Table of contents

1. Main points

The unemployment rate was 4.3% in the three months to August 2017, the joint lowest since 1975.

There were 94,000 more people in work compared with the three months to May 2017, out of which 78,000 were women.

The inactivity rate was 21.4%, down slightly when compared with the previous three months.

In real terms, average weekly earnings fell by 0.4% on the previous year (excluding bonuses) and by 0.3% (including bonuses).

In the three months to June 2017 (the latest available period), the probability of remaining in employment, for those in work, was 97.3%, the highest comparable rate since 1997.

2. Main labour market indicators

UK unemployment rate remains at its lowest since 1975

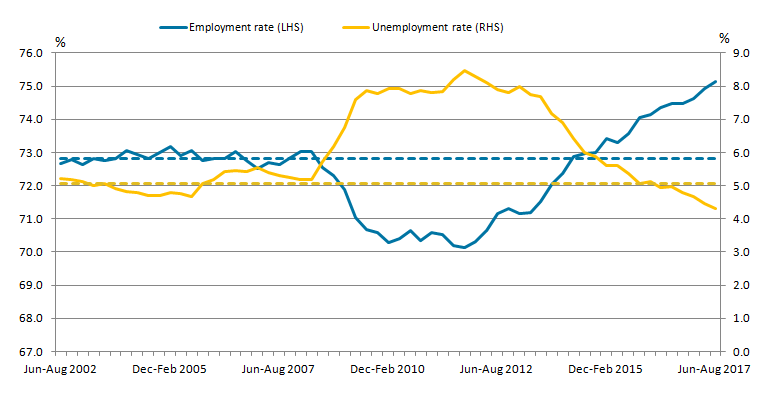

Latest estimates from the Labour Force Survey show that the UK unemployment rate declined by 0.2 percentage points to 4.3% in the three months to August 2017 compared with three months ago. The employment rate increased by 0.2 percentage points to 75.1% in the three months to August 2017 compared with three months ago. Figure 1 shows that the latest period during which the employment rate matched the pre-economic downturn average of 72.8% was May to July 2014, and since then the employment rate has been outperforming its pre-downturn average. The unemployment rate has been outperforming its pre-economic downturn average of 5.1% since February to April 2016.

Figure 1: Employment and unemployment rate

UK, seasonally adjusted, June to August 2002 to June to August 2017

Source: Source: Office for National Statistics, Labour Force Survey

Notes:

- Dashed lines indicate pre-crisis average between June to August 2002 and June to August 2007

Download this image Figure 1: Employment and unemployment rate

.png (22.7 kB) .xlsx (12.1 kB){kind=link}

The number of people in work increased by 94,000 in the three months to August 2017 compared with three months ago. In the three months to August 2017 there were 78,000 more women in employment compared with three months ago. Full-time employment increased by 25,000 to 23.56 million in the three months to August 2017 compared with the previous quarter, whereas part-time employment increased by 69,000 to 8.55 million over the same period. An increase in the total employment level was accompanied by a decrease in the total unemployment level by 52,000 in the three months to August 2017 when compared with the previous quarter.

In the three months to August 2017 the number of self-employed workers increased by 57,000 to reach a record high level of 4.86 million, whereas the number of employees increased by 39,000. However, recent trends in full-time and part-time working for the self-employed show different patterns. In the three months to August 2017 the number of self-employed people working full time decreased by 0.4% on the quarter, whereas the number of self-employed working part-time increased by 5.1% on the quarter.

Table 1: Unemployment rate by age category UK, seasonally adjusted, June to August 2017

| Unemployment rate (%) | Change on year (percentage points) | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Aged 16 and Over | 4.3 | -0.7 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Aged 16-17 | 22.3 | -5.3 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Aged 18-24 | 10.8 | -1.3 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Aged 25-34 | 3.8 | -0.7 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Aged 35-49 | 2.9 | -0.5 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Aged 50-64 | 3.1 | -0.4 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Source: Office for National Statistics, Labour Force Survey | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Notes: | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 1. 16 and over age category represents the headline UK unemployment rate. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Download this table Table 1: Unemployment rate by age category UK, seasonally adjusted, June to August 2017

.xls (28.7 kB)Table 1 shows unemployment rates for different age groups and headline unemployment rate (aged 16 and over) in the three months to August 2017, as well as the change in unemployment rates on the previous year. By age category, two age groups, 35 to 49 and 50 to 64, had the lowest unemployment rates. However, it is the two younger age groups, 16 to 17 and 18 to 24, that have seen the largest decline in the unemployment rate in the three months to August 2017 compared with the same period a year ago (Table 1).

