unemployment and inactivity have caused the employment gross outflow to increase, after decreasing for three consecutive quarters.

Figure 6: Outflow from employment, seasonally adjusted (aged 16 to 64), UK

July to September 2012 to July to September 2017

Source: Office for National Statistics

Download this chart Figure 6: Outflow from employment, seasonally adjusted (aged 16 to 64), UK

Image .csv .xlsFigure 7 shows that the job-to-job flow in Quarter 3 (July to Sept) 2017 is broadly stable when compared with Quarter 2 (Apr to June) 2017.

Figure 7: Job-to-job flow rate, seasonally adjusted (aged 16 to 69), UK

July to September 2003 to July to September 2017

Source: Office for National Statistics

Download this chart Figure 7: Job-to-job flow rate, seasonally adjusted (aged 16 to 69), UK

Image .csv .xlsFigure 8 shows that both the employment net flow and the employment quarterly change in stock have decreased, with the quarterly stock becoming negative for the first time since Quarter 1 (Jan to Mar) 2013.

Figure 8: Employment: net flows versus change in stock, seasonally adjusted (aged 16 to 64), UK

July to September 2012 to July to September 2017

Source: Office for National Statistics

Download this chart Figure 8: Employment: net flows versus change in stock, seasonally adjusted (aged 16 to 64), UK

Image .csv .xls8. Inactivity

Figure 9 shows that the gross inflow to inactivity has increased as a result of increases in both the flows from unemployment and employment.

Figure 9: Inflow to inactivity, seasonally adjusted (aged 16 to 64), UK

July to September 2012 to July to September 2017

Source: Office for National Statistics

Download this chart Figure 9: Inflow to inactivity, seasonally adjusted (aged 16 to 64), UK

Image .csv .xlsFigure 10 shows that the gross outflow from inactivity has fallen for a second consecutive quarter. This is driven by falls in the flows from inactivity to unemployment and employment.

Figure 10: Outflow from inactivity, seasonally adjusted (aged 16 to 64), UK

July to September 2012 to July to September 2017

Source: Office for National Statistics

Download this chart Figure 10: Outflow from inactivity, seasonally adjusted (aged 16 to 64), UK

Image .csv .xlsFigure 11 shows that both the inactivity net flow and the inactivity quarterly change in stock have become positive. In addition, the inactivity net flow is at its highest since Quarter 4 (Oct to Dec) 2010.

Figure 11: Inactivity: net flow vs change in stock, seasonally adjusted (aged 16 to 64), UK

July to September 2012 to July to September 2017

Source: Office for National Statistics

Download this chart Figure 11: Inactivity: net flow vs change in stock, seasonally adjusted (aged 16 to 64), UK

Image .csv .xls9. Technical note

There are differences between the data used for the published Labour Force Survey (LFS) aggregate estimates and the longitudinal data used to estimate the gross flows.

Flows are currently adjusted for non-response bias through special calibration weights in the longitudinal datasets. These aim to account for the propensity of certain types of people to drop out of the LFS between one quarter and the next. For example, housing tenure features in the weighting of the longitudinal data because, historically, households in rented accommodation have been more likely to drop out of the survey than owner-occupiers.

There is some evidence that the longitudinal datasets are affected slightly by response error, which causes a slight upward bias in the estimates of the gross flows. For example, if it was erroneously reported that someone had moved from unemployment to employment then, in addition to the outflow from unemployment being overestimated, so would the inflow to employment. In the main quarterly LFS dataset, any such misreporting errors tend to cancel each other out.

The differences in the net flows for inactivity shown in Figure 11 are mainly the result of excluding the entrants to, and leavers from, the population in the flows estimates contained in this piece of analysis. This effect is normally one that increases the number of people who enter inactivity. This is because the increase in inactivity from those people turning 16 years old is greater than those leaving inactivity due to becoming 65 years old.

The stocks derived from the longitudinal datasets differ from those obtained from the quarterly LFS datasets due to being based on a subset of the main LFS sample. The restriction to measuring only those who are commonly aged 16 to 64 years across successive quarters discounts those entering or leaving the population and also those over 64 years old. All such people are accounted for in the headline LFS aggregates.

There has been a revision in the seasonally adjusted job-to-job estimate for Quarter 2 (Apr to June) 2017.

Back to table of contents10. References

Jenkins J and Chandler M (2010) Labour market gross flows data from the Labour Force Survey. Economic and Labour Market Review, February 2010.

Back to table of contents