In the three months to August 2017, the inactivity rate declined marginally to 21.4% when compared with the previous quarter. The inactivity level for those aged 16 to 64 decreased by 17,000 on the quarter to 8.81 million, driven by fall in economic inactivity amongst three older age groups: 25 to 34, 35 to 49 and 50 to 64. Average weekly hours for full-time workers remained at 37.5 hours, whereas average weekly hours for part-time workers increased slightly (by 0.2 hours) to 16.3 hours in the three months to August 2017 compared with the previous quarter. Out of all people in employment, 72.1% worked 31 hours or more as their usual weekly hours in the three months to August 2017. However, this proportion varies substantially for men and women. In the three months to August 2017, of all men in employment, 85.6% worked 31 hours or more compared with 56.9% of all women in employment.

The number of vacancies increased by 0.4% to 783,000 in the three months to September 2017 compared with the previous quarter. In the three months to September 2017 there was a 0.6% increase in vacancies in the service sector.

Figure 2: Regular average weekly earnings growth, real and nominal

Great Britain, seasonally adjusted, three month on three month a year ago, August 2006 to August 2017

Source: Office for National Statistics, Monthly Wages and Salaries Survey

Notes:

- CPIH is the rate of Consumer Prices Index inflation including owner occupiers’ housing costs. It is shown as negative here to demonstrate the impact it has on real wages

Download this chart Figure 2: Regular average weekly earnings growth, real and nominal

Image .csv .xlsNominal average weekly earnings for employees in Great Britain increased by 2.2% including bonuses in August 2017, and by 2.1% excluding bonuses compared with a year earlier. In real terms, average weekly earnings fell by 0.4% on the previous year (excluding bonuses) and by 0.3% (including bonuses). The recent fall (since the three months to March 2017) in real wages is due to higher rates of inflation, which has outpaced nominal wage growth.

In February 2017, the annual rate of Consumer Prices Index including owner occupiers’ housing costs (CPIH) inflation rose above 2.0% and increased to 2.7% in August 2017. From October 2013 to February 2017, the annual rate of CPIH inflation was not higher than 2.0% and real wage growth reached a peak of 2.6% in July 2015 (Figure 2).

Labour disputes data show that the number of stoppages as well as workers involved in those stoppages as a cumulative total in the 12 months to August 2017 were 80 and 47,000 respectively. This is lower than the 12 months to 2016 where the cumulative total number of stoppages and workers involved was 107 and 151,000 respectively.

Back to table of contents3. Labour Market Flows

The numbers of people in employment, unemployed and economically inactive in the UK show relatively small changes from quarter to quarter. However, these changes are the net effect of large numbers of people moving between different labour force categories, most notably the three economic activity groupings of employment, unemployment and inactivity. Labour market flows data complement changes in headline levels of employment, unemployment and inactivity, and help to explain trends in these three statuses. Gross flows are the total number of people moving, for example, from employment to unemployment, or inactivity, and the total number of people who move in the opposite direction. In total there are nine different flow categories for the three economic activity groupings, with another two being those individuals entering or leaving working age.

This section of the article uses two-quarter longitudinal data back to 2001, which is the first point at which consistently weighted time series are available. For analysis of the longitudinal datasets, the stock of the employed, unemployed and inactive at each quarter need to be obtained by summing the three corresponding flow categories. For example, employed is given by summing those employed at both quarters, those who move from unemployment to employment and those moving from inactivity to employment. It should be noted that the stocks derived from the longitudinal dataset differ slightly to those obtained from a quarterly cross-sectional dataset and published figures due to attrition and also because those who are entering or leaving working age are excluded.

Figure 3: Quarterley flows across UK labour market

UK, seasonally adjusted, January to April to June 2017

Embed code

Figure 3 shows estimated gross flows, that is, the total inflow or outflow for working-age employment, unemployment and inactivity from one calendar quarter to the next. The period covers January to March 2017 (Quarter 1) and April to June 2017 (Quarter 2). Approximately 3.22 million people move across the labour market either by moving from one pool to another or changing employment every quarter. More people left inactivity (937,000) than any other stock. The number of people who moved from inactivity to employment was 540,000. This was higher than those who moved from unemployment to employment, which was 439,000. Comparing these gross flows with the published quarterly changes in the headline Labour Force Survey aggregates reveals how substantial the underlying movements hidden behind these values are.

Figure 4: Comparison of four-quarter moving average of flows as a percentage of working age population

UK, seasonally adjusted, April to June 2003 to April to June 2017

Source: Office for National Statistics, Labour Force Survey

Notes:

1.We use a four-quarter moving average to adjust for volatility in the series.

Download this chart Figure 4: Comparison of four-quarter moving average of flows as a percentage of working age population

Image .csv .xlsFigure 4 compares four-quarter moving average flows as a percentage of working-age population since April to June 2003 with the latest available period (April to June 2017). In the three months to June 2017, on average 459,000 people (1.12% of the working age population) moved from unemployment to employment every three months, whereas 290,000 people (0.70% of working age population) moved from employment to unemployment, the lowest since the earliest comparable period in 2001. Flows from employment to unemployment as a four-quarter moving average have been falling since July to September 2016. This means that not only are there more people in work (higher employment levels) as per published Labour Force Survey indicators, but on average a record low level of employed people are transiting into the unemployed category.

In the three months to June 2017, on average 544,000 people (1.32% of the working population) moved from inactivity to employment every quarter, whereas on average 567,000 people (1.38% of the working population) every quarter moved in the other direction – from employment to inactivity (Figure 4). The gross outflow from employment was 797,000 in the three months to June 2017; this is lower when compared with the same period in 2015, which was 901,000. In fact, this gross outflow from employment is at its lowest since the three months to March 2006. Recently, the flows from employment to unemployment and vice versa have fallen by a larger proportion compared with the other flows (Figure 4).

In contrast, Figure 4 shows that there was a notable rise in the flow from employment to unemployment during the most recent economic downturn. This is because in economic downturns, as the labour market gets looser, there are more movements between the statuses. The unemployment pool is most affected as more of the unemployed find a job or stop searching for one. Also, more of the inactive population may start looking for a job and more workers lose theirs. In other words, gross flows in and out of the three pools appear countercyclical1. In expansions, as the labour market becomes tighter, there are fewer movements between these three statuses, whereas in economic downturns, there are more movements between the statuses.

Figure 5: Contributions to net inflows to employment, from inactivity and unemployment

UK, seasonally adjusted, Quarter 2 (Apr to Jun) 2002 to Quarter 2 (April to June) 2017

Source: Office for National Statistics, Labour Force Survey

Download this chart Figure 5: Contributions to net inflows to employment, from inactivity and unemployment

Image .csv .xlsIn the latest available period (April to June 2017), the net inflow into employment was 182,000 whereas the net contributions from unemployment to employment and from inactivity to employment were 176,000 and 6,000 respectively (Figure 5). Net inflows from unemployment to employment are the largest contributor to the overall net inflows into employment. However, net inflows from inactivity to employment turned positive in the three months to June 2017 after being negative for the five previous consecutive quarters. The net inflows from inactivity to employment have been higher in recent years than the long-run average.

Figure 6: Outflows from inactivity, to employment and unemployment

UK, seasonally adjusted, Quarter 2 (Apr to Jun) 2002 to Quarter 2 (April to June) 2017

Source: Office for National Statistics, Labour Force Survey

Download this chart Figure 6: Outflows from inactivity, to employment and unemployment

Image .csv .xlsFigure 6 shows outflows from inactivity to employment and unemployment. Net outflows from inactivity have been largely positive and represent the largest net outflows when compared with the other three stocks. In the three months to June 2017, the net outflow from inactivity was 107,000, which is higher than the net outflow from unemployment (75,000). When compared with a net inflow to employment, which was 182,000 during the same period, it seems that employment is the only stock where inflows are greater than outflows. This pattern coincides with the overall recent trend in the labour market where employment has been rising and unemployment and inactivity have been falling.

Consistent with an unemployment rate at a generational low, and record high economic activity rate, the flows data show an increase in the number of people moving from inactivity directly to employment. However, the outflows from inactivity to unemployment have been driving the overall outflow from inactivity. The net outflows from inactivity were negative during Quarter 1 (Jan to Mar) 2007 and Quarter 2 (Apr to June) 2009. This was mainly due to sharp falls in the net outflow from inactivity to employment during these two periods, which dragged down the overall net outflows from inactivity.

Labour market flows do not capture the full extent to which someone who is of working age is likely to change their economic status. Hazard rates are the transition probabilities that imply the relative likelihood of someone changing status or remaining in the same category. Table 2 shows hazard rates for separations (movement from employment to unemployment) and hiring, job moves expressed in thousands, for the latest available period (April to June 2017), as well as their respective correlation with the unemployment rate.

Table 2: Job moves and correlation with unemployment rate UK, seasonally adjusted, April to June 2017

| UK, seasonally adjusted, April to June 2017 | |||

|---|---|---|---|

| Job moves (thousands) | Hazard rate (%) | Correlation with unemployment rate¹ | |

| Total job-to job- moves | 748 | -.769** | |

| Separations (Employment to unemployment) | 263 | 0.9 | .688** |

| Hiring (Unemployment to employment) | 439 | 28.7 | -.836** |

| Resignations | 287 | -.839** | |

| Retired or gave up work | 16 | -.495** | |

| Other Reasons | 388 | -.546** | |

| **. Correlation is significant at the 0.01 level (2-tailed). | |||

| Notes: | |||

| 1. Correlation coefficient is based on the earliest available data for hazard rates and flows respectively. | |||

| 2. Correlations for separations and hiring are based on hazard rates. | |||

Download this table Table 2: Job moves and correlation with unemployment rate UK, seasonally adjusted, April to June 2017

.xls (28.2 kB)Table 2 indicates that in the three months to June 2017, the probability of separation (a move from employment to unemployment) for people in employment was 0.9%, whereas for those in unemployment the probability of being hired was 28.7%. The hazard rate for hiring was higher than for any other flow. The hazard rate for remaining in the same status was 97.3% for employment (highest since the earliest available period in 1997), and 88.1% for inactivity in the three months to June 2017. For unemployment this was much lower at 52.7%. The correlations with unemployment rate (column three, Table 2) imply that separations are countercyclical and job hiring is procyclical2. The correlation coefficient for resignations is similar to hiring, which highlights that resignations also seem to follow trends in economic cycles.

The overall trend in job-to-job moves has been procyclical. The number of job-to-job moves fell sharply following the economic downturn in 2008. However, this has been gradually rising post-crisis to a four-quarter average of 779,000 in the three months to June 2017. Out of these job-to-job moves, on average 40% (312,000) of people moved to high-skilled jobs compared with 32% (246,000) who moved to low-skilled jobs during the same period. Furthermore, out of those who moved jobs, on average 40% (310,000) moved from high-skilled jobs compared with 33% (259,000) who moved from low-skilled jobs. This implies that those in high-skilled jobs are more mobile within the employment pool.

Overall, Table 2 shows that the separations rate (from employment to unemployment) appears countercyclical, whereas job-to-job moves, hiring, resignations, retirements and giving up work appear procyclical. In other words, recessions are periods when it is harder for an unemployed individual to find a job, an employed person is more likely to lose their job, an employed person is less likely to change jobs and is less likely to resign or give up their work. Transition probabilities between employment and inactivity do not seem to have a cyclical component.

Notes for: Labour Market Flows

- Inversely correlated with economic cycles and the overall state of the economy.

- Positively correlated with economic cycles and the overall state of the economy